-

Bloqade QAOA Portfolio Optimization

Inspiration We started as five freshmen with almost no quantum background, but we were excited by the challenge of applying quantum computing to a real-world finance problem. The insurance portfolio optimization setting immediately stood out to us because it combines return, risk, liquidity, and solvency constraints in a way that feels practical and important. Our main motivation was to build something that was understandable, useful, and impressive without pretending we were quantum experts from day one.

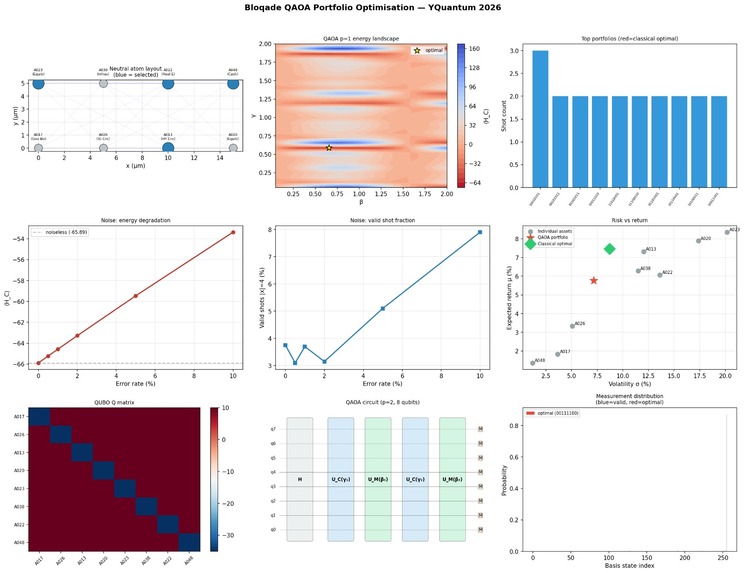

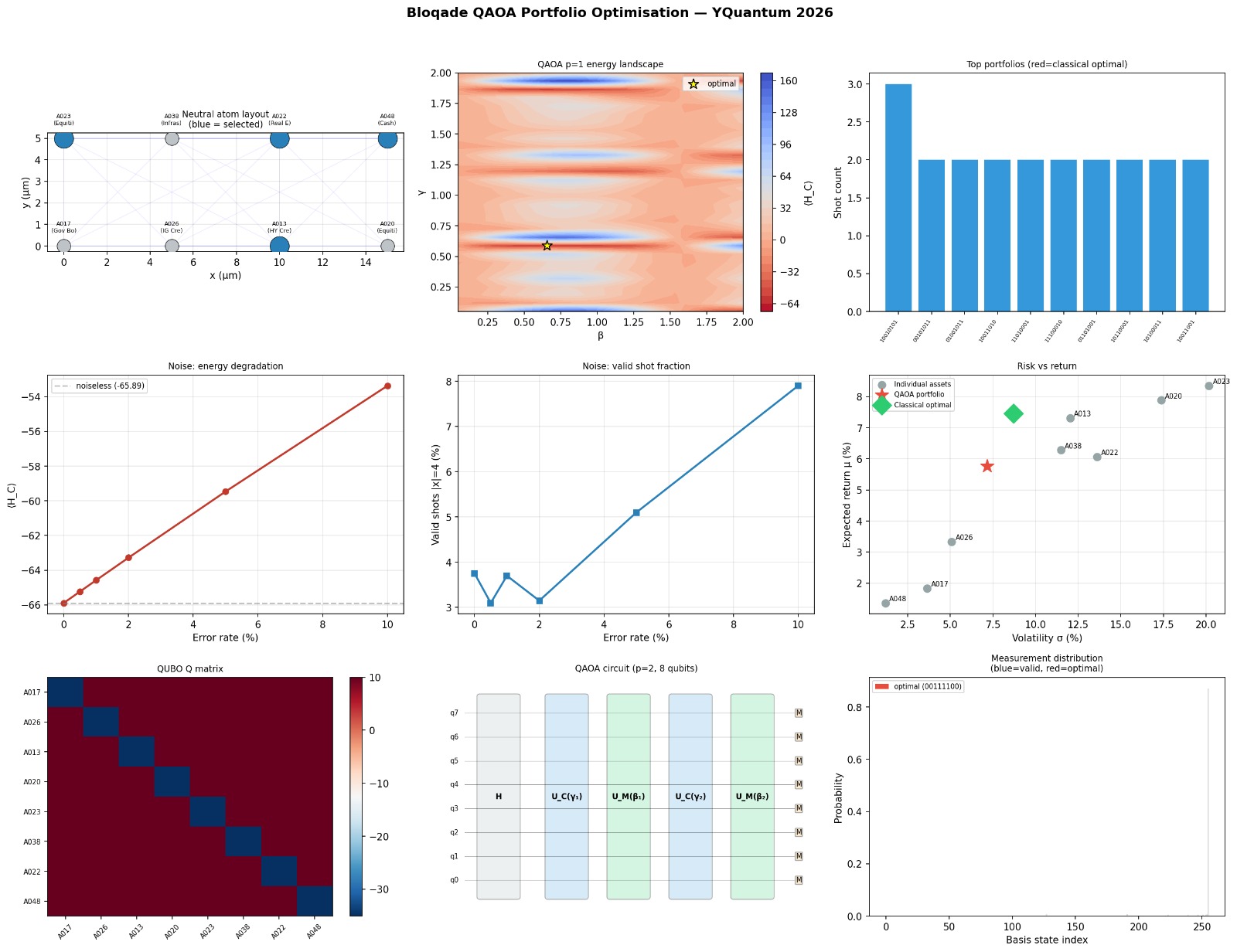

What it does QuBots is a quantum-classical hybrid portfolio optimization demo for insurance investing. It takes a set of assets, models the tradeoff between return and risk, and then reformulates the selection problem into a QUBO / Ising representation. From there, we compare classical portfolio methods with a quantum-style QAOA workflow on Bloqade’s neutral atom simulator, including noise and connectivity effects.

How we built it We started from zero and learned the basics step by step: what qubits are, what QUBO means, and why optimization problems can be mapped into quantum circuits. First, we built a classical baseline in Python so we could understand the finance side of the problem and verify that our results made sense. Then we reduced the full dataset to an 8-asset version, encoded it as a binary optimization problem, and built a QAOA circuit for the neutral-atom hardware model. Along the way, we relied on a lot of debugging, documentation reading, and simplifying our scope so we could get a working MVP instead of getting stuck trying to do everything at once.

Challenges we ran into The biggest challenge was that everything was new to us. We had to learn finance, optimization, and quantum computing at the same time, which made the early stages slow and confusing. We also spent time dealing with Python environment issues, package compatibility problems, and figuring out how to make the Bloqade workflow run reliably. Another challenge was learning how to explain quantum ideas in a way that still felt clear to judges and stakeholders.

Accomplishments that we're proud of We are proud that we turned a difficult and unfamiliar topic into a working project. We built a complete pipeline from financial data to portfolio optimization to quantum-inspired execution and analysis. We also created a demo that shows both the technical side and the practical side of the problem, which makes the project easier to understand for non-quantum audiences. For five freshmen with no quantum background, getting this far is something we are genuinely proud of.

What we learned We learned that quantum computing becomes much less intimidating when you break it into small, understandable pieces. We learned how important a classical baseline is before attempting any quantum approach. We also learned that good hackathon projects are not just about code — they are about scope control, teamwork, communication, and persistence. Most of all, we learned that starting from zero is okay as long as you keep moving forward.

What's next for QuBots If we keep developing QuBots, we want to improve the quantum-side implementation, make the noise analysis more realistic, and create a cleaner stakeholder-facing interface. We would also like to test additional portfolio scenarios and compare more optimization strategies. In the future, QuBots could become a more polished tool for understanding how quantum methods might help with real insurance portfolio decisions.

Log in or sign up for Devpost to join the conversation.