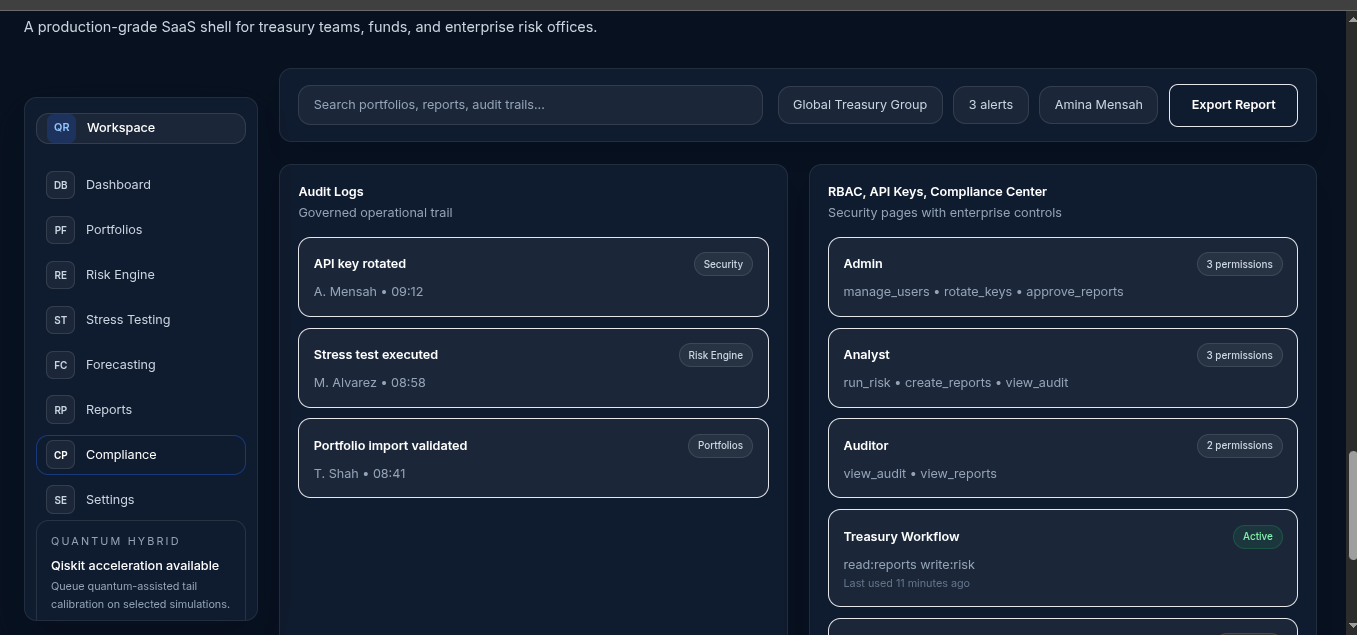

Inspiration

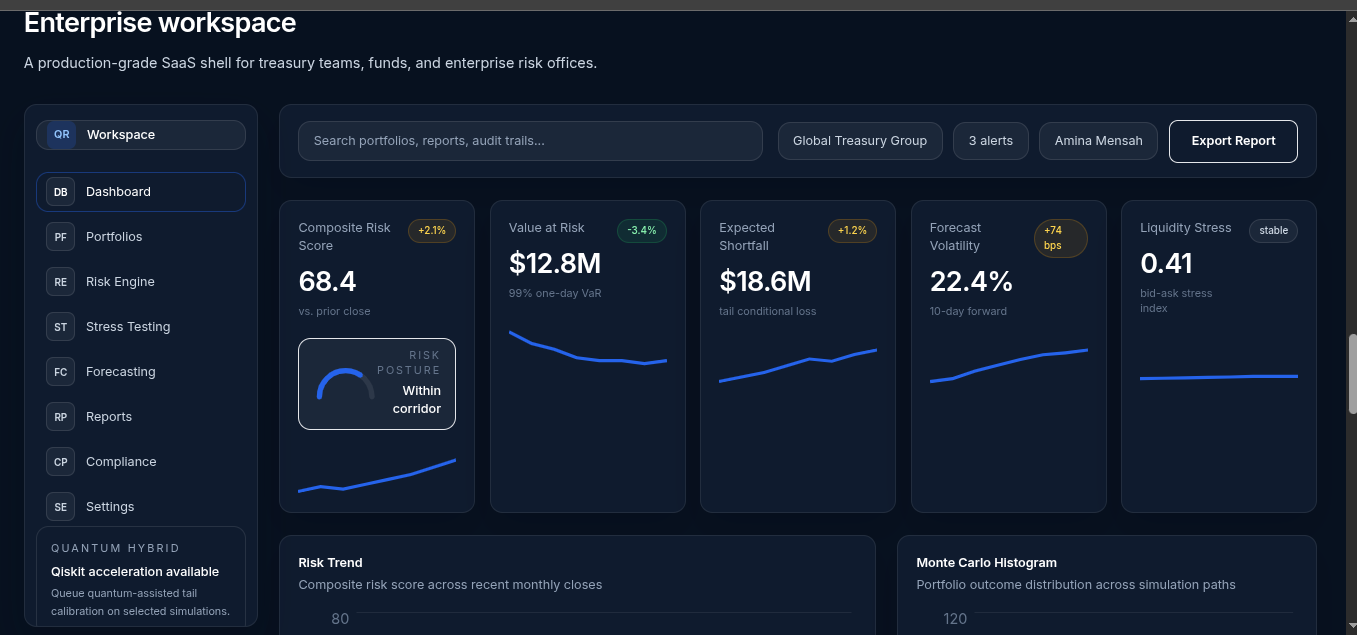

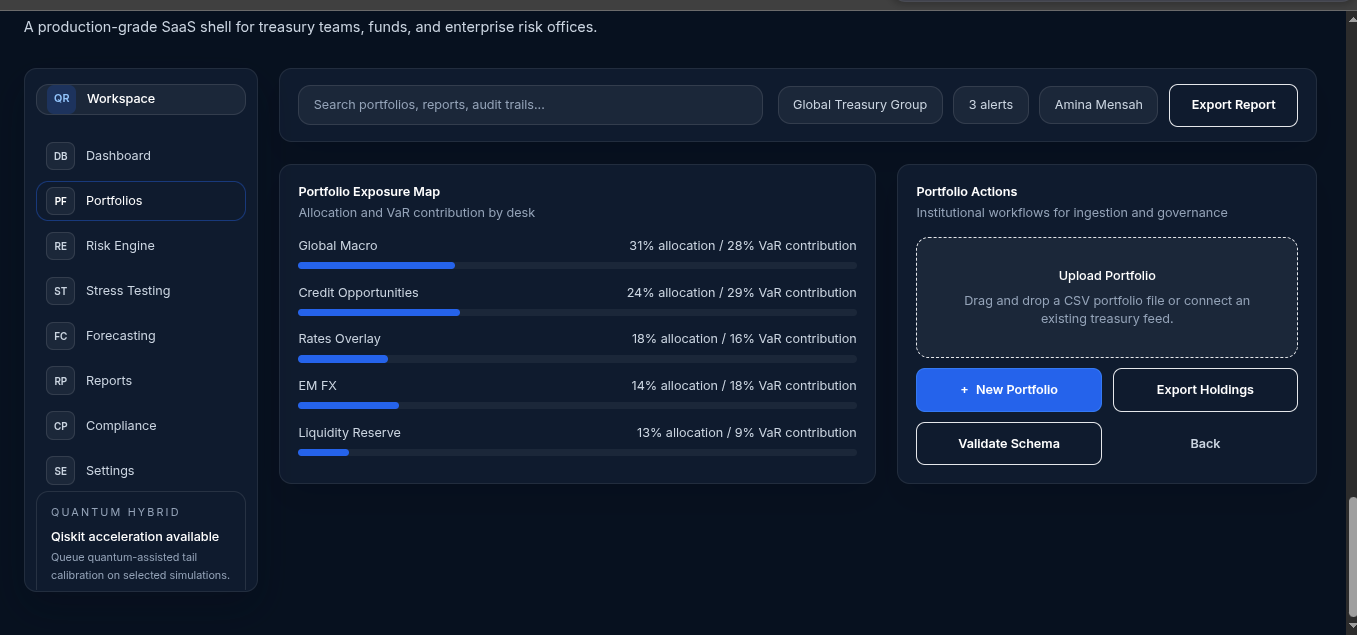

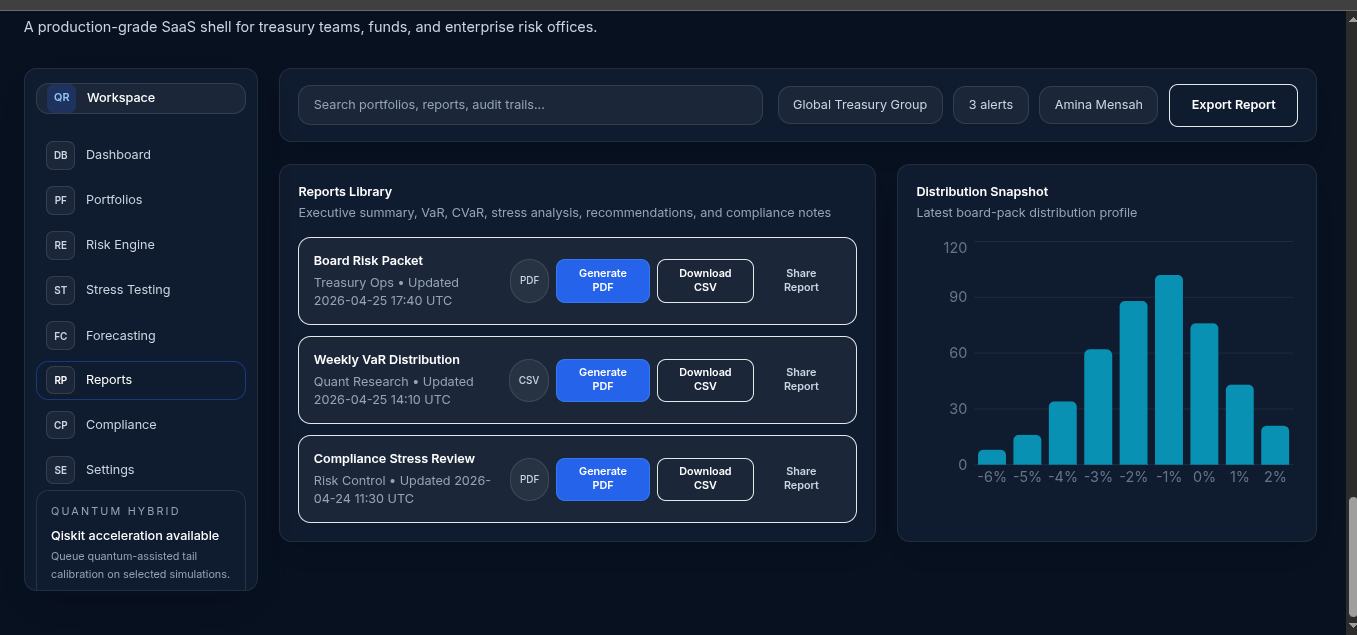

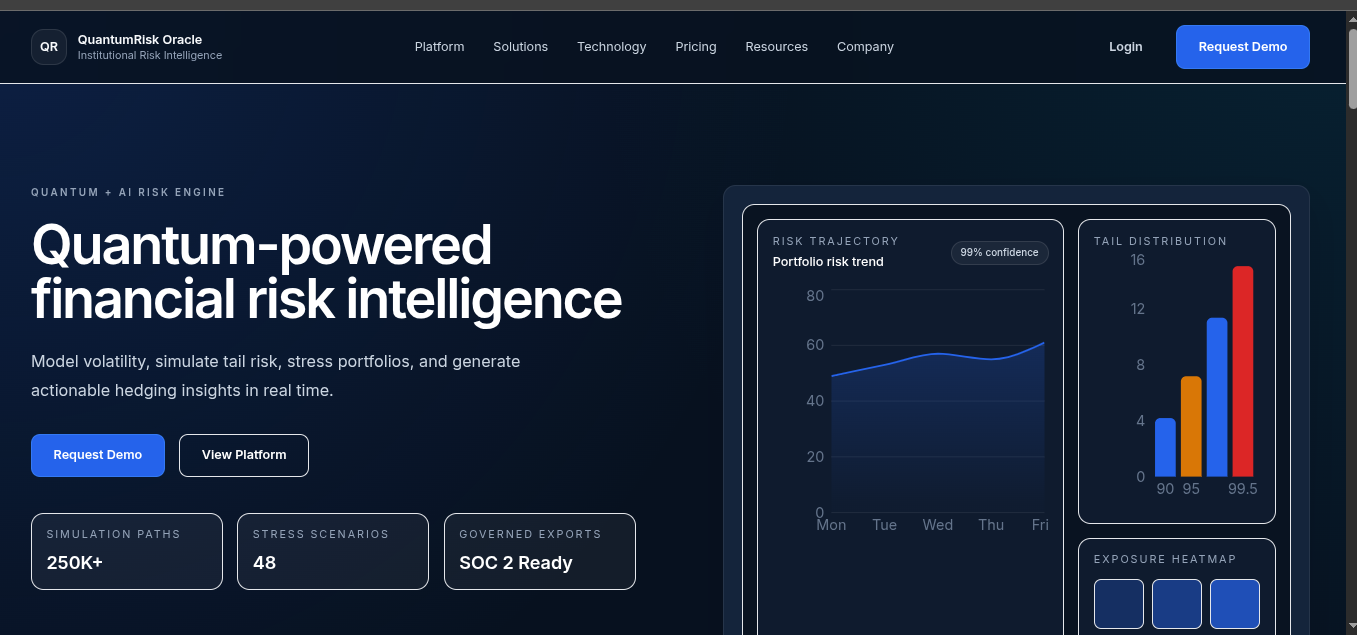

Financial risk intelligence has historically been concentrated in large institutions with access to proprietary infrastructure, quantitative research teams, and advanced computational resources. Smaller businesses and growing financial firms often lack tools capable of forecasting volatility, modeling downside exposure, and stress testing portfolios under uncertainty.

QuantumRisk Oracle was inspired by one core question:

$$ \textit{Can advanced financial risk modeling be democratized through hybrid quantum and AI systems?} $$

We explored the intersection of probabilistic simulation, machine learning, and quantum-inspired optimization to build a platform that transforms complex portfolio analytics into clear, actionable decision intelligence.

At the mathematical core of financial risk lies uncertainty modeling:

$$ VaR_{\alpha}(X) = \inf \left{ x \in \mathbb{R} : P(X \le x) \ge \alpha \right} $$

Tail-risk exposure can be measured using:

$$ CVaR_{\alpha}(X) = \mathbb{E}[X \mid X \ge VaR_{\alpha}(X)] $$

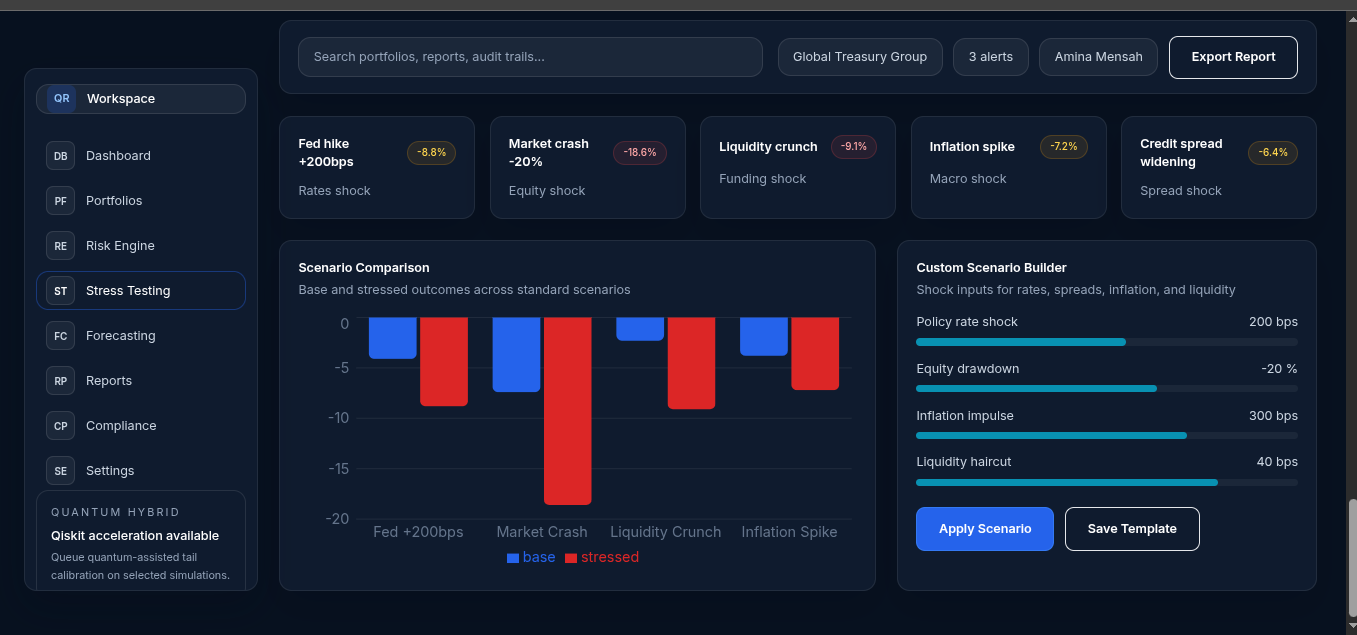

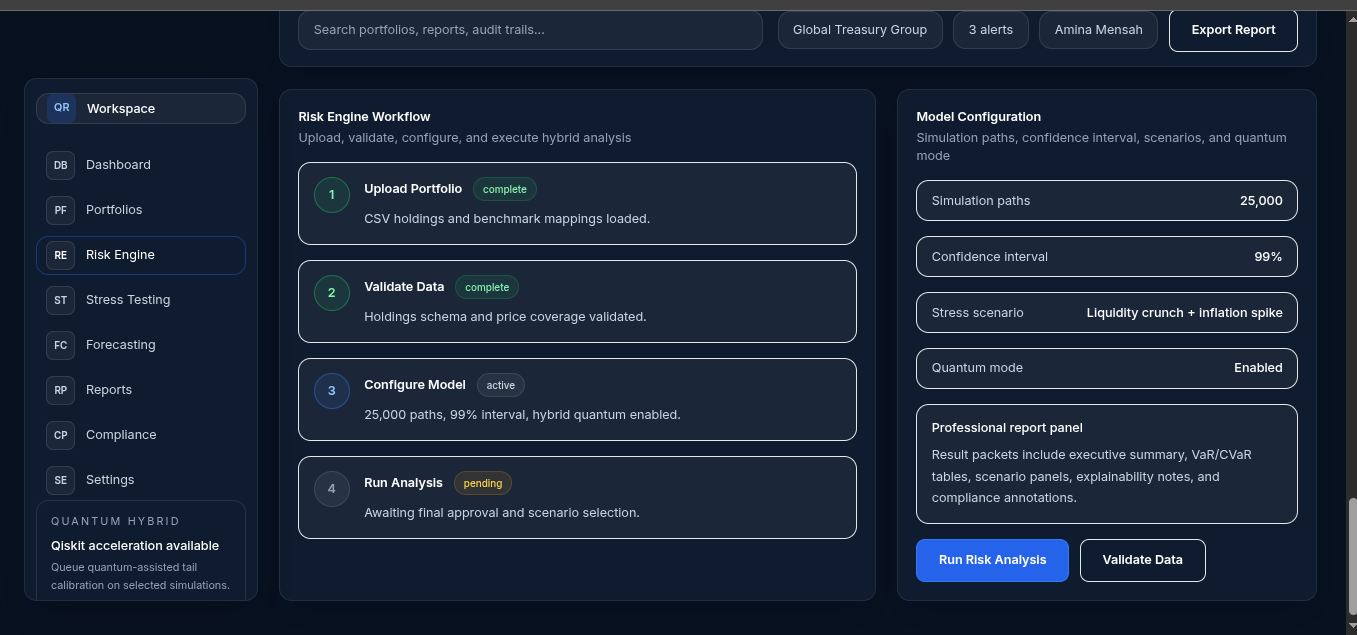

Classical Monte Carlo simulation estimates these efficiently, but hybrid quantum-inspired approaches may improve computational performance and enhance sensitivity to extreme tail events.

Our system combines:

$$ \text{AI Forecasting} + \text{Quantum Simulation} + \text{Risk Analytics} \;\rightarrow\; \text{Actionable Financial Intelligence} $$

The mission behind QuantumRisk Oracle is simple:

Make institutional-grade risk intelligence scalable, explainable, and accessible for every modern business.

Built With

- actions

- ai

- amazon-web-services

- celery

- cloud

- devops

- docker

- flask

- frameworks

- github

- infrastructure

- kubernetes

- ml

- postgresql

- python

- pytorch

- qiskit

- quantum

- react

- redis

- shap

- sql

- tailwindcss

- typescript

- xgboost

Log in or sign up for Devpost to join the conversation.