-

-

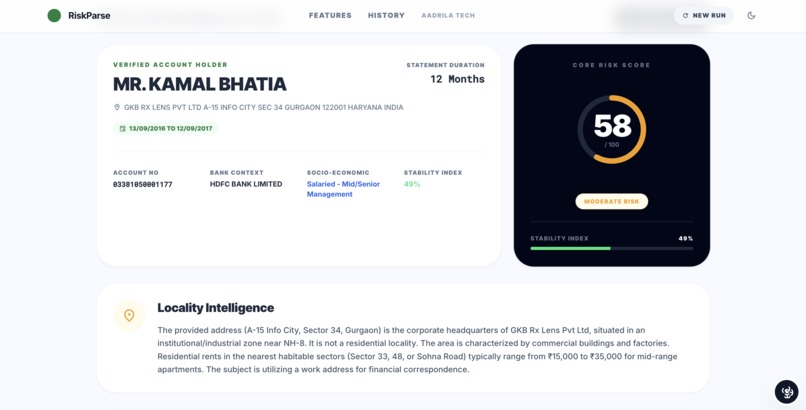

First section of the report.

-

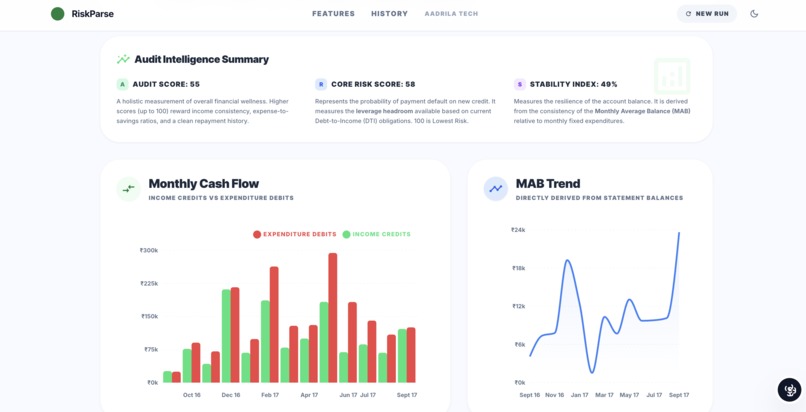

Second Section of the report.

-

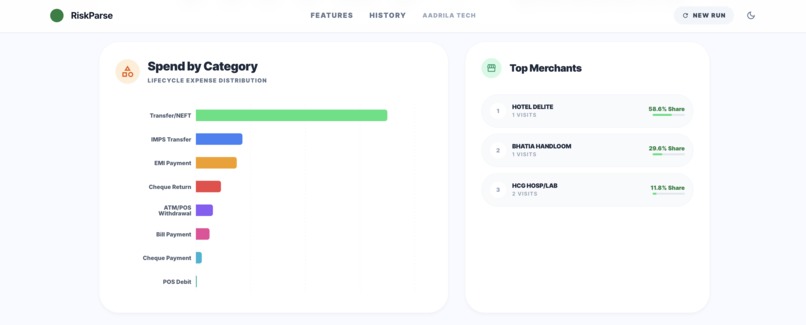

Third Section of the report.

-

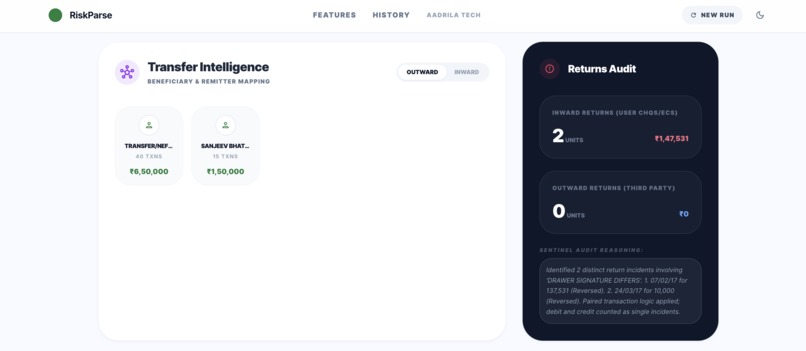

Fourth Section of the report.

-

Fifth Section of the report.

-

Sixth Section of the report.

Inspiration

RiskParse was inspired by a recurring gap we observed in lending and insurance workflows: bank statements contain some of the richest and most honest financial signals, yet they are still reviewed manually or used in a very limited way.

Credit decisions often rely heavily on bureau scores or static documents, which fail to capture real cash-flow behavior, especially for thin-file customers, self-employed individuals, and first-time borrowers. At the same time, underwriters spend significant time manually scanning transaction tables, making subjective judgments that are difficult to scale or audit.

We were motivated to build a system that could read a bank statement the way an experienced underwriter would—by understanding patterns, priorities, and behavior—while remaining explainable, consistent, and regulator-friendly.

What it does

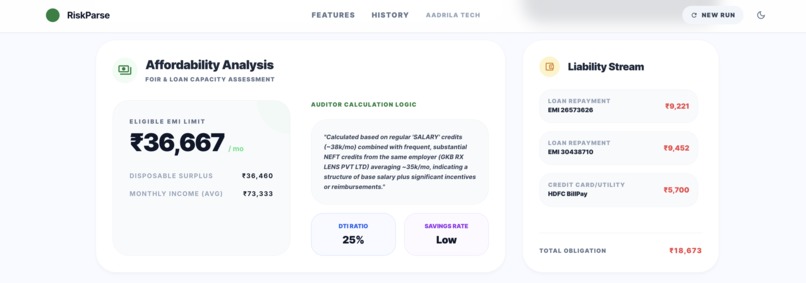

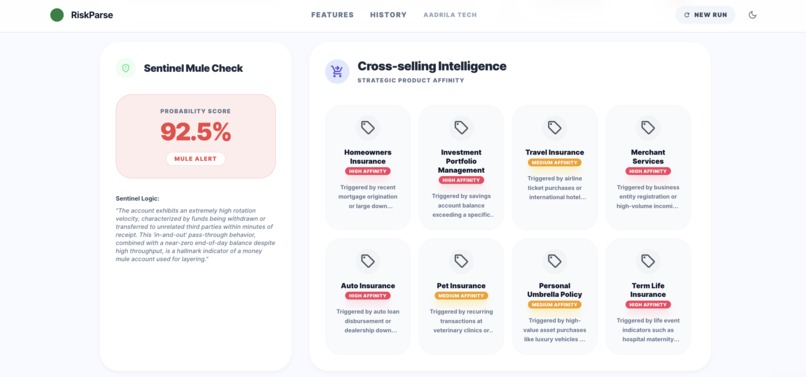

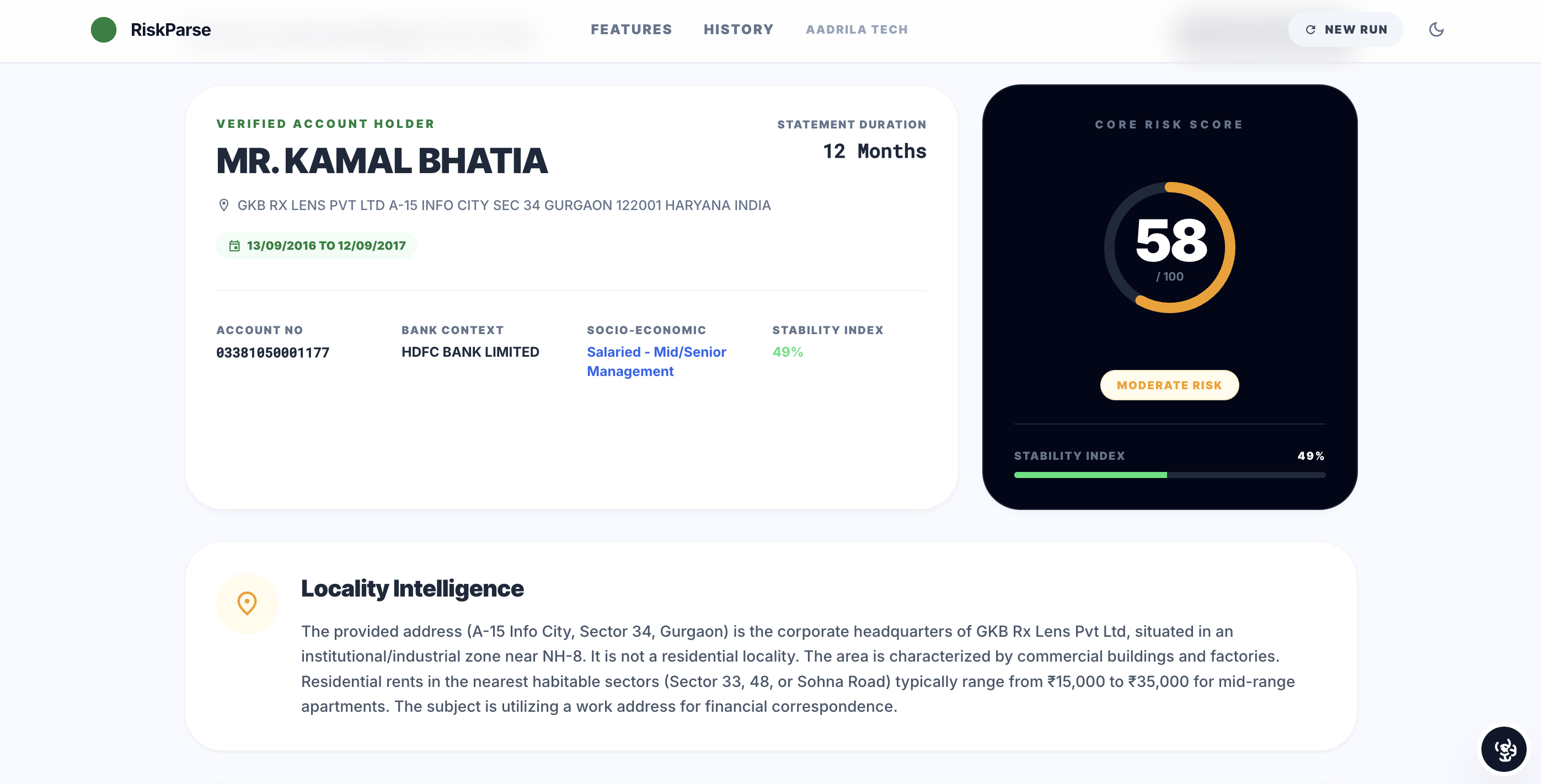

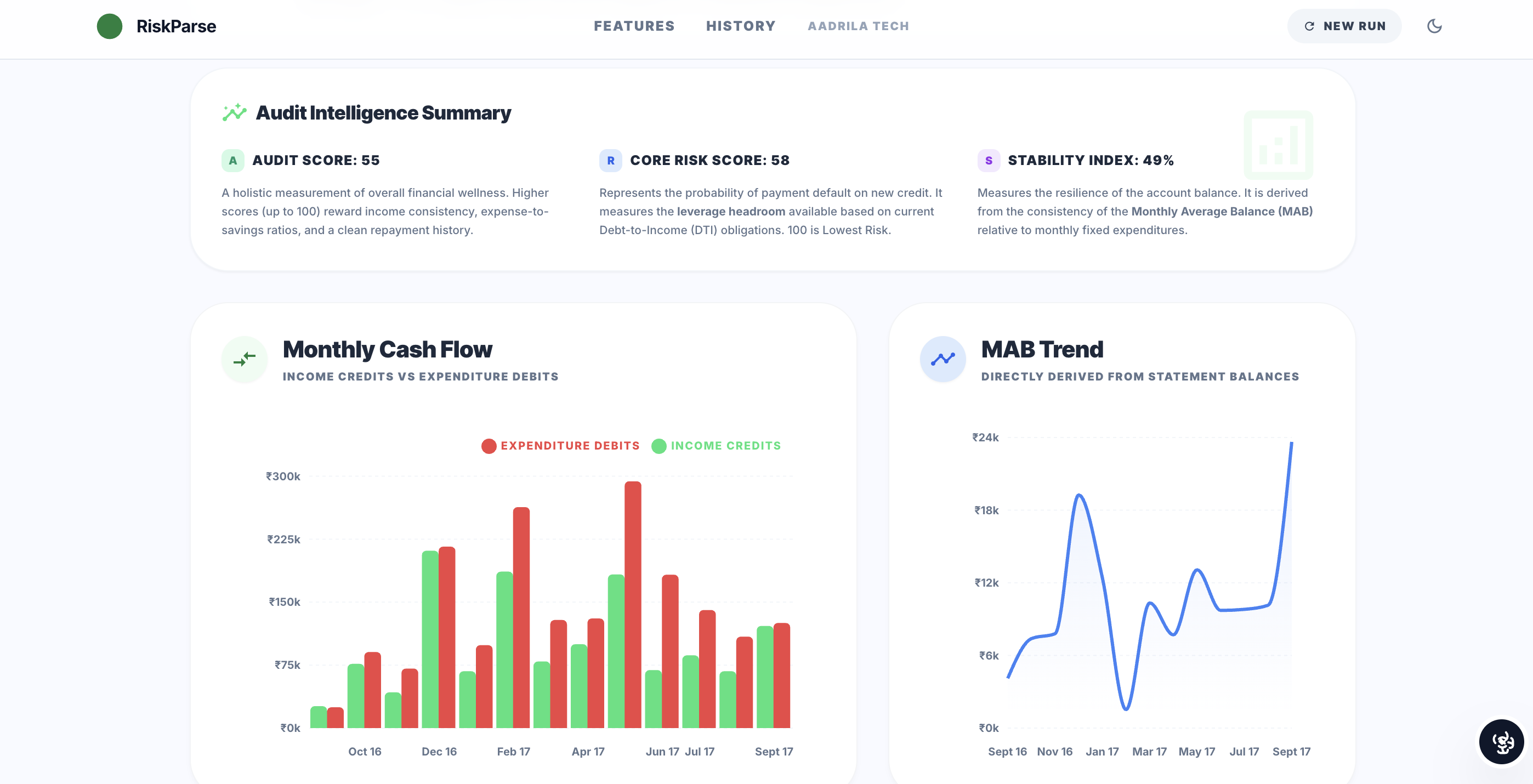

RiskParse converts bank statements into clear, explainable risk intelligence.

Given a bank-issued digital statement, the system:

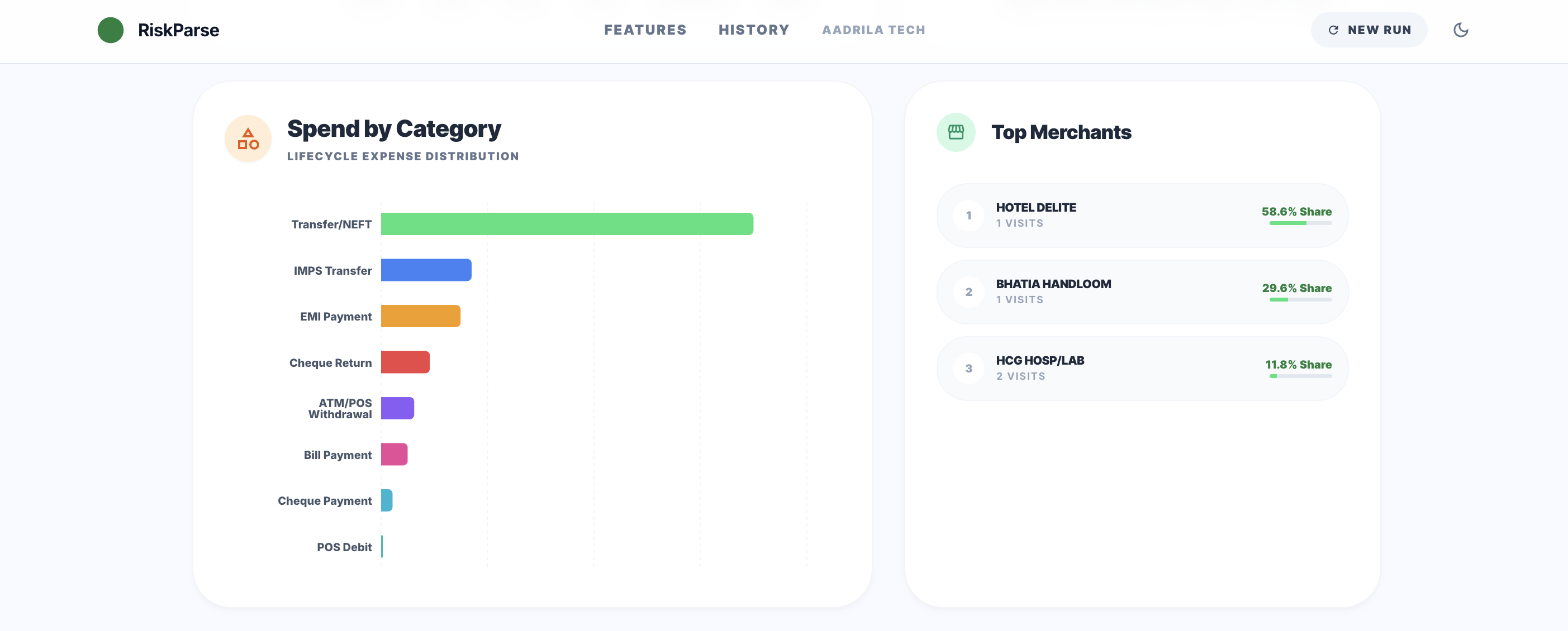

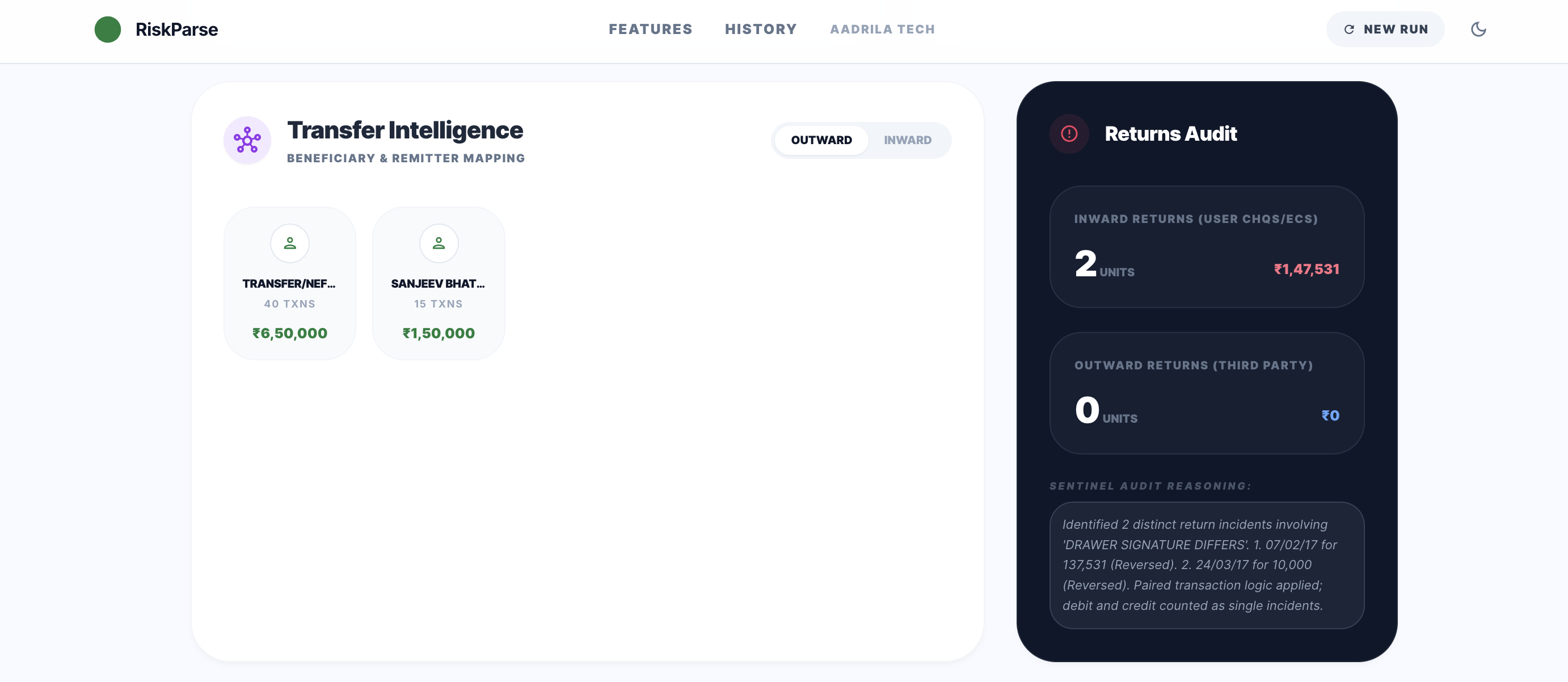

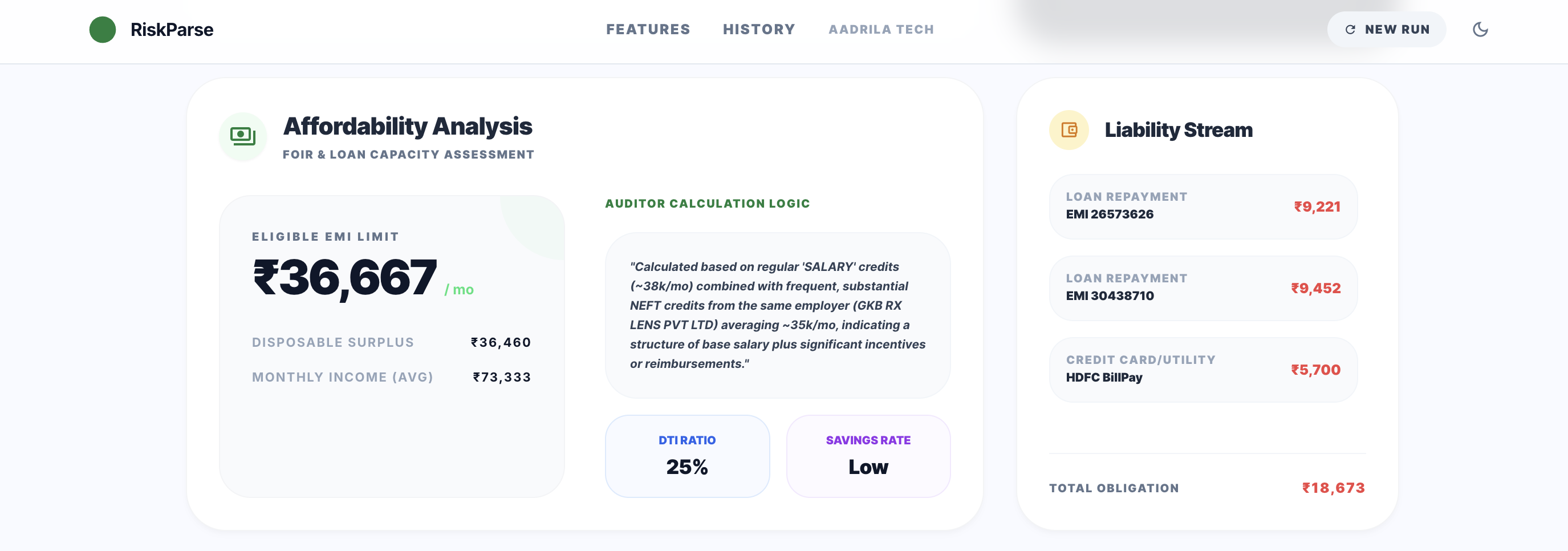

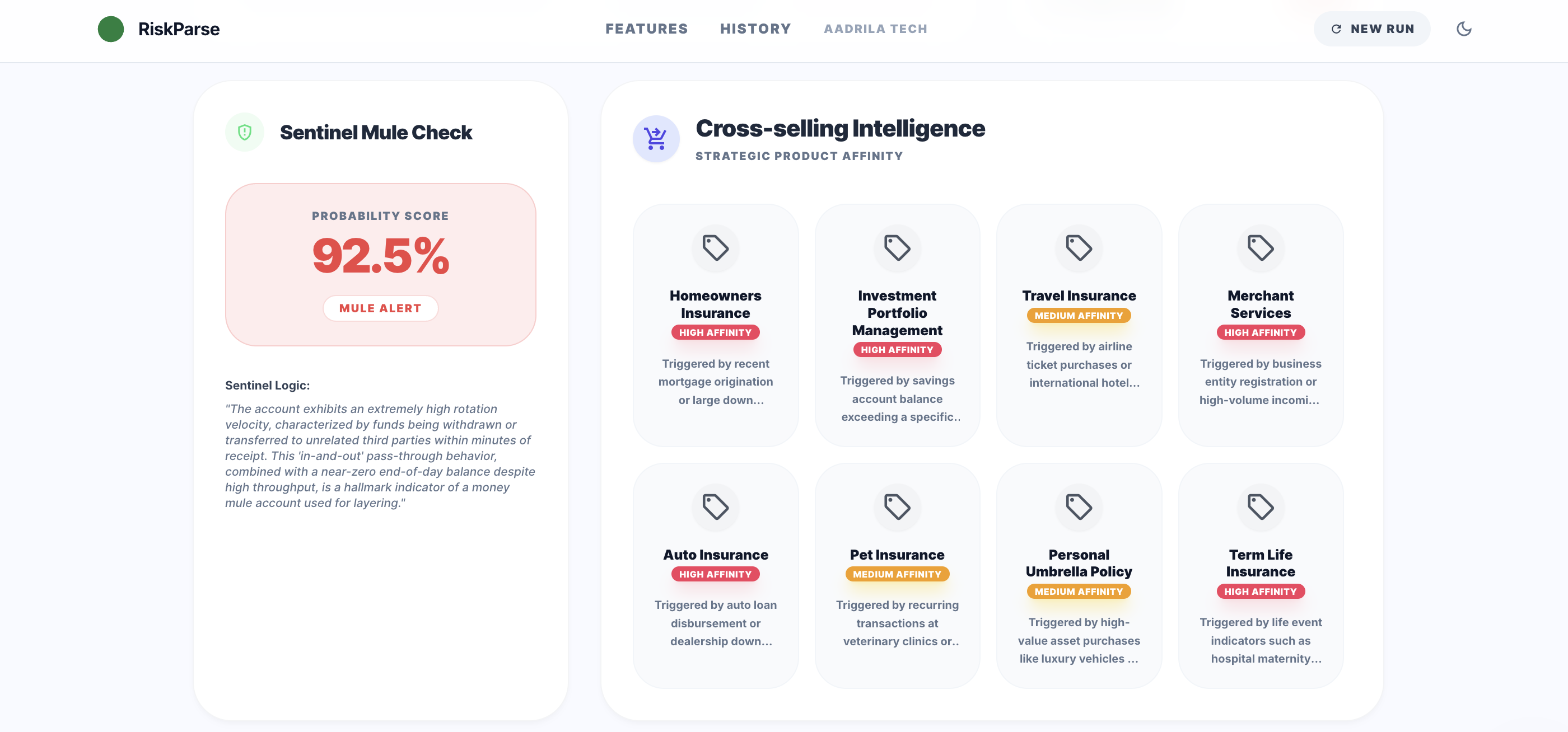

- Extracts and structures transaction-level data

- Categorizes income, expenses, obligations, utilities, subscriptions, and cash usage

- Analyzes behavioral patterns such as income stability, spending discipline, and liquidity stress

- Generates a human-readable financial profile

- Produces a confidence-weighted 0–100 risk score with clear explanations

The result is a lender-ready view of risk derived entirely from transaction behavior, without relying on credit bureaus or opaque black-box models.

How we built it

RiskParse is built as a multi-stage intelligence pipeline:

Parsing and Structuring

Bank-issued digital PDFs are converted into structured transaction data, including dates, descriptions, amounts, and balances.Transaction Enrichment

Transactions are categorized and enriched with behavioral markers such as recurring payments, essential vs discretionary spend, and timing relative to income or EMIs.Dual-Agent Analysis

- An exploratory agent analyzes raw transaction sequences to detect subtle patterns and emerging stress signals.

- A structured profile agent consumes summarized behavioral data to produce a bounded, auditable financial profile.

Deterministic Risk Scoring

Instead of training a premature ML model, we use transparent rules to compute a confidence-weighted risk score based on income stability, expense discipline, obligations, and liquidity behavior.

This architecture balances the flexibility of AI with the reliability required in regulated environments.

Challenges we ran into

One of the biggest challenges was avoiding over-inference. Bank transactions can reveal a lot, but drawing conclusions that are too strong or speculative can create bias and compliance issues. We had to design strict boundaries around what the system is allowed to infer.

Another challenge was balancing insight with determinism. AI models are excellent at discovering patterns, but financial institutions require consistency and auditability. Designing schemas, confidence measures, and reconciliation logic was critical to making outputs trustworthy.

Performance was also a concern, as statements can contain hundreds of transactions. We optimized feature computation and minimized unnecessary processing to keep response times low.

Accomplishments that we're proud of

- Built an end-to-end system that turns raw bank statements into explainable risk signals in minutes

- Designed a dual-agent architecture that separates exploration from decision-making

- Created a risk scoring framework that works without labeled training data

- Ensured all outputs are auditable, transparent, and suitable for regulated financial use

- Demonstrated that meaningful risk intelligence can be derived from transaction behavior alone

What we learned

We learned that financial behavior is more informative than static financial snapshots. Patterns over time—such as how obligations are prioritized or how cash buffers change—often matter more than absolute numbers.

We also learned that explainability is a product feature, not an afterthought. In financial services, trust, clarity, and governance are just as important as predictive power.

Finally, we learned that starting with deterministic logic and AI-assisted reasoning provides a strong foundation before introducing machine learning models.

What's next for RiskParse

Next, we plan to:

- Expand coverage across more bank formats and geographies

- Introduce portfolio-level analytics for lenders and insurers

- Use accumulated insights to selectively introduce supervised learning models

- Enhance early-warning and pre-delinquency signals

- Deepen integrations with loan origination and underwriting systems

Our goal is to make transaction-based risk intelligence a standard layer in financial decision-making, helping institutions lend and insure with greater confidence and fairness.

Built With

- css

- gemini

- pdf.js

- react

- recharts

- tailwind

- typescript

Log in or sign up for Devpost to join the conversation.