-

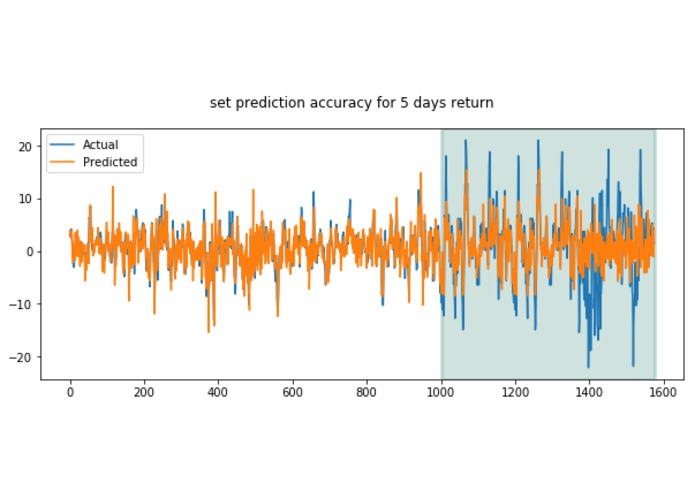

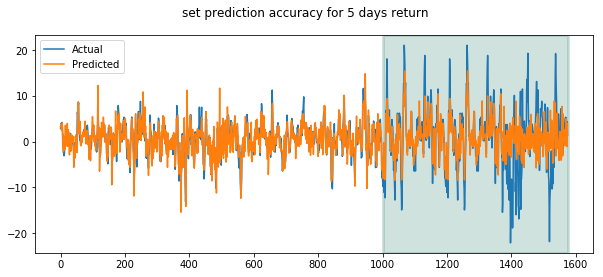

Predicted price movement highly overlap with the actual price movement

-

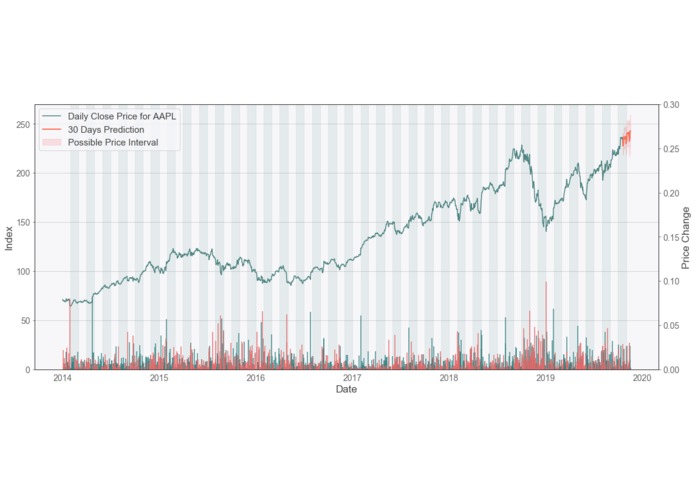

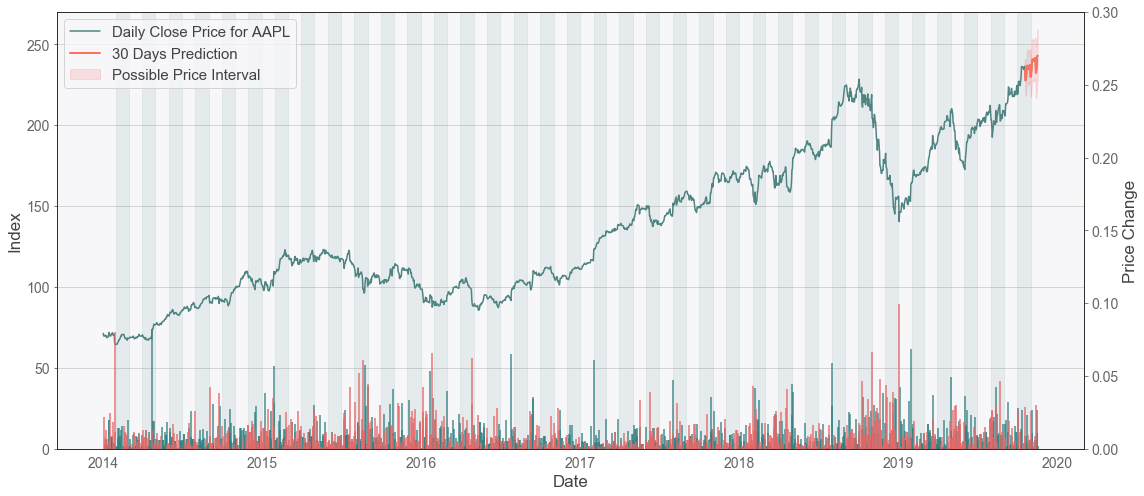

Time series analysis and prediction on AAPL using SARIMA model. It not perform well because of lack of seasonality and self-correlation.

-

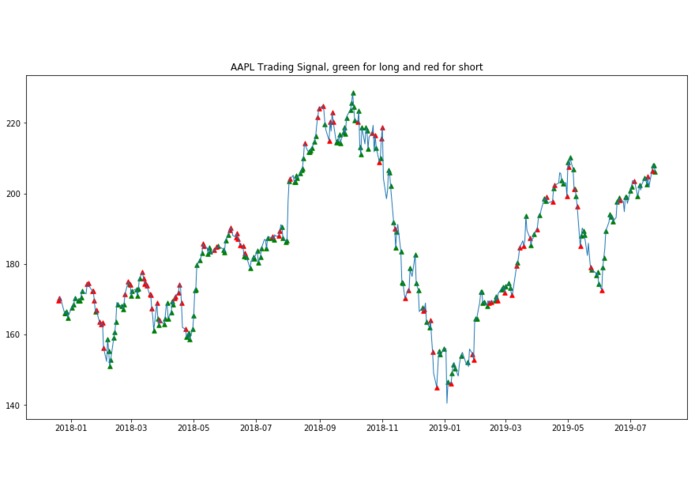

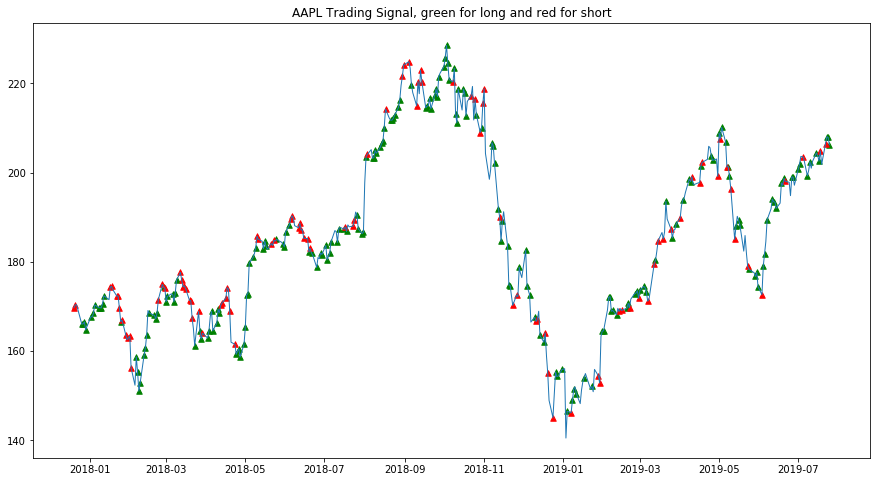

Even it is testing dataset, the model gives shorts signal at the peaks and long signal at bottom. What a promising result

-

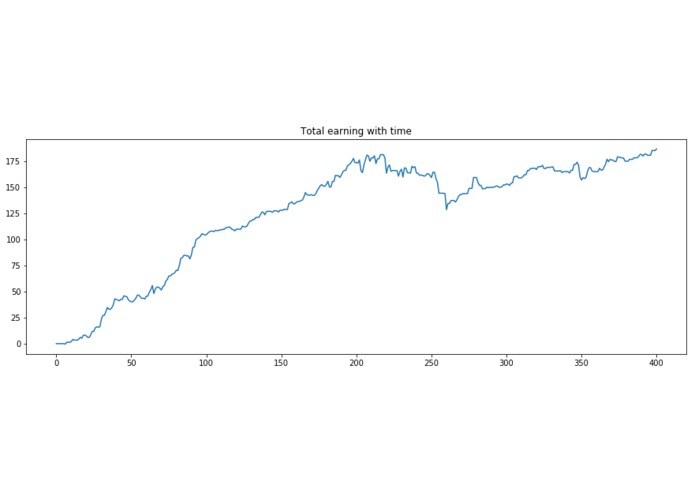

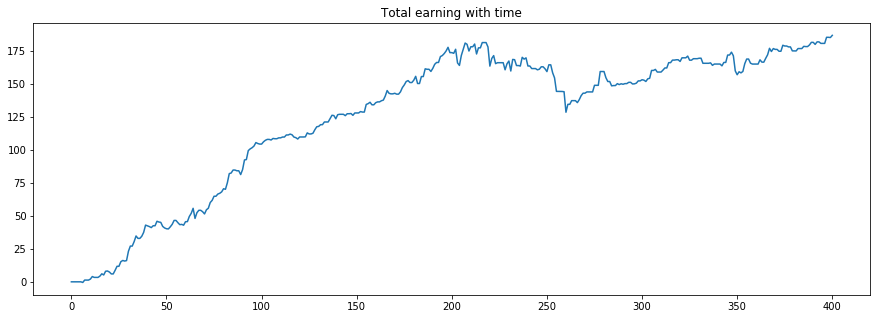

Earning starting with 0 total asset and only trade in testing dataset. We could earn 180 out of 0

-

Using PCA to preserve most of the key and high-quality information while reduce the total complexity to prevent overfitting

This is a thorough analysis on stock price and identify the most important key feature that will help improve the predicting power, which eventually help us developed a powerful algo trading model.

Key content:

- Statistical modelling on selected US stock, de-trending and find seasonality.

- Forecasting price movement based on SARIMA model with hyper-parameter tuning on AWS with optimization in parallel computing.

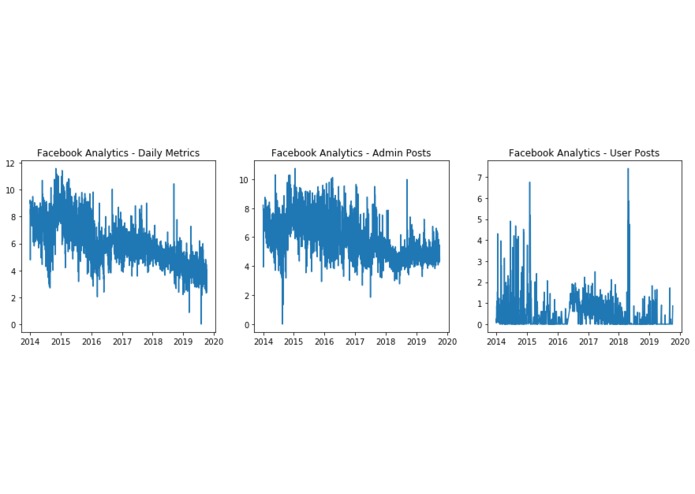

- Exploratory data analysis on social media sentiment scores and engagement scores to identify feature with highest data quality and relevance.

- Use Principle Component Analysis (PCA) to reduce the dimensions and complexity of features, making model more robust.

- Conduct chain analysis to find one’s most related firm.

- Multi-Variate Encoder-decoder Conv-LSTM on sentiment, supply chain and stock prices of relevant firms. Achieved promising result of 76% AUC-ROC result for testing datasets of 3 totally different firms and models, predicting price change after 5 days.

- Extra analysis on how shareholder scores are negatively correlated to stock prices

Result:

- For instance of AAPL, by following the trading signal and applying on the testing dataset, we could earn astonishingly $180 out of 0 starting assets. For AMZN and GOOGL, we achieved 170 and 160 within one year. It shows how robust our model is.

- The AUC for testing dataset is 76% and the predicted 5-days return highly correlated with the actual return.

- We also identify the relationship between shareholder score and stock performance

Challenge:

- the constrain of our data source, many of the major suppliers and customers of the target firm are listed in Taiwan, Japan and Dubai. We did not have the access to those information about their sharer price and financials.

Log in or sign up for Devpost to join the conversation.