-

-

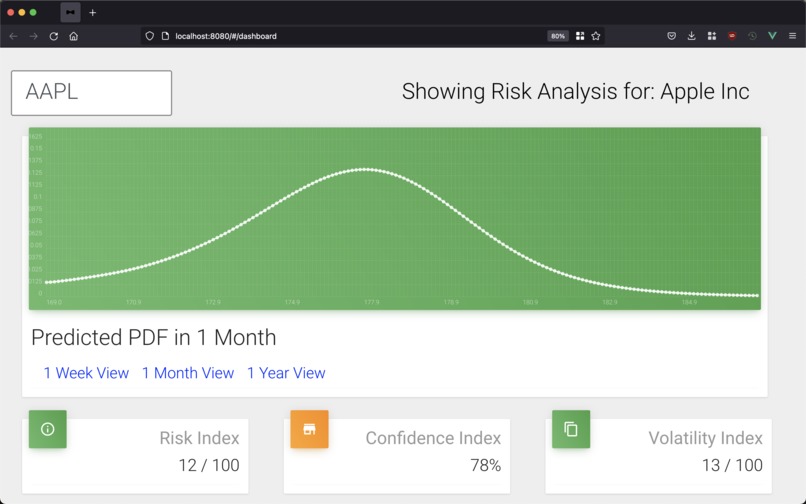

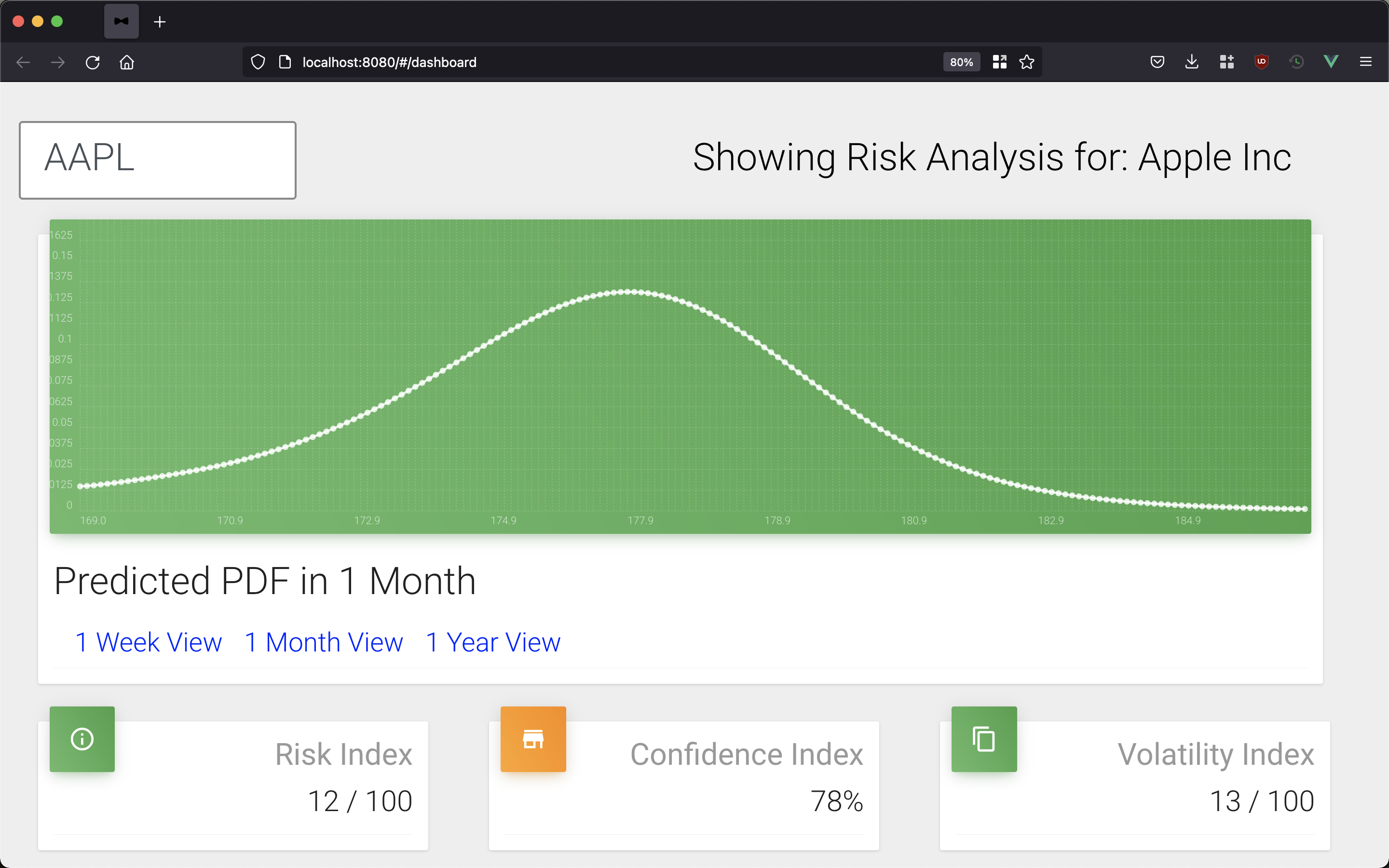

Generated Probability Distribution + Advance Analytics for $AAPL in One Month

Inspiration

We came across the Black Scholes and Breeden Litzenberger models and found their implementation interesting. This fueled the idea of an ML based algorithm that works to ideally outperform the predictions from these models.

What it does

The neural network takes in an input layer of a distribution of current premiums for stock options and their associated strike prices + expiration dates. Manipulating this data through hundreds of calculations it aims to generate a probability distribution function (PDF) made from 30 discrete points (where the x axis is the strike price).

How we built it

- We collected and cleaned upwards of 2 GB of data using Python

- Developed a sequential model in Python

- Developed an adaptation of the Breeden Litzenberger equation to combine with real time data from the stock market to verify the model.

- Built a RAT API in Flask to give live predictions using the model

- Designed a frontend in Vue.js to display live data to users utilizing Flask API

Challenges we ran into

- Data set being too large for the 24 hour time span

Accomplishments that we're proud of

- Developing a solid probability function modeller that works as a proof of concept

What we learned

- We got better with pre-processing data

Log in or sign up for Devpost to join the conversation.