-

Our crazy trading strategy racking us hella points

Inspiration

This project was inspired by a book I read called Python for Finance where I learned how to apply financial concepts using Python.

What it does

It parses a context either in natural language or structured input and decides the ticker that an investor should invest in along with their risk index. The price data for these tickers are then ran through an efficient frontier optimization algorithm that allocates the appropriate weights for each of these tickers.

How we built it

The context is passed to Google Gemini Flash to do NLP and determine the tickers and risk index. The price data is queried from a local PostgreSQL with Timescaledb extension that holds data from yfinance. Then, a optimization algorithm is ran to determine the appropriate weights for each asset.

Challenges we ran into

The prior model we used, qwen 2.5, was not giving appropriate tickers and disregarded the context so we had to switch to Google Gemini Flash which supercharged our strategy. We also had trouble parsing input strings to JSON but this was solved with regex.

Accomplishments that we're proud of

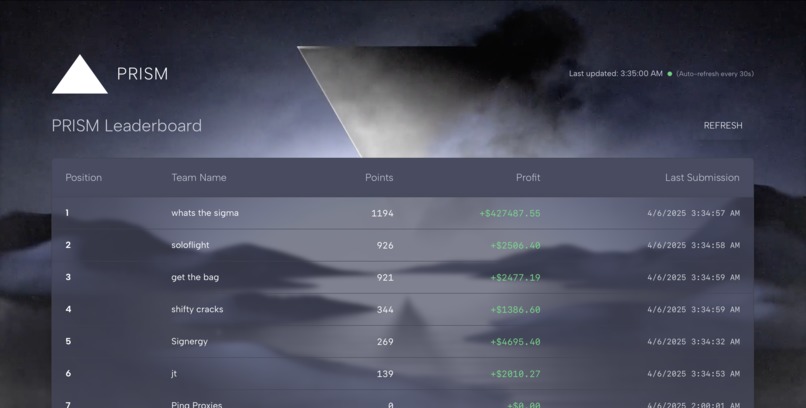

We managed to make 7 figure profits and rank high in multiple rounds despite being a late joiner. Other teams and the organizers learned quickly about us when we started trading in round 3. Our team spearheaded some of the rounds.

What we learned

We learned how to optimize portfolio risk management and create different investment portfolios for people with different backgrounds as well as low-latency programming to continuously query the API and submit to gain points.

What's next for whats the sigma

We are going to dominate the financial markets and day trade our way to success

Built With

- gemini

- numpy

- pandas

- postgresql

- python

- timescaledb

Log in or sign up for Devpost to join the conversation.