-

-

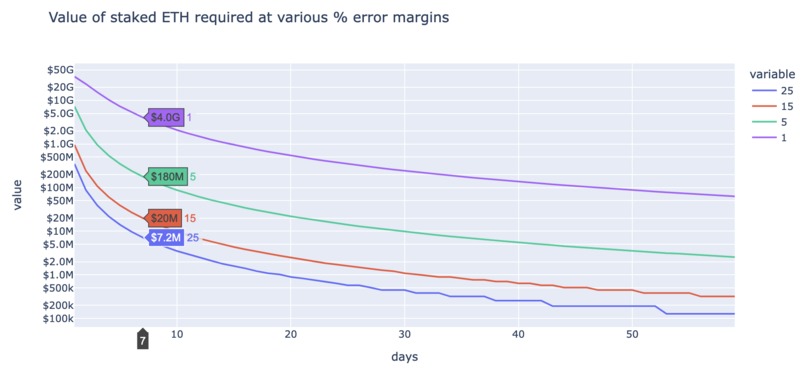

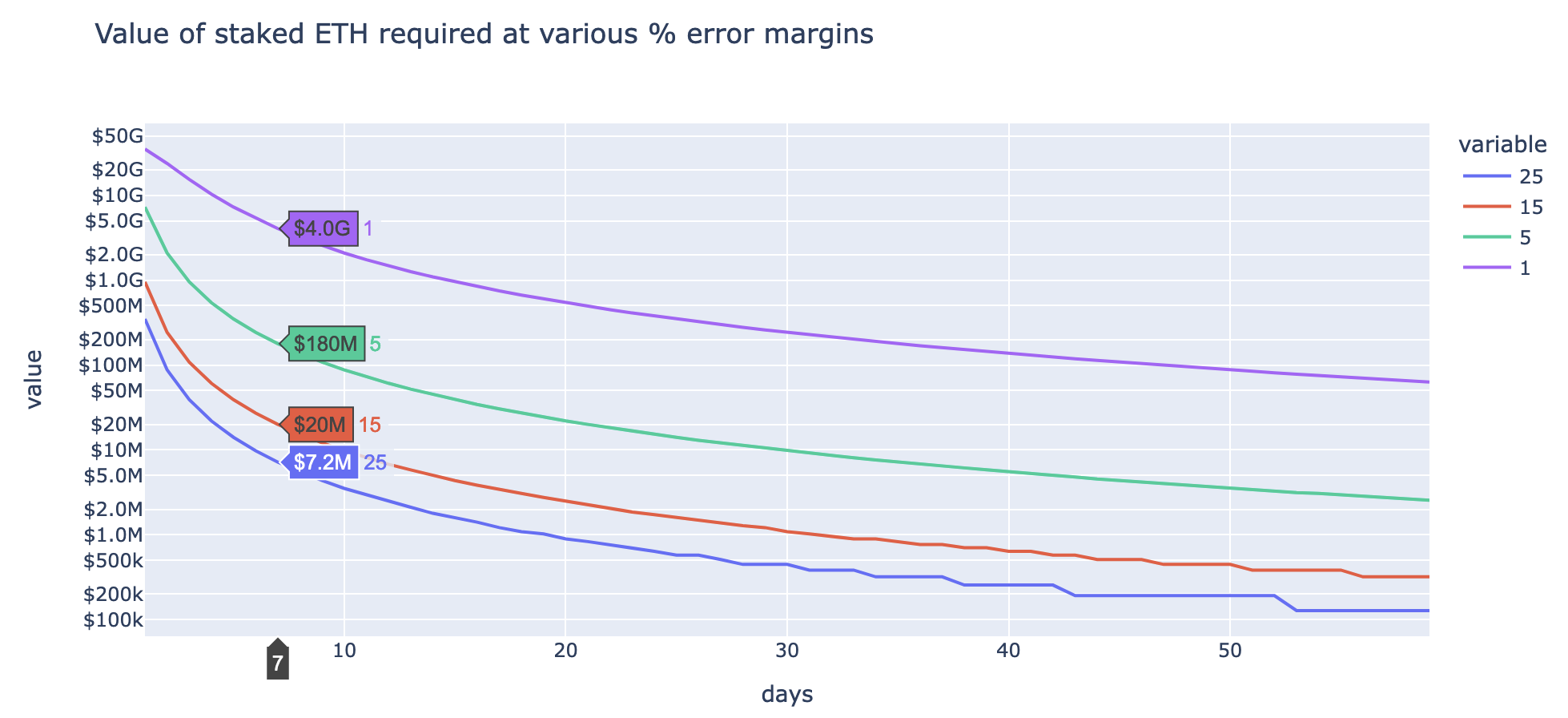

Sampling sizes

-

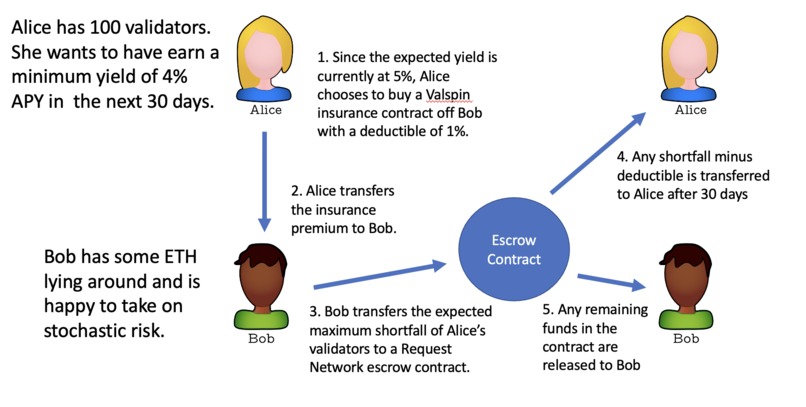

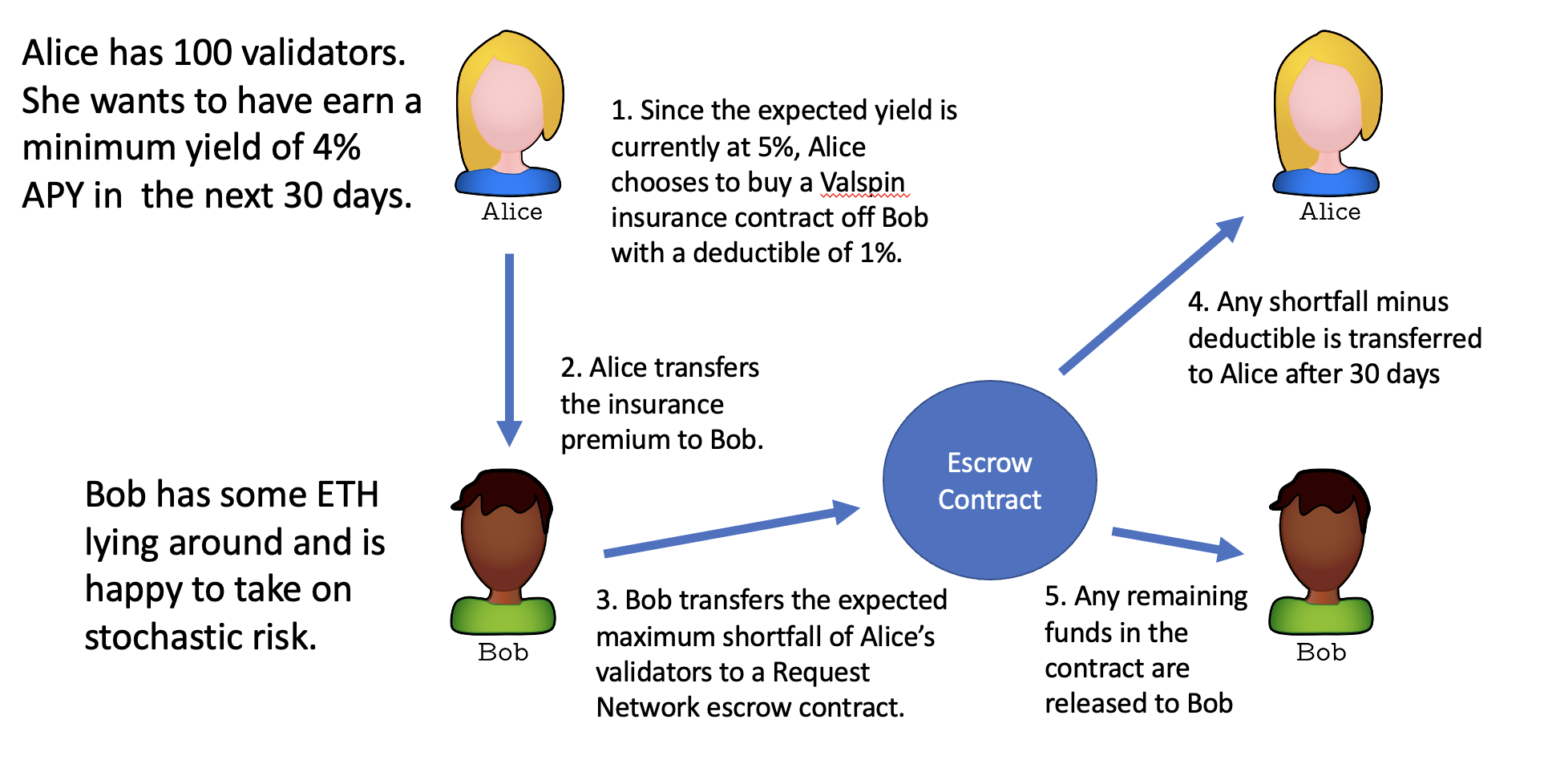

Insurance product

-

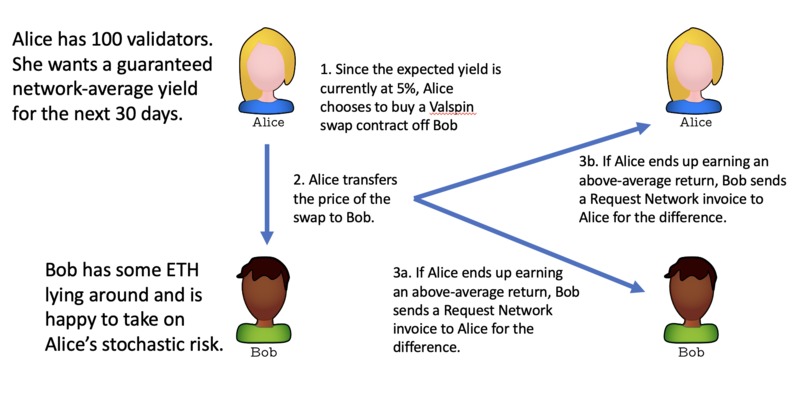

Swap product

Inspiration

As Blackrock and other financial institutions come into the cryptoasset universe with ETFs and ETPs based on total return indices, the demand for hedging products will rise. ETFs are traded on indices that depict the average return across the network on an asset. When ETH staking is integrated, it becomes difficult to replicate the index physically, something the financial institution must do, as validators are heavily impacted by the stochastic nature of proposer rewards. Only 7200 blocks are proposed per day and 700k validators compete to propose these blocks. Therefore, each validator proposes a block only once every 97 days. Since a block proposal pays a significant portion of a validator's total rewards, a staker needs a huge number of validators to have a large enough sample size to get close to the average network yield.

What it does

Valspin offers two products for validator owners to hedge away stochastic event risk, a swap contract and an insurance contract. Hedging away stochastic risk with such products is especially attractive to TradFi institutions issuing index products which promise investors an average return and any other entity that has a guaranteed liability at a future point in time and wants to lock in ETH staking yield. Such entities cannot benefit from pooling solutions on-chain, as commingling funds is always a big no-no.

Insurance Contract

Our insurance contract allows a staker to cover any downside stochastic event risk. The staker buys the contract from an investor for a predetermined premium. The investor guarantees a potential payout in a Request Network escrow contract. If the staker's validators underperform the average network return over that time period, the contract sends funds to the staker to cover any losses (subtracting any agreed-upon deductible). The remaining funds are returned to the investor. If the staker's validators outperform the average return by the end of the contract, no funds are transferred.

Swap Contract

Our swap contract allows a counterparty (e.g. an investor) to provide the capital to cover a staking entity's stochastic risk. The staker pays a small fee to the investor. At the end of the swap, a Request Network invoice is sent to the staker if they earned an above-average return, paying the investor the outsized earnings. If the staker earned less than the expected return, the staker submits an invoice to the investor to cover their losses.

How we built it

We built this project with a lot of statistical modelling based on staking yield rates and the state of the consensus layer. We fetch yields by calculating the difference between the WSTETH-ETH ratio from month to month, as returned by Chronicle. These along with some other parameters are passed into Python Flask endpoints and called by a React framework. Here, the staker can enter the number of validators and days they want to insure or swap. The calculated price is passed to a Request Network invoice, where the staker can pay the premium or cost of the desired product.

Challenges we ran into

Unfortunately, one can only query Chronicle oracle feeds starting from the block height at which the address was whitelisted. This made it difficult to pull an accurate average yield on ETH staking through a combination of the WSTETH and ETH feeds.

Accomplishments that we're proud of

We're most proud of the modelling work we've done.

What's next for Valspin

There is guaranteed to be appetite for these products. We intend to pursue the project further.

Log in or sign up for Devpost to join the conversation.