-

-

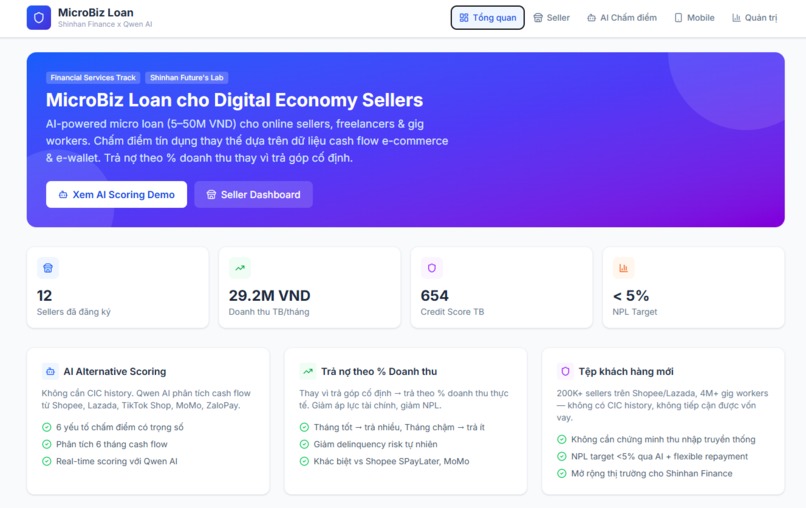

cover

-

open dashboard sf12

-

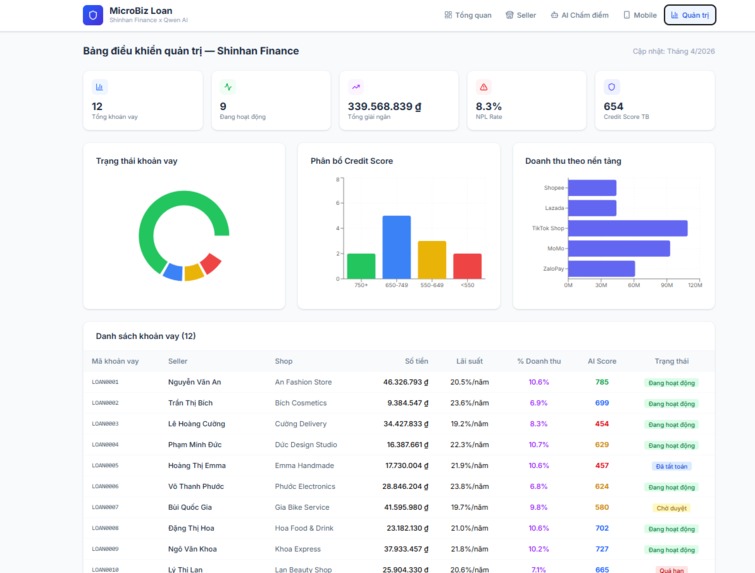

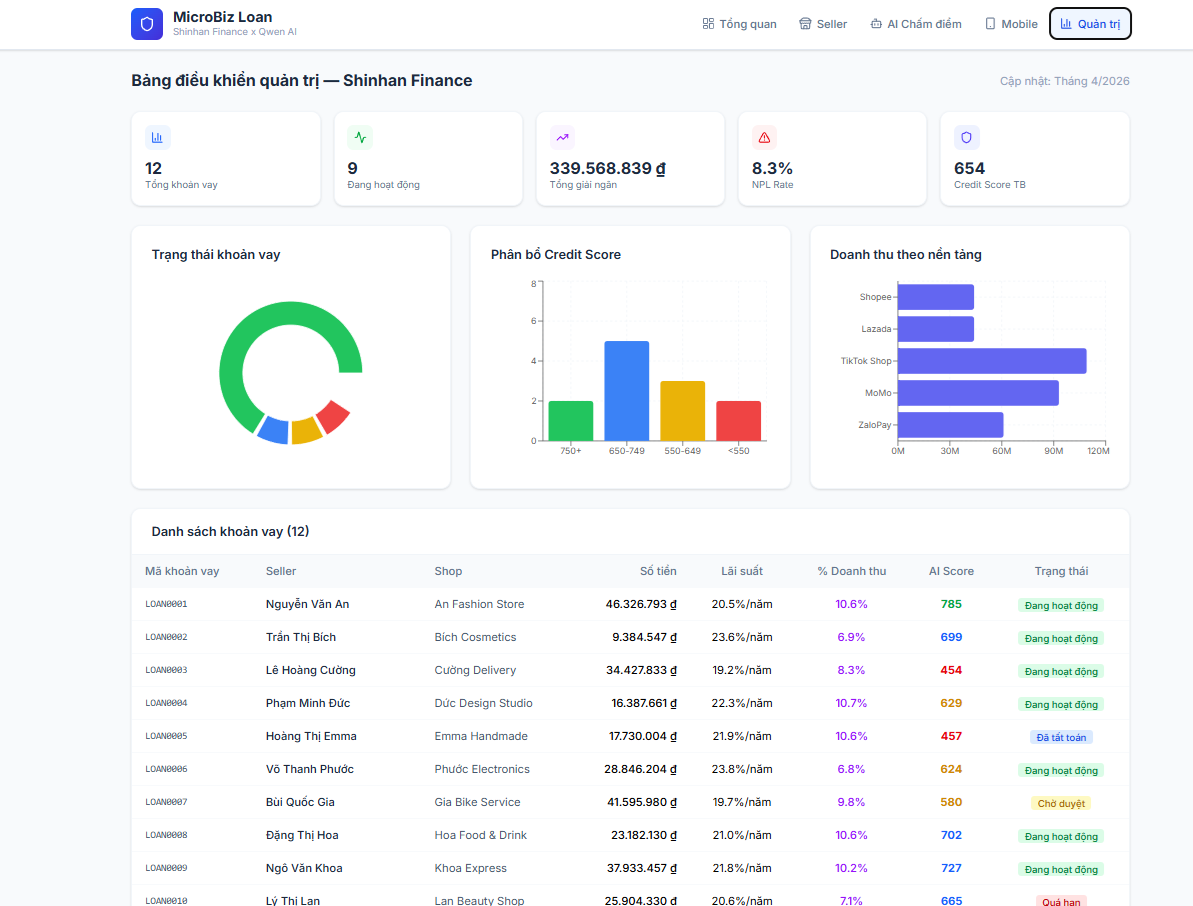

administrator sf12

-

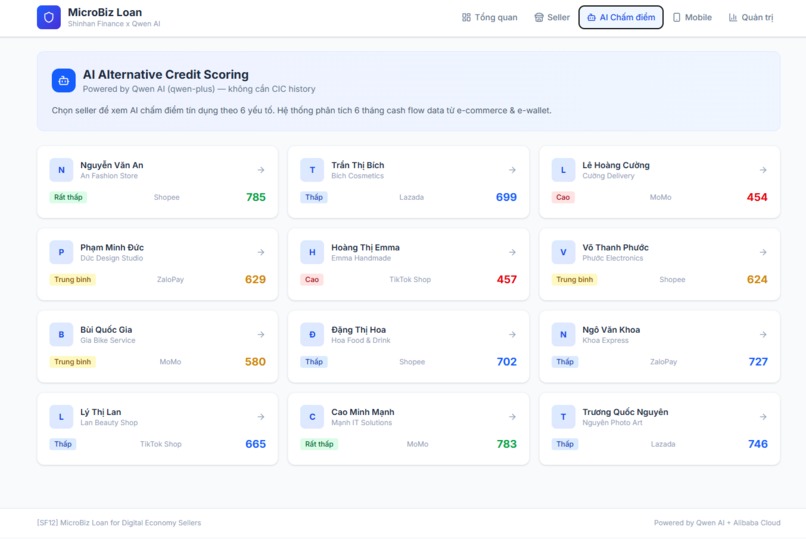

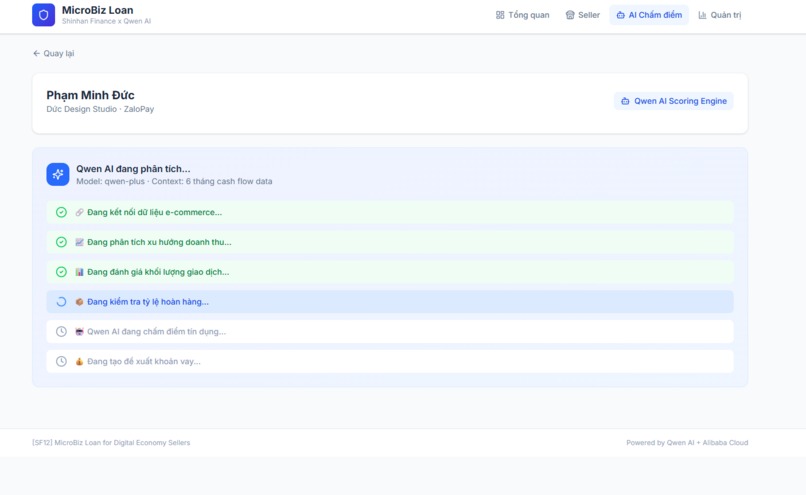

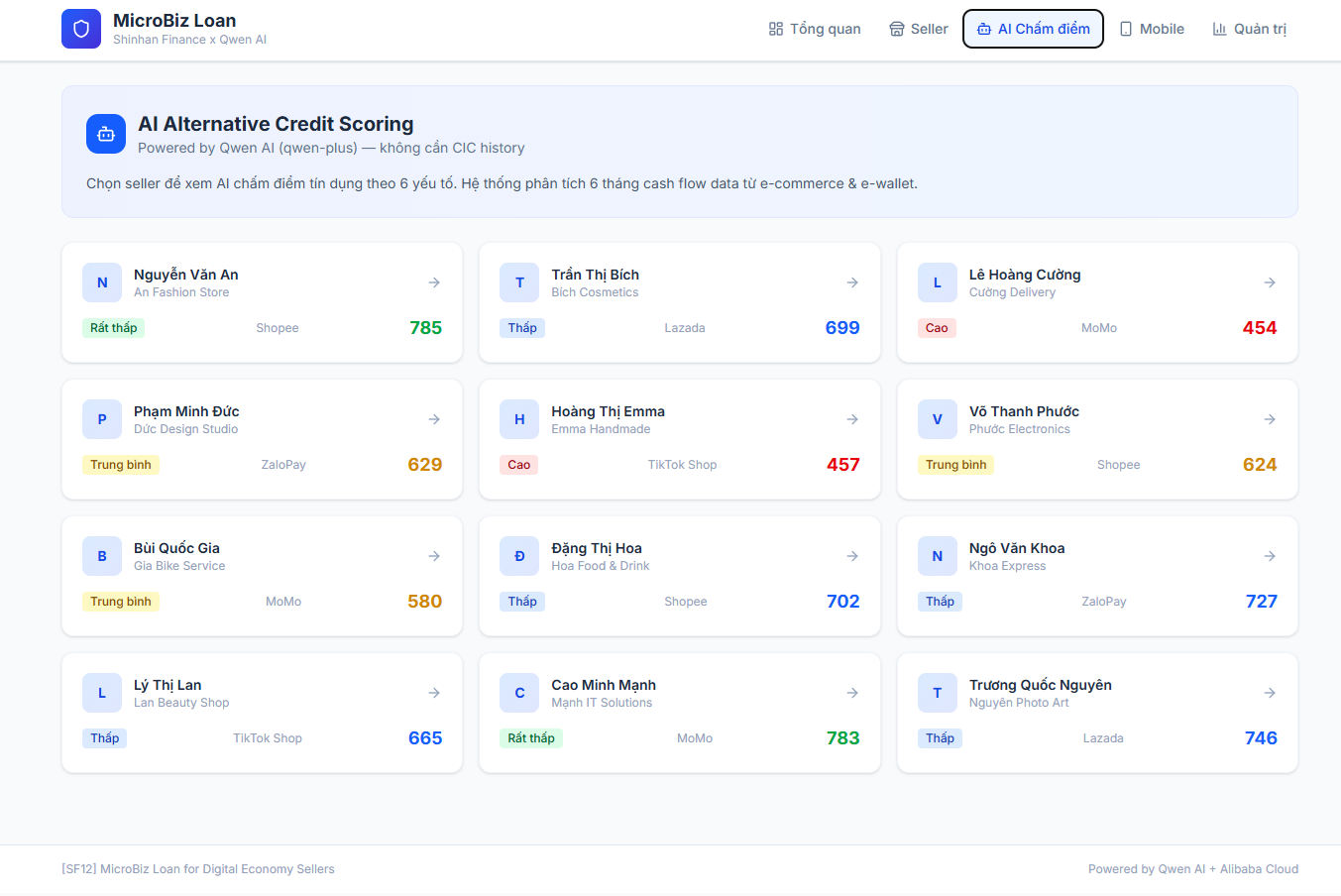

A.I analytic sf12

-

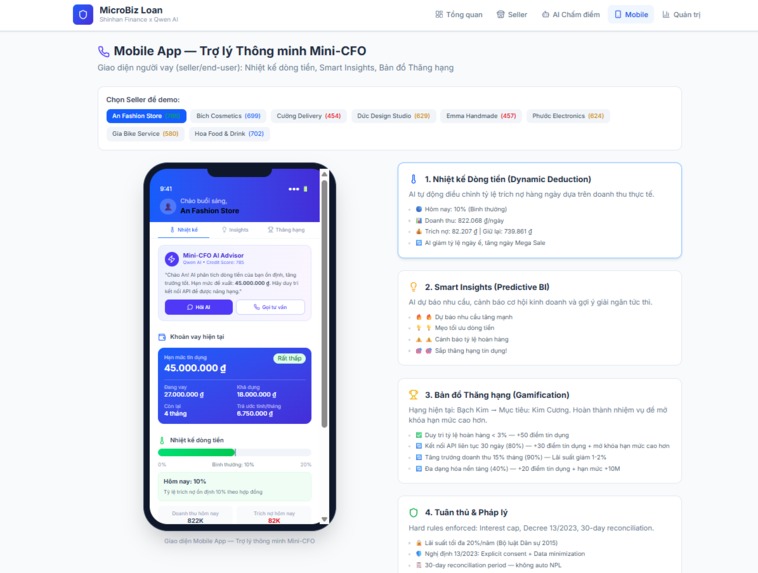

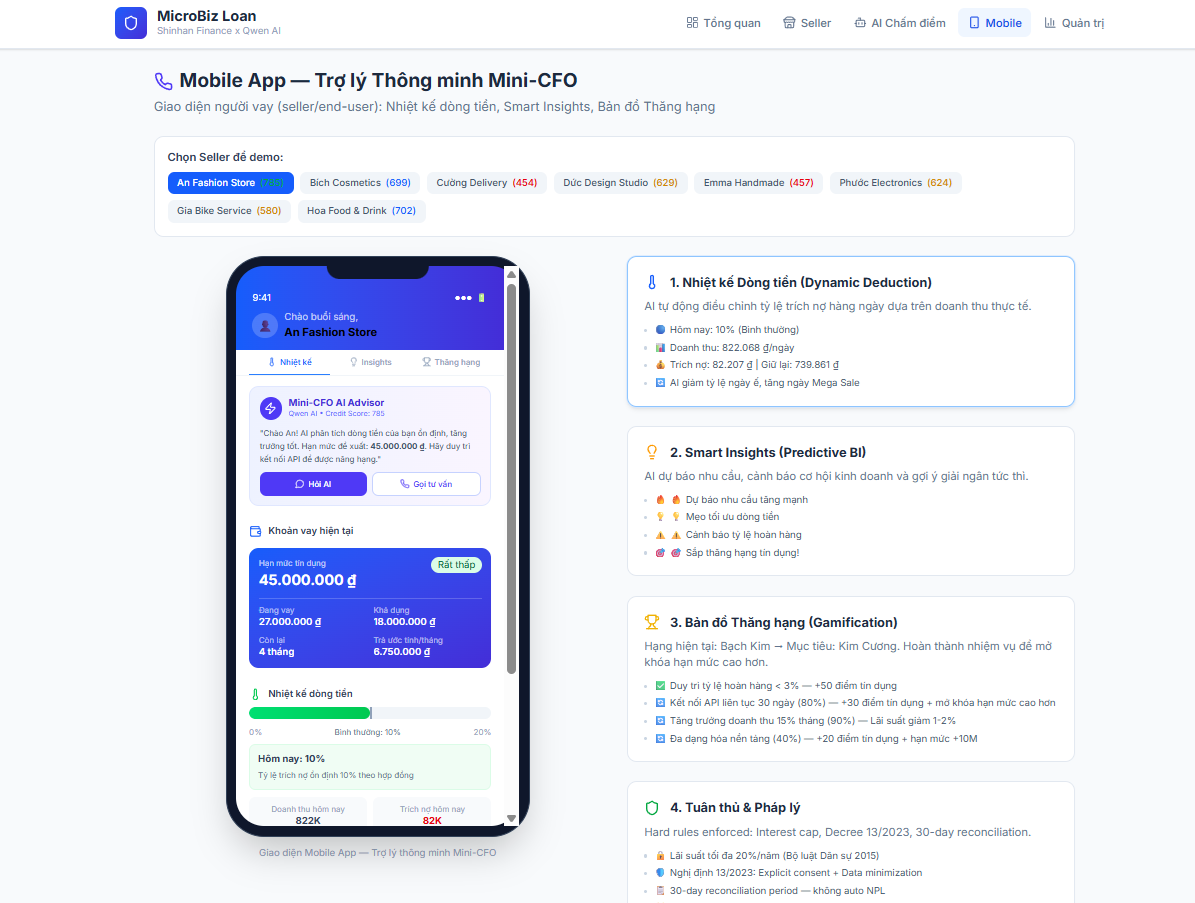

mobile dashboard demo sf12

-

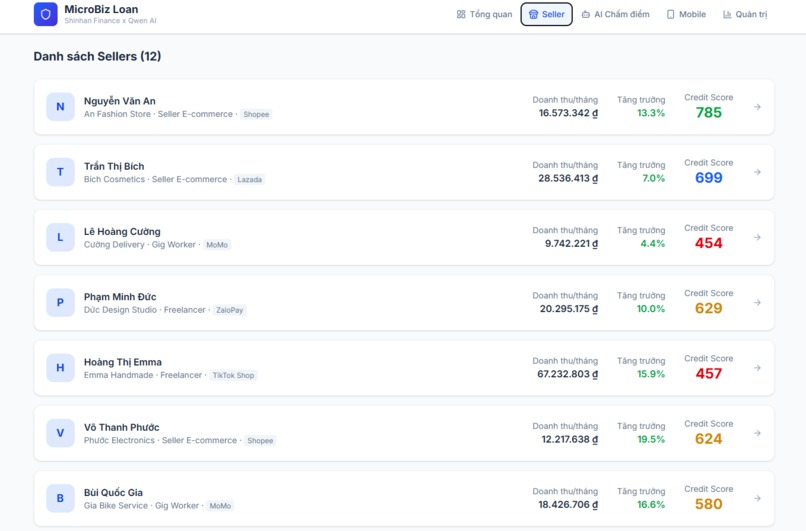

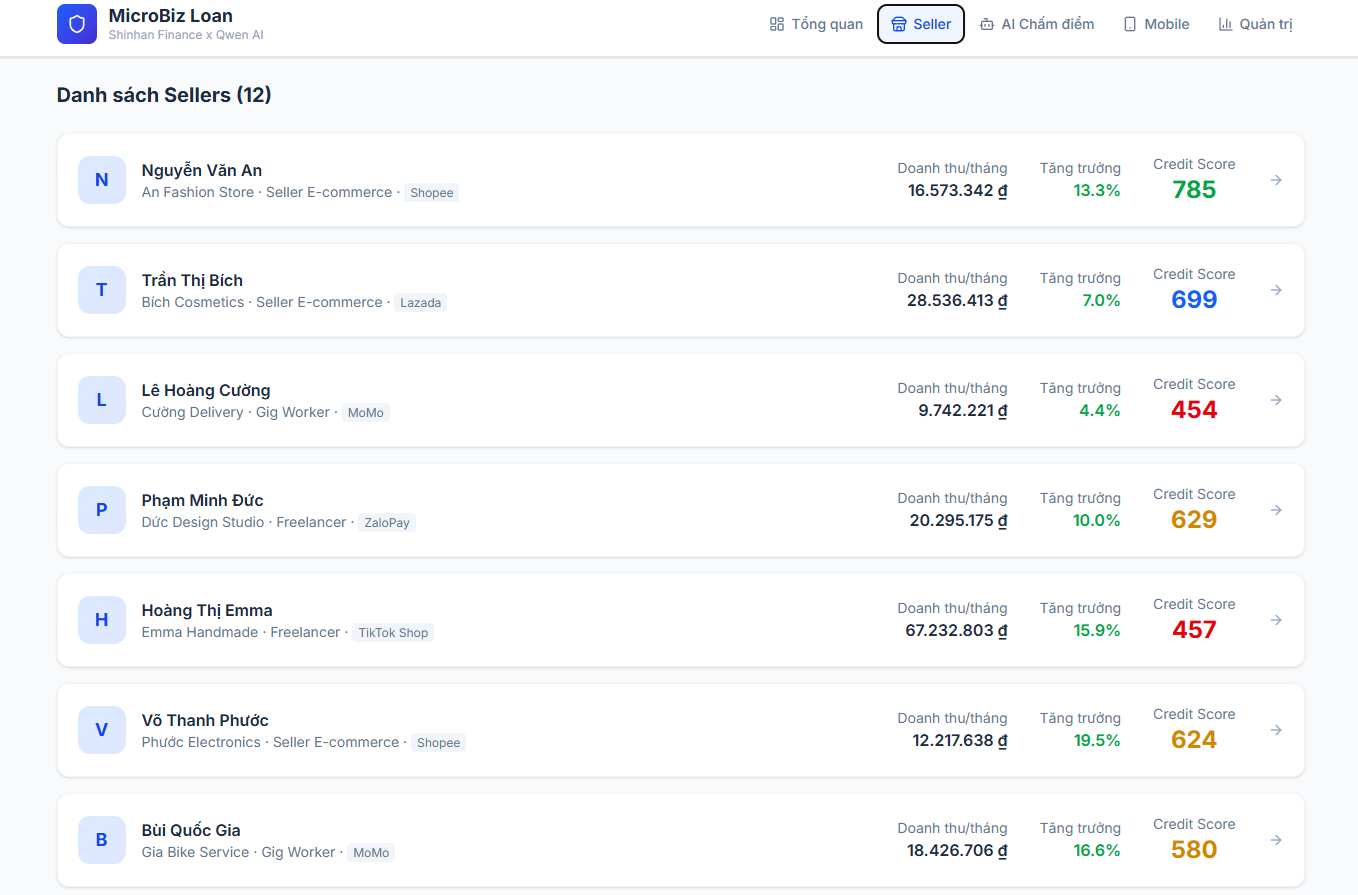

Seller /customer list sf12

-

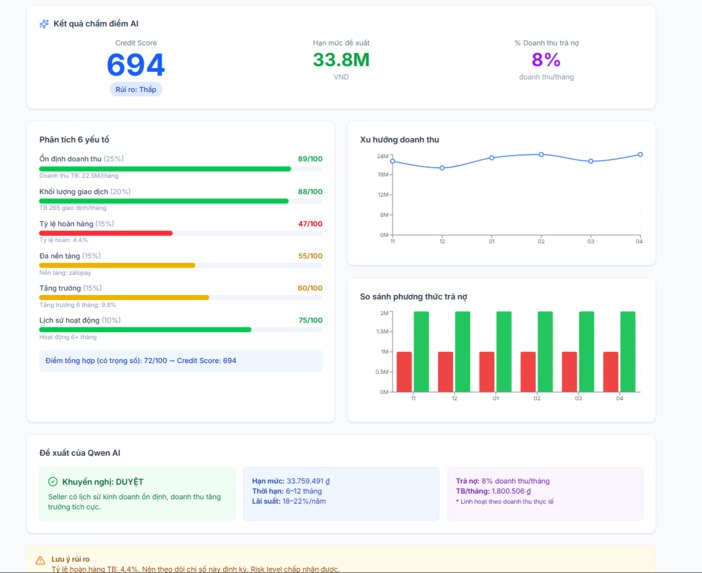

A.I analytic customer score

-

A.I analytic customer summary

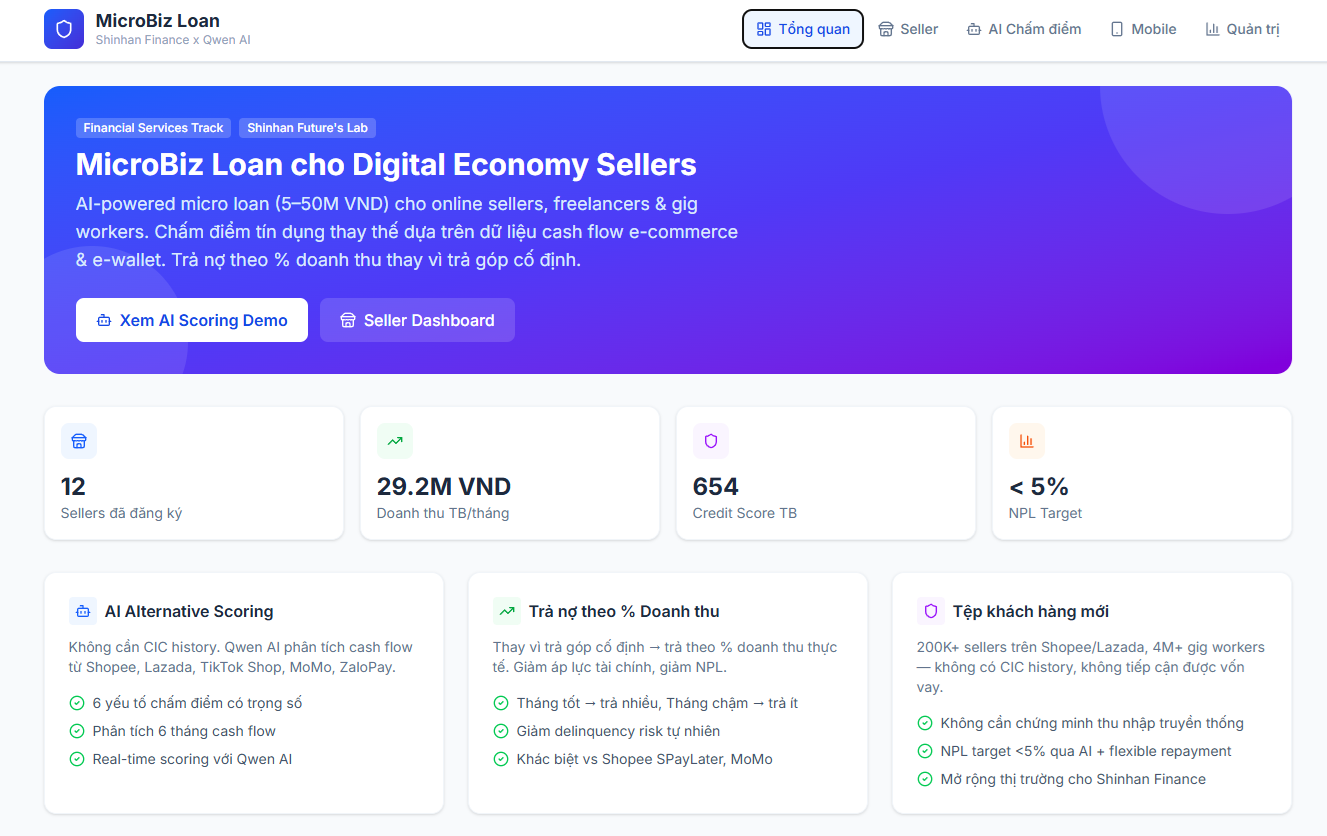

MicroBiz Loan

[SF12] Connects digital economy sellers in Vietnam with working capital using AI-powered alternative credit scoring.

Problem

Online sellers, freelancers, and gig workers are invisible to traditional credit systems. They have no CIC history, no payslips, no tax declarations. When a TikTok Shop seller needs 10M VND to restock before a Mega Sale, banks say "no" because there's no paper trail.

Solution

A "Mini-CFO" for digital economy sellers:

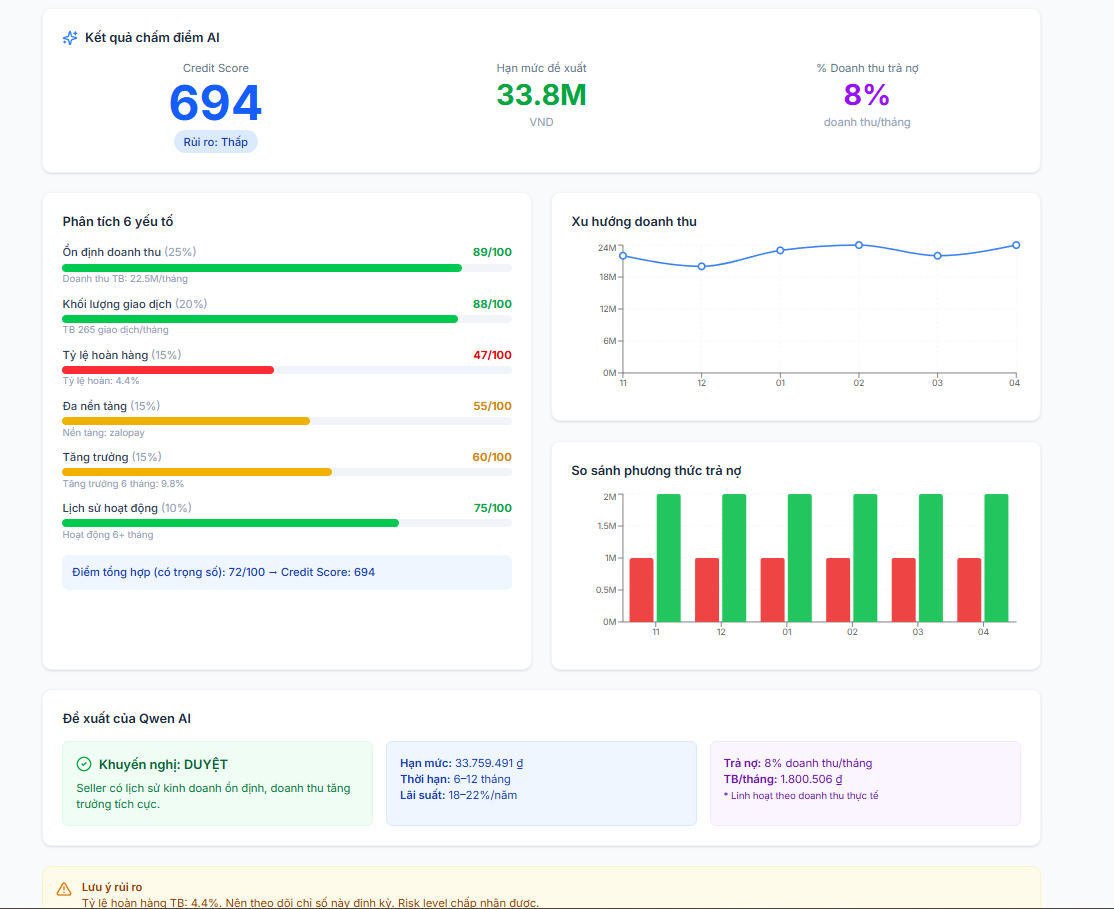

AI Alternative Credit Scoring — No CIC needed. Qwen AI analyzes 6 months of e-commerce cash flow (Shopee, Lazada, TikTok Shop) and e-wallet data (MoMo, ZaloPay) to produce a 300-850 credit score with explainable reason codes.

Revenue-Based Repayment — Borrowers repay as a % of daily revenue instead of fixed installments. On slow days, the deduction auto-adjusts down to preserve working capital. On Mega Sale days, it increases to help them pay off early.

Smart Insights — AI detects demand peaks from historical patterns and alerts sellers: "Your 200-unit stock will run out in 3 days. Trend is +40% this week. Disburse 15M now to capture the surge."

Credit Gamification — Transparent level-up progression. Sellers see exactly what to do to unlock higher limits: maintain refund rate <3%, keep API connected, grow revenue 15% month-over-month.

Admin Risk Dashboard — Portfolio-level view for Shinhan: real-time NPL tracking, credit score distribution, and anomaly detection.

Tech Stack

| Layer | Technology |

|---|---|

| AI Engine | Qwen Plus via DashScope API |

| Backend | FastAPI + SQLAlchemy + SQLite |

| Credit Engine | AI-first scoring + rule-based fallback (6 weighted factors) |

| Frontend | React 19 + Vite + Tailwind CSS + Recharts |

| Data | 50 sellers, 8 months, 500+ cashflow records |

Scoring Factors

| Factor | Weight |

|---|---|

| Revenue consistency | 25% |

| Transaction volume trend | 20% |

| Return/refund rate | 15% |

| Platform diversity | 15% |

| Growth trajectory | 15% |

| Account activity | 10% |

Key Features

- Dual-mode scoring: Qwen AI first, rule-based fallback with 6 weighted factors

- Explainable AI: Every credit decision includes reason codes and weighted factor breakdowns

- Revenue-based repayment simulator: Visual comparison of fixed vs dynamic payment plans

- Animated scoring visualization: 6-step sequential analysis with progress bars

- Vietnamese-localized UI: All labels and platform names in Vietnamese

Challenges Solved

- Structured JSON reliability from LLM — Solved with explicit output format requirements and robust rule-based fallback

- Scoring factor weighting — Balanced 6 factors to produce realistic 300-850 scores with iterative calibration

- Revenue-based repayment math — Built month-by-month projection showing compounding effect of dynamic deductions

- Demo data realism — Multi-stage generator with configurable seeds for believable cash flow patterns

What We Learned

- AI for credit scoring is viable but needs guardrails — LLMs analyze cash flow patterns effectively, but rule-based fallback is essential for production reliability

- Revenue-based financing aligns incentives — When repayment scales with revenue, borrowers don't get crushed during dry spells, and lenders get paid faster during boom periods

- Explainability beats raw accuracy — A 720 score with reason codes is more actionable than a 720 score with no explanation

- Data quality determines everything — Realistic cash flow patterns (seasonality, growth curves, platform quirks) are essential for meaningful scoring

NPL Target: <5%

Achieved through conservative scoring, dynamic deduction caps, and real-time portfolio monitoring.

Built With

- css

- fastapi

- json

- next.js

- postcss

- python

- qwen

- tailwind

- typescript

- vercel

Log in or sign up for Devpost to join the conversation.