Inspiration

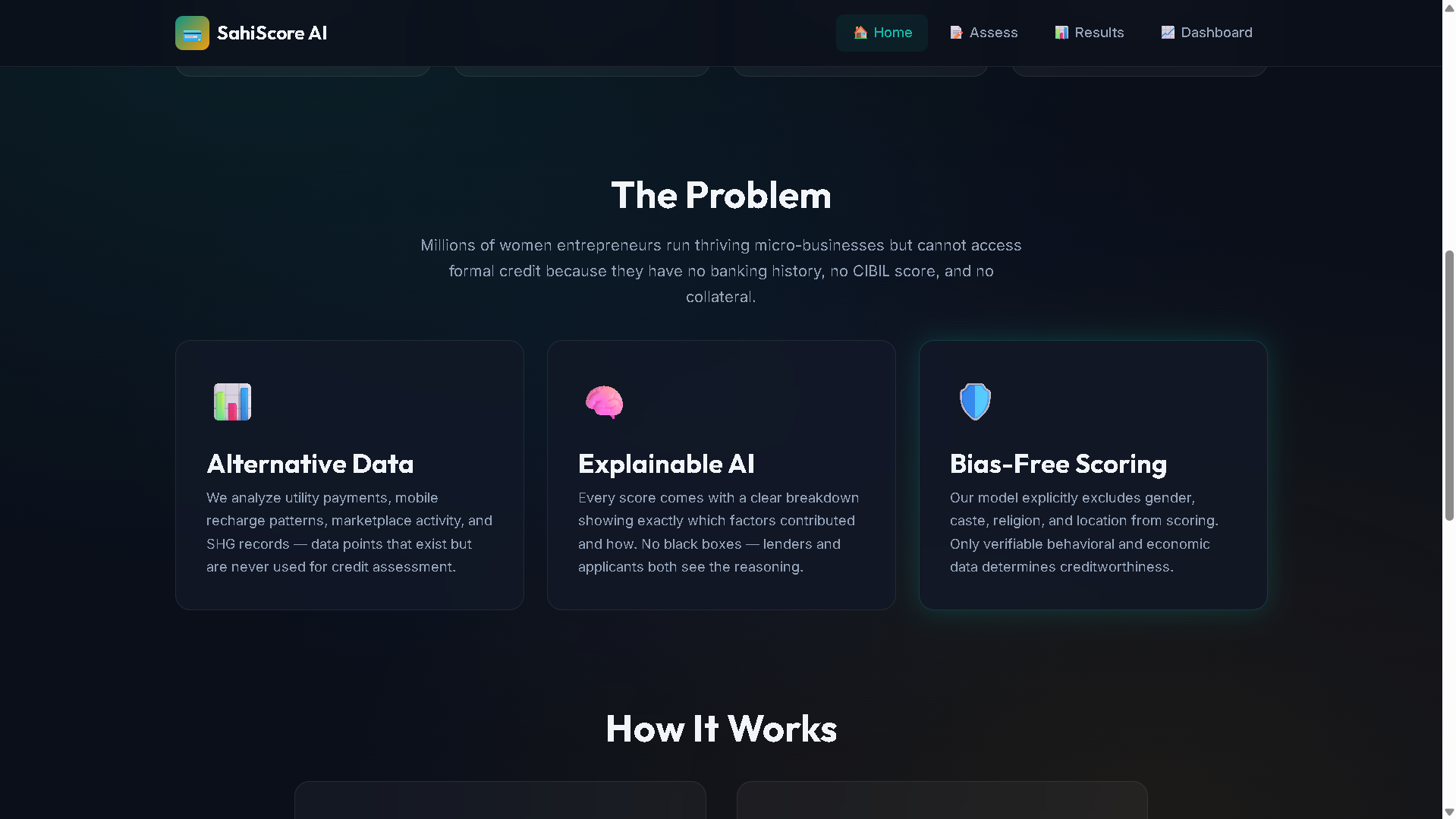

Over 350 million women in India remain unbanked — not because they lack financial discipline, but because traditional credit scoring systems like CIBIL require formal banking histories that these women simply don't have. Despite running thriving micro-businesses with a remarkable 98% repayment rate in Self-Help Groups (SHGs), they remain invisible to lenders.

We were inspired by the paradox: the most creditworthy borrowers in India are the ones who can't get a credit score.

What it does

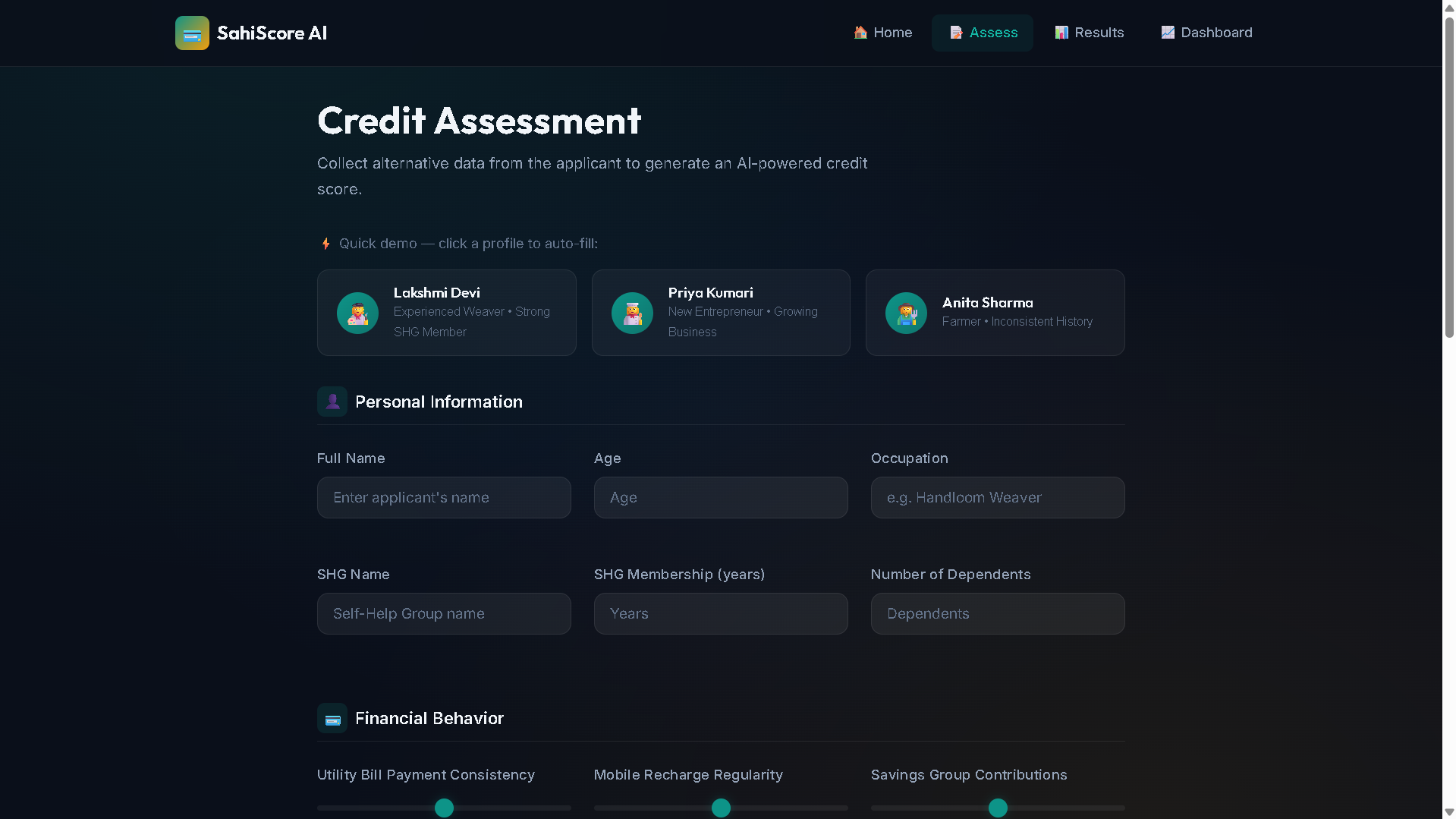

SahiScore AI is an alternative credit scoring system that generates reliable credit scores (300-900) for unbanked women entrepreneurs using non-traditional data sources:

- 💳 Financial Behavior (35%) — Utility bill payments, mobile recharge patterns, SHG savings contributions, internal loan repayment history

- 📊 Economic Activity (30%) — Years in business, monthly revenue, supply chain participation, product diversity, marketplace activity

- 🤝 Community Trust (25%) — SHG meeting attendance, peer trust scores, community references, leadership roles

- 🏠 Stability (10%) — Residential stability, SHG membership duration, family situation

The system provides:

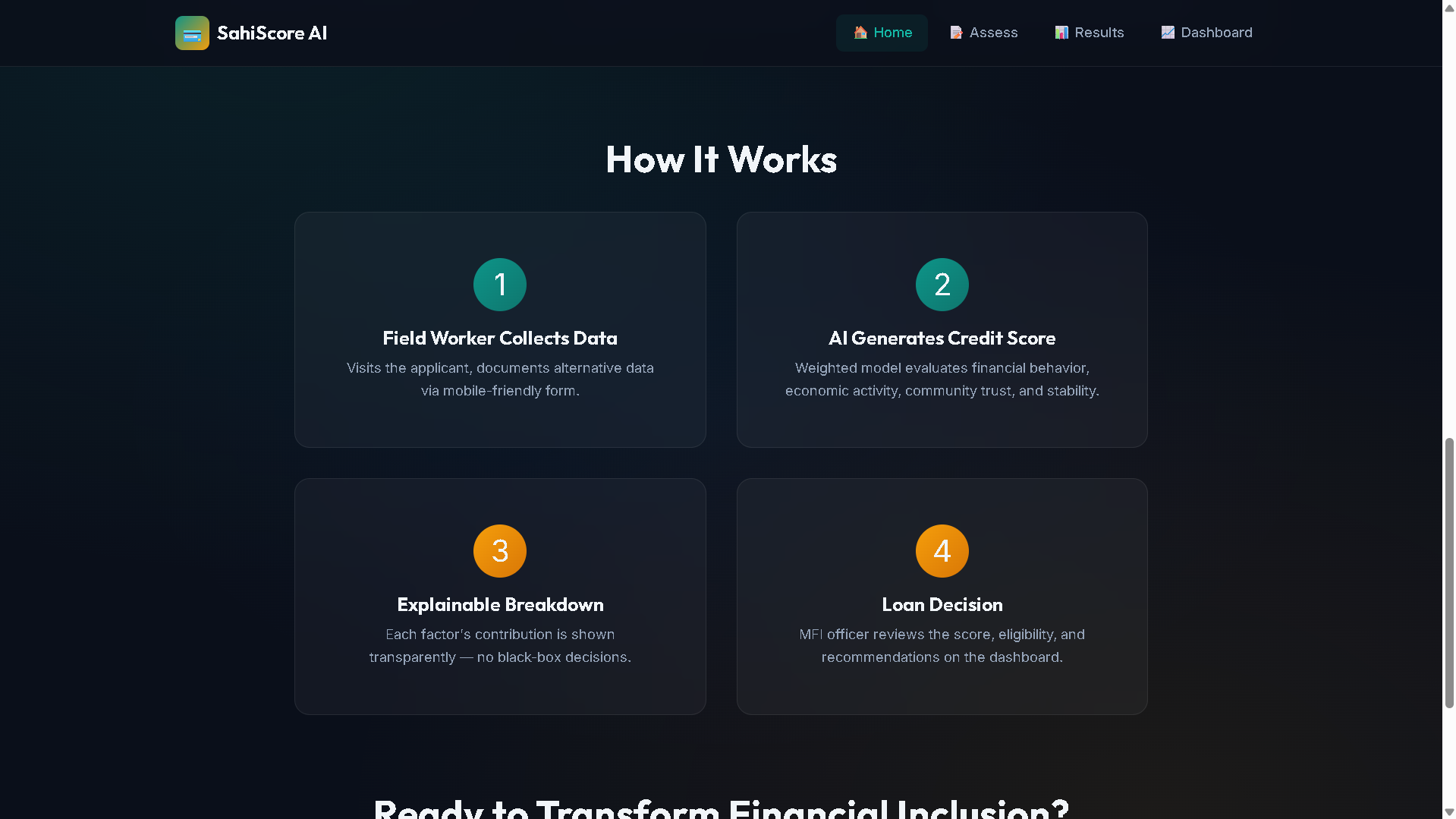

- Explainable AI — Every score comes with a SHAP-inspired factor contribution chart showing exactly why the applicant received their score

- Bias-Free Scoring — Gender, caste, religion, ethnicity, and location are explicitly excluded from all calculations

- Loan Eligibility — Automatic recommendations for loan amount, interest rate, and tenure

- MFI Dashboard — A comprehensive overview for micro-finance officers to manage all assessments

How we built it

- Frontend: Vite + vanilla JavaScript with a custom CSS design system featuring dark theme, glassmorphism, and micro-animations

- Scoring Engine: A weighted multi-factor model inspired by real ML credit scoring approaches, with explainability output modeled after SHAP (SHapley Additive exPlanations)

- Visualizations: Chart.js for interactive factor contribution charts, score distribution histograms, and risk breakdown doughnuts

- Demo System: 3 pre-built personas representing real-world archetypes (experienced weaver, new entrepreneur, seasonal farmer) for instant walkthroughs

Challenges we ran into

- Designing a scoring model that is both realistic and demonstrably fair — we had to carefully choose which alternative data points to include while ensuring none could serve as proxies for protected characteristics

- Balancing explainability with simplicity — the SHAP-style factor chart needed to be understandable by field workers with limited technical background

- Creating a mobile-friendly interface that works in low-connectivity rural environments while still looking premium

Accomplishments that we're proud of

- Built a fully functional prototype with 4 complete pages and a working scoring engine

- The system assessed 9 demo applicants, with 8 qualifying for micro-loans — unlocking an estimated ₹4.65 lakh in potential credit

- Every single score is 100% explainable — no black-box decisions

- Zero bias by design — the model explicitly excludes all protected characteristics

What we learned

- Alternative data is surprisingly predictive: SHG attendance and peer trust scores correlate strongly with repayment behavior

- Explainability isn't just an ethical requirement — it's a trust-building tool that makes both lenders and borrowers more confident

- Financial inclusion technology needs to be designed for the field, not for the boardroom

What's next for SahiScore AI

- Partner with actual SHG federations for real-world pilot testing

- Integrate with Aadhaar-based e-KYC for identity verification

- Add offline-first PWA capabilities for areas with limited connectivity

- Train a proper ML model on anonymized SHG repayment data

- Build a regional language interface (Hindi, Tamil, Bengali) for direct applicant interaction

Built With

- chart-js

- css

- html

- javascript

- machine-learning

- vite

Log in or sign up for Devpost to join the conversation.