-

-

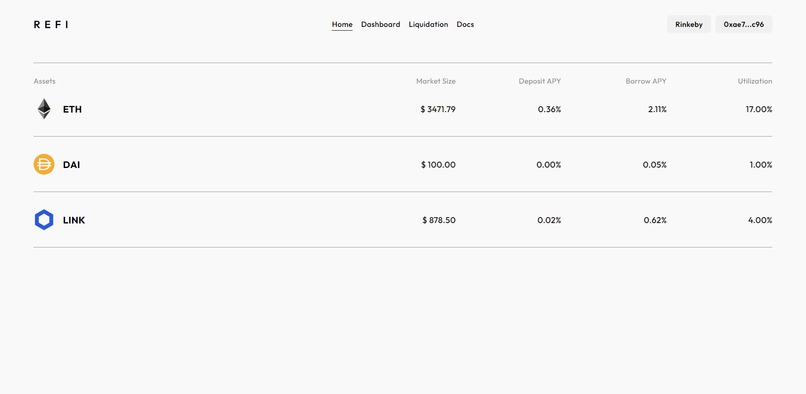

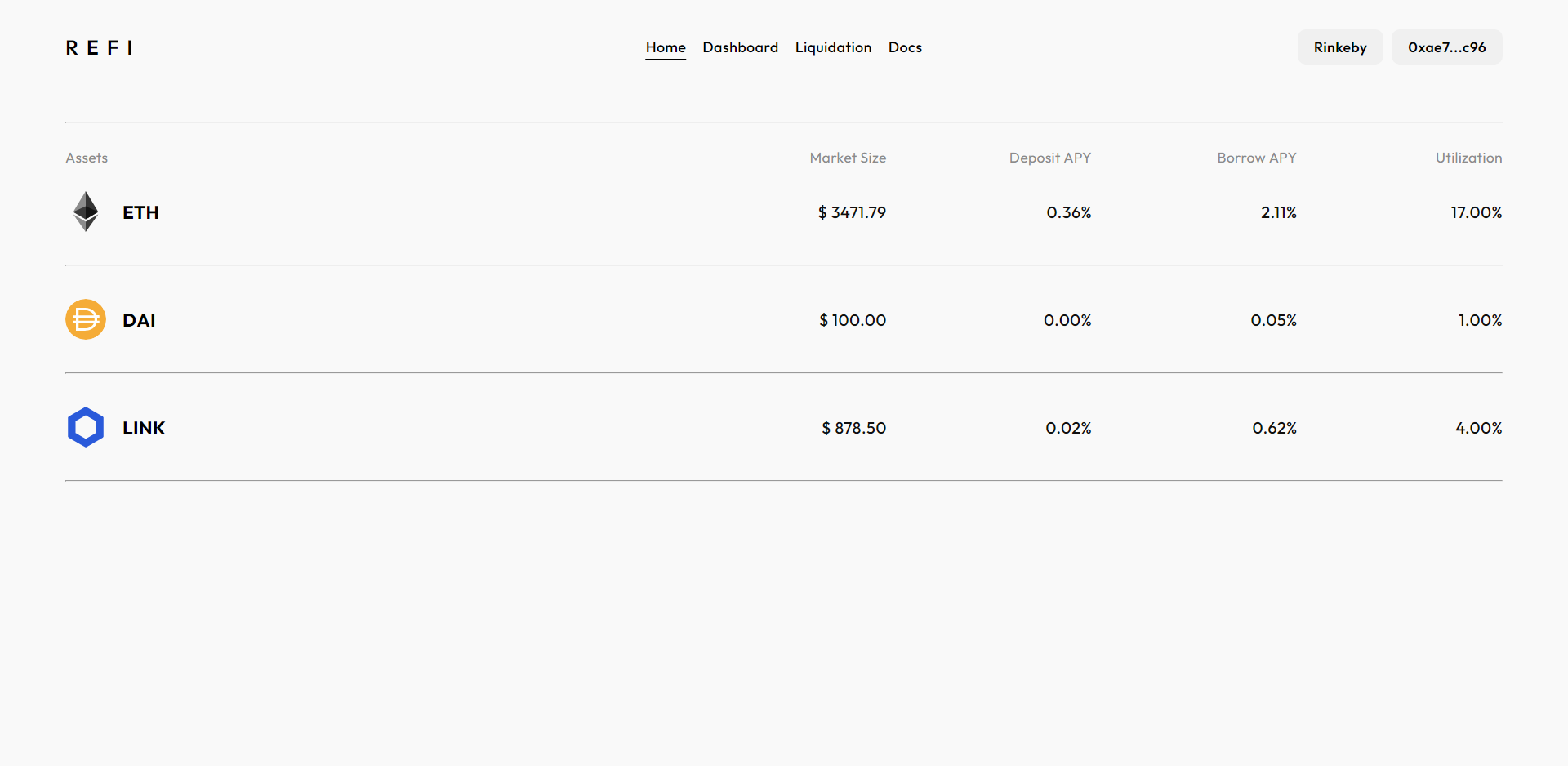

Protocol's home page

-

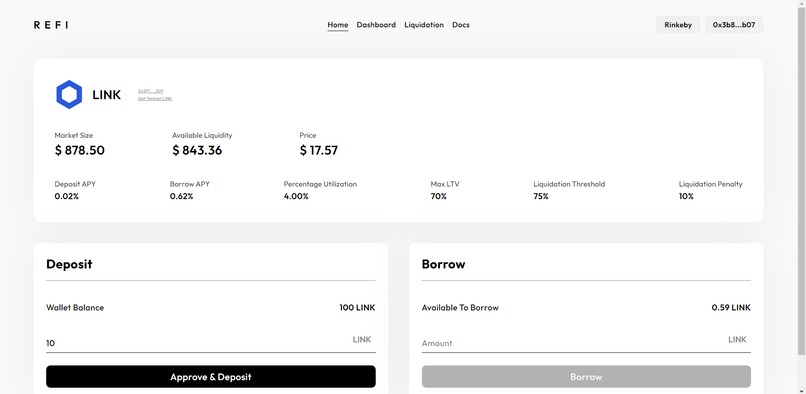

Deposit or borrow individual asset

-

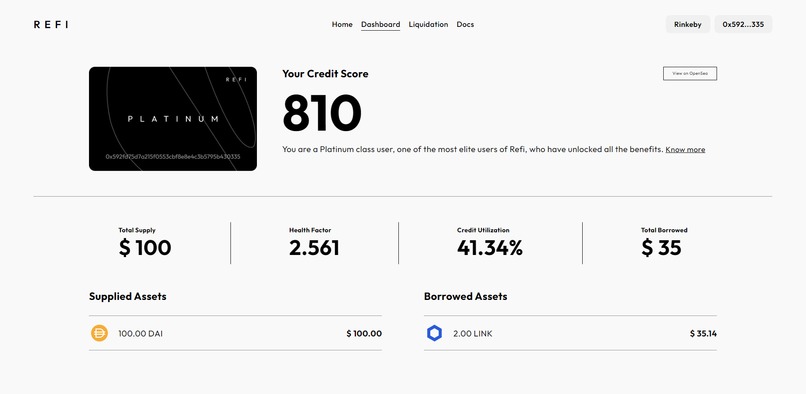

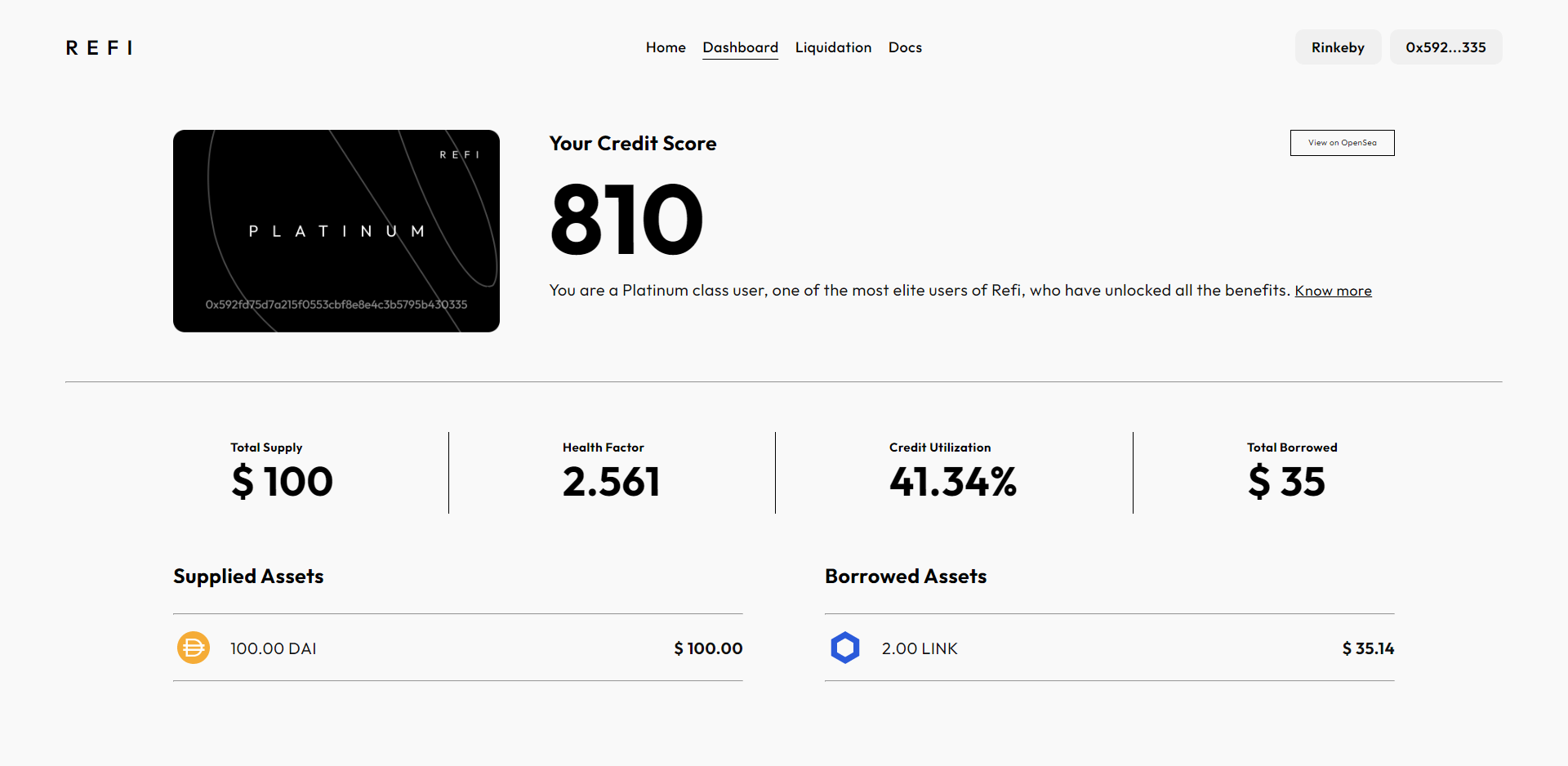

User's dashboard

-

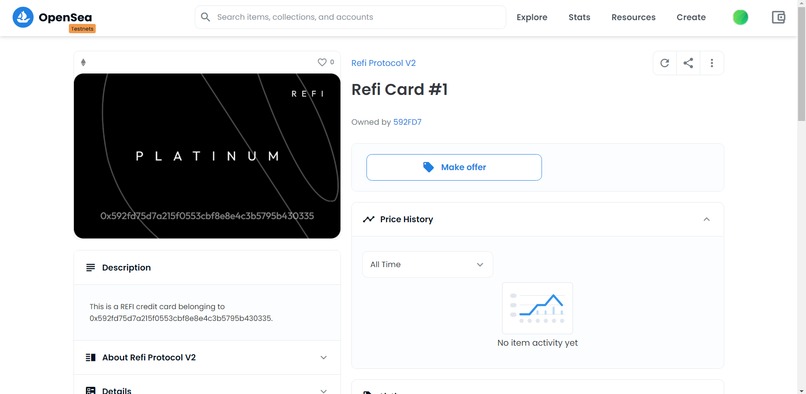

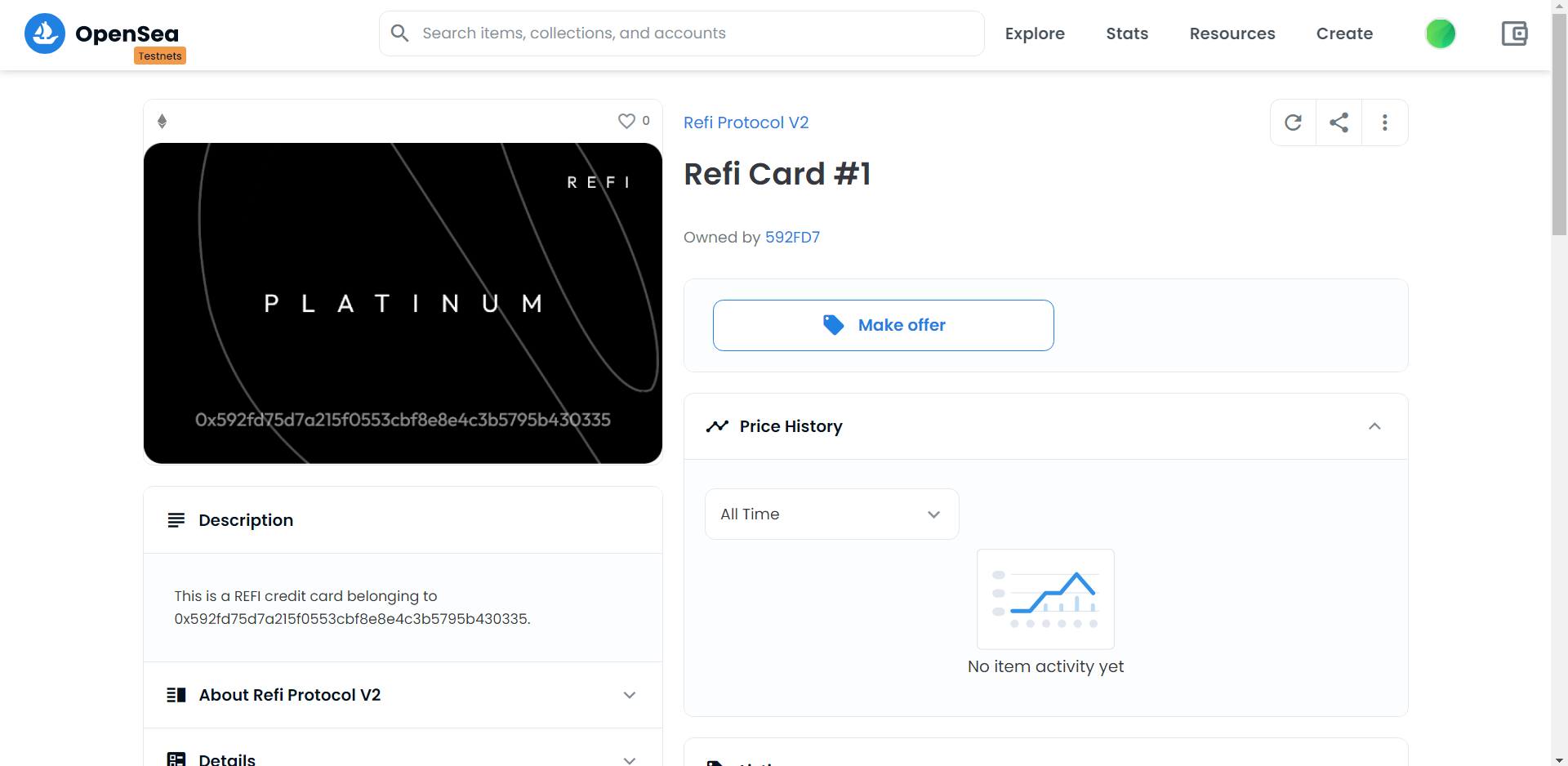

Credit card as NFT

Inspiration

In the existing DeFi protocols, all users have to adhere to the same rules or conditions of lending and borrowing. The users with a good credit record, who maintained their borrow positions at optimal state without ever defaulting don’t get any incentives for doing so. Thus, Refi rewards responsible borrowers with extra borrowing power and thereby incentivizing them and ensuring more liquidity of protocol is borrowed by them. Also, existing Defi protocols feel too complicated with all the technical terms and complex UIs. We have tried our best to keep the UI as simple as possible for normal users. We have also provided a brief documentation explaining all the technical terms related to the protocol. To simplify crypto payments experience, Refi issues on-chain credit cards similar to real world cards. Since the web2 experience of credit cards is replicated in web3, this takes the UX for crypto payments to the next level.

What it does

Refi is a variable interest rate lending & borrowing protocol that maintains a credit score for its users and also issues on-chain credit cards. Refi tracks every user's financial activities in its lending pool and calculates/maintains an on-chain credit score. The higher the credit score, the higher a user can borrow against their deposited collateral. The users are divided into 4 classes based on their credit score i.e. Bronze (300-600), Silver (600-700), Gold (700-800) and Platinum (800-900). All users of a class receive the same benefits and higher classes provide higher borrowing capacity. Users can get their Refi credit card as an NFT. The credit card has a borrow limit and lets user borrow and pay in a single transaction. This allows user to pay an asset without holding it or swapping existing ones for it. And since the card is an NFT with all necessary features, it makes external dapps easier to integrate Refi payments.

Features -

- Lending & borrowing protocol built on top of AAVE with Simple and Minimal UX

- Protocol health monitored using Chainlink price feeds

- Deployed Subgraph that tracks all positions on the protocol and serves as a base for liquidation data

- Dedicated liquidation page that makes it easier for liquidators to find under-collateralized loans

- Unique on-chain Credit scoring framework for Defi protocols

- Dynamic LTV and Liquidation threshold based on user’s credit score

- On-chain Refi credit cards that make crypto payments seamless

- Credit cards minted as dynamic NFTs that change their look and feel based on user’s credit score

- Immutable storage of credit card images on IPFS

How we built it

In order to implement a credit scoring framework, we needed a base DeFi protocol. We chose AAVE v2 as they had an extensive and beginner friendly documentation with a well organized code base. We would really like to thank the AAVE community for this, as it definitely helped a lot. We built a minimal implementation of it consisting of only variable rate lending and borrowing. The next phase was to create a credit scoring framework. To know more about the approach used in calculating and maintaining credit scores see this

Challenges we ran into

As complete beginners in the field of DeFi, it took us a lot of time and efforts to understand AAVE's algorithms and architecture. Thus, for the initial iteration of Refi, we decided to drop some features from AAVE v2. So, to get started, we built a minimal implementation of it consisting of only variable rate lending and borrowing.

What we learned

For this project, we first studied the Aave protocol in depth. And during this process, we learnt some really important things.

- How a Defi lending/borrowing protocol works at its core

- Variable and stable interest rate mechanisms

- How to design the architecture for an industry grade smart contract application

- Upgradable proxy architecture

- Solidity design patterns

- Advanced solidity features

What's next for Refi

Currently the project is at prototype stage. We plan to implement the following features that will make it usable and manageable by masses.

- A DAO with Governance mechanism that grants higher voting power to higher class users

- Upgradable contract architecture

- Other AAVE features such as stable rate, flash loan, etc.

- “Pay with Refi” widget for Dapps to easily integrate card payments

Log in or sign up for Devpost to join the conversation.