About the Project

Inspiration

Stock price prediction is a challenging problem due to market volatility and complex time-series patterns. I was inspired to explore how deep learning, especially LSTM neural networks, can capture long-term dependencies that traditional models fail to handle.

What I Learned

Through this project, I gained hands-on experience with:

- Time-series data preprocessing and feature scaling

- Designing and training LSTM-based deep learning models

- Evaluating models using metrics like RMSE, MAE, and R²

- Working with real-world financial data from Yahoo Finance

How I Built the Project

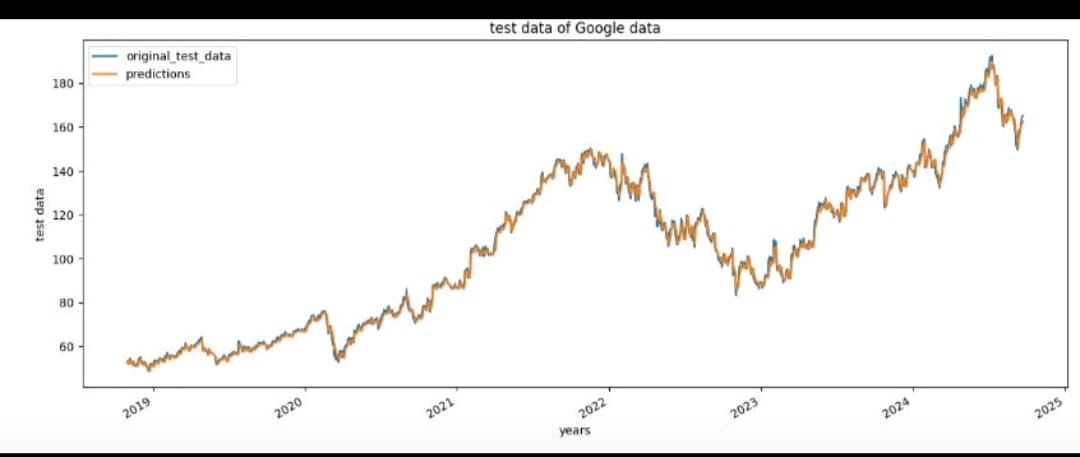

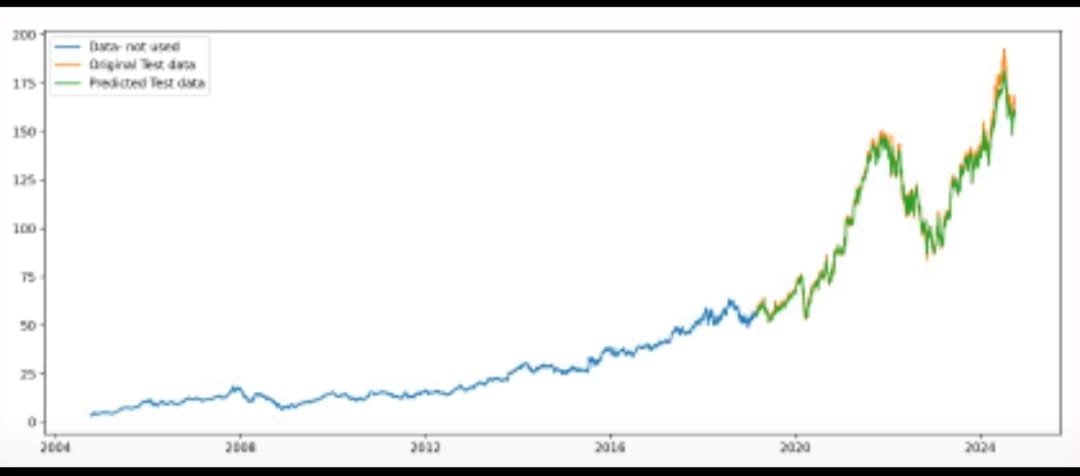

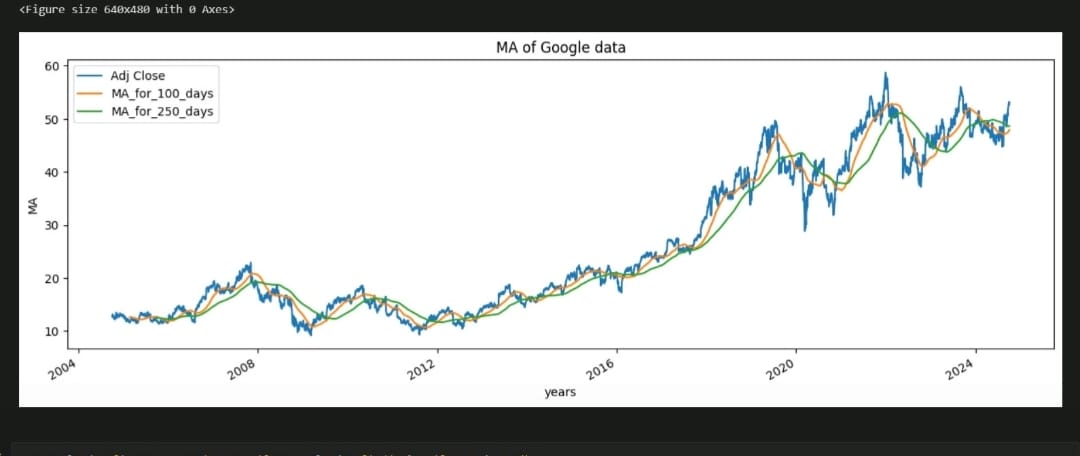

I collected 20 years of historical stock price data for Google and Cisco. The data was cleaned, normalized using MinMaxScaler, and split into training and testing sets.

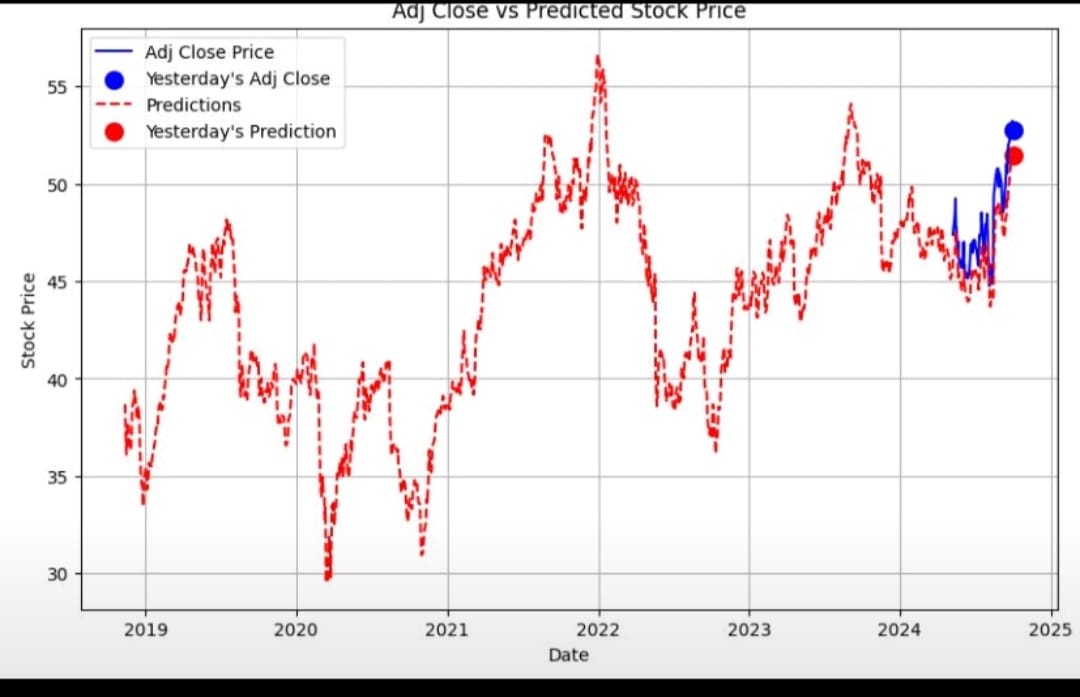

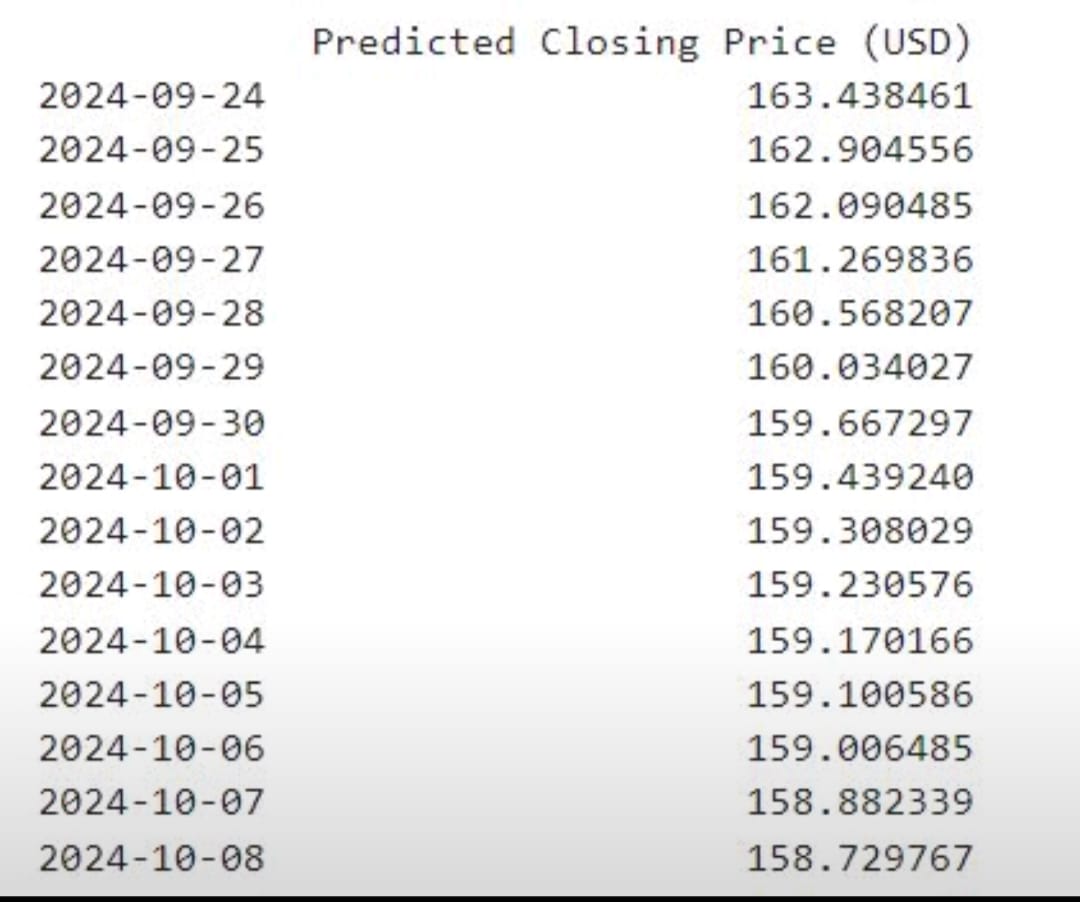

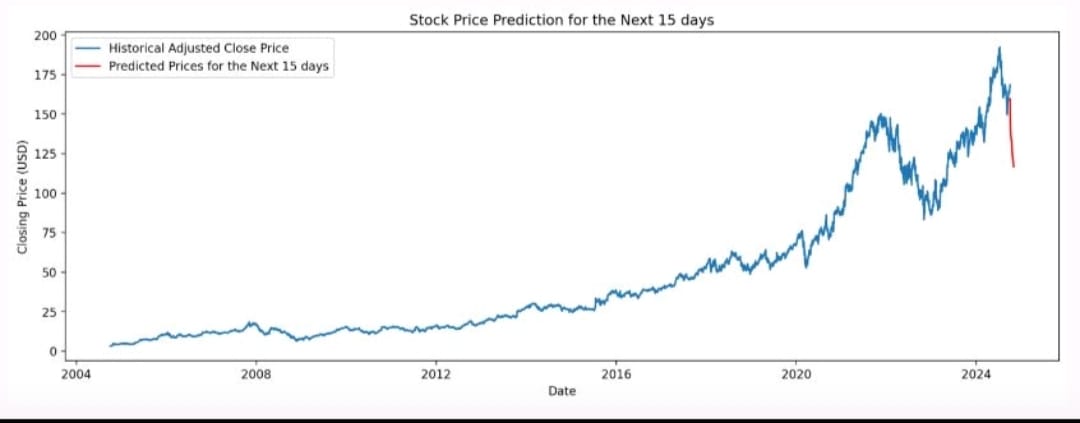

The model architecture consists of stacked LSTM layers, followed by Dense layers and Dropout for regularization. The model predicts future stock prices based on sequential input data.

The loss function was minimized during training, and performance was evaluated using: [ RMSE = \sqrt{\frac{1}{n} \sum_{i=1}^{n} (y_i - \hat{y}_i)^2} ]

Challenges Faced

- Handling noisy and volatile stock market data

- Preventing overfitting in deep learning models

- Selecting optimal hyperparameters such as sequence length and number of LSTM units

- Balancing model accuracy with computational efficiency

Outcome

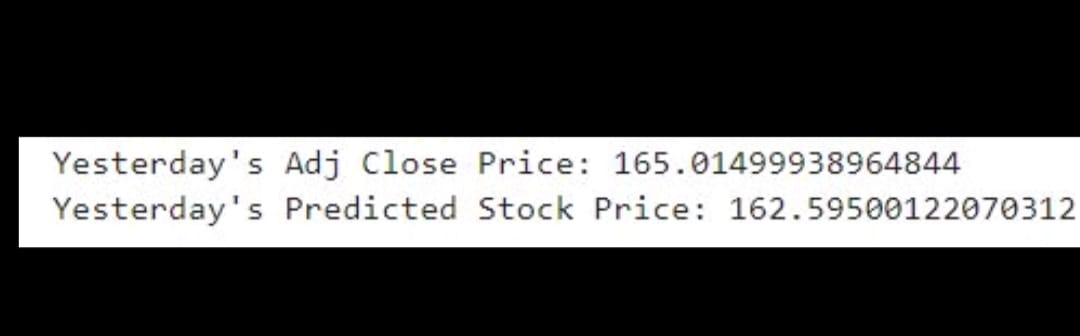

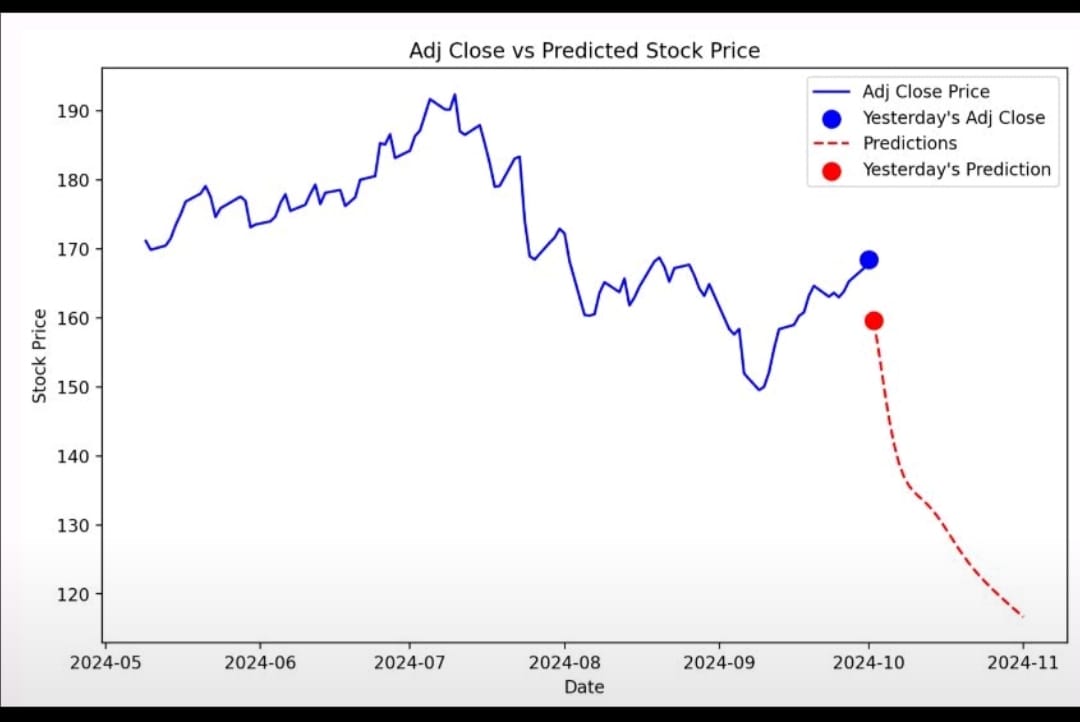

The final model successfully captured both upward and downward trends in stock prices and achieved low RMSE values, demonstrating the effectiveness of LSTM networks for financial time-series prediction. This project strengthened my understanding of applied machine learning in real-world scenarios.

Built With

- ai

- lstm

- ml

- python

- streamlit

- yahoo-finance

Log in or sign up for Devpost to join the conversation.