-

-

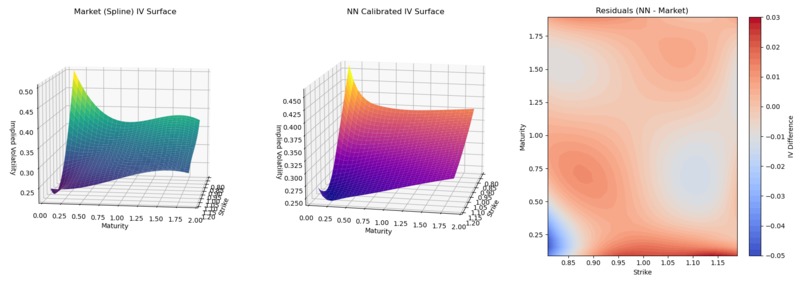

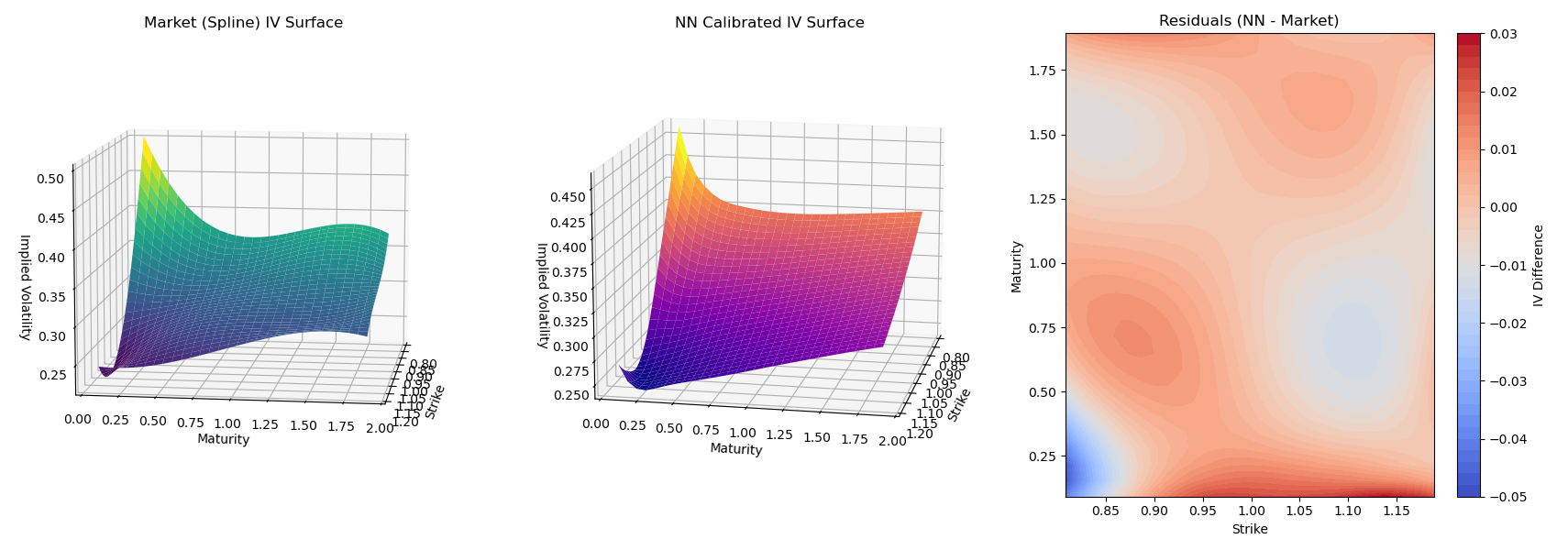

MSFT option IV surface vs Neural Network Rough Bergomi IV surface + Residuals

-

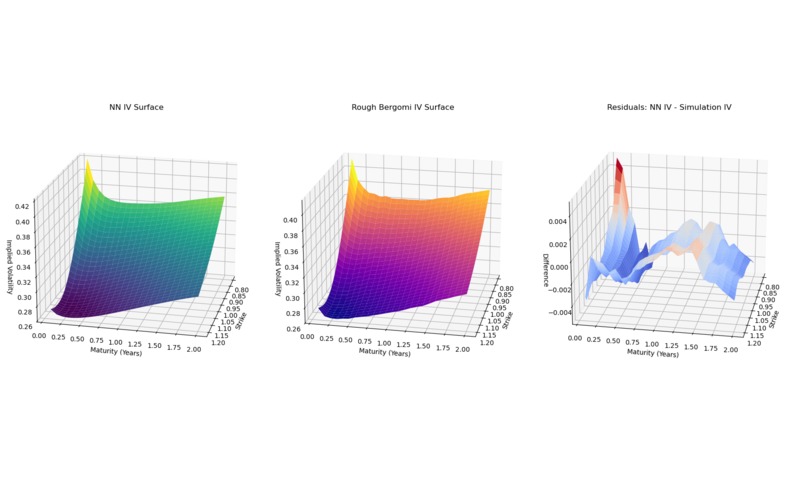

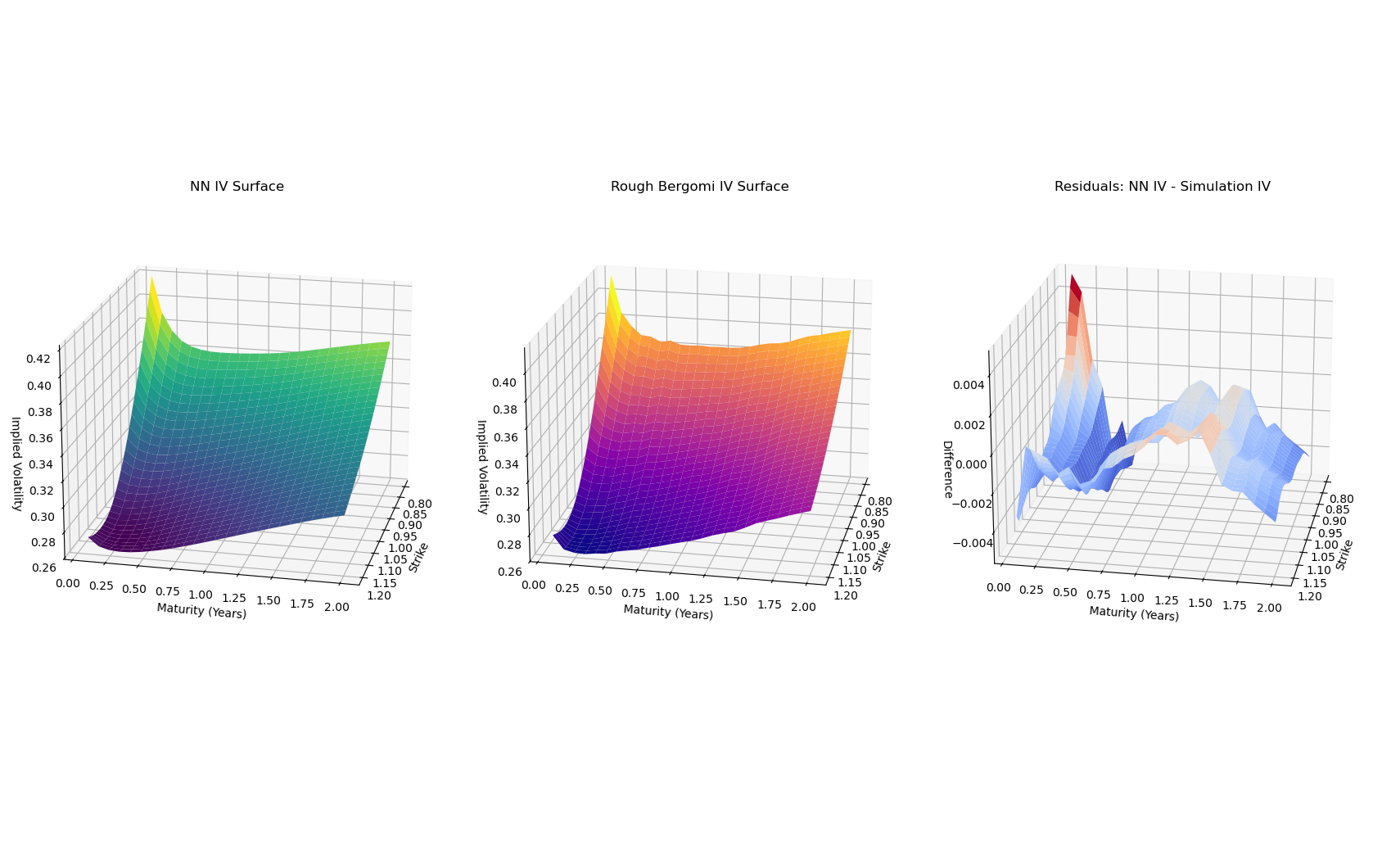

Neural Network IV surface vs Numerical Rough Bergomi IV Surface

Inspiration

Utilize a highly accurate model to price options and simulate market dynamics.

What it does

Rough Bergomi Parameter Computation

How we built it

- Pull and clean MSFT option data

- Implement a numerical approximation to the rough Bergomi model

- Generate 750000 points of synthetic data using this numerical approximation

- Train a neural network on the synthetic data to approximate the solution to the rough Bergomi model (for speed)

- Calibrate this trained neural network to obtain the 6 parameters of the rough Bergomi model.

Challenges we ran into

Optimising Time and space for the data generation

Accomplishments that we're proud of

Our model showed about 99% accuracy to real world MSFT data, nearly perfectly fitting an IV surface

What we learned

- Fractional Brownian Motion

- Rough Stochastic Volatility.

What's next for Rough Bergomi Stochastic Volatility Calibration

More accurate numerical approximation (time constraints)

Log in or sign up for Devpost to join the conversation.