-

-

cover

-

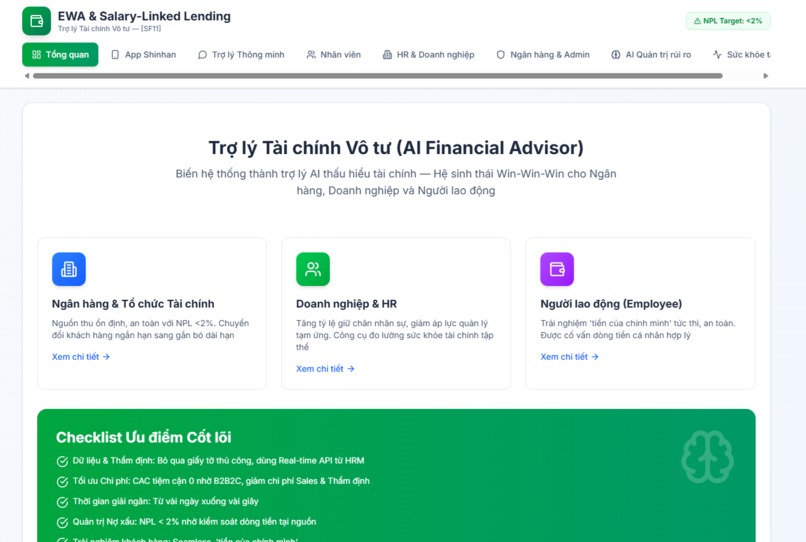

dashboard

-

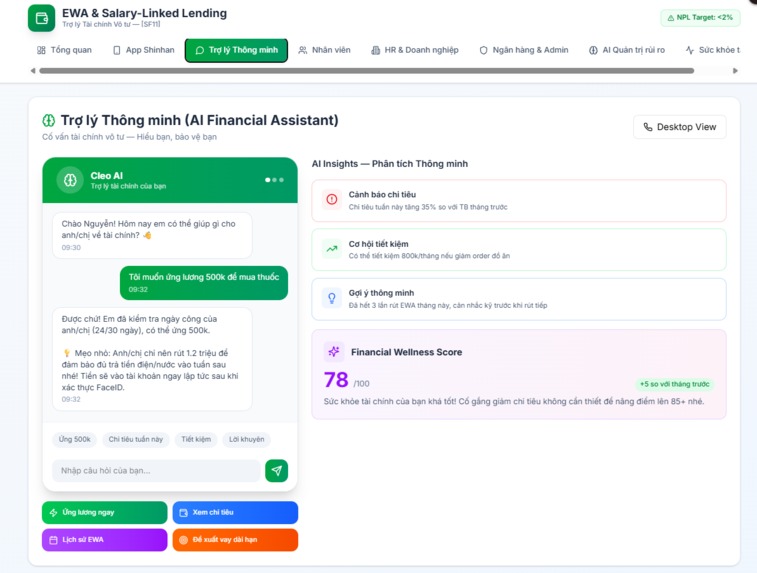

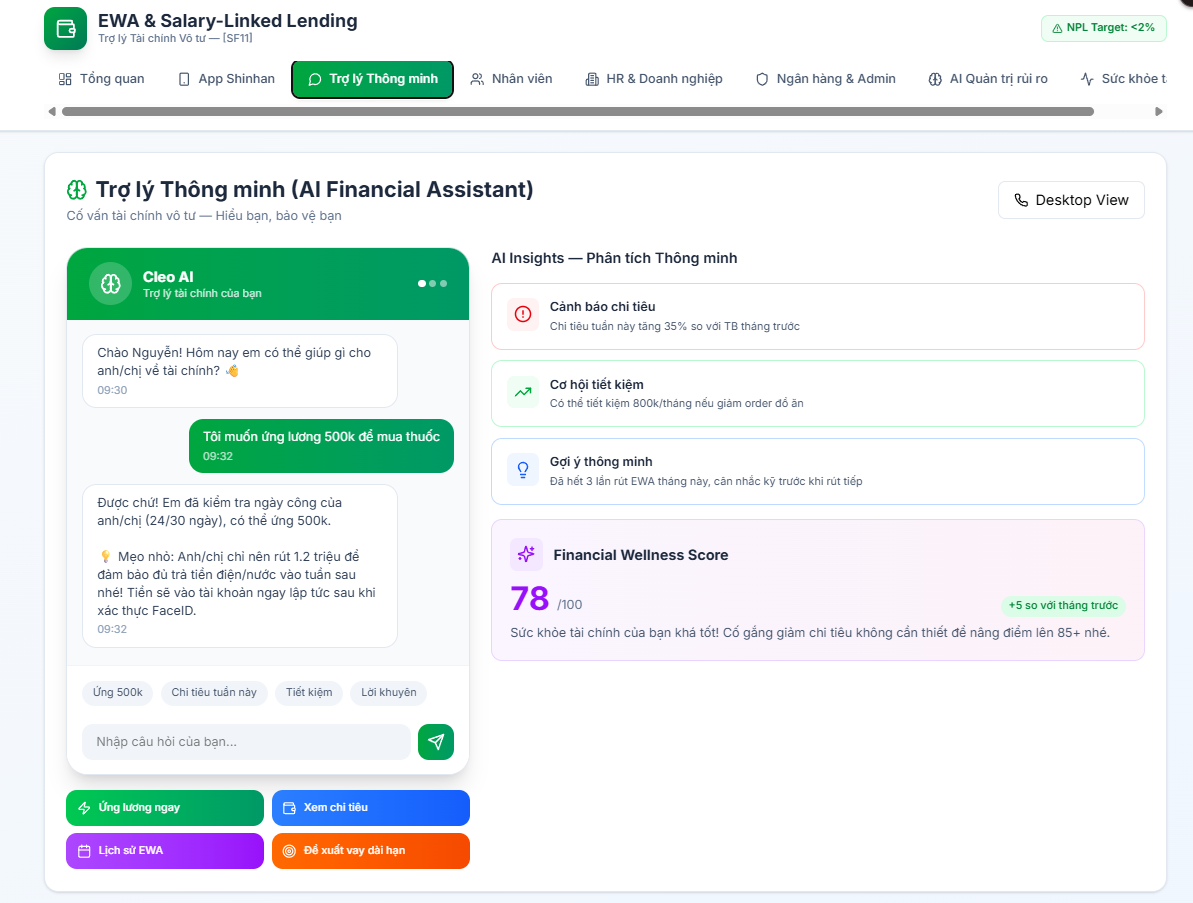

app shinhan a.i chat

-

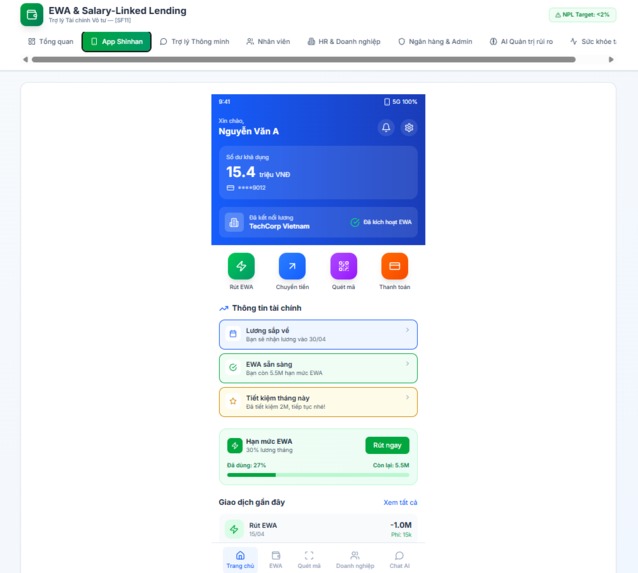

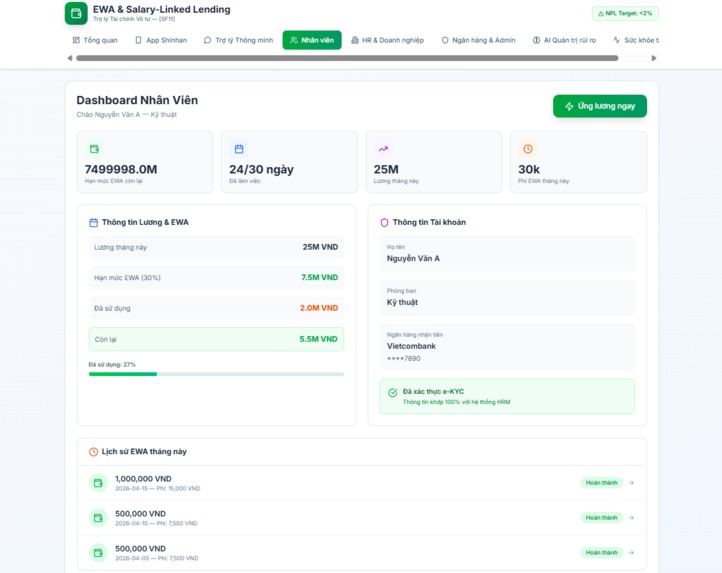

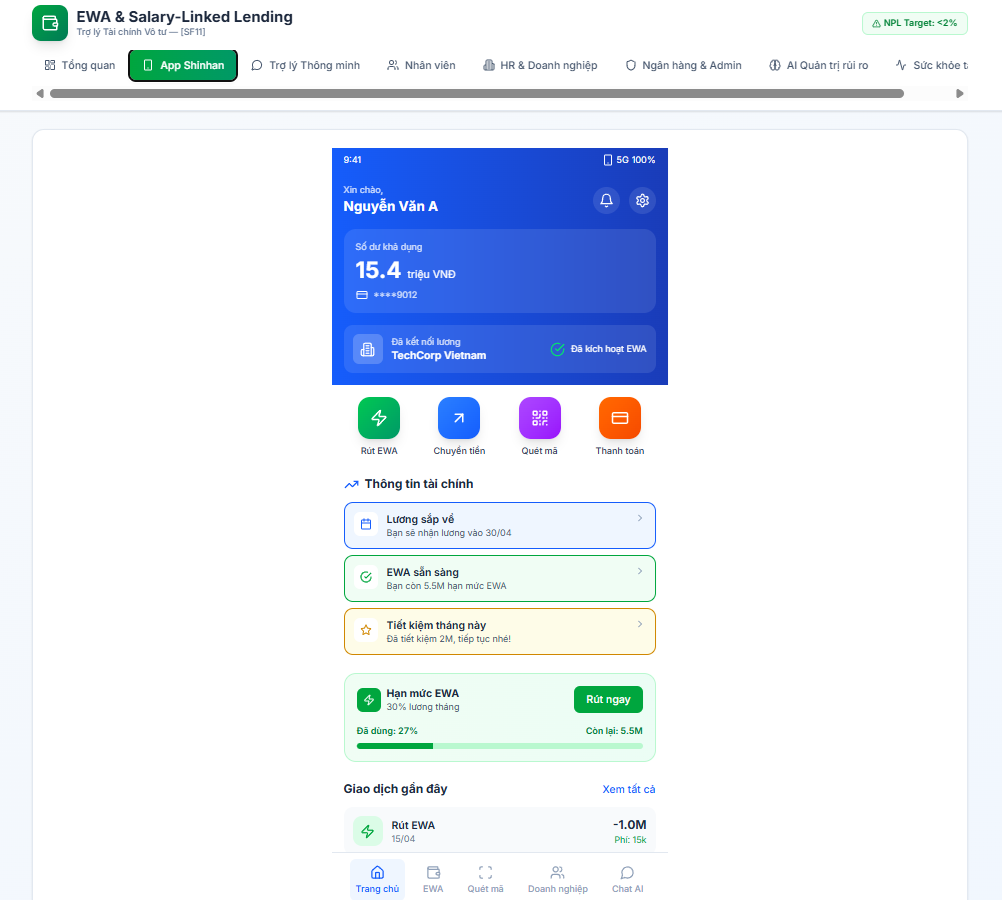

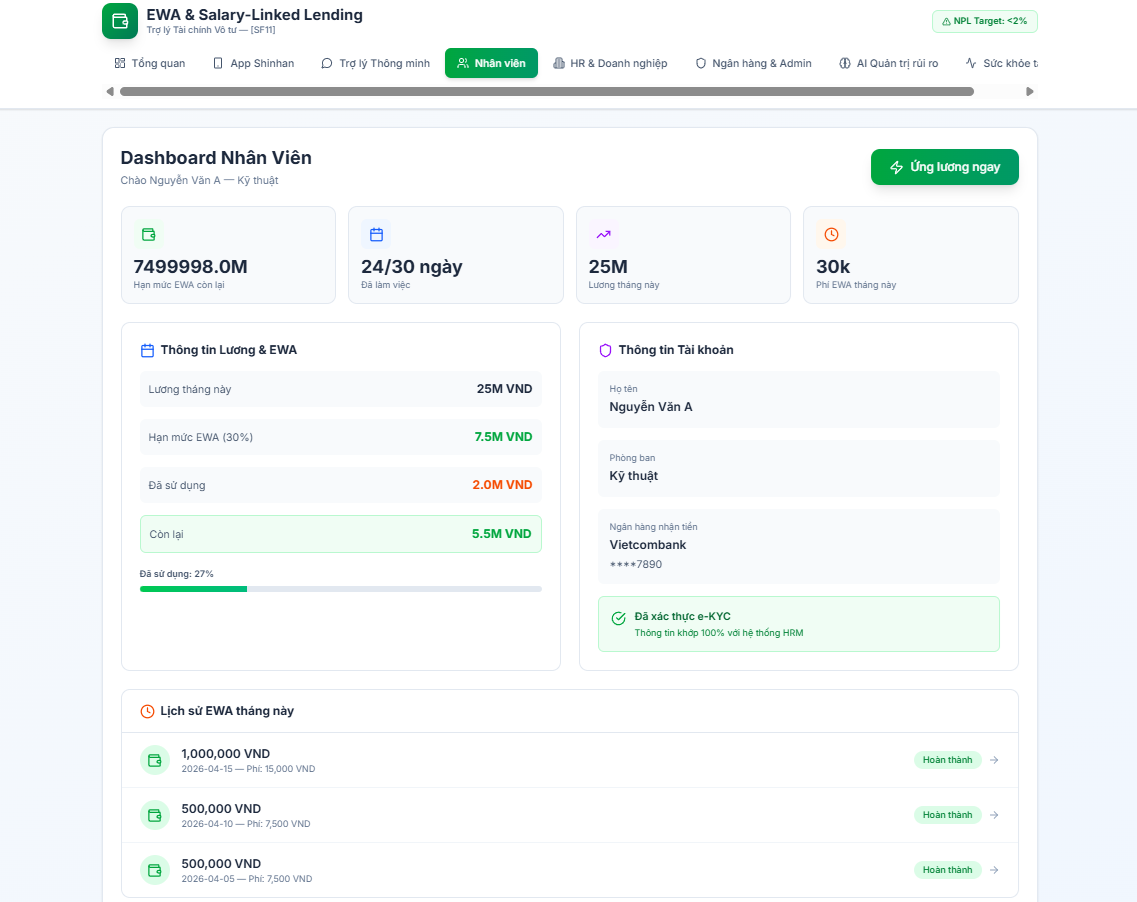

app shihan for employee

-

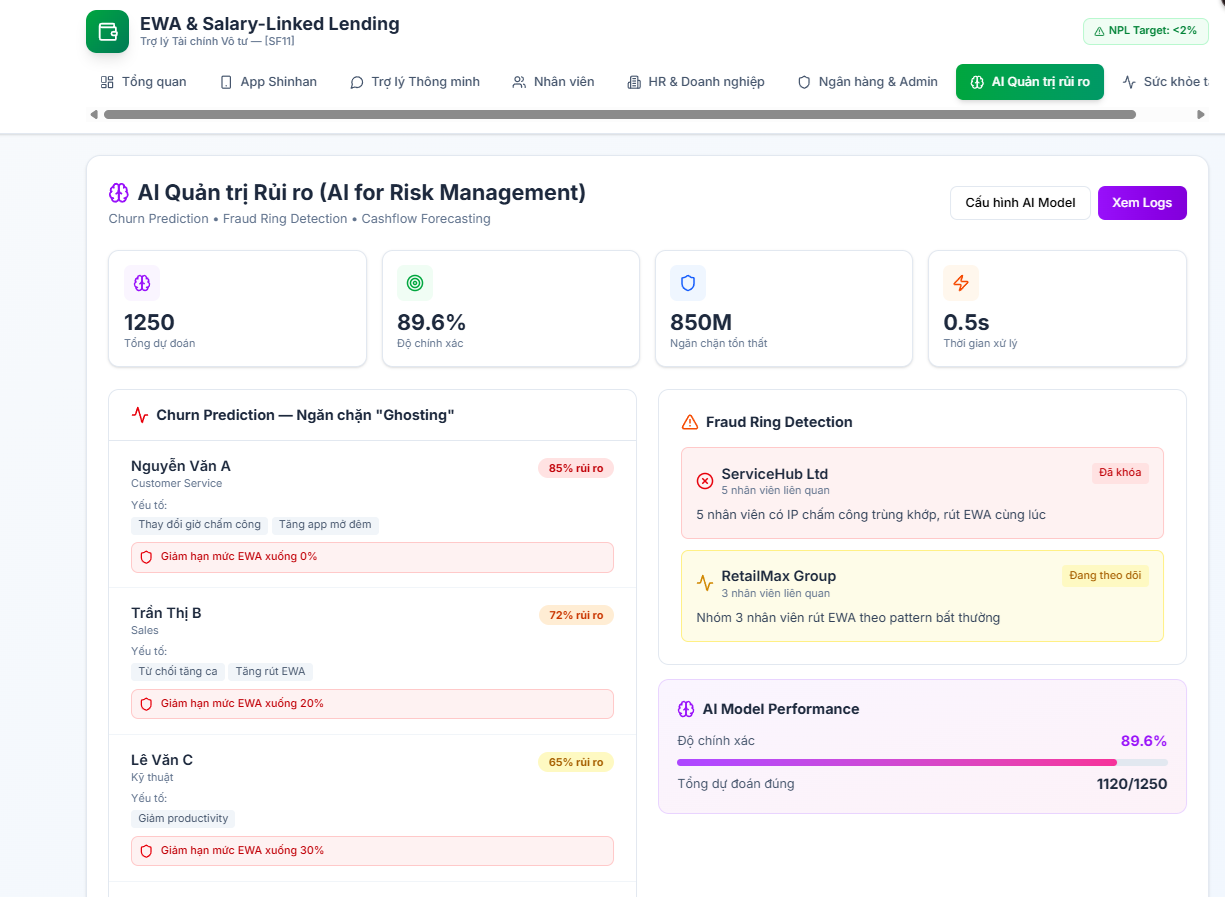

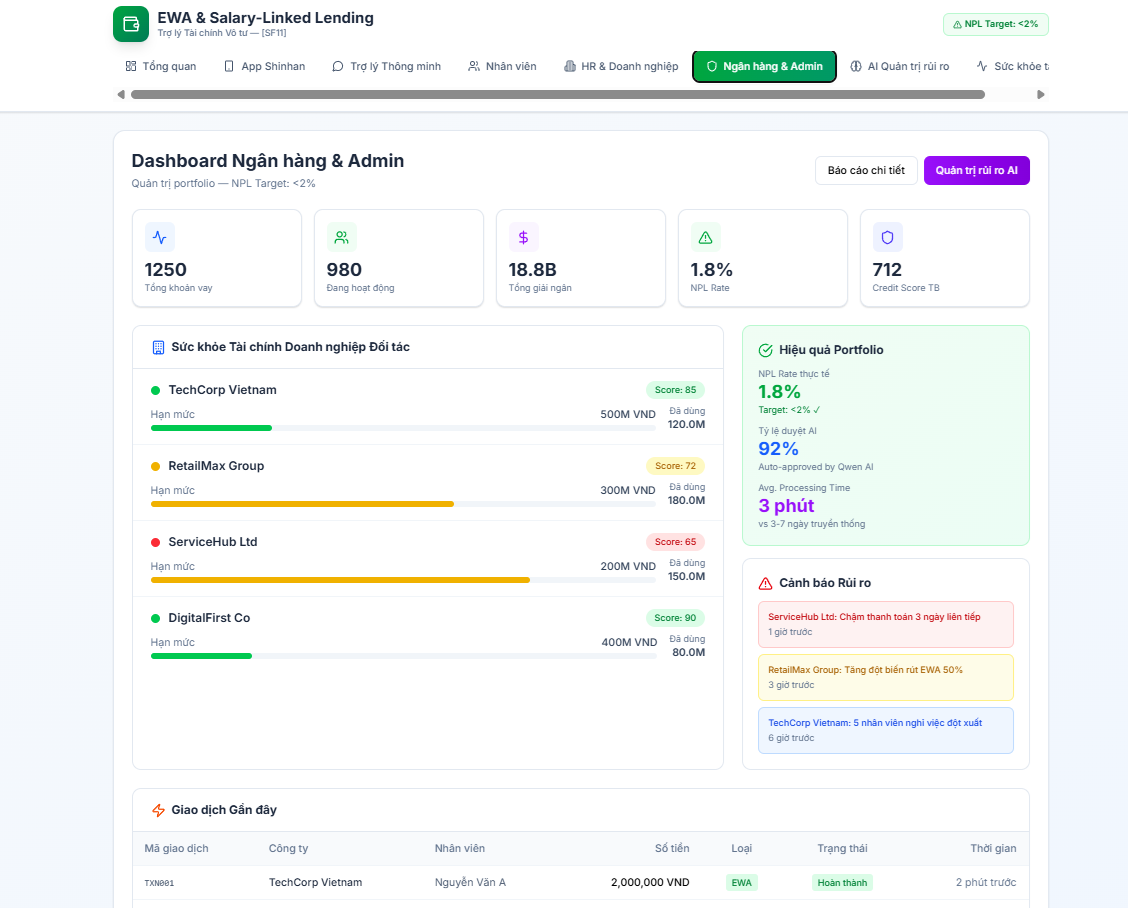

admin - risk management 1

-

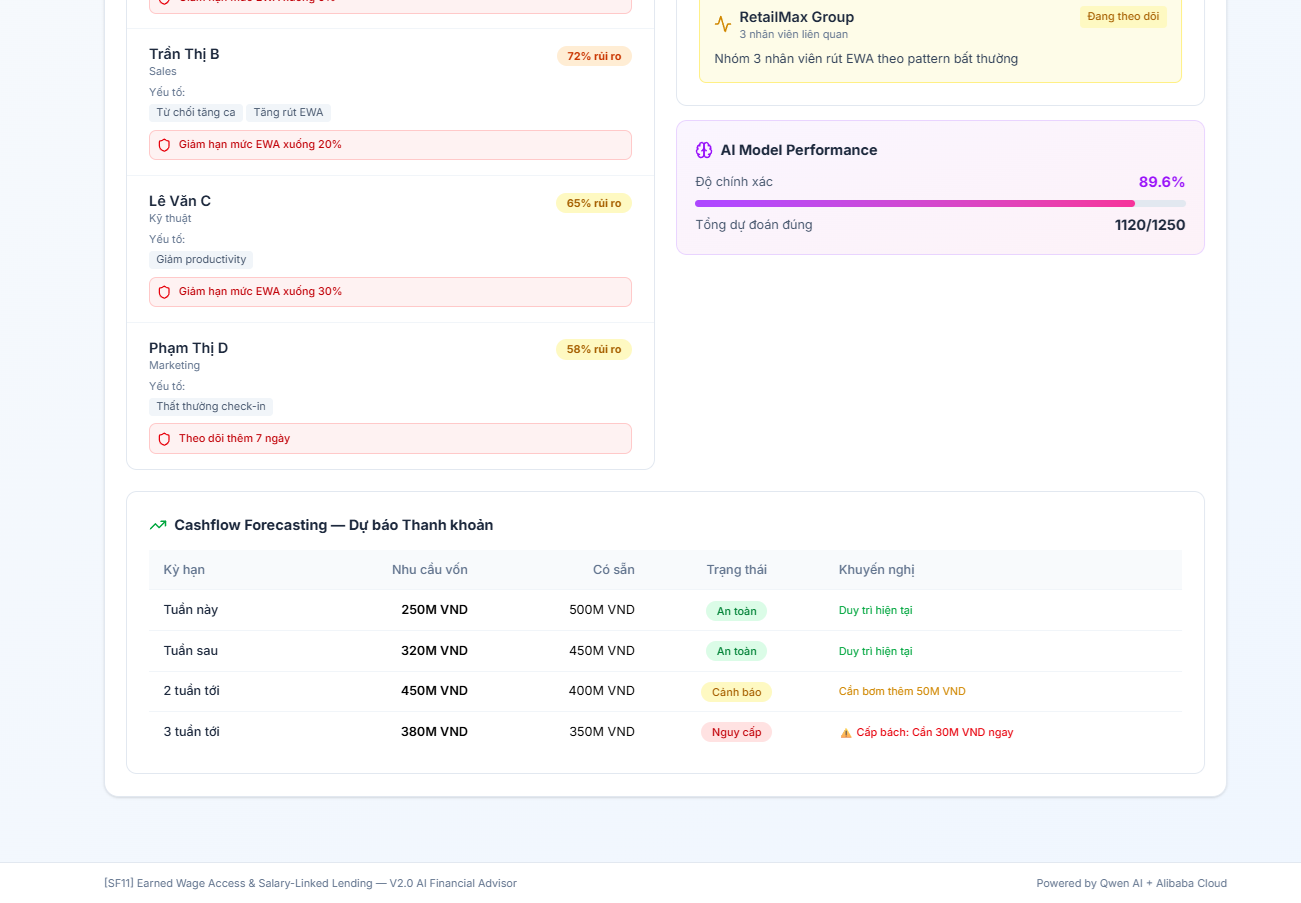

admin - risk management 2

-

admin - check business (accountant)

-

admin - index dashboard

-

admin - check customer (employee)

-

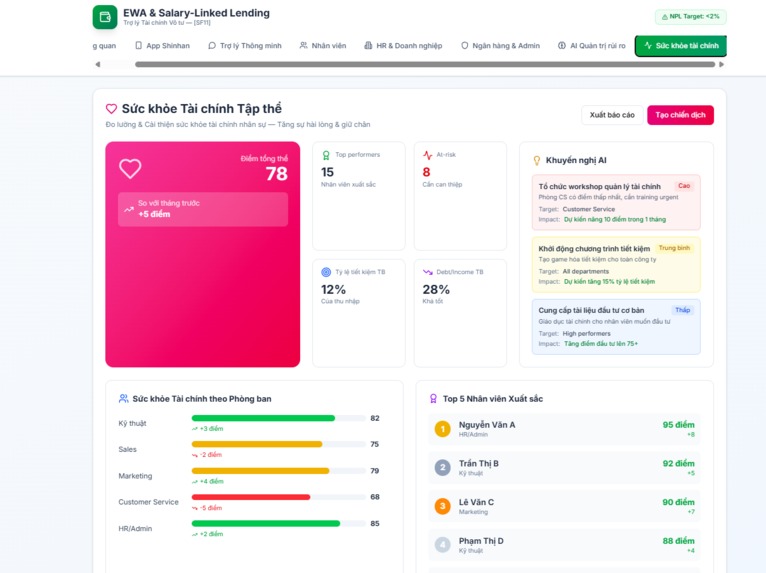

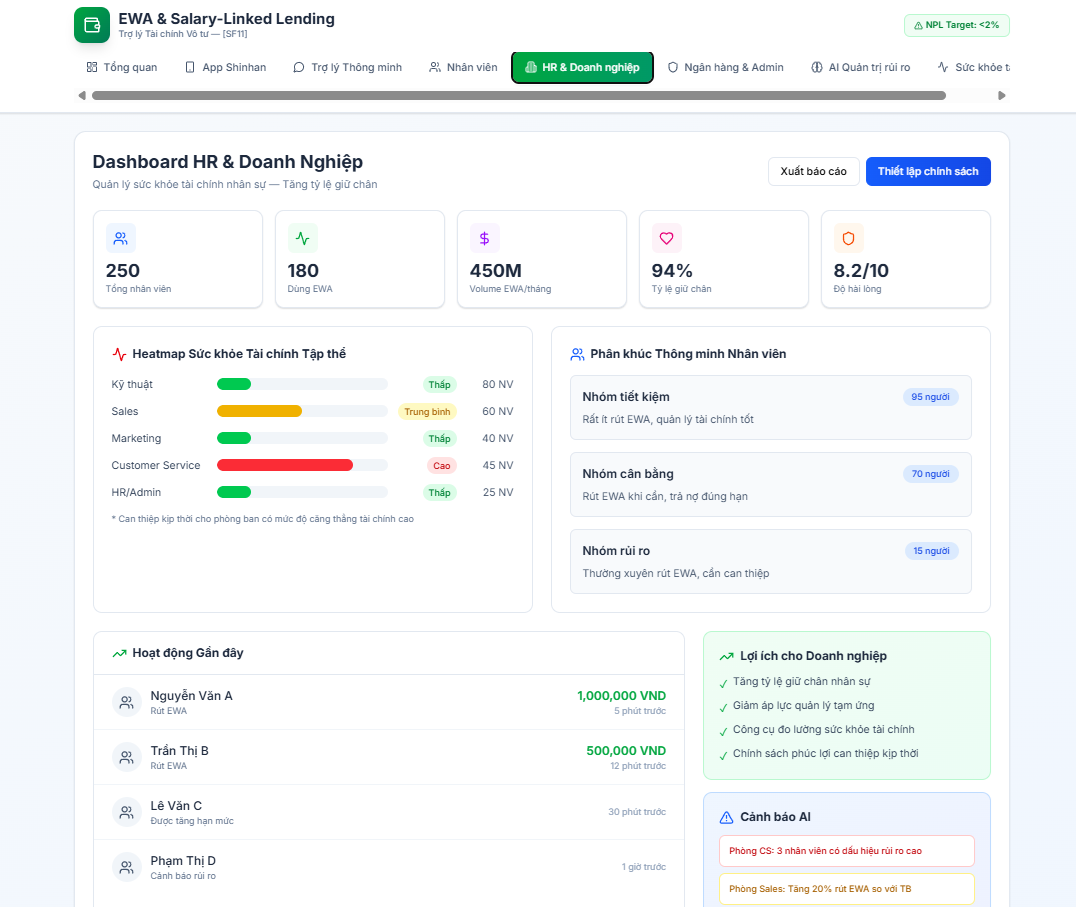

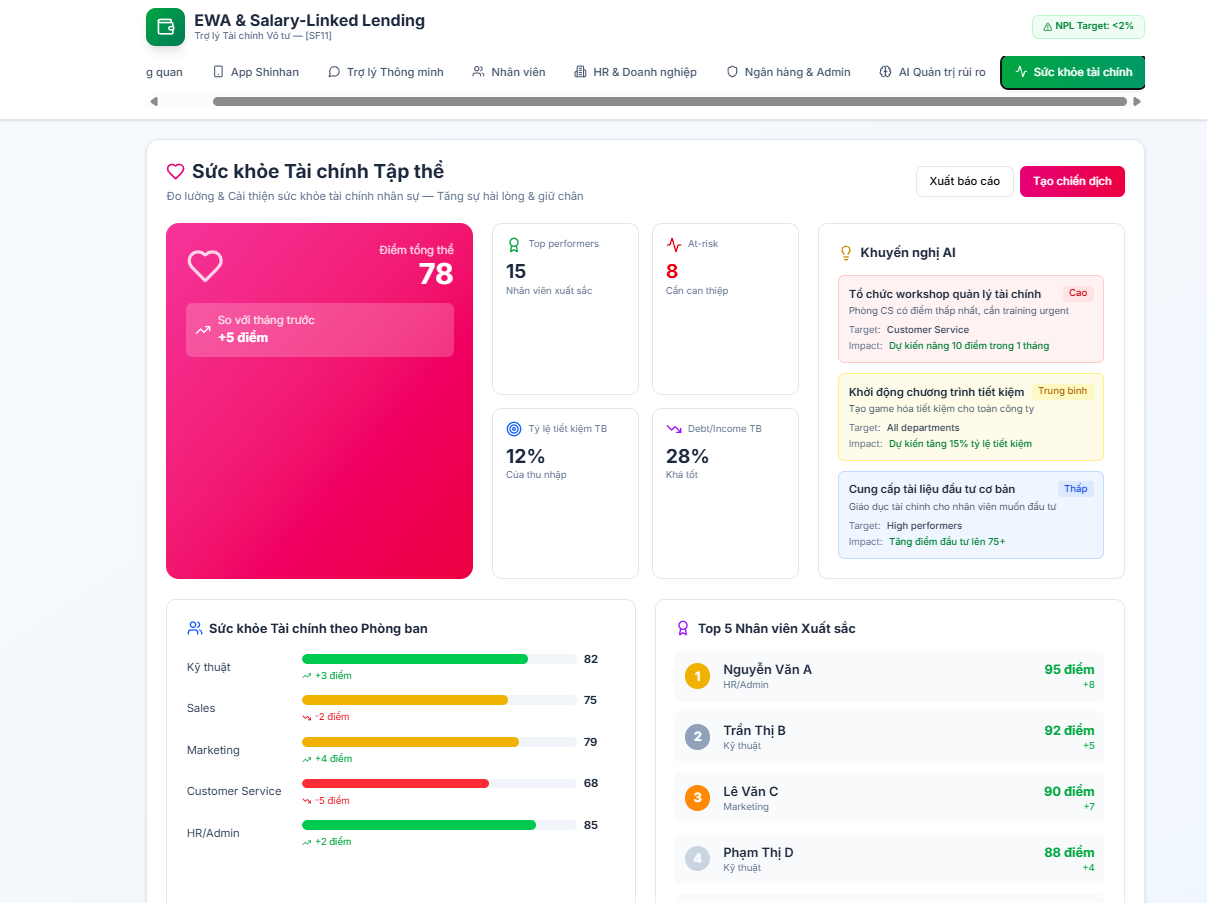

admin - business health

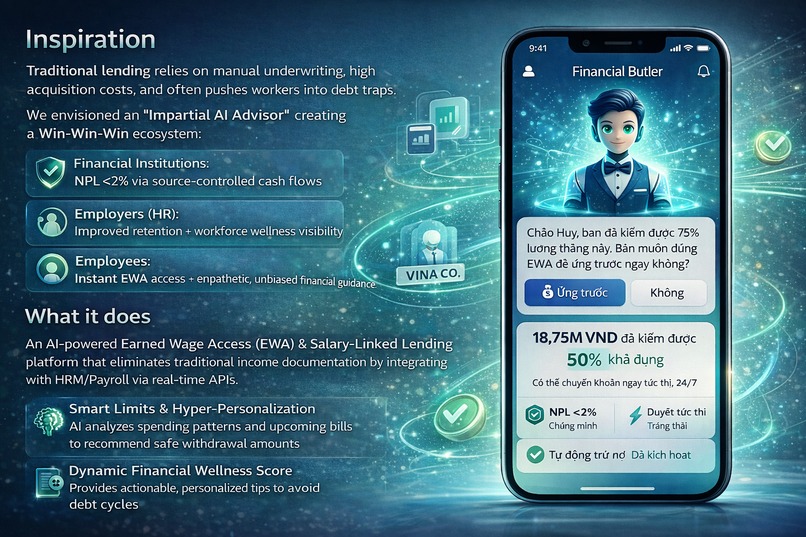

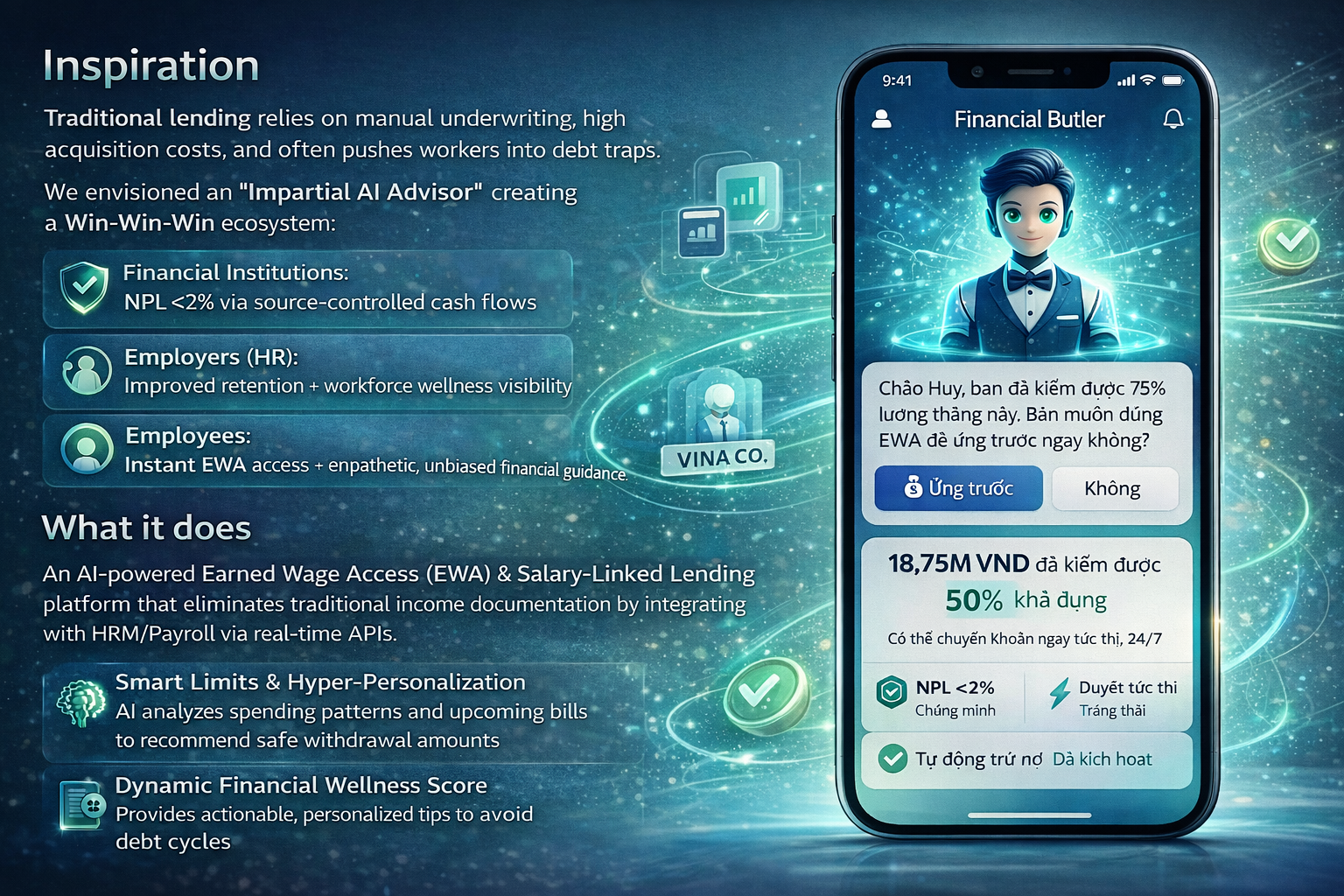

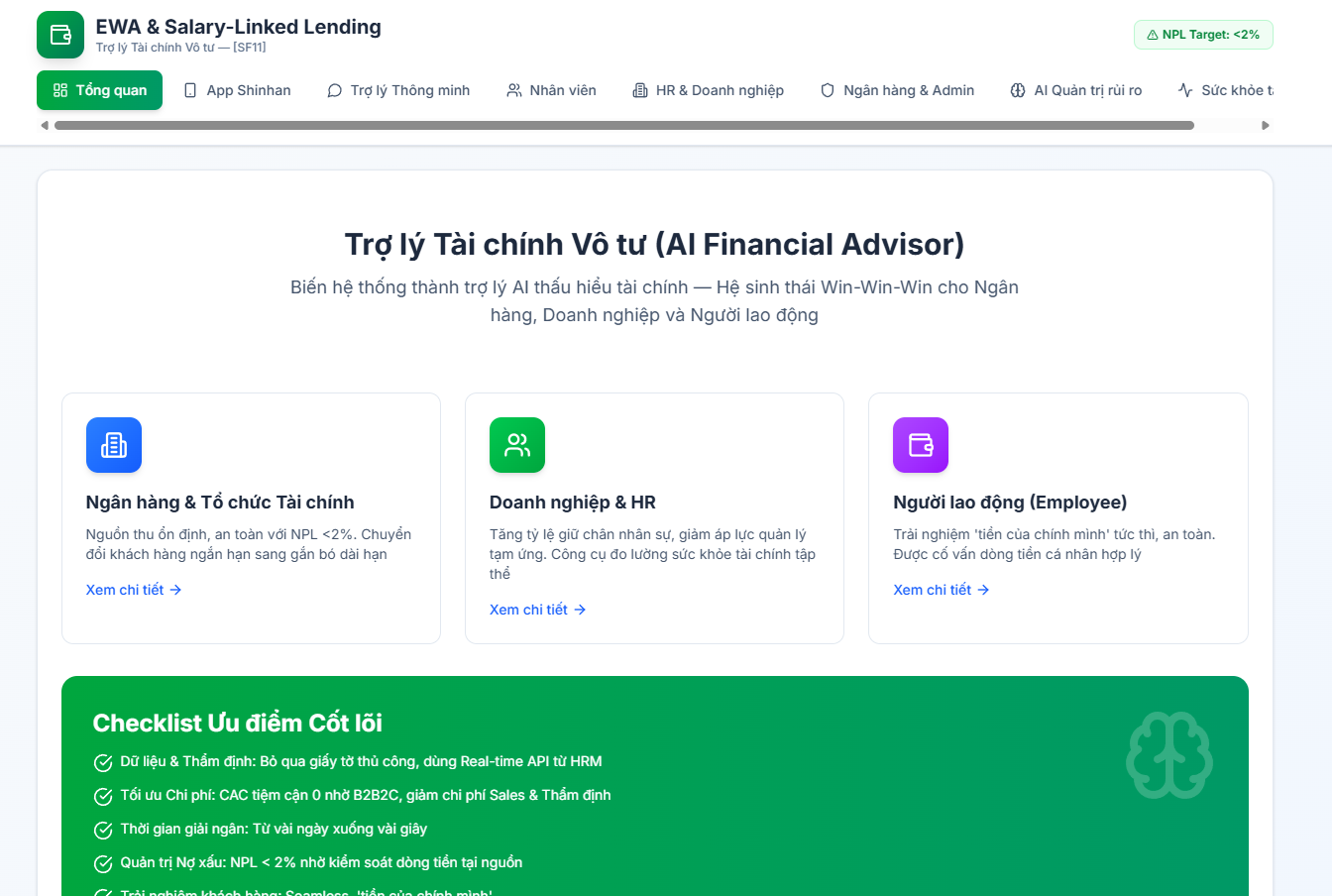

Inspiration

Traditional lending relies on manual underwriting, high acquisition costs, and often pushes workers into debt traps. We envisioned an "Impartial AI Advisor" creating a Win-Win-Win ecosystem:

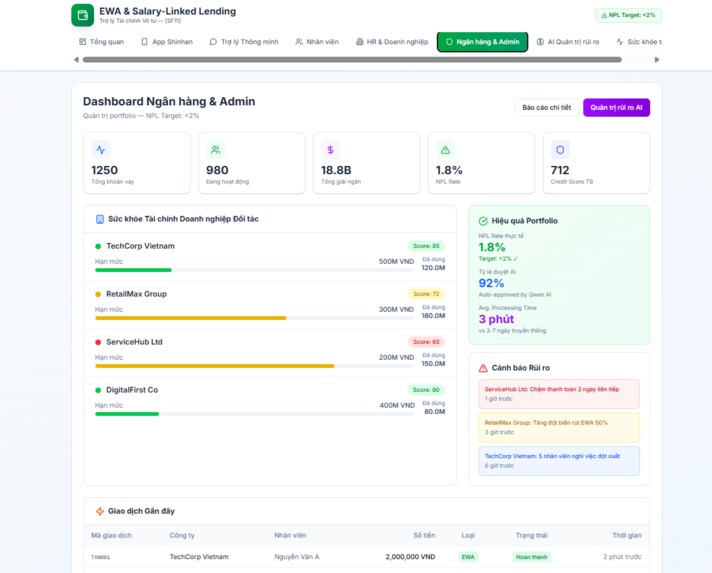

- Financial Institutions: NPL <2% via source-controlled cash flows

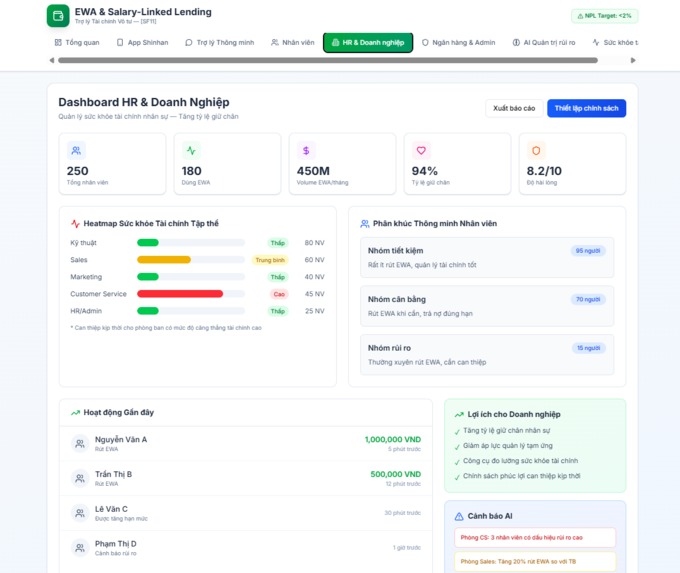

- Employers (HR): Improved retention + workforce wellness visibility

- Employees: Instant EWA access + empathetic, unbiased financial guidance

What it does

An AI-powered Earned Wage Access (EWA) & Salary-Linked Lending platform that eliminates traditional income documentation by integrating with HRM/Payroll via real-time APIs. Beyond dispensing funds, acts as a "Financial Butler":

- Smart Limits & Hyper-Personalization: AI analyzes spending patterns and upcoming bills to recommend safe withdrawal amounts

- Dynamic Financial Wellness Score: Provides actionable, personalized tips to avoid debt cycles

- Automated Cross-Selling: Proactively suggests converting EWA to lower-interest structured loans when users max out limits

How we built it

Cloud Infrastructure (Alibaba Cloud):

- API Gateway + Message Queue for async, high-volume transaction spikes (holidays, back-to-school)

- Split Payment/Escrow architecture auto-deducts fees/principles before salary reaches user account AI Brain (Qwen + ML):

- Conversational Interface: Qwen LLM powers natural language Financial Butler ("I need $20 for groceries" → checks balance, processes contextually)

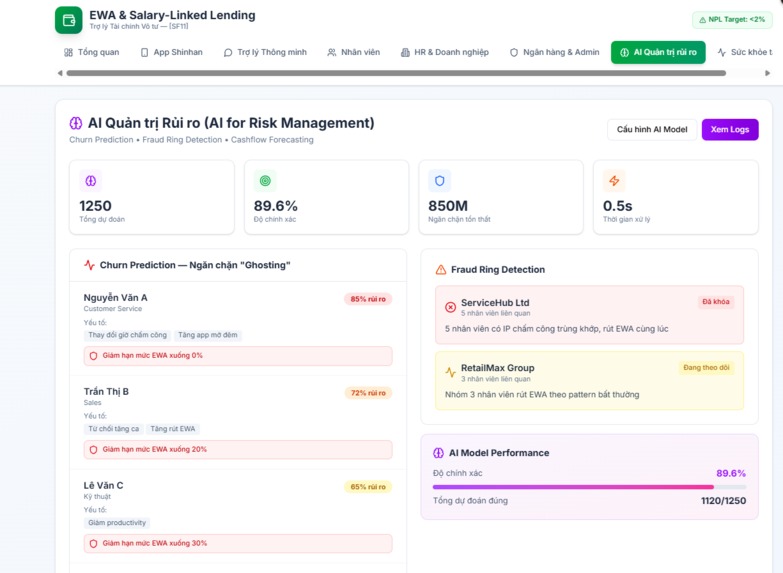

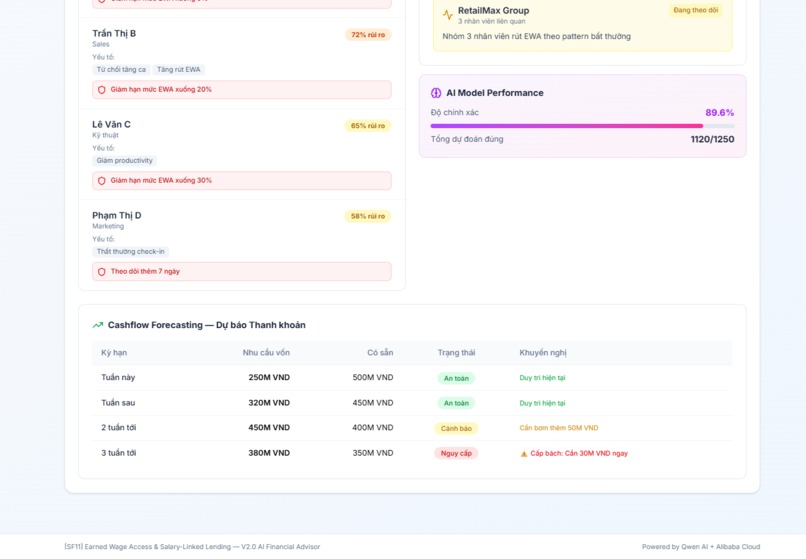

- Churn Prediction: Detects "ghosting" behavior before HR paperwork via metadata analysis

- Anomaly Detection: Spots fraud rings (ghost employees sharing clock-in timestamps/IP addresses)

Challenges we ran into

- Deterministic Limits vs. Human Unpredictability: Hard-coded rules couldn't detect sudden "ghosting" behavior → pivoted to probabilistic AI models

- Liquidity Forecasting: Built AI Cashflow Forecasting module to predict withdrawal spikes based on seasonality

- UX vs. Anti-Fraud: Implemented seamless biometric authentication tied to device binding without adding friction

Accomplishments that we're proud of

Transformed a cold, transactional lending tool into an empathetic financial companion. The Split Payment/Escrow reconciliation flow intercepts payroll before it hits the user's account, auto-settling EWA debt—practically eliminating default risk and achieving NPL <2%.

What we learned

In fintech, automation solves present problems, but AI solves future problems. Relying solely on clean data and IF/THEN rules fails when scaling. AI's true value is reading behavioral patterns and providing scalable empathy—financial guidance, not just loans.

What's next

- Corporate Dashboard: AI-generated "Financial Stress Heatmap" for HR to visualize anxiety across departments

- Multi-lingual Qwen: Support for diverse, blue-collar migrant workforces in industrial zones

- Macro-Economic Integration: Real-time global supply chain indicators to foresee sector layoffs and pre-approve relief structures

Built With

- css

- fastapi

- json

- next.js

- postcss

- python

- qwen

- tailwind

- typescript

- vercel

Log in or sign up for Devpost to join the conversation.