-

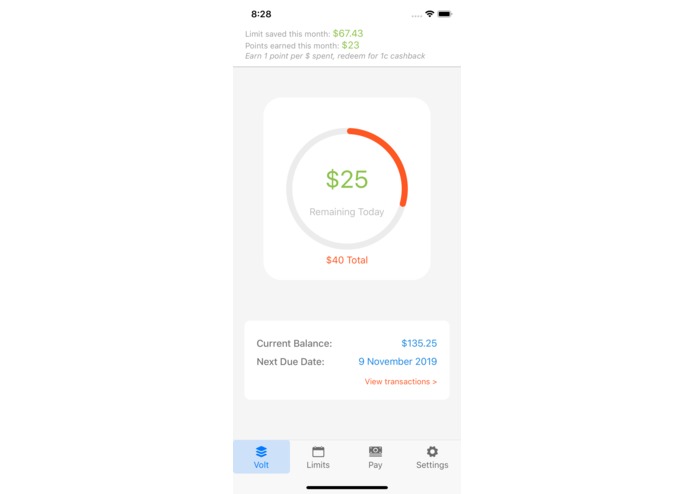

Volt - Dashboard

-

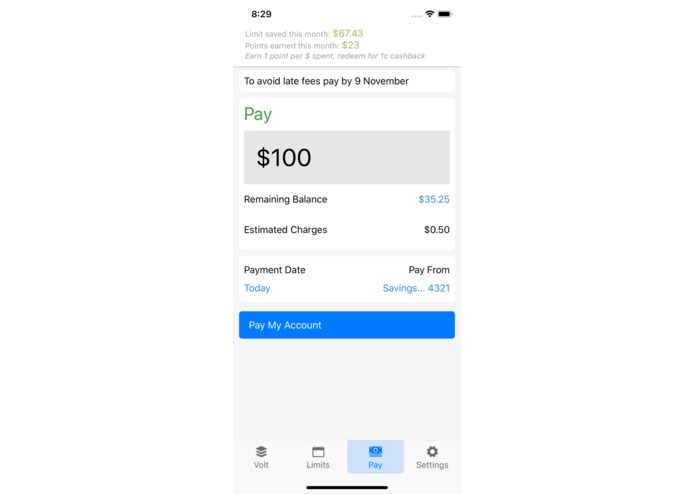

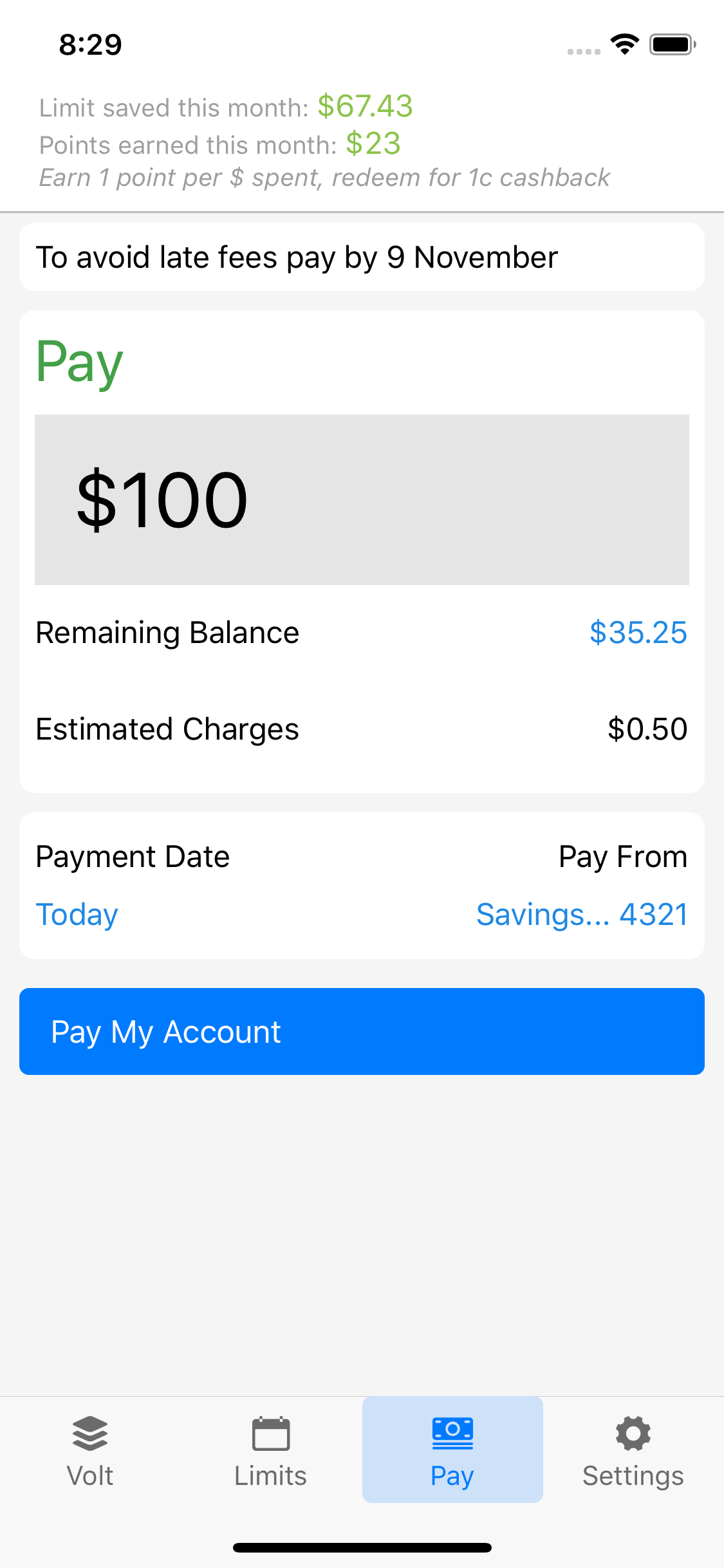

Volt - Pay your account

-

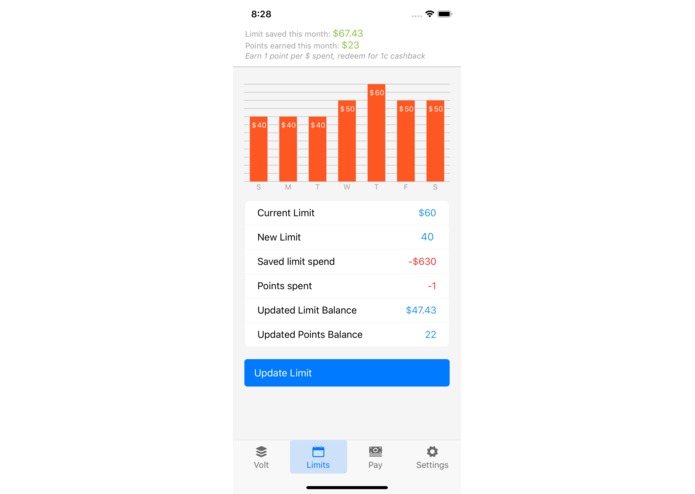

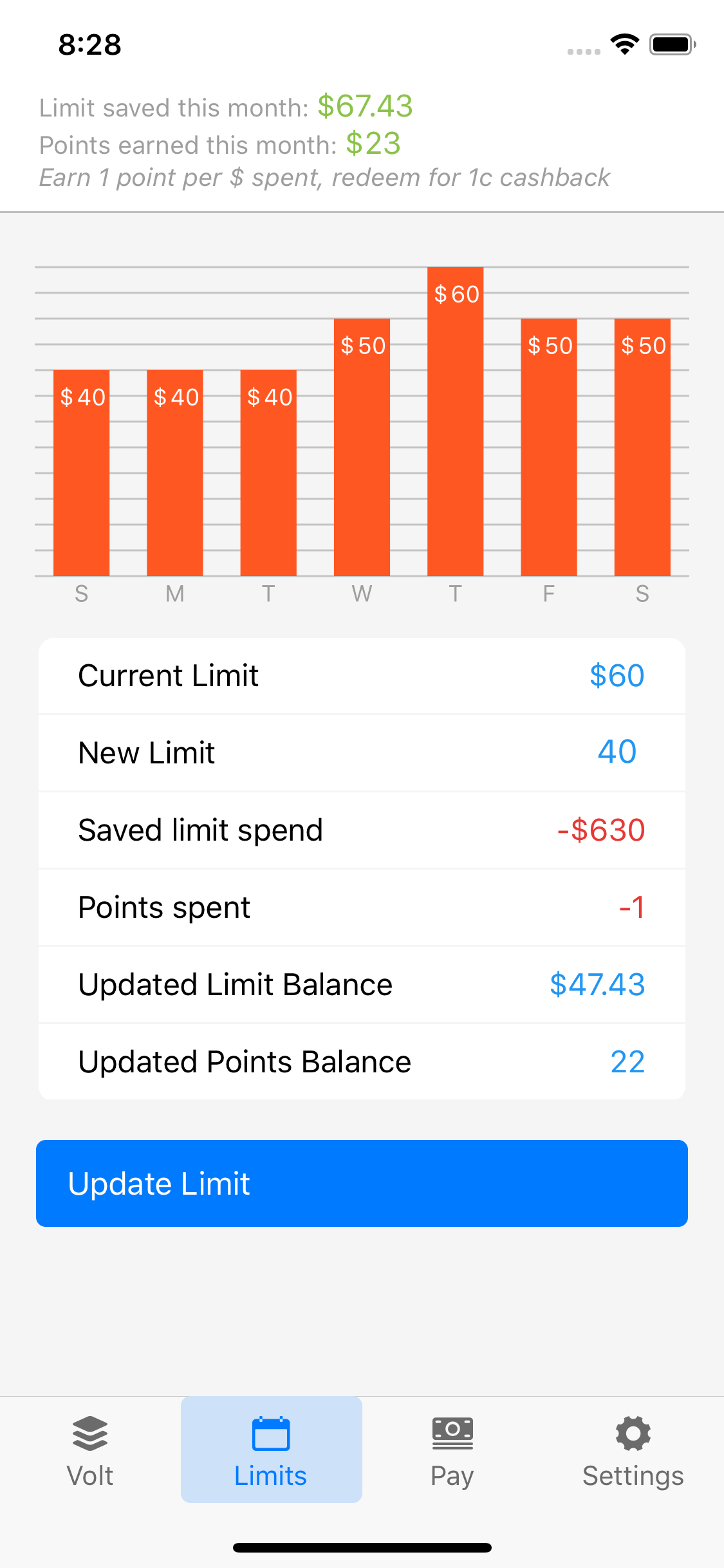

Volt - Manage Limits

-

Inspiration

Friends and family who don't have a credit card have say they avoid credit to stay clear of the temptation created by large monthly limits - opting to manage their spend with debit cards or simple cash-in-hand. In fact, the #1 reason why Americans do not obtain a credit card is that they do not trust themselves with a large line of credit.

Similarly Americans without credit scores find themselves locked out from accessing credit.

However these same Americans are missing on thousands of dollars of rewards a year that credit card owners earn in points and cashbacks.

What it does

Volt is a responsible credit card with a daily limit that matches your day-to-day. No more large $1,000+ monthly limits, simply get $25 to spend on Monday.

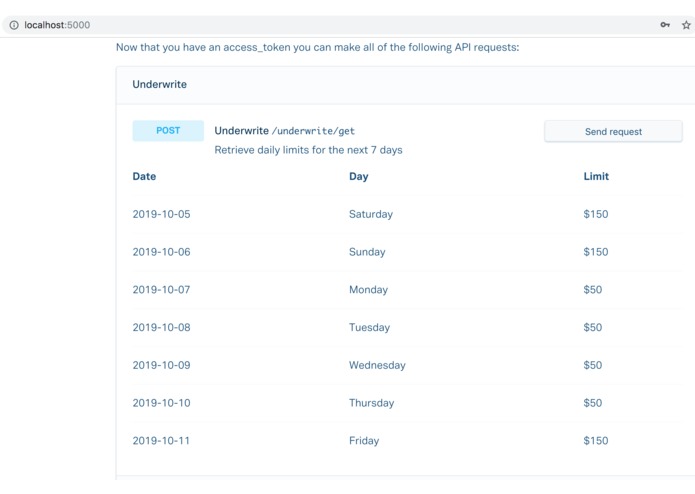

Our technology is unique in that we underwrite daily, changing limits as your personal circumstances change, without requiring a credit score.

Volt App

A simple clean app to manage your account and your limits. With the app you can:

- Receive daily notifications informing you of your limit today

- See your limits for the week

- Earn rewards and points which can be applied to your account when you Pay as cashback

- Manually adjust limits if you have accrued unused credit limits in the month (will cost you cashback)

- Pay your account

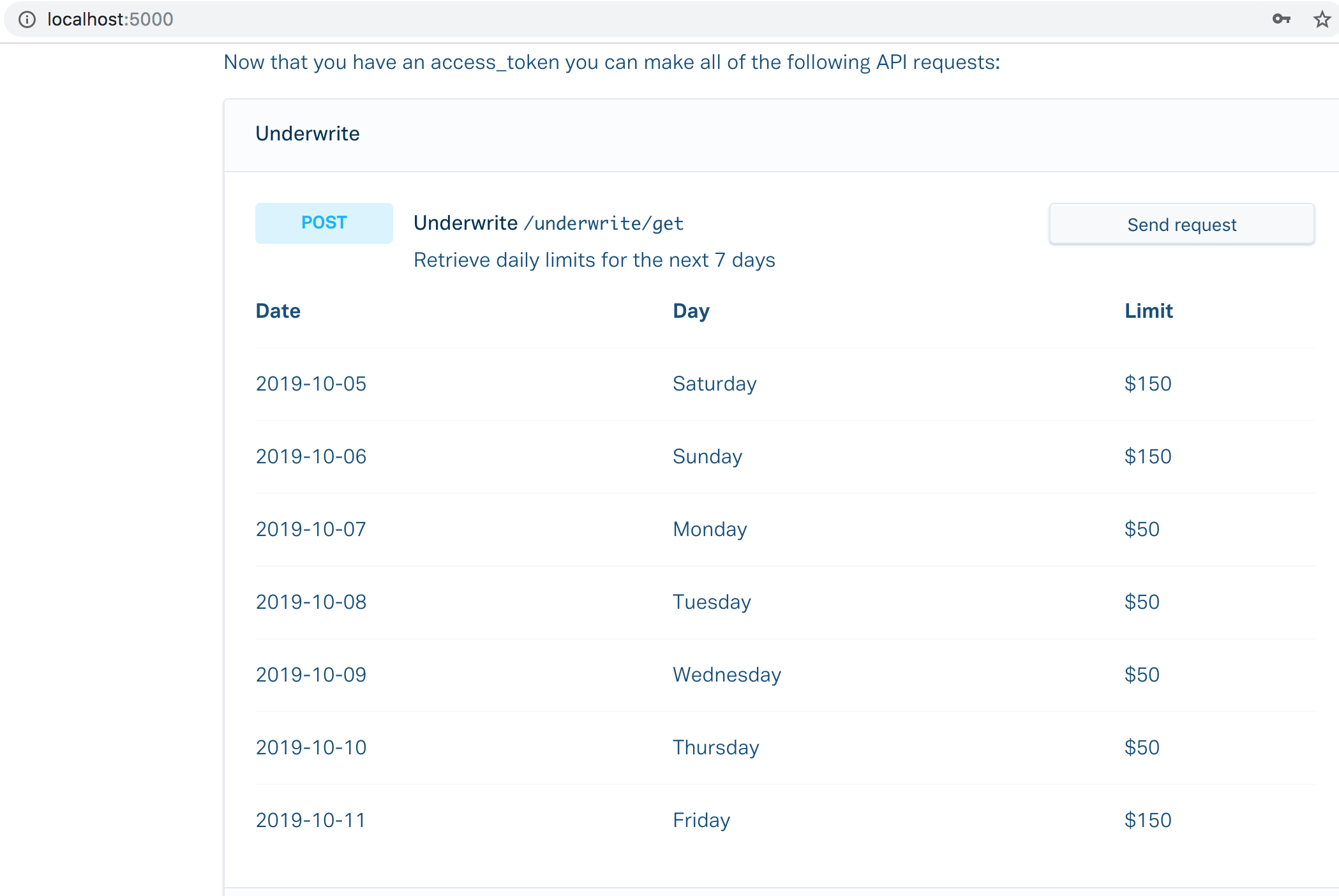

Volt Server

Volt is unique in that we underwrite and assign credit limits daily. Our underwriting model takes advantage of traditional underwriting techniques (income, expenditure etc.) as well as uses machine learning to predict future spending and tailor daily limits to fit your life.

We look at your income, spend and cash balances to give you an initial total limit. We then use our predictive technology to craft this limit around your week (spend more on Friday's, get a higher limit on that day and a lower limit during other days of the week, up to an amount that suits your income level).

Similarly our limits change daily - if you've had a change in your personal circumstances see your limit automatically increase or decrease over time (Regulation: we assign a "maximum" monthly limit when you sign up and do not exceed that without your consent). In that way we're building a more responsible credit card that you won't accidentally overspend on.

How we built it

Backend

Python, Plaid, StatsModel, numpy

See repo readme for detail on underwriting method and details

Front end app

React Native

Challenges we ran into

- Transactional data that's well categorised and complete

- Avoiding the double counting of liabilities and repayments of those liabilities when using transactional data to manage spend

- Certain expenses (utilities etc.) are large and happen infrequently. Our model needs to accomodate for payments that happen less frequently than once every month and consider these in monthly expenditure vs. monthly income.

- Similarly, for these expenses to payable using Volt, we need to forecast them and create "outsized" limits on those days. We predict expenses using historical data to accommodate this, and also allow users to manually override spend.

- Choosing the right predictive models, and potentially one day including external factors beyond time series spend.

Accomplishments that we're proud of

- Used some new technologies we hadn't experimented with before (statsmodel)

- Used plaid for the first time, really happy with it..

- React Native is a lot better than we remember from a few years ago ha..

What we learned

- Cleaning and accurately categorising transactional data is harder than it should be (banks argh!)

- Initially our spend is not that predictable.. (initial model with p-values > 0.05). Continue to work on the model but likely need to clean spend data further and consider some external factors (credit scores where available, timing of payments and receiving pay, etc.)

What's next for Volt

- Continue to refine and improve our user by user based spend and income prediction. Include external factors that may influence this (e.g. credit scores where available).

- Eventually move away from traditional underwriting methods which do not work for the increasingly flexible and variable way we work and live (gig economy etc.). Circumstances are changing daily, and so should the financial products that you use every day.

- Launch this!

Log in or sign up for Devpost to join the conversation.