-

-

Landing page

-

privacy

-

about

-

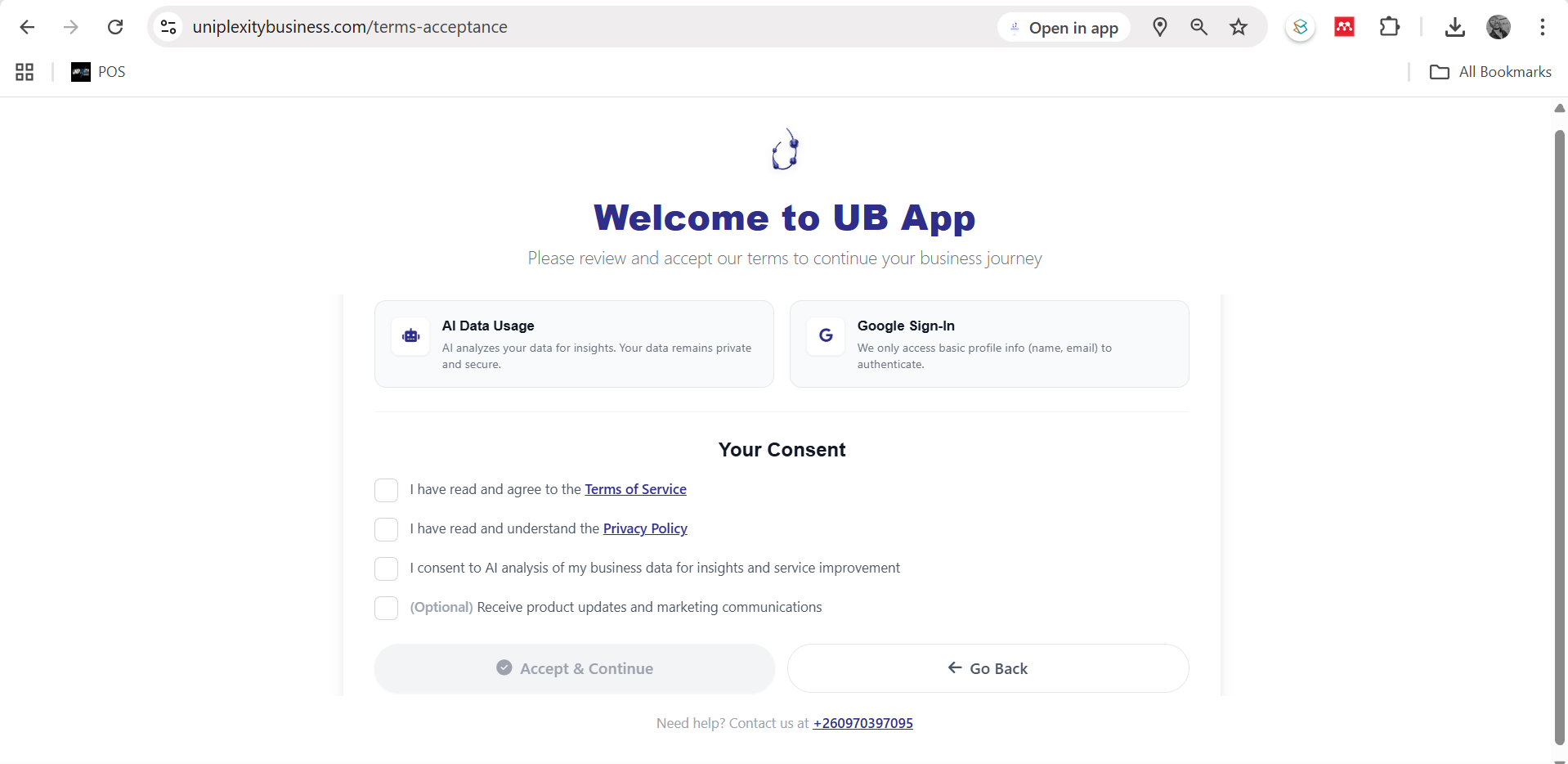

terms

-

help

-

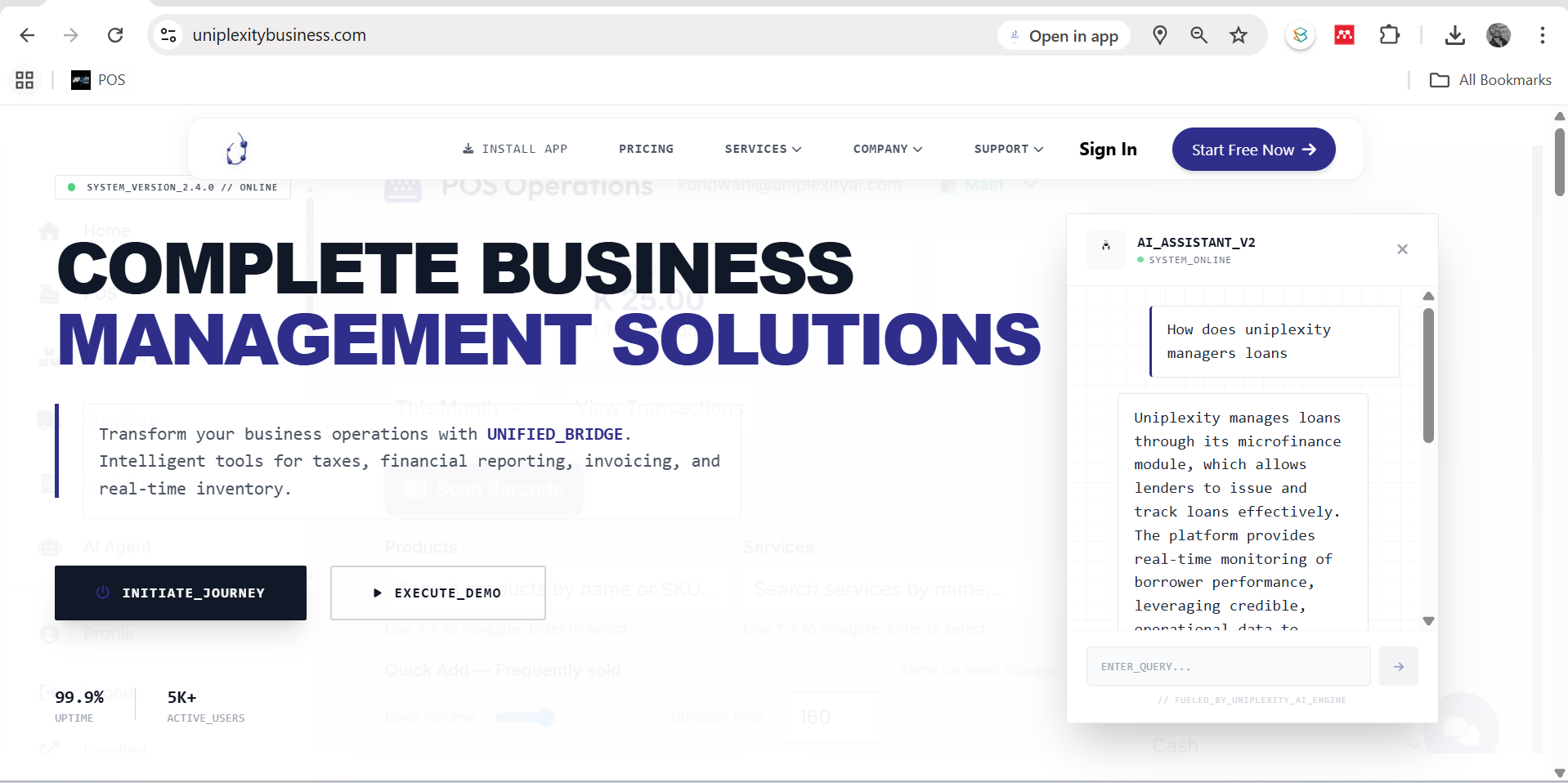

UB Ai assistant

-

your consent

-

sign up

-

sign up

-

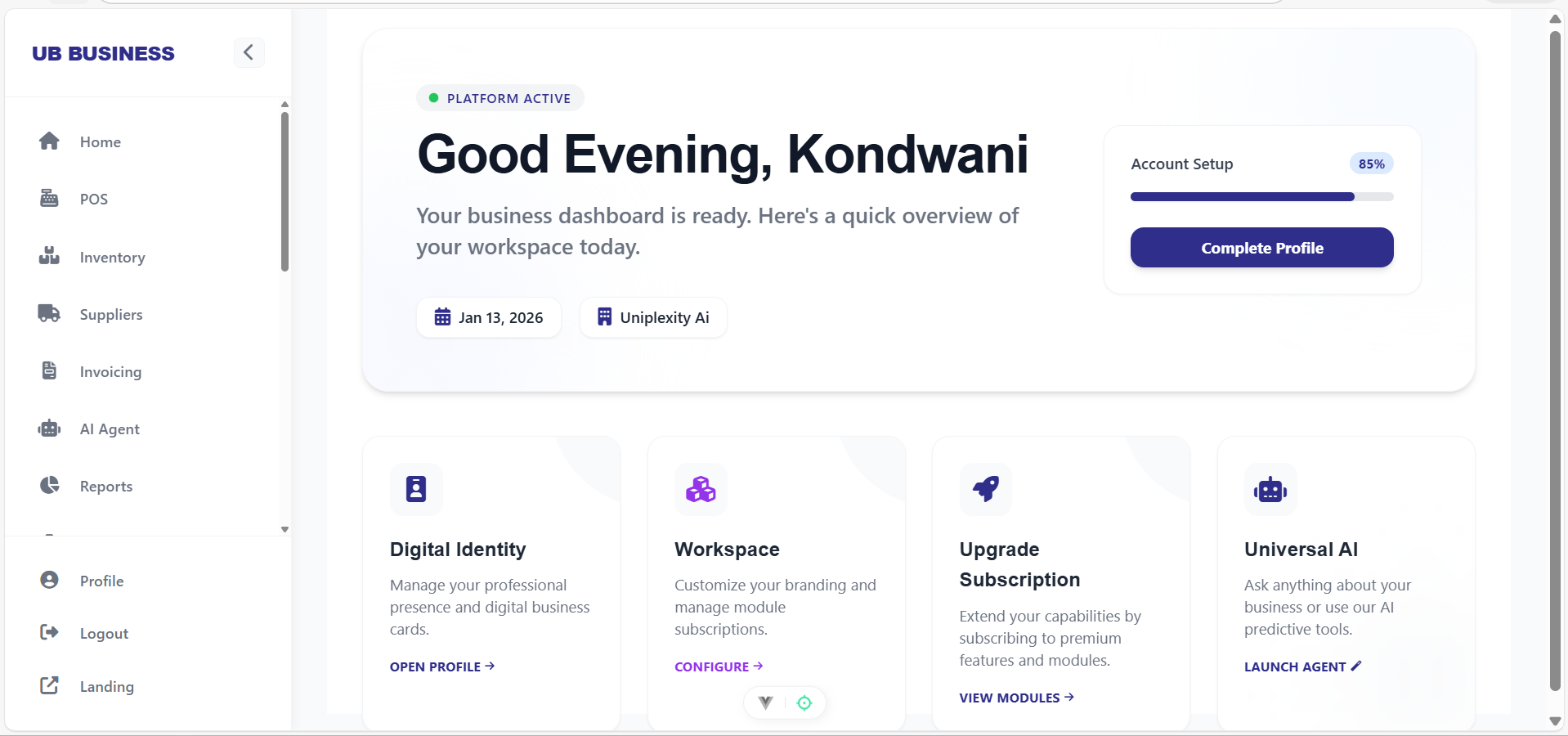

home

-

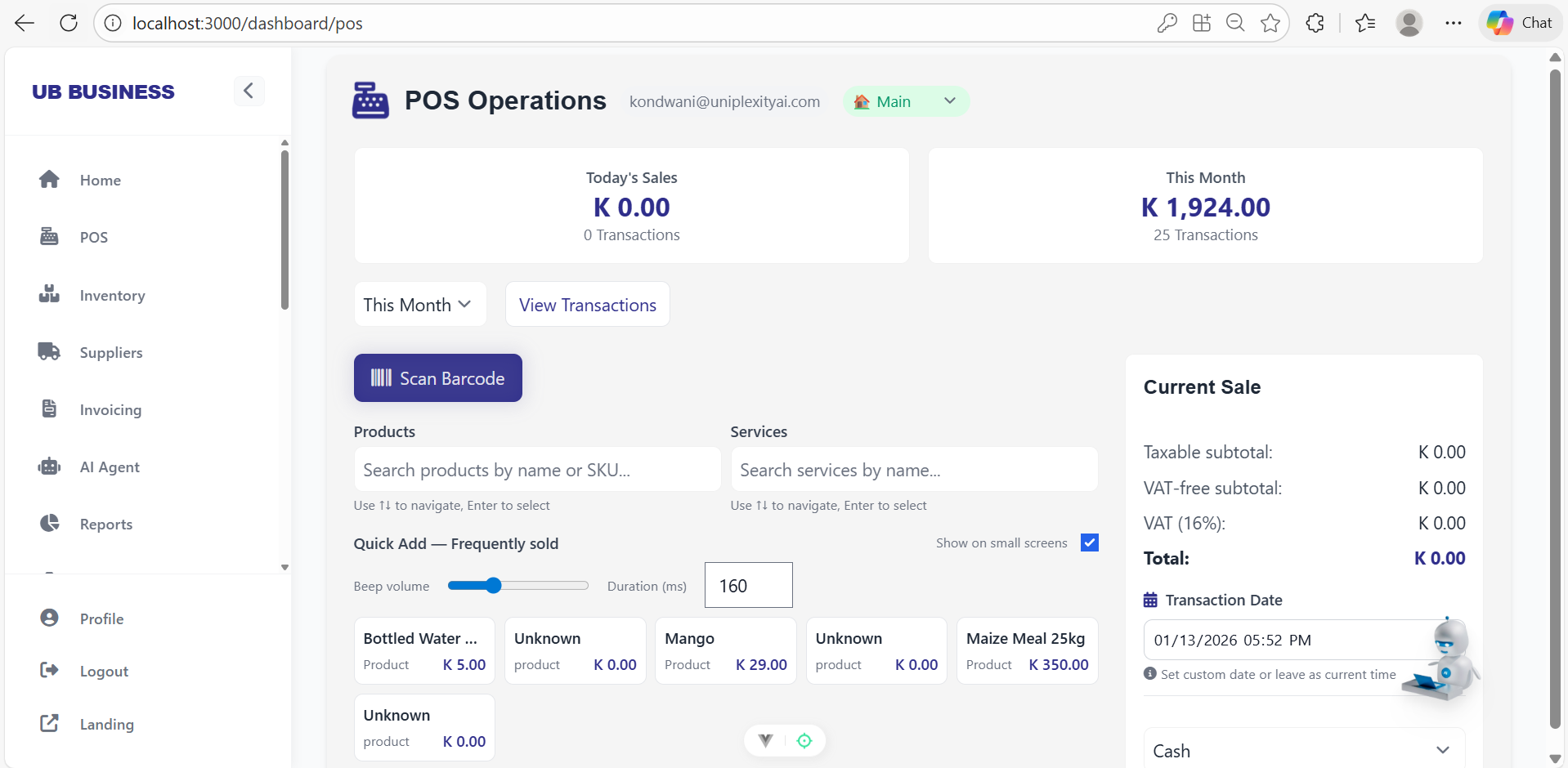

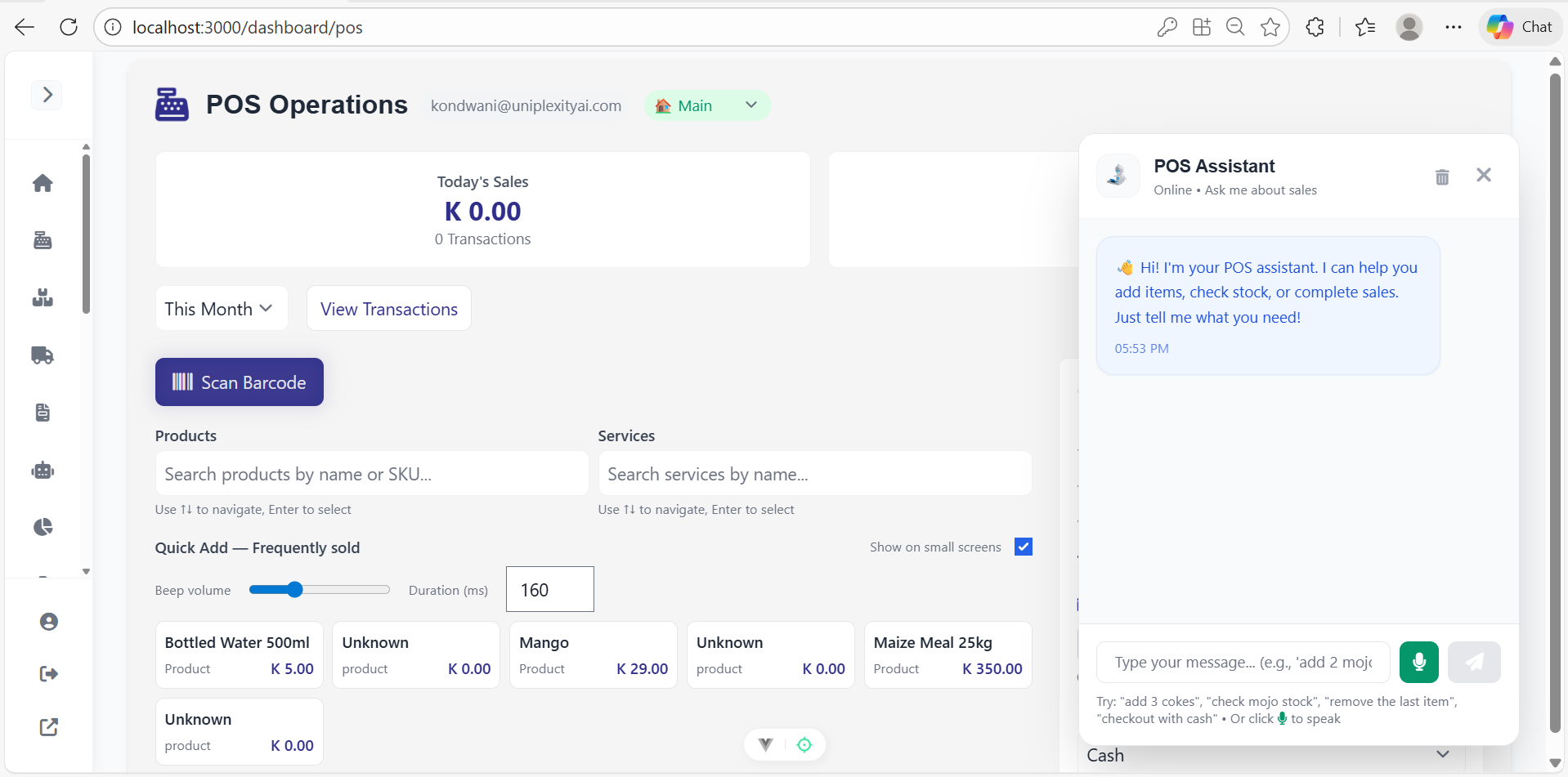

pos

-

pos chat bot

-

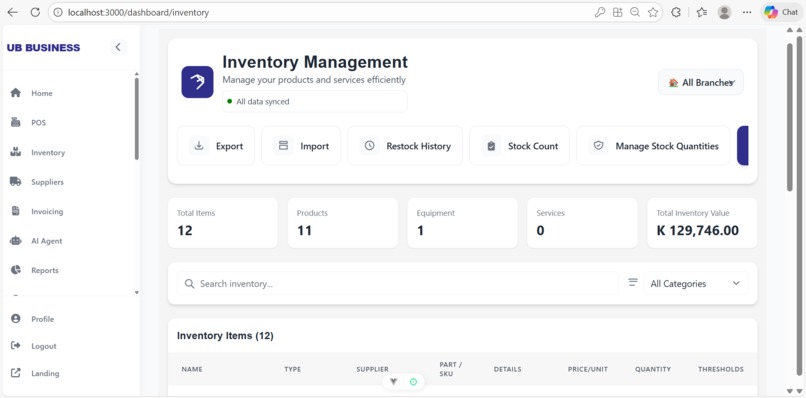

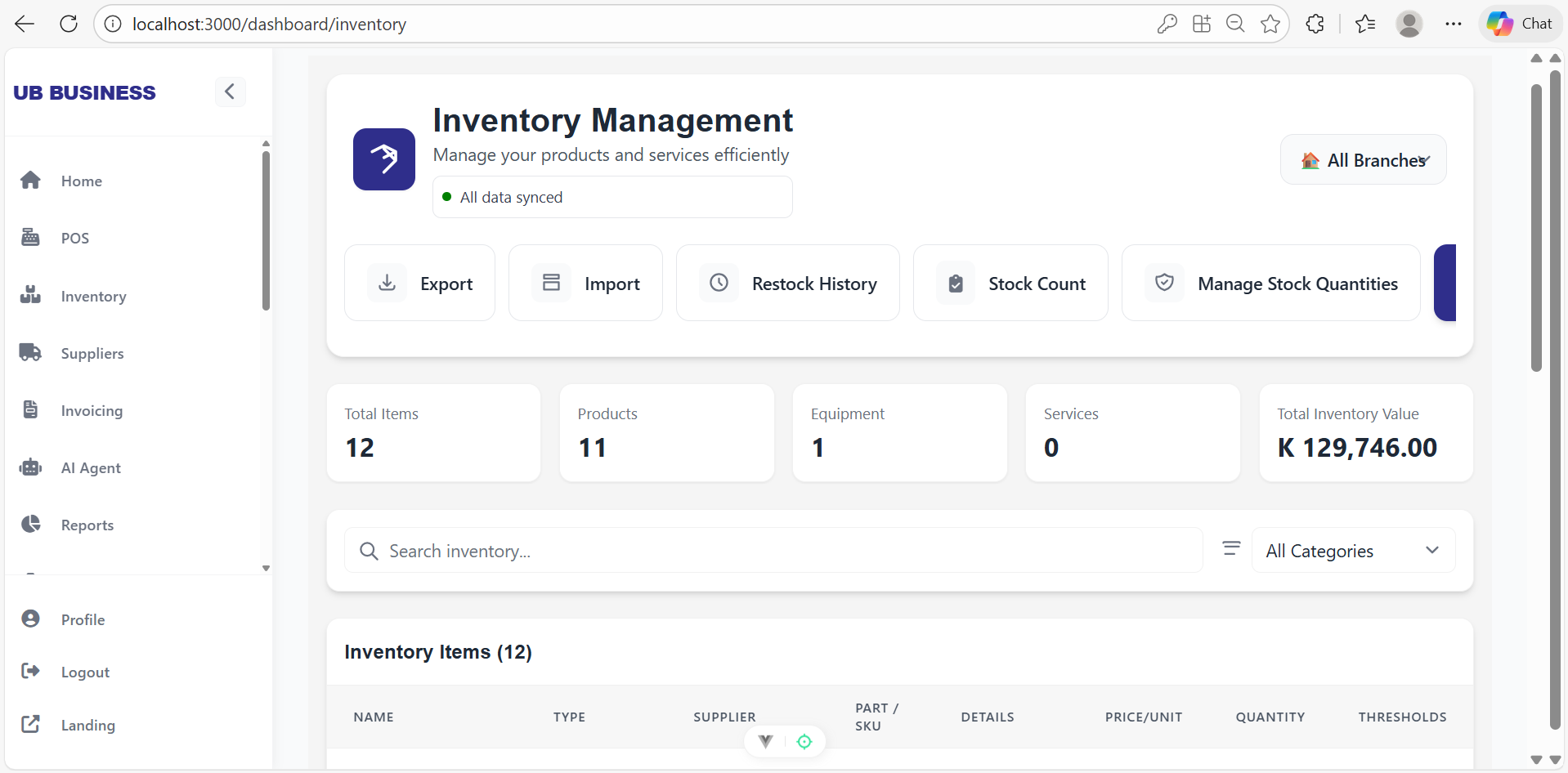

inventory

-

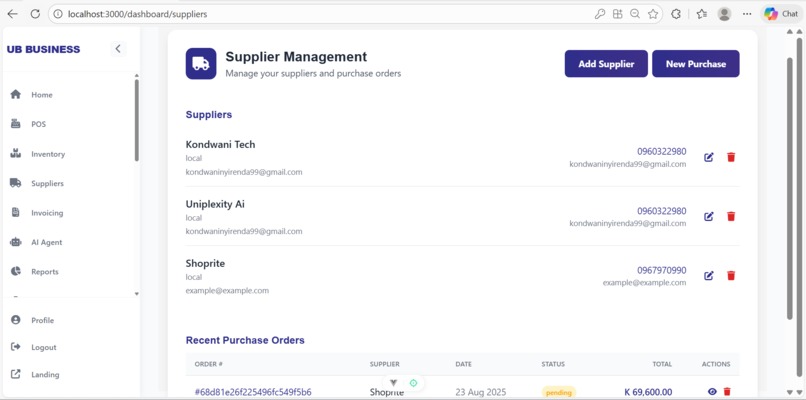

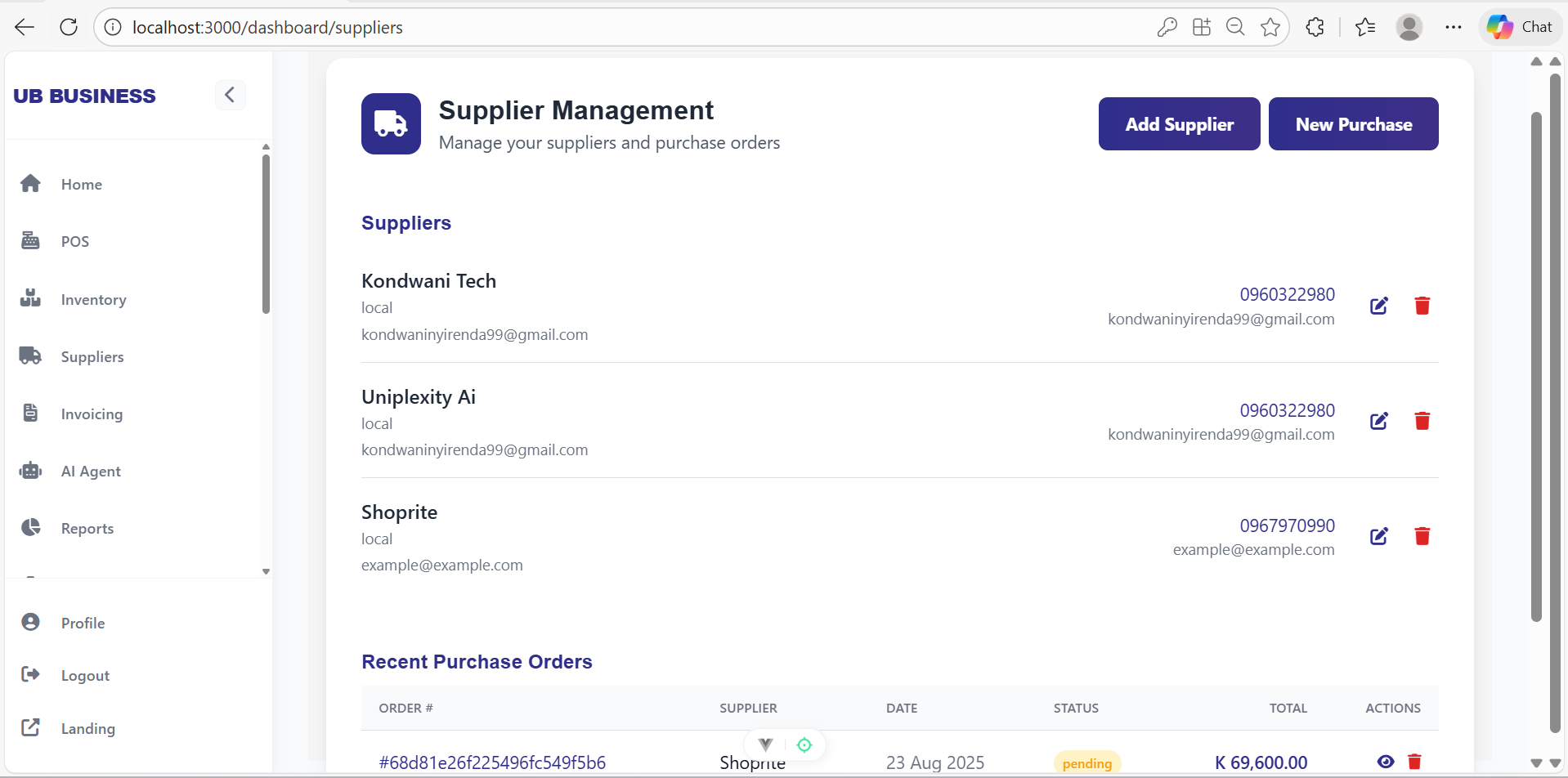

supplier manaement

-

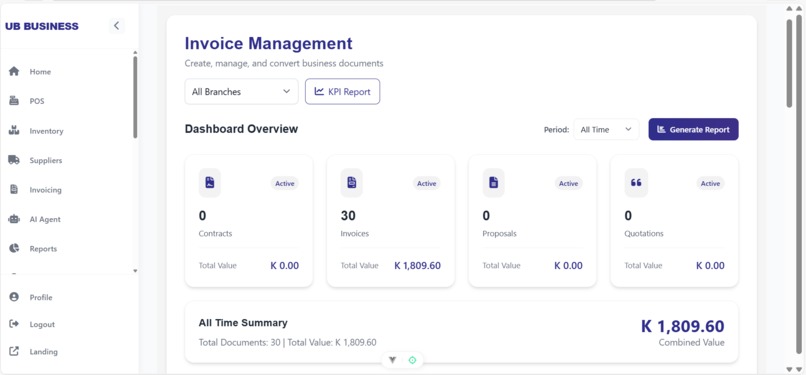

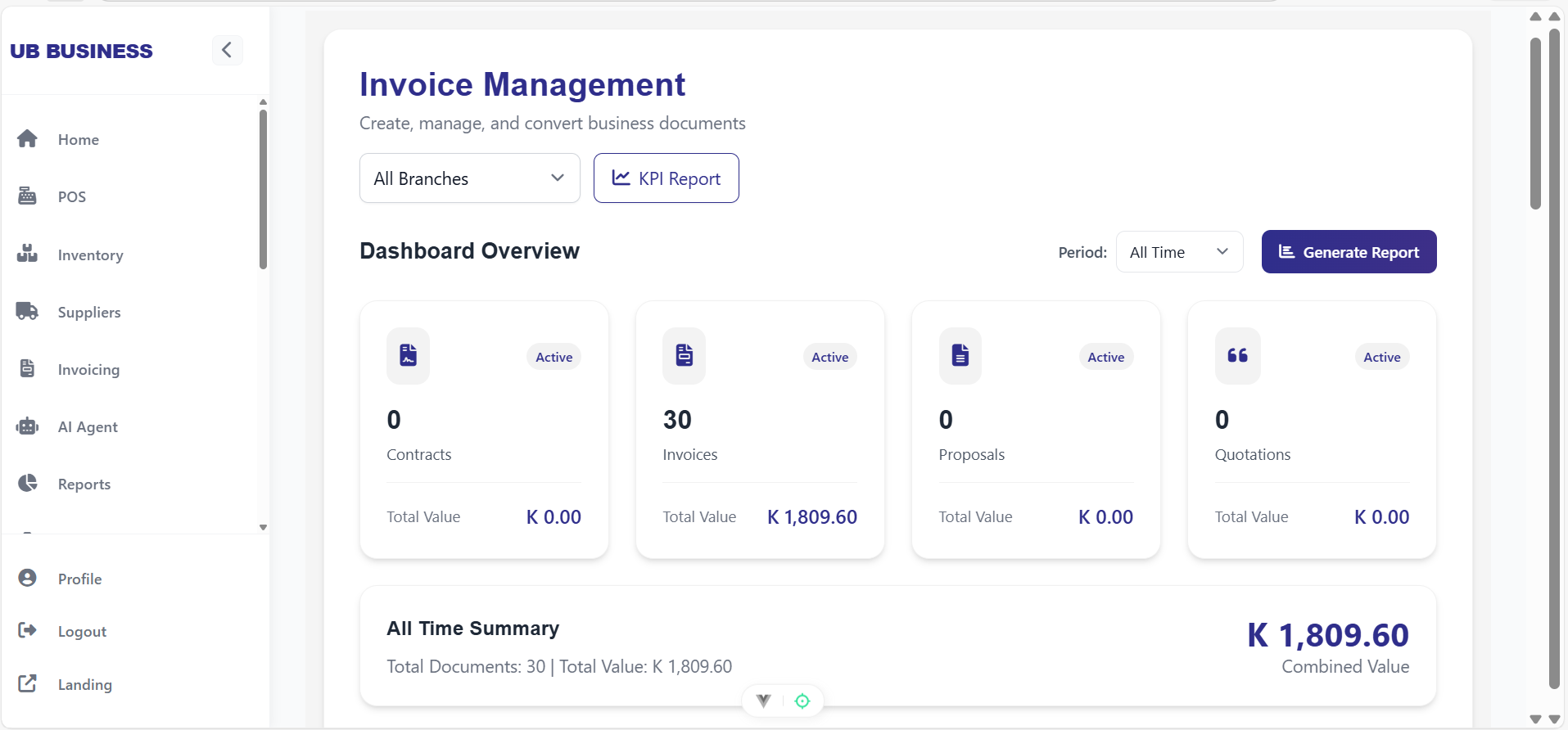

invoice

-

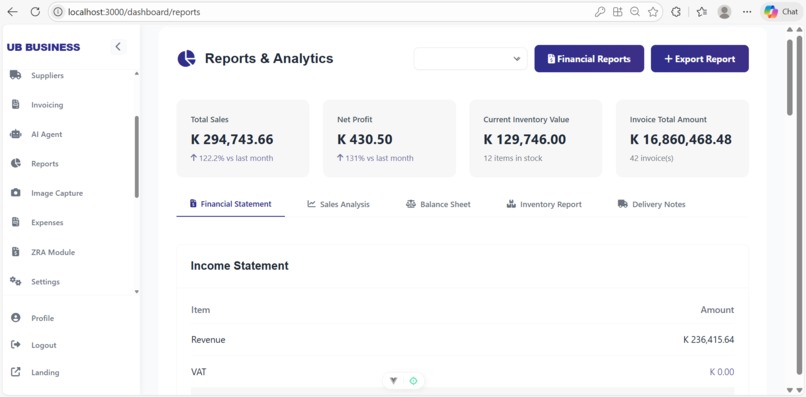

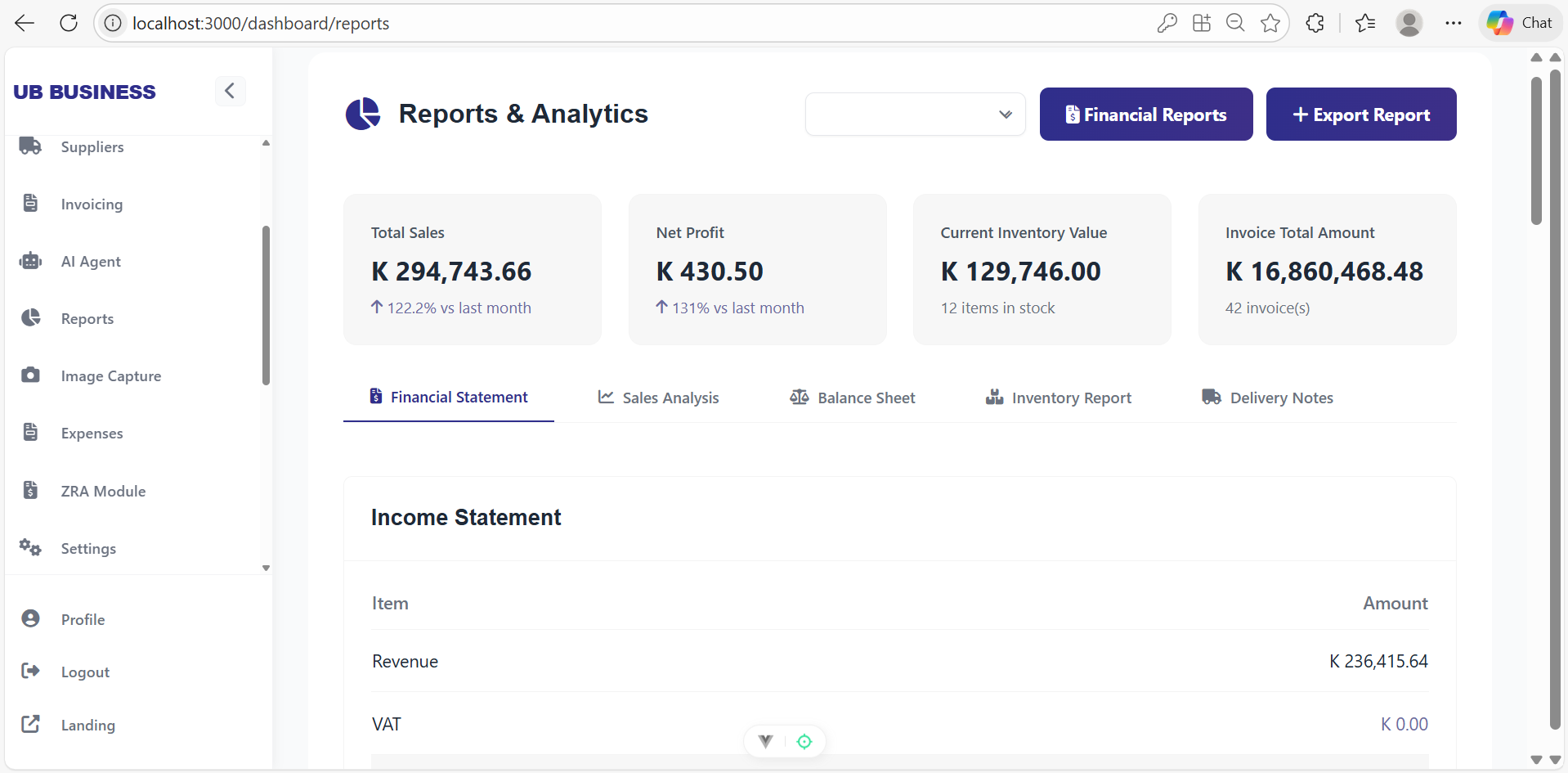

reports

-

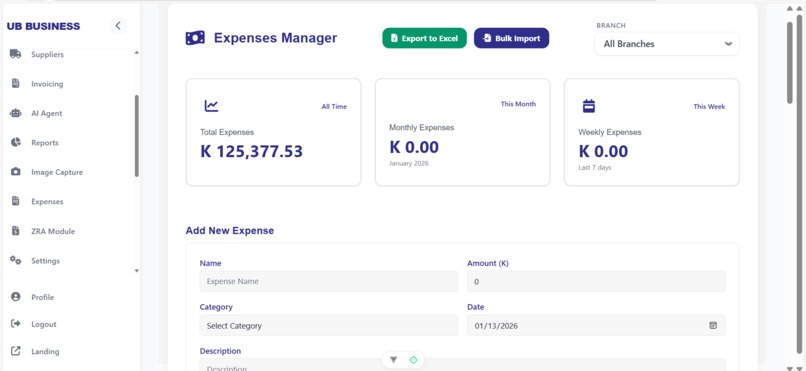

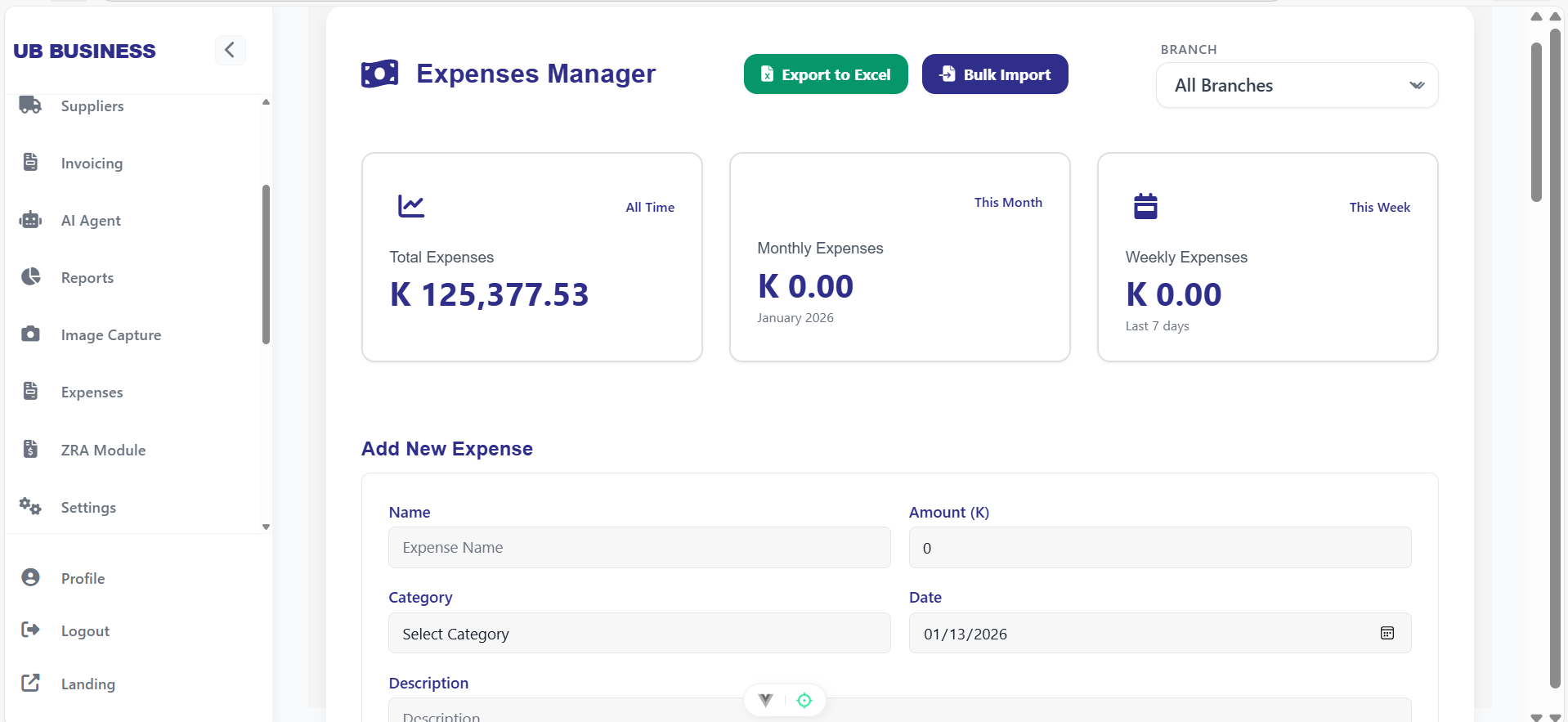

expenses

-

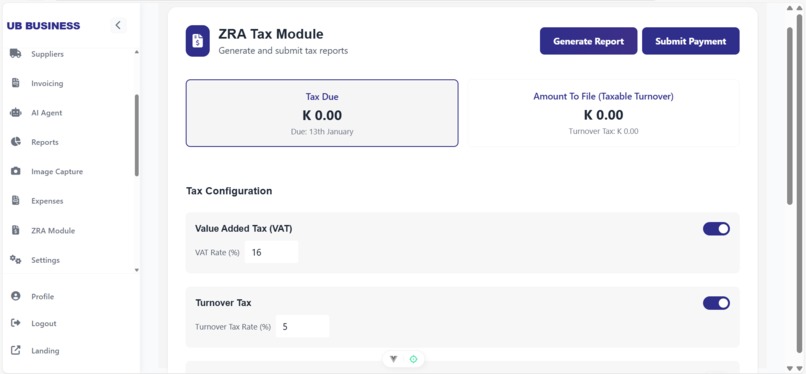

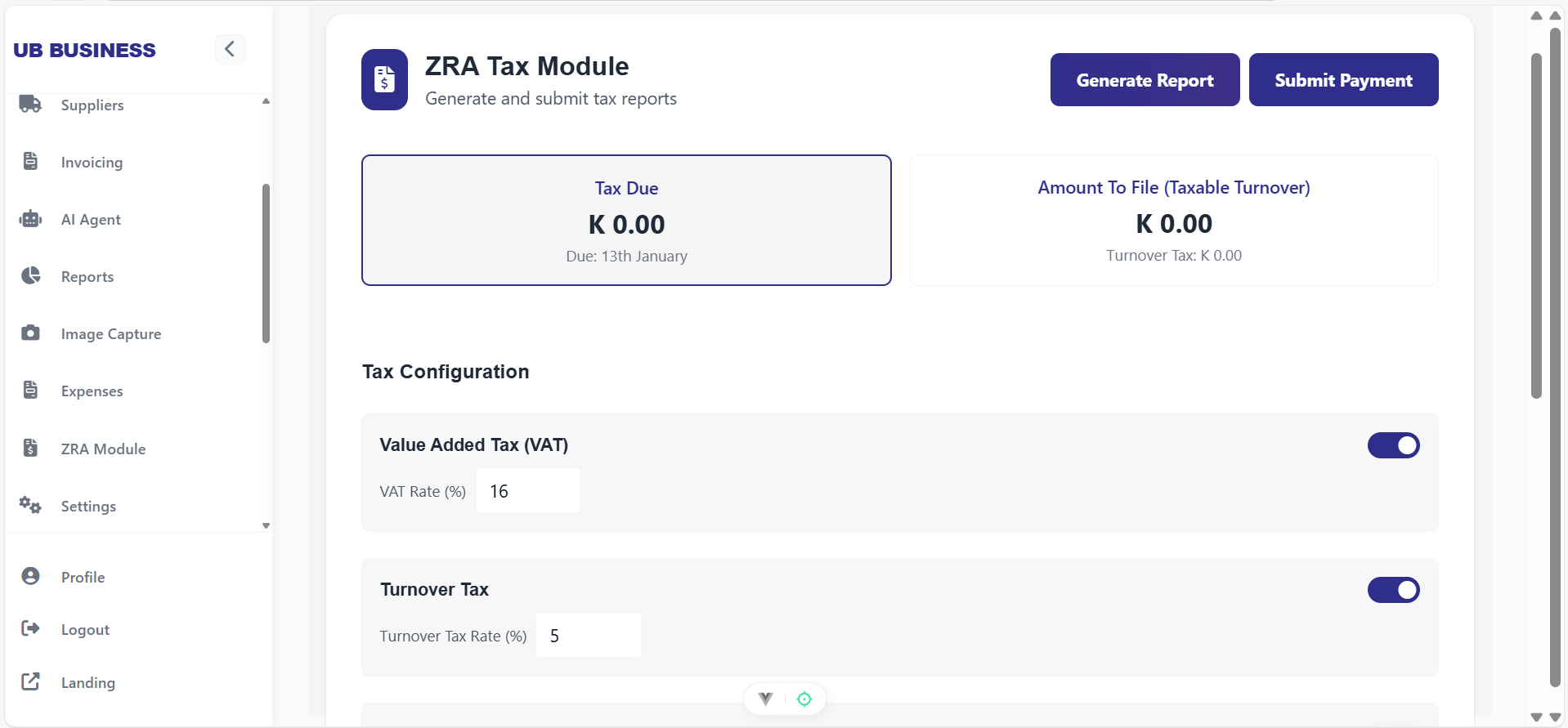

compliance

-

settings

-

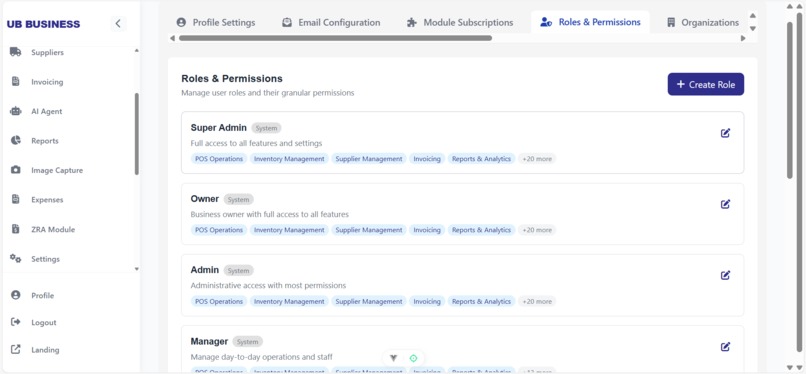

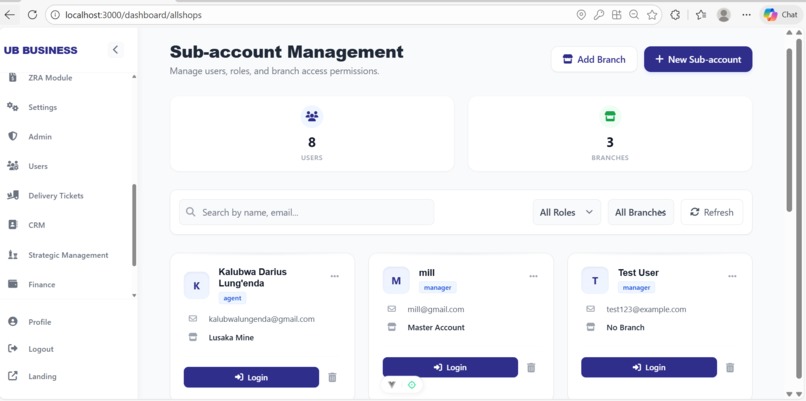

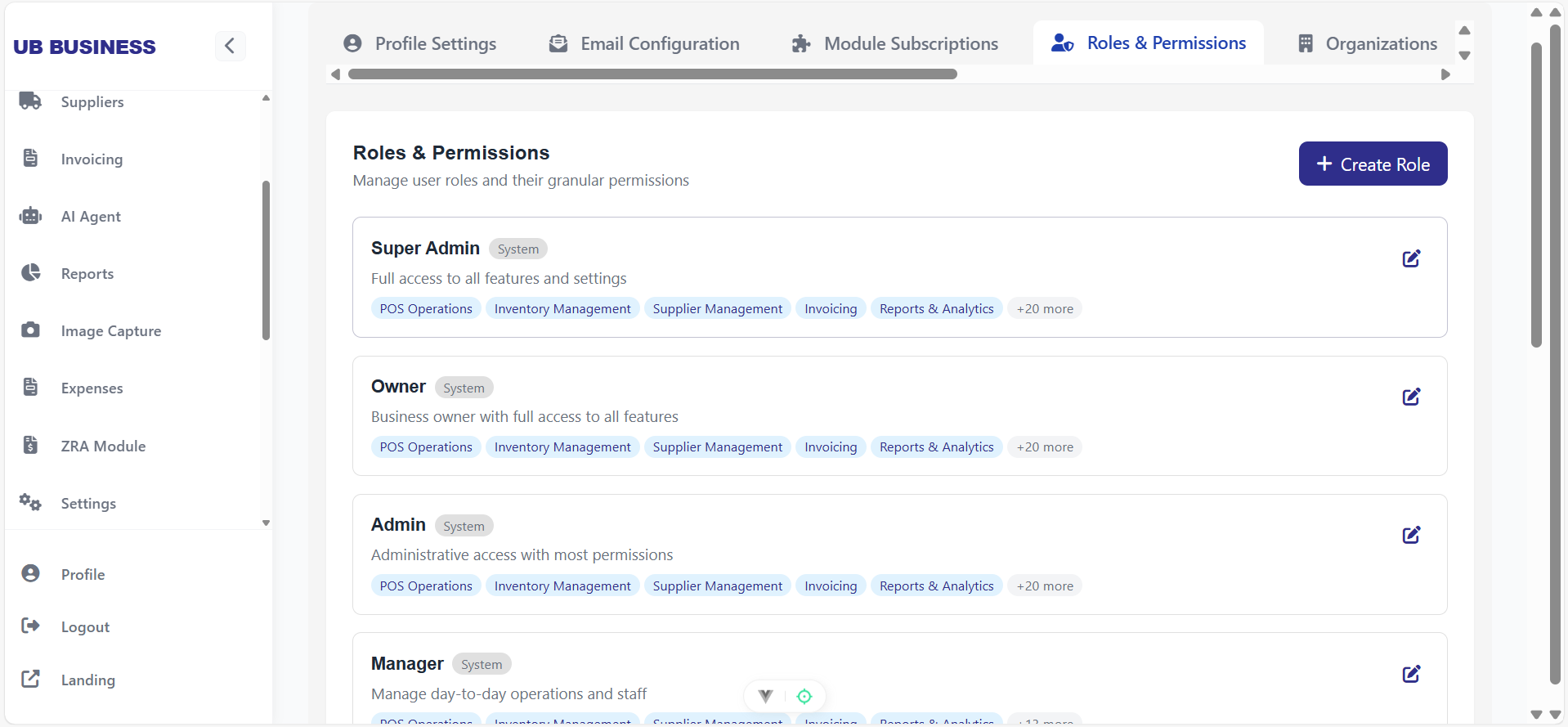

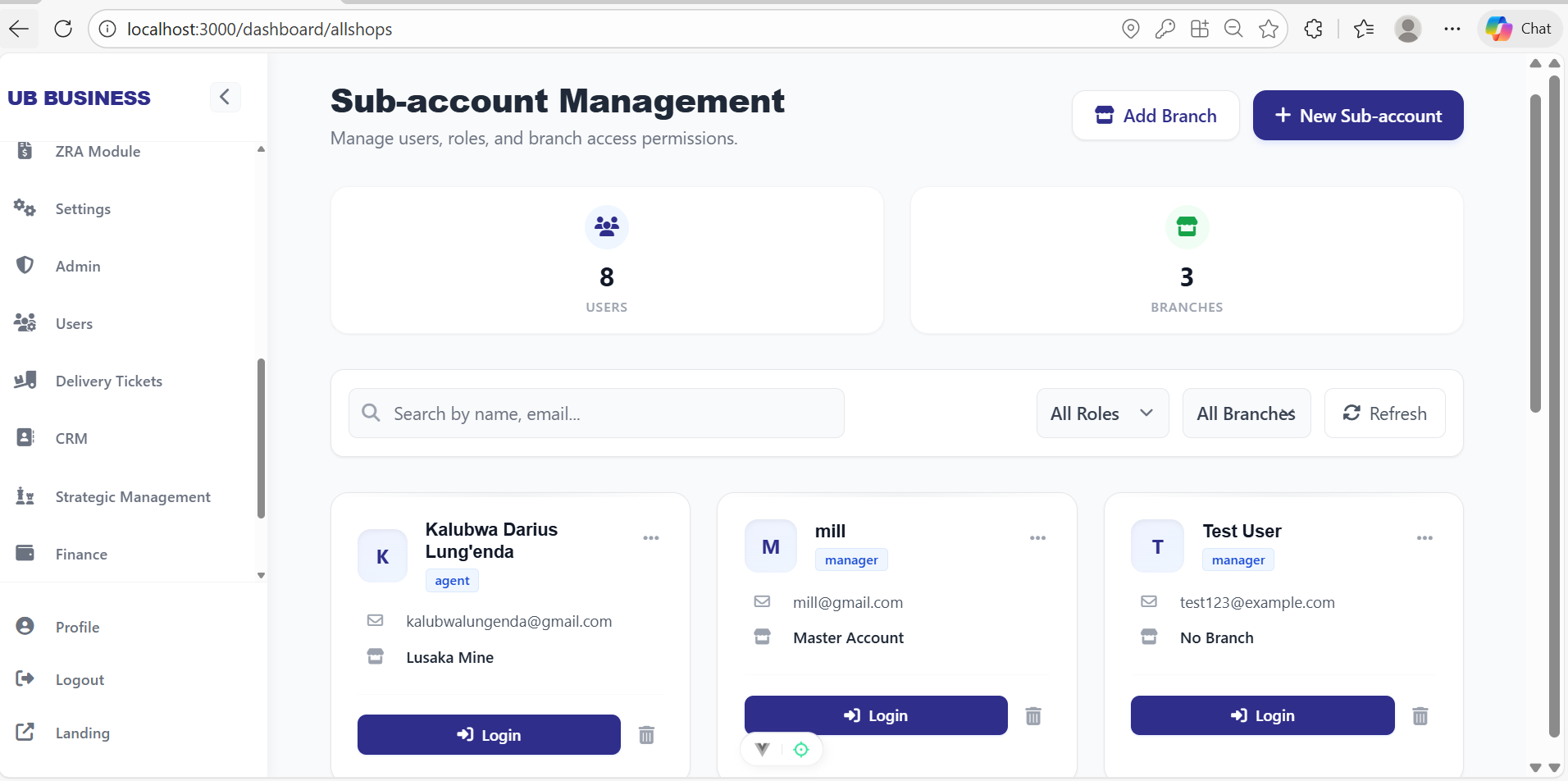

user management

-

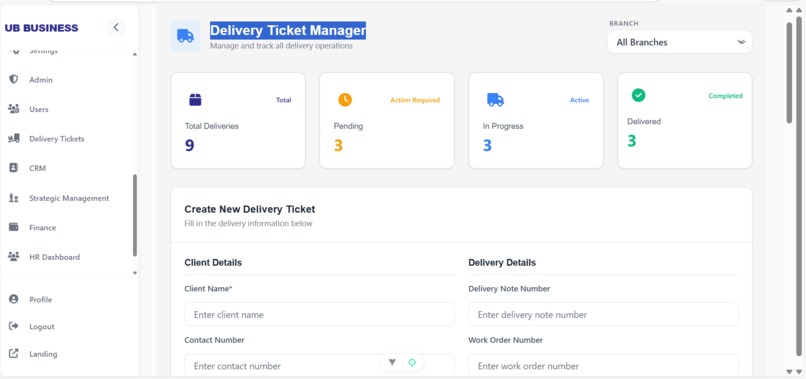

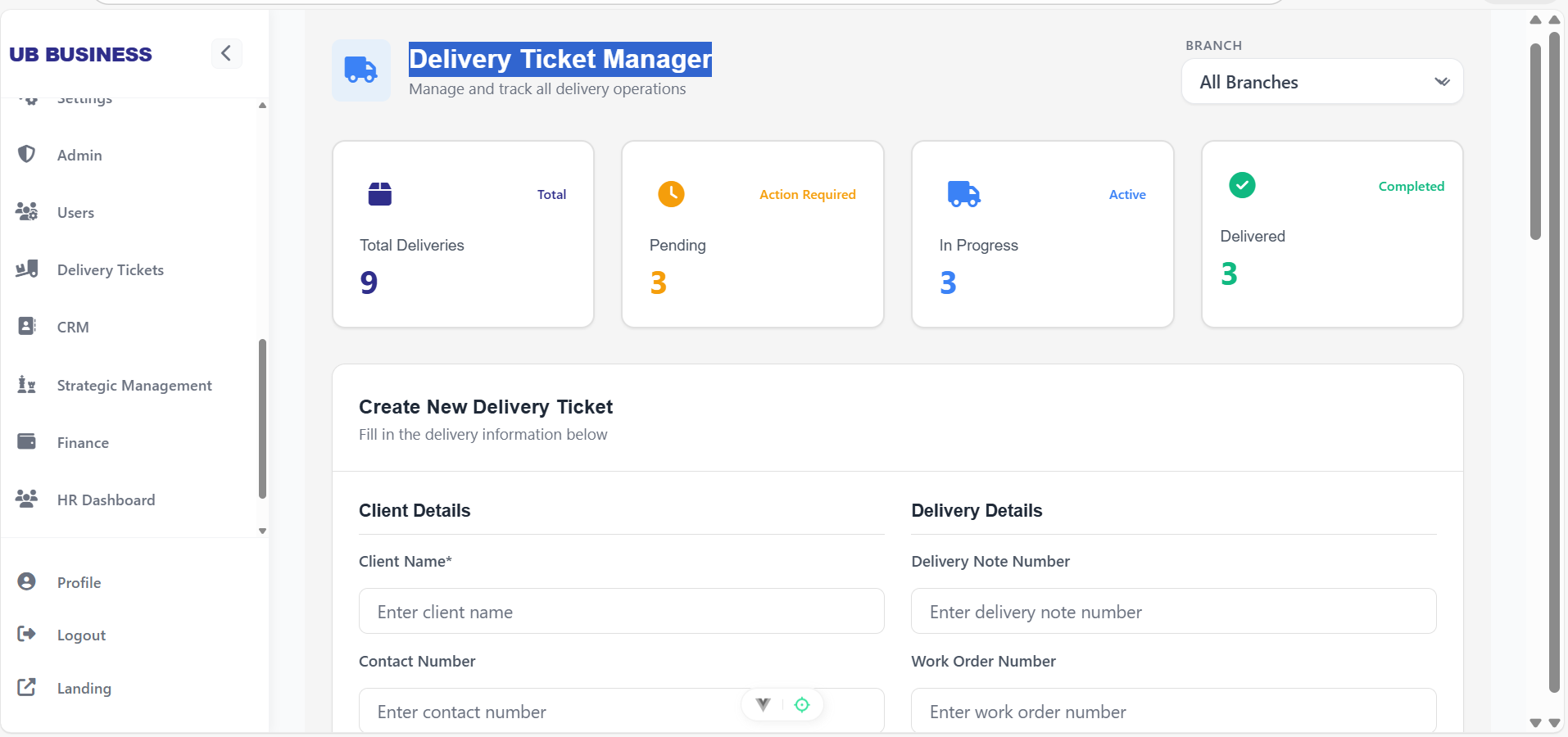

delivery manaement

-

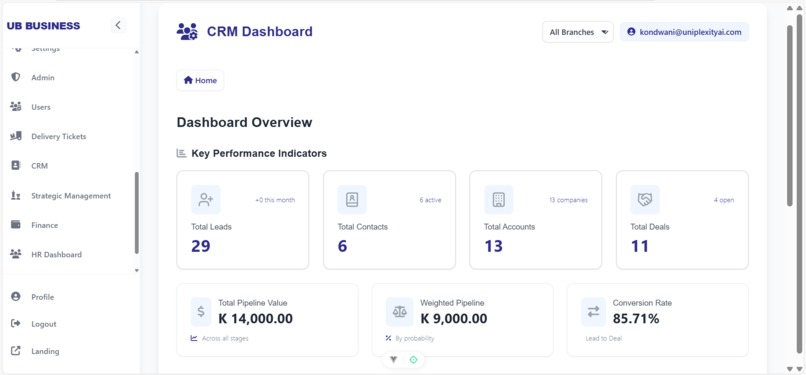

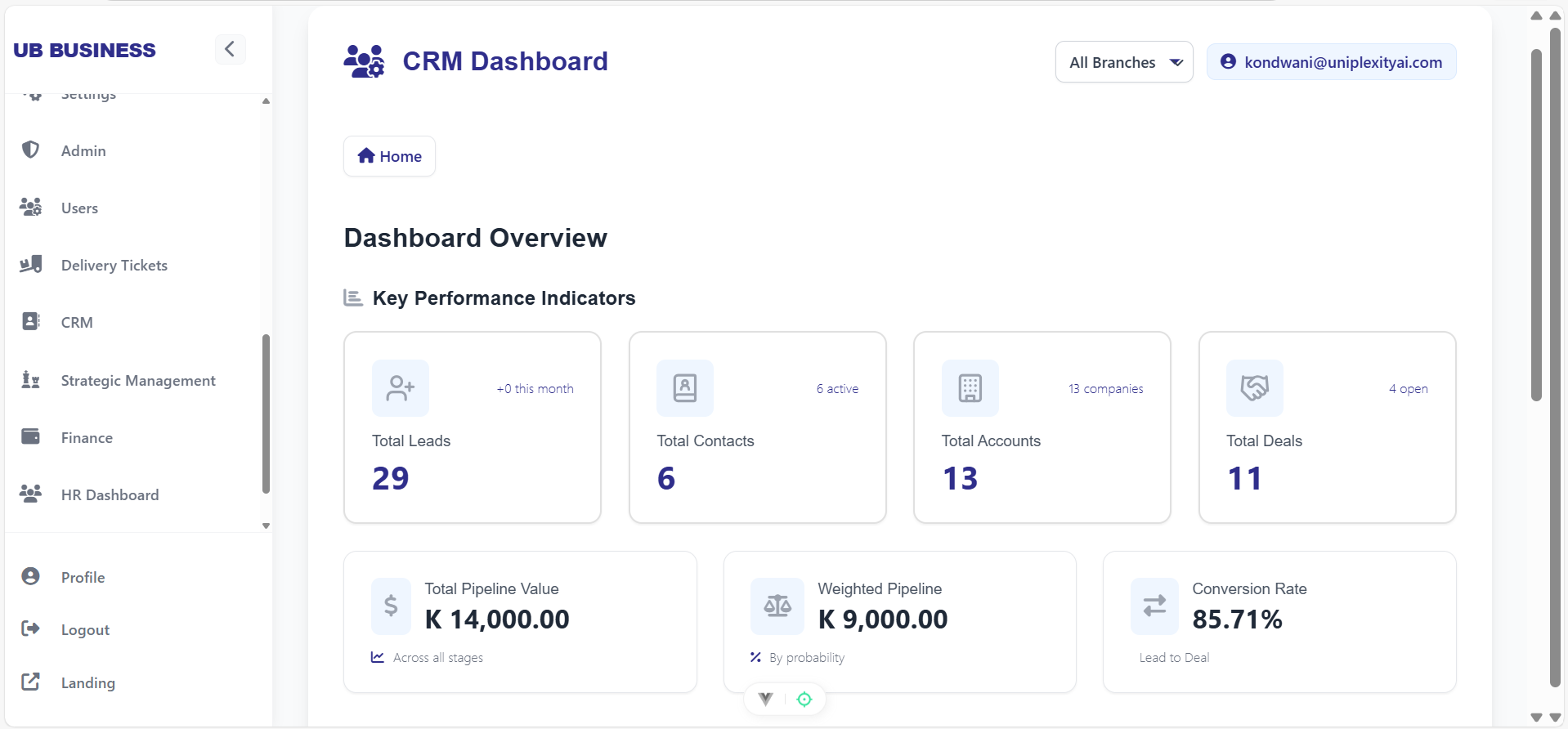

crm

-

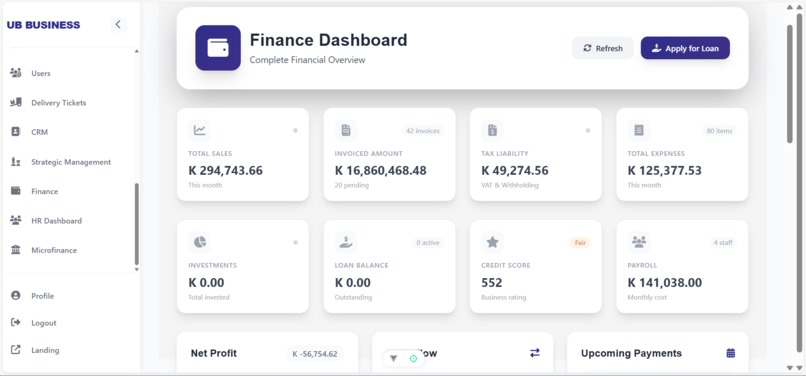

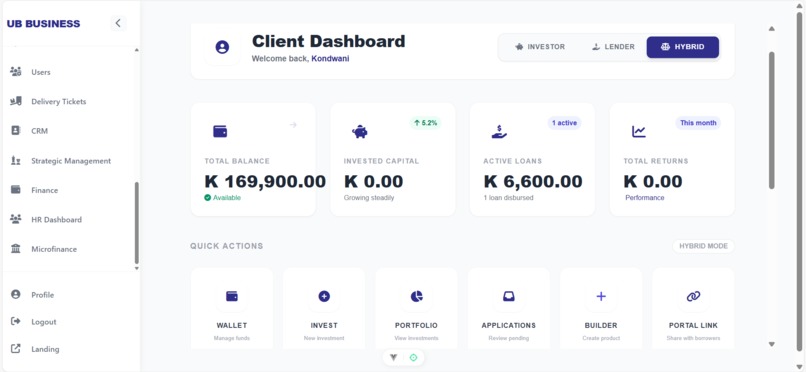

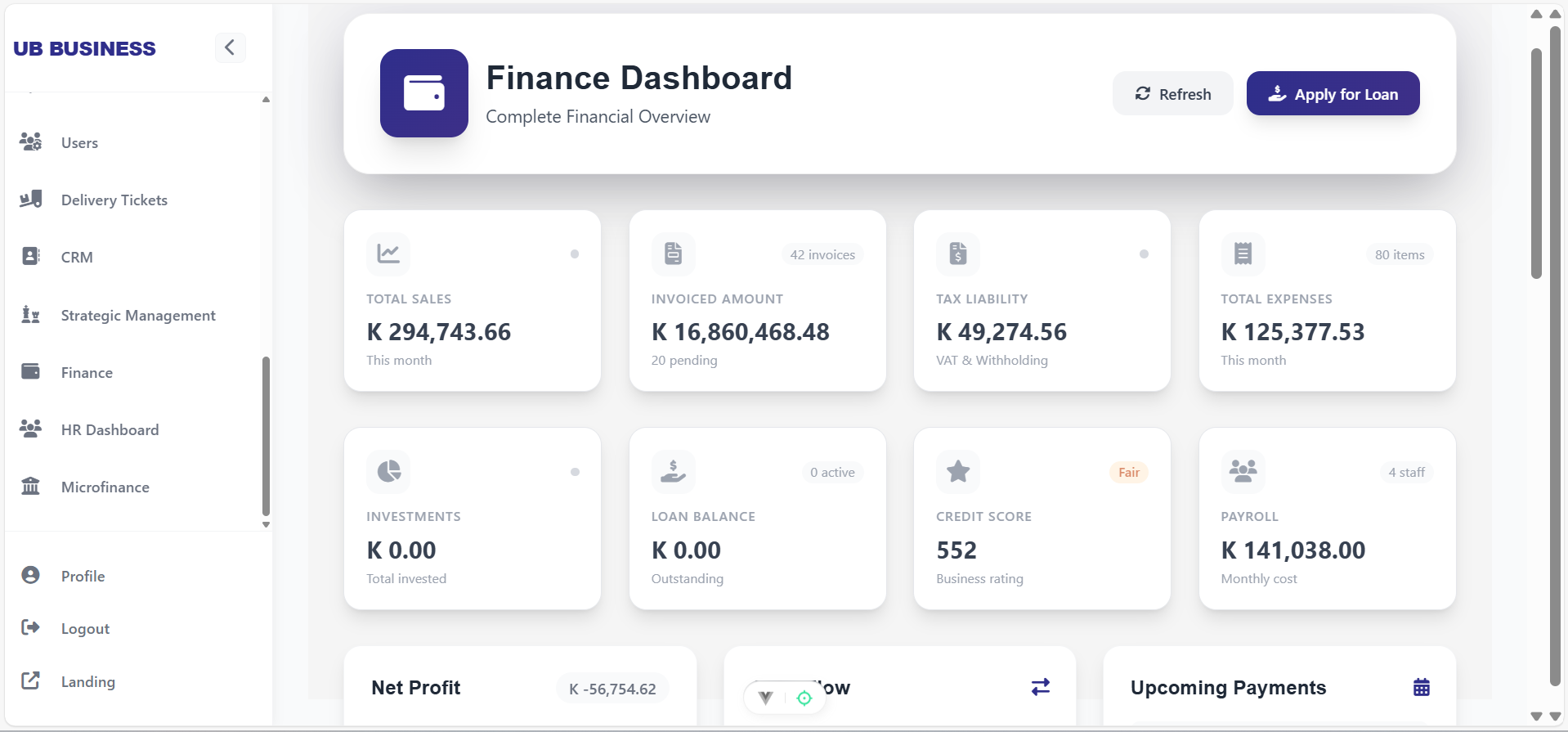

finance

-

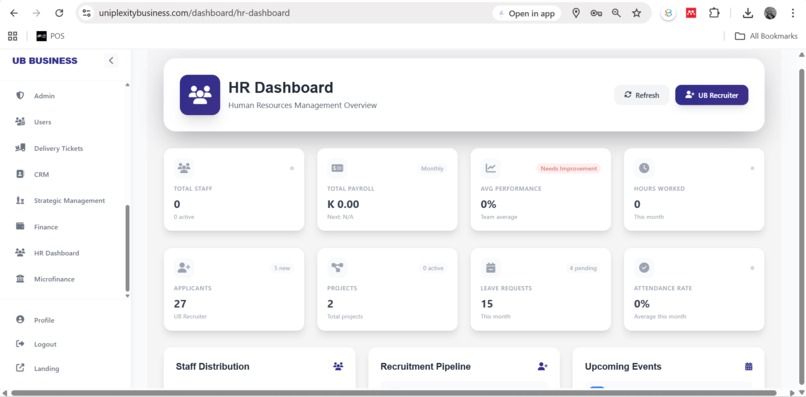

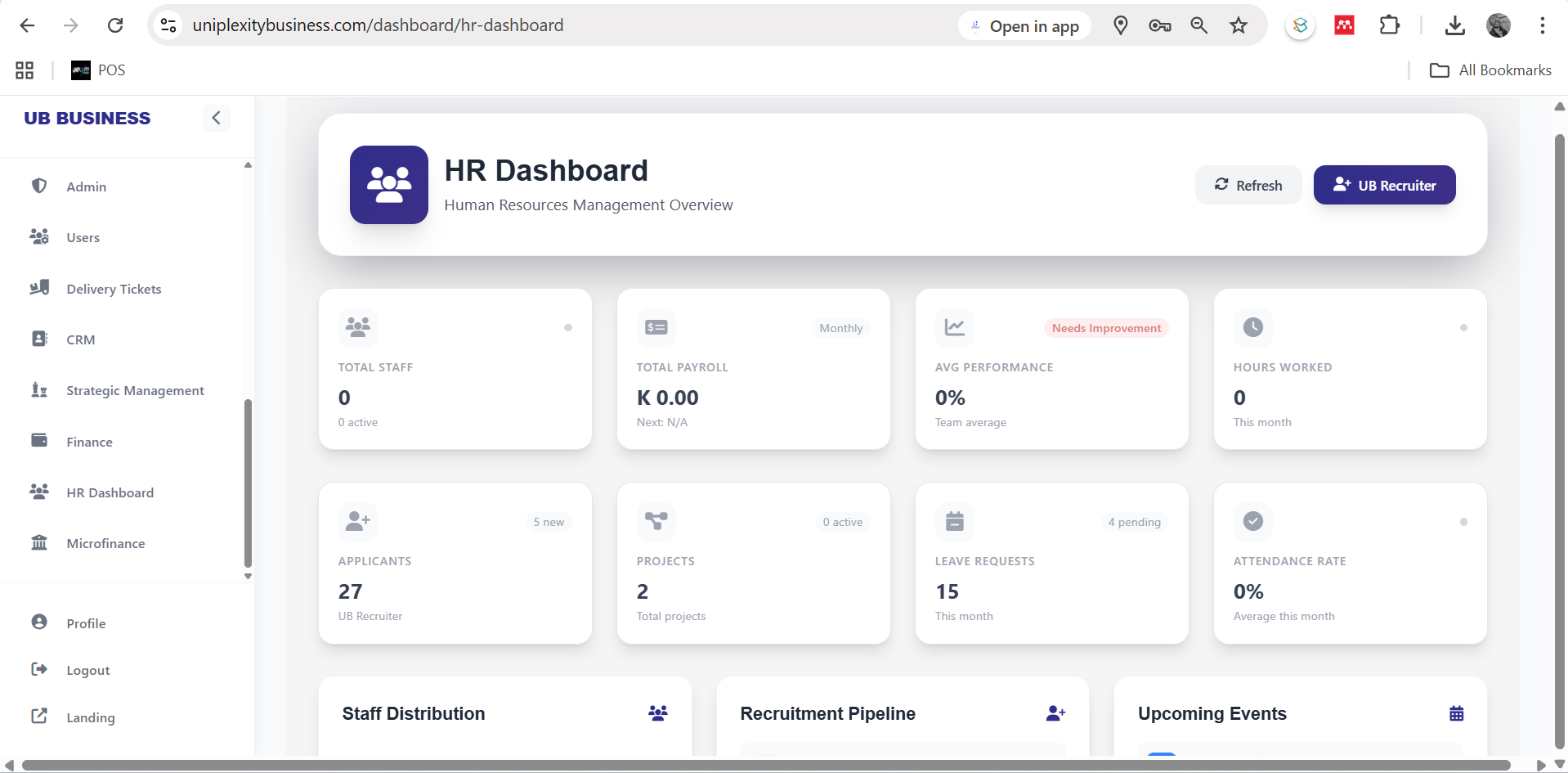

hr

-

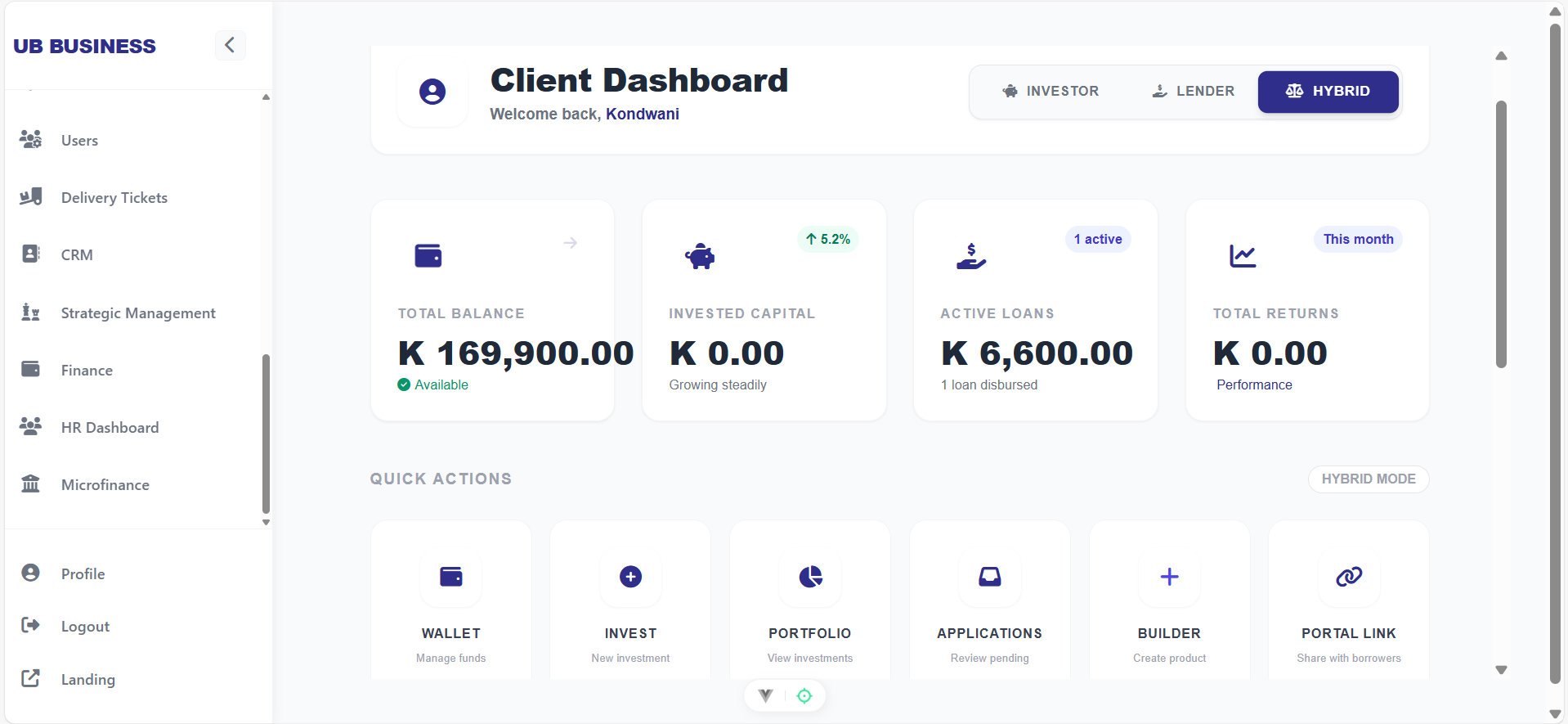

microfinance

-

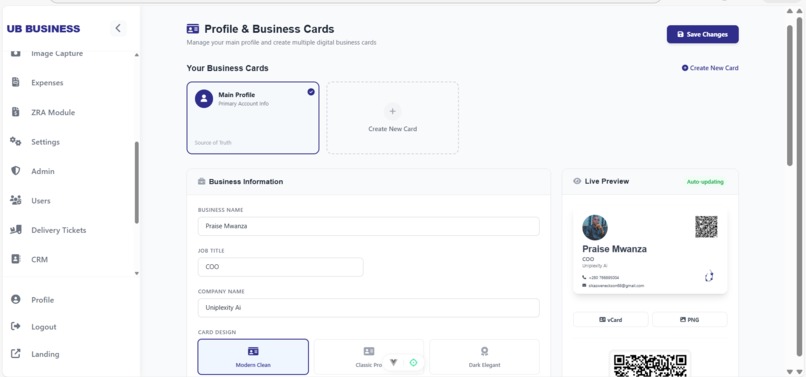

digital cards

-

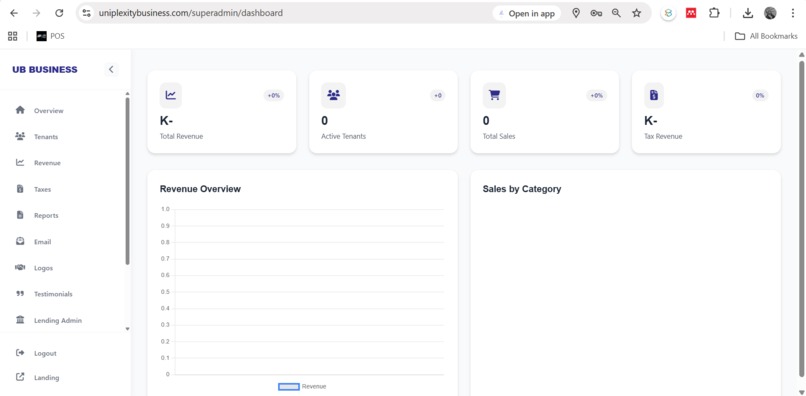

super admin

Inspiration

Small and medium enterprises (SMEs) are the backbone of emerging economies, contributing over 80% of employment and more than 50% of GDP across Africa. Yet despite their economic importance, the vast majority remain financially invisible.

In Zambia, only about 4% of SMEs are formally registered, and even fewer maintain lender-grade financial records. This does not mean the remaining 96% are unviable or risky. It means the financial system was never designed to see how they actually operate.

From working directly with startups, informal traders, cooperatives, and early-stage enterprises, we observed a persistent pattern:

- Businesses operate daily, generate revenue, pay workers, move inventory, and serve customers

- But their records are fragmented across notebooks, WhatsApp messages, mobile money statements, POS receipts, delivery notes, and photos

- None of this data fits neatly into traditional underwriting requirements such as audited financial statements, collateral, or formal registration

On the other side, lenders face strict regulatory and risk constraints. They are forced to rely on static, paper-based indicators that systematically exclude otherwise healthy businesses.

The result is a structural mismatch:

- SMEs are judged as “high risk” not because they are risky, but because they are invisible

- Lenders want to lend, but cannot justify decisions without verifiable data

This gap between real economic activity and formal credit assessment is what inspired Uniplexity Business.

What It Does

Uniplexity Business is an AI-powered ERP and lending infrastructure that captures how a business actually operates and converts that behavior into trusted, low-risk credit signals for SME financing.

Unlike traditional loan platforms that begin at the moment of application, Uniplexity starts months earlier by becoming part of the SME’s daily operations.

At its core, Uniplexity is a lightweight, modular ERP system designed specifically for informal and semi-formal SMEs. It aggregates and structures operational data across the following layers:

Operational Layers We Capture

- Finance: transactions, cash-flow patterns, invoices, loan repayments

- HR: workforce activity, attendance, payroll regularity

- POS: sales volume, frequency, seasonality, customer flow

- Inventory: stock movement, turnover rates, shrinkage patterns

- Logistics: delivery tickets, fulfillment consistency, supplier relationships

- Media & Documents: images of receipts, contracts, delivery notes, operational evidence

This data is continuously timestamped, normalized, and stored, creating a living operational history of the business.

The AI Credit Intelligence Layer

Where the real innovation lies

Uniplexity’s AI engine transforms raw operational data into explainable, behavior-based credit intelligence, enabling lenders to move beyond paperwork.

The system:

- Generates dynamic credit profiles that evolve with business performance

- Measures consistency, resilience, and growth trends, not just snapshots

- Identifies early risk signals such as declining sales frequency or inventory stagnation

- Produces transparent, auditable risk scores suitable for regulated lenders

This enables:

- Faster loan origination

- Risk-based pricing rather than blanket high interest rates

- Continuous post-disbursement monitoring instead of blind lending

For SMEs, Uniplexity replaces fragmented record-keeping with a single system that improves structure, credibility, and finance readiness.

For lenders, it provides a live, real-world view of business performance—far more predictive than static documents.

What Makes Uniplexity Different

Uniplexity is not a marketplace, not a loan app, and not a standalone ERP.

It is financial infrastructure.

Our model is unique because:

- We monetize infrastructure usage, not loan volume

- We create value before lending occurs, reducing acquisition and default risk

- We generate proprietary operational datasets that compound over time

- We align incentives:

\[ \text{SMEs improve operations} \rightarrow \text{Lenders reduce risk} \rightarrow \text{System strengthens} \]

Unlike traditional credit scoring or fintech lending apps, Uniplexity:

- Does not depend on formal registration as a starting point

- Does not replace lenders it empowers them

- Does not lock SMEs into debt it prepares them for sustainable finance

This creates high switching costs, deep data moats, and long-term institutional partnerships.

How We Built It

We built Uniplexity as a desktop-based, modular ERP platform with an integrated AI lending layer, optimized for environments with inconsistent connectivity and diverse business maturity levels.

Core Components

Multi-source data ingestion layer

Aggregates structured and unstructured data from finance, POS, HR, inventory, logistics, and imagesERP standardization engine

Cleans, timestamps, and converts operational events into lender-grade recordsAI risk & analytics engine

Translates operational behavior into credit insights and explainable scoresLender-facing dashboard

Enables underwriting, monitoring, portfolio analytics, and early risk detectionSME-facing interface

Helps businesses understand performance, compliance readiness, and credit health

The architecture is designed for scalability, auditability, and seamless integration into existing lending workflows without forcing lenders to change how they operate.

Challenges We Ran Into

1. Data Standardization

Informal data is messy, inconsistent, and incomplete. We focused on behavioral patterns over perfection, prioritizing frequency, consistency, and trends rather than accounting purity.

2. AI Explainability

Black-box credit models fail regulatory scrutiny. We built explainable risk outputs that clearly show why a business is scored a certain way, grounded in observable operations.

3. Dual-User Design

Most platforms serve either lenders or SMEs not both. Uniplexity is deliberately designed as shared infrastructure, where SMEs gain ERP value and lenders gain risk intelligence.

These challenges shaped Uniplexity into a product that prioritizes trust, adoption, and real-world usability.

Accomplishments We’re Proud Of

- Built a working ERP capturing real operational behavior across multiple SME functions

- Developed an AI-driven credit intelligence layer grounded in daily business reality

- Reduced friction for SMEs while increasing confidence for lenders

- Positioned Uniplexity as core lending infrastructure, not a consumer fintech product

What We Learned

- SMEs already generate valuable data it is just unstructured and ignored

- Operational consistency is often a stronger predictor of repayment than collateral

- Trust at scale requires systems, not relationships

- ERP + AI is not about automation it is about credibility

What’s Next for Uniplexity Business

In the next phase, we will:

- Pilot Uniplexity ERP with SME lenders, MFIs, and loan originators

- Introduce sector-specific operational benchmarks (retail, transport, agriculture, services)

- Link ERP data to formalization, compliance, and registration workflows

- Scale adoption to help raise SME formalization from ~4% to 12%, unlocking billions in dormant credit demand

Our Long-Term Vision

We believe that operational performance not paperwork should define creditworthiness.

Uniplexity’s long-term vision is to make ERP-driven, behavior-based credit assessment the global standard for SME lending starting in Africa and scaling to every emerging market where businesses are real, but invisible.

Log in or sign up for Devpost to join the conversation.