-

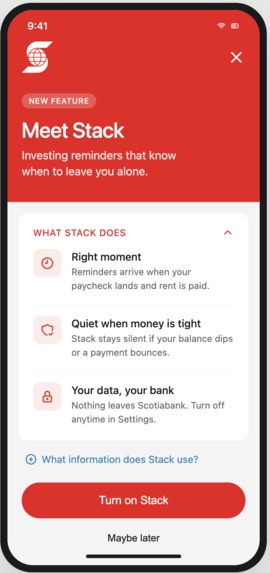

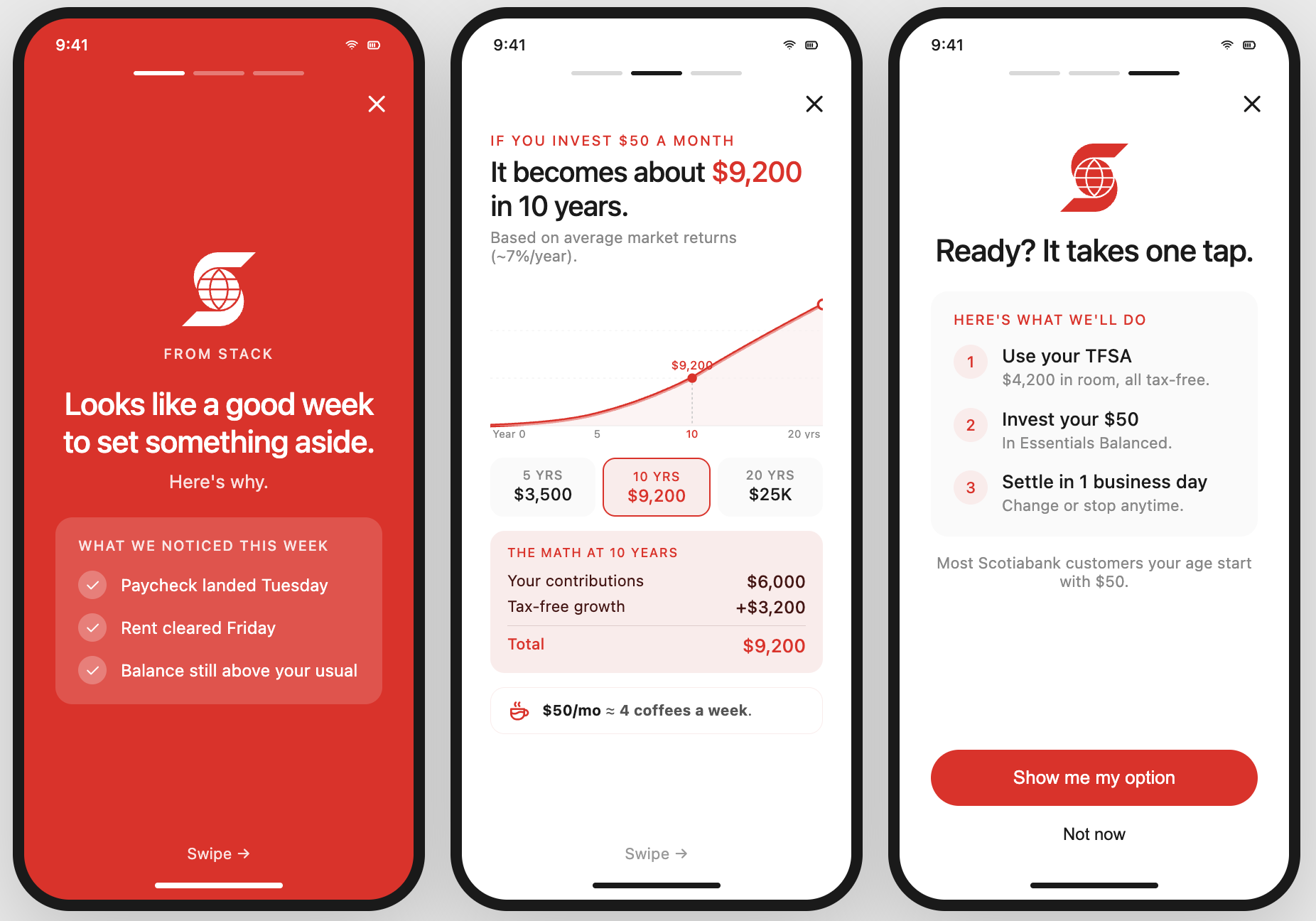

Screen 1

-

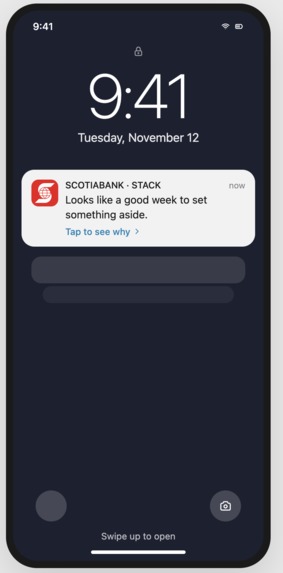

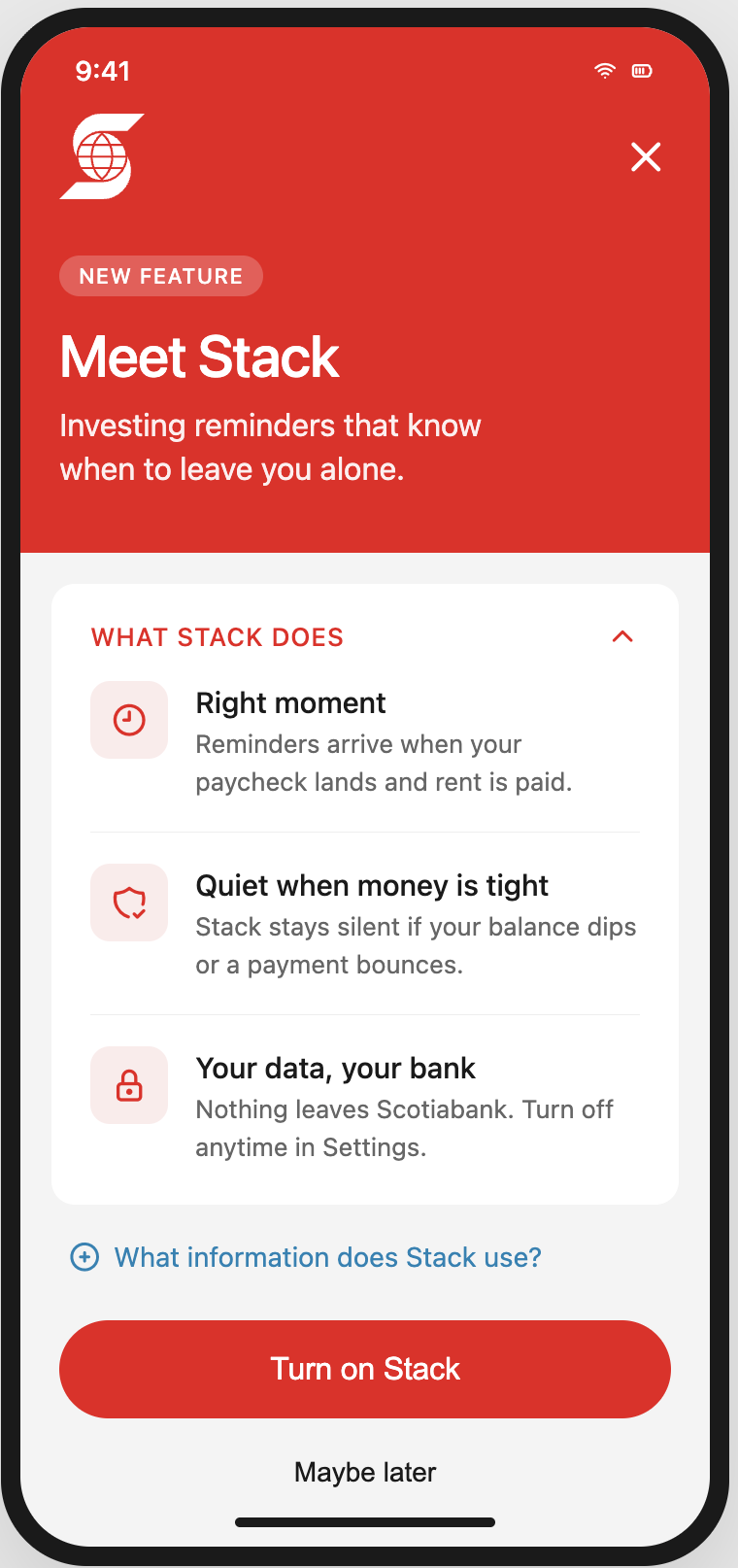

Screen 2

-

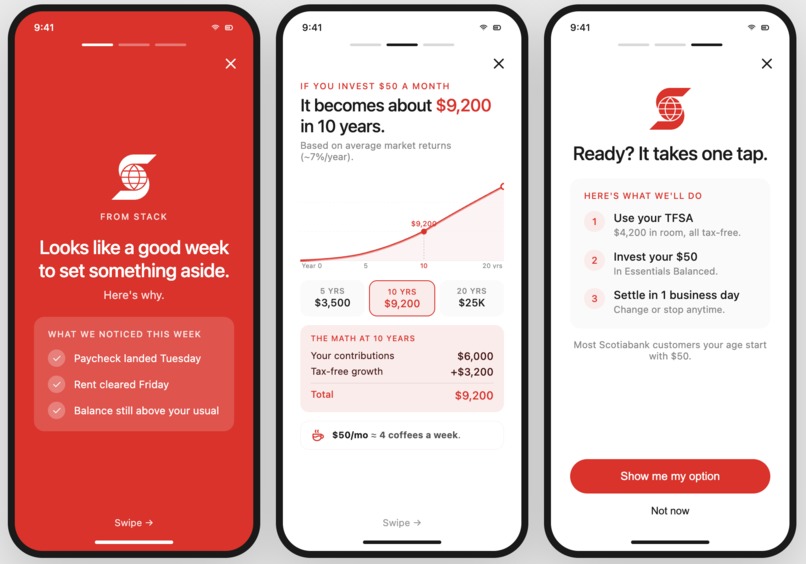

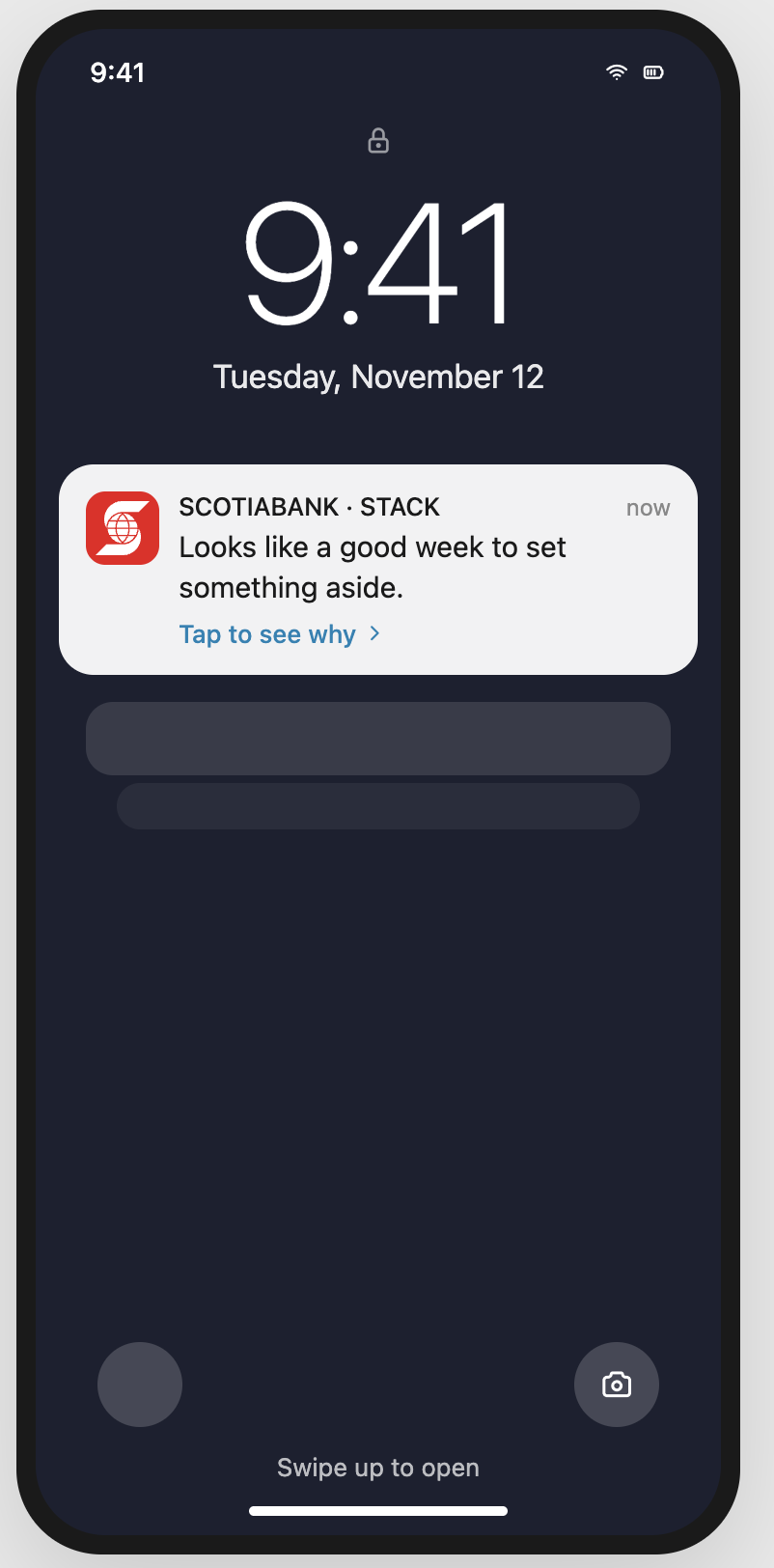

Screen 3

-

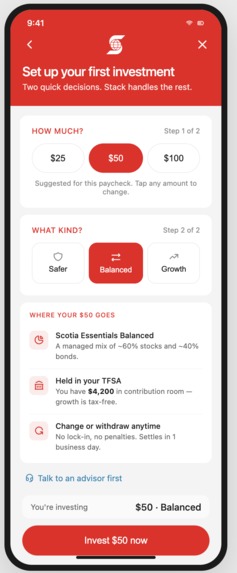

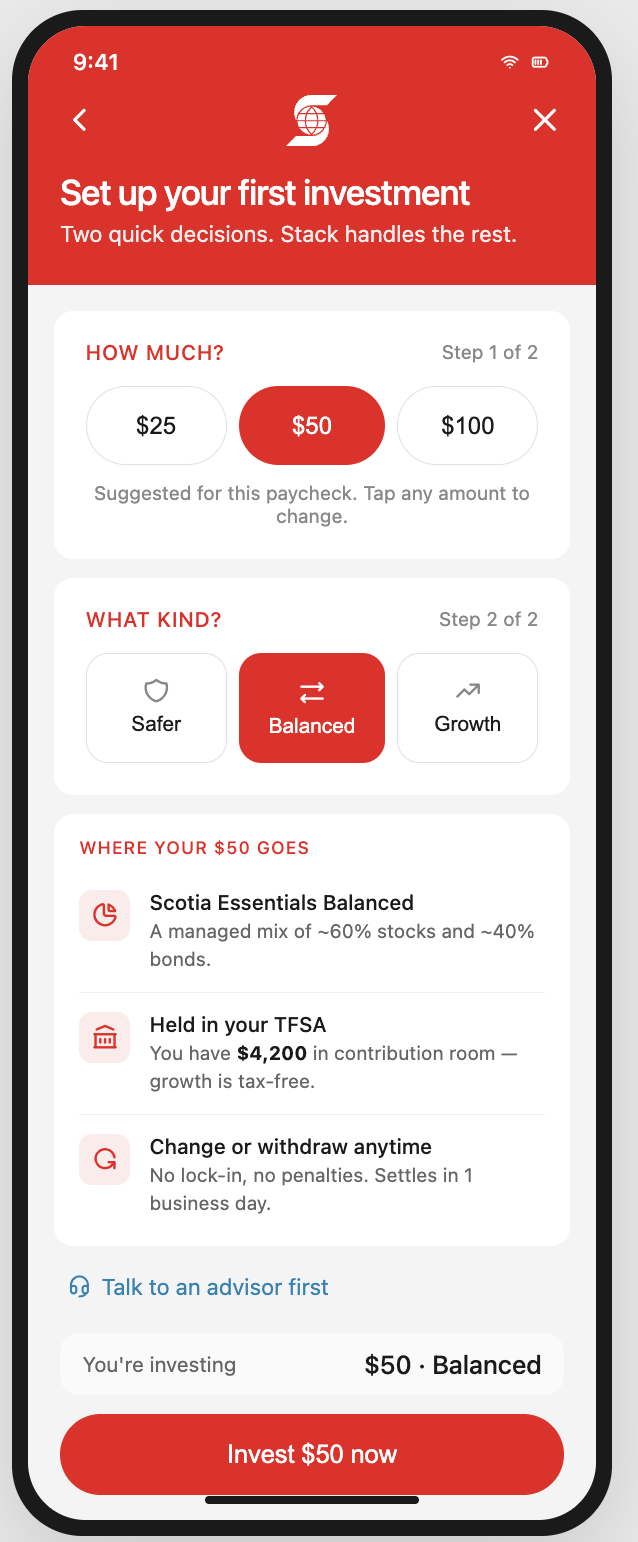

Screen 4

-

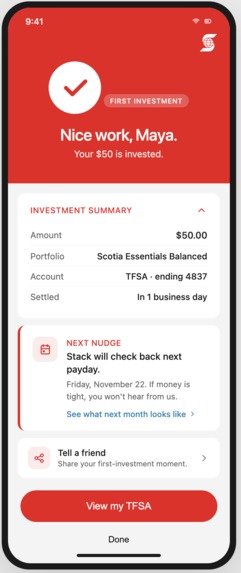

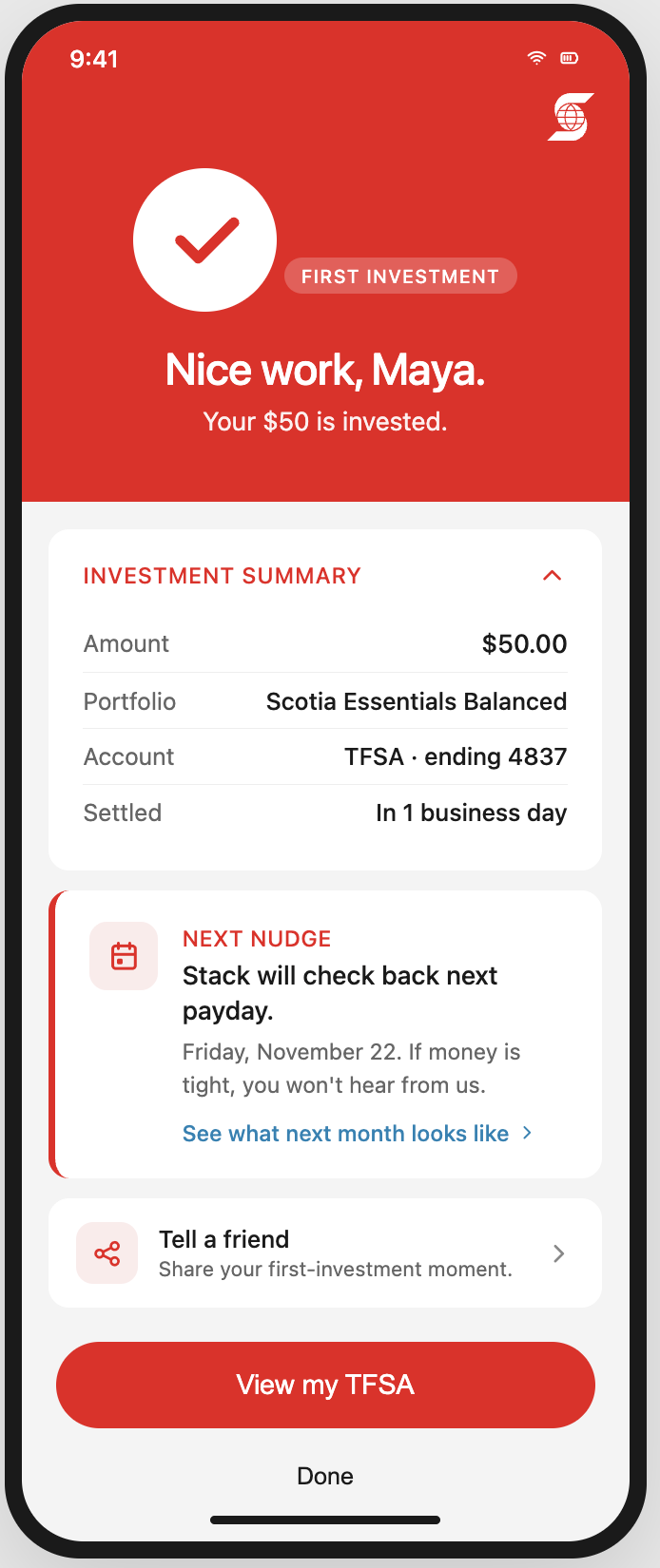

Screen 5

-

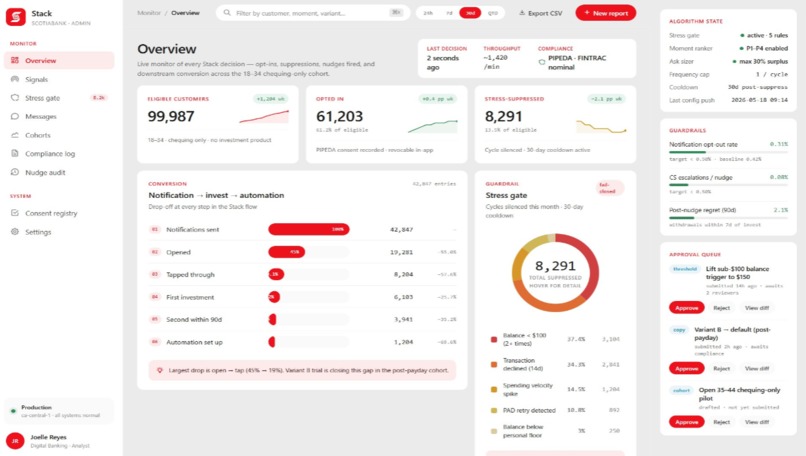

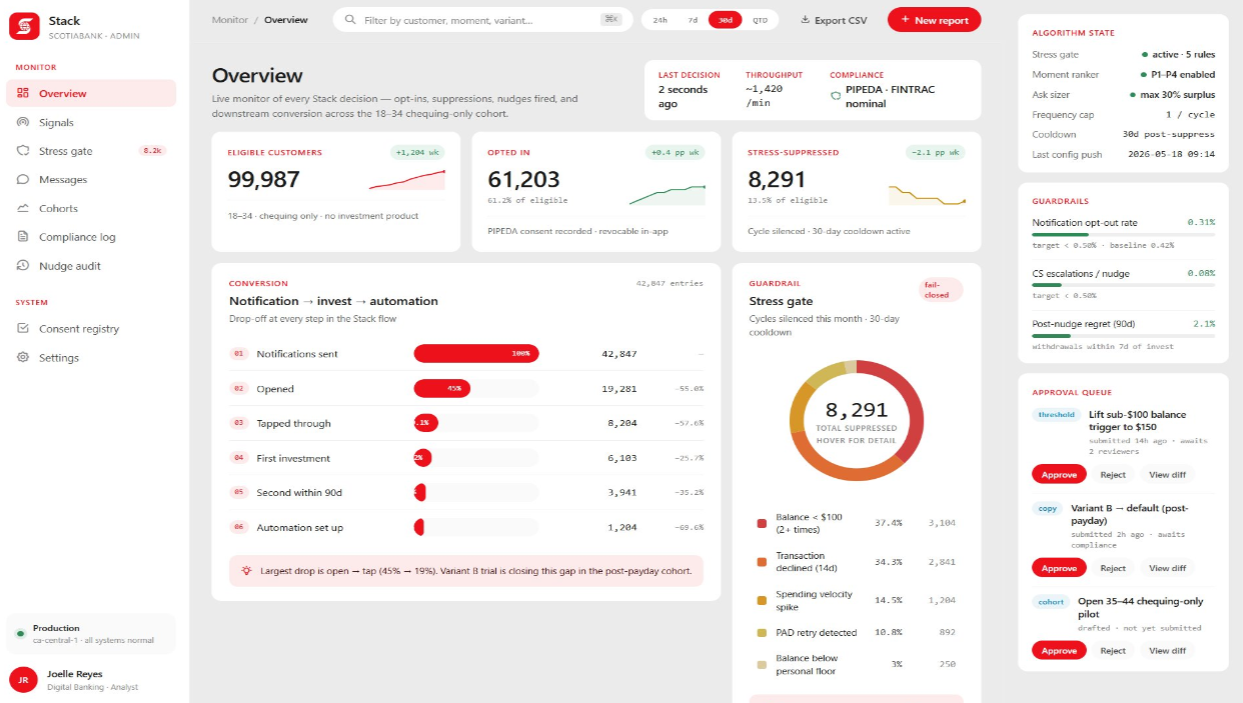

Admin Panel

What inspired us

Everyone on our team has had the same conversation. A friend asks if they should start investing. Everyone says yes. Nobody does anything about it.

We kept asking why. The case data gave us the answer. 43% of younger Canadians say they don't know where to begin. Not that they don't have money. They have the money. The problem is the moment. The confidence. The clarity.

Then we looked at what Scotiabank actually sees: every paycheck, every rent payment, every balance dip. A complete picture of a customer's financial life that no fintech can access.

The insight was simple. Scotiabank already knows when she has unspent money. It just hasn't built the system to act on it.

That became STACK.

What we learned

Narrow beats broad. Every version of this idea that tried to solve everything was weaker than the version that solved one thing: timing.

The stress gate is the product. We spent a long time designing the nudge. The part that made the whole thing trustworthy was designing the silence. Knowing when not to ask is harder than knowing when to ask. It is also what separates STACK from every competitor.

Existing infrastructure is a moat. RBC NOMI moved $3.6 billion to savings using the same behavioral mechanic we apply to investing. Scotia Savings Finder already detects payday surplus inside Advice+. STACK is the next step from infrastructure that already exists and already works.

Compliance is a feature. Framing STACK as an awareness nudge rather than an investment recommendation puts it on the fastest possible compliance path. That one distinction makes the 18 month timeline real rather than optimistic.

How we built it

We started with the case data and worked backward from the specific moment of failure: the 48 to 72 hour window after payday when surplus money sits unassigned. That window opens 26 times per year. It closes every single time without action.

The algorithm ranks four trigger moments by investment intent signal strength: tax refund window, post-payday surplus, idle money anomaly, post-rent clearance. One notification per pay cycle. Never more.

The stress gate checks five suppression signals before any cycle runs. Any one of them triggers 30 days of complete silence.

The sizing logic keeps the ask proportional to detected surplus:

$$\text{Suggested amount} = \min(0.30 \times \text{surplus}, \text{ floor-safe amount})$$

The experience opens with a 60 second lesson. Then two choices: how much times what kind. Scotia's data fills in the account type. One tap.

The prototype was built in Google AI Studio. Five screens: consent, lock screen notification, 60 second lesson, two decision screen, confirmation. The stress gate toggle was the demo moment we designed everything else around.

The admin panel shows signal performance, stress gate suppression activity, nudge audit log, A/B message framing results, and a compliance log exportable to CSV.

Challenges we faced

The "has this been done" question. RBC NOMI exists. Scotia Savings Finder exists. We spent real time figuring out whether STACK was actually new or just a description of things that already exist. The answer: the mechanic has been proven for savings. Nobody has pointed it at investment conversion inside a Canadian bank. That gap is the whole product.

The compliance framing. The first version of the pitch described STACK as making investment recommendations. It does not. It surfaces the output of Scotiabank's existing suitability engine through a better timed notification. Getting that language precise changed the compliance timeline from unknown to 18 months.

The AUM number. The $3.6B figure on the deck required being honest about assumptions. The number we can fully defend from real data is $1.1B by Year 5 on conservative inputs. $3.6B holds if you include the Tangerine secondary deployment and early wealth transfer retention. We kept both numbers in the deck and labeled the assumptions clearly.

Log in or sign up for Devpost to join the conversation.