Inspiration

Looked at existing stable coin implementations and research:

makerDAO

SchellingDollar (https://blog.ethereum.org/2014/11/11/search-stable-cryptocurrency/)

Seignorage Shares (https://github.com/rmsams/stablecoins)

- Investigate and prototype various stable coin approaches.

- Must not require a token that needs to be separately distributed (e.g. no ICO).

- Must be fully decentralised, apart from the pricing oracle (which could be replaced by e.g. a Uniswap / Kyber based DAI / ETH oracle, or a SchellingCoin implementation).

- Must be a novel approach.

What it does

Two approaches prototyped - Seignorage Shares and Socialised CDPs

Seignorage Shares

Implemented a version of Seignorage Shares which:

- Allows anyone to deposit ETH

- Convert ETH < = > USD using the MakerDAO oracle

- Withdraw up to the amount of ETH deposited

- Send / receive USD across different parties

Comments:

- In order for their to be demand for USD (to unlock collateral) ETH needs to move both up and down (to create both credit and deficits in the USD token)

- Simple scheme - easy to reason about, but possible for the “bank” to become insolvent in a continually falling market

- Does not allow leveraging

- Does not require over-collateralisation

- Fully decentralised / public good stable coin - no ICO, no token.

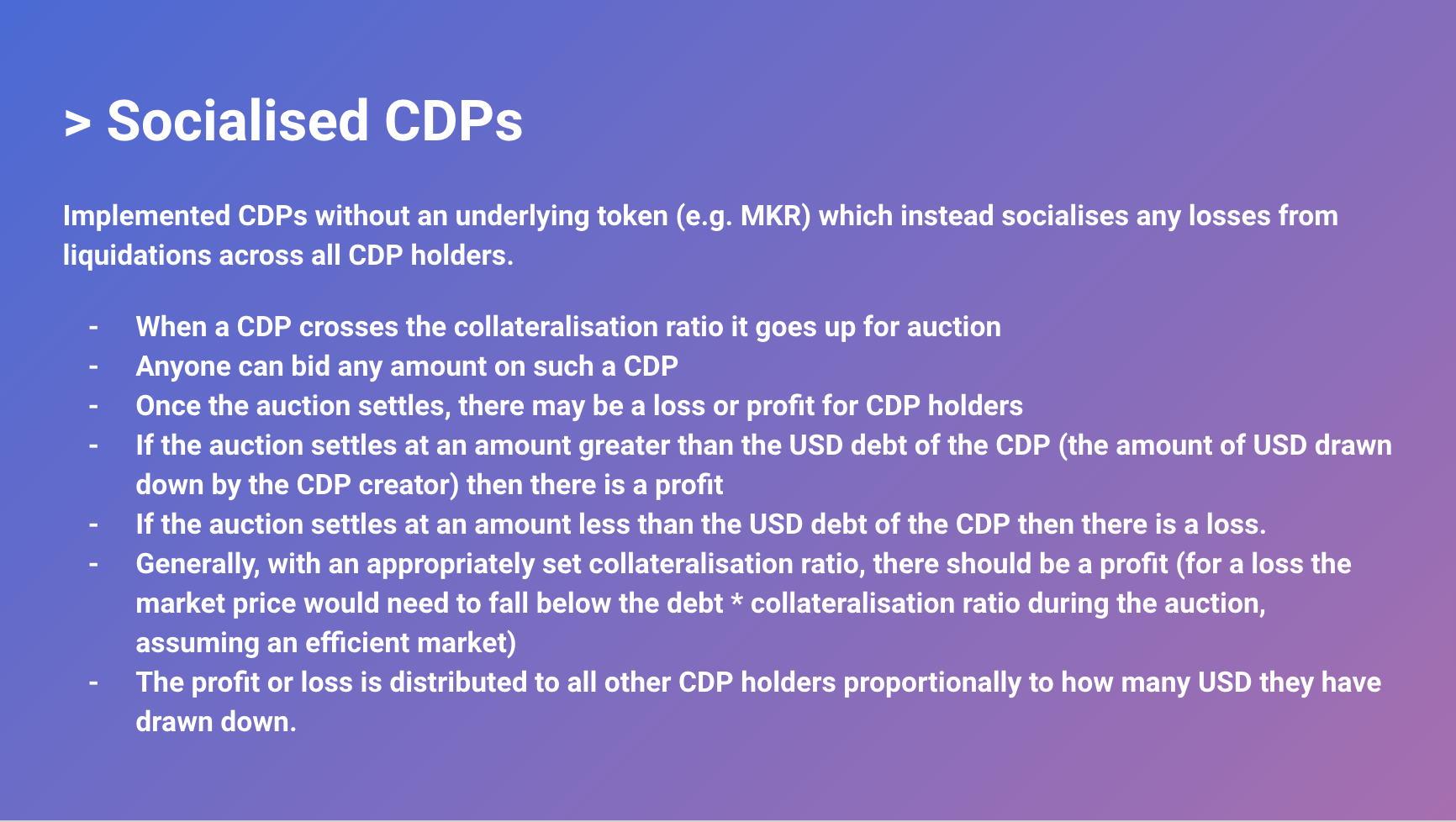

Socialised CDPs

Implemented CDPs without an underlying token (e.g. MKR) which instead socialises any losses from liquidations across all CDP holders:

- When a CDP crosses the collateralisation ratio it goes up for auction

- Anyone can bid any amount on such a CDP

- Once the auction settles, there may be a loss or profit for CDP holders

- If the auction settles at an amount greater than the USD debt of the CDP (the amount of USD drawn down by the CDP creator) then there is a profit

- If the auction settles at an amount less than the USD debt of the CDP then there is a loss.

- Generally, with an appropriately set collateralisation ratio, there should be a profit (for a loss the market price would need to fall below the debt * collateralisation ratio during the auction, assuming an efficient market)

- The profit or loss is distributed to all other CDP holders proportionally to how many USD they have drawn down.

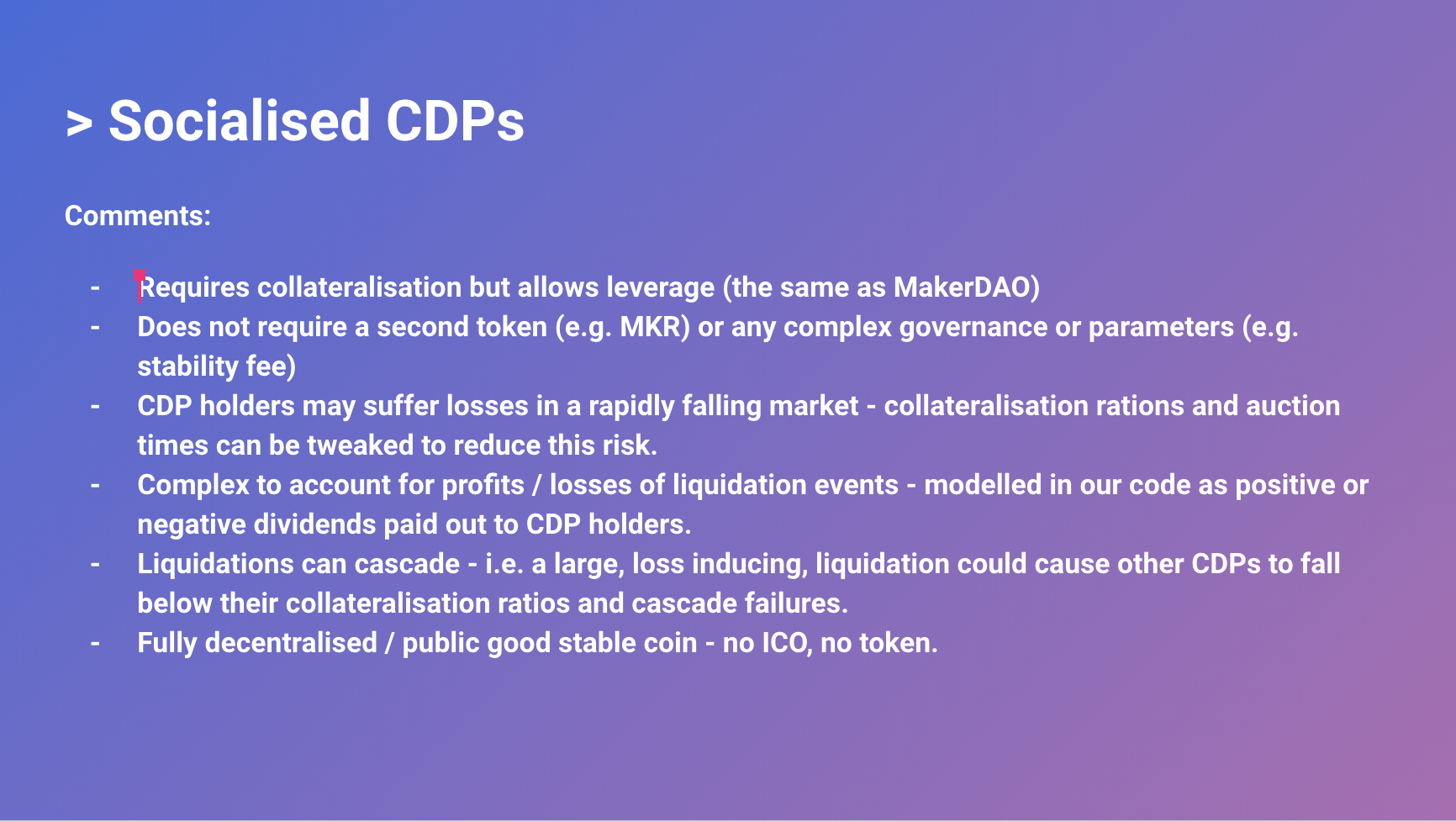

Comments:

- Requires collateralisation but allows leverage (the same as MakerDAO)

- Does not require a second token (e.g. MKR) or any complex governance or parameters (e.g. stability fee)

- CDP holders may suffer losses in a rapidly falling market - collateralisation rations and auction times can be tweaked to reduce this risk.

- Complex to account for profits / losses of liquidation events - modelled in our code as positive or negative dividends paid out to CDP holders.

- Liquidations can cascade - i.e. a large, loss inducing, liquidation could cause other CDPs to fall below their collateralisation ratios and cascade failures.

- Fully decentralised / public good stable coin - no ICO, no token.

Challenges we ran into

Interpreting game theoretic properties of approaches under various market conditions (market trends, volatility).

Coming up with novel variations on existing approaches that prioritised simplicity over multi-token models.

Accomplishments that we're proud of

Two novel approaches prototyped for discussion amongst the wider community.

What we learned

Analysing game theoretic approaches of stable coins is hard!

What's next for StableCoins

We will publish our two novel approaches and prototyped code then invite community discussion / iteration. Stable coins as a public good with minimum governance and no requirement for a utility token is our aim.

We'll continue researching other models for stable coins.

Log in or sign up for Devpost to join the conversation.