Inspiration

Hundreds of millions of dollars were made in the stock market within a split second. Not because of a price spike, or even a price change at all;

In fact, nothing was even traded. Investors just capitalized upon the $0.89 ticker difference between the NYSE and the NASDAQ.

Markets are full of inefficiencies — slippage between intended and actual price, arbitrage gaps across correlated instruments, momentum signals that disappear in seconds. For those who can act on them fast enough, the opportunities are real. As a team of avid investors, we built QuantMind to solve a problem we face ourselves: how to consistently spot and capitalize on these windows before they close, without needing a dedicated financial advisor or an expensive Bloomberg terminal.

What it does

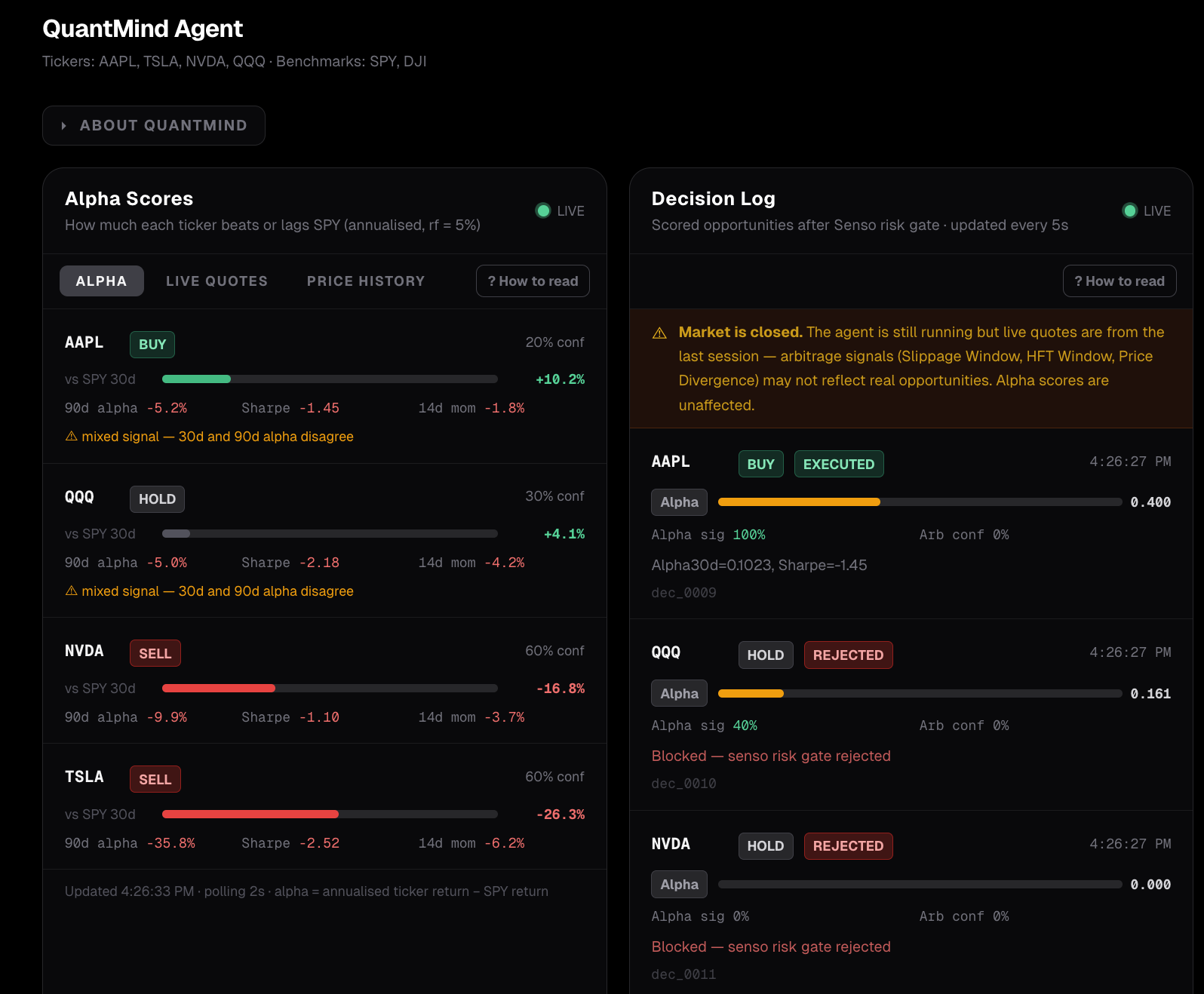

QuantMind is an autonomous AI agent that continuously analyzes financial markets, identifies alpha opportunities, and gets smarter after every cycle. It monitors multiple tickers against benchmark indexes like DJI and SPY, detects high-frequency arbitrage windows and positive slippage opportunities, and refines its own strategy based on what worked and what didn't — with no human required to keep it running. The agent doesn't just execute — it learns. Every decision it makes is logged, evaluated, and fed back into its own model through Overmind's optimization loop. Traders can also provide direct feedback to fine-tune the agent's risk appetite and market focus, making it adaptive to both market conditions and human intent.

How we built it

We built QuantMind as a four-layer autonomous agent stack: Python pipelines market data from Yahoo Finance into Ghost every 5 seconds, where a Claude-powered decision engine reads live OHLCV data, calculates rolling alpha and Sharpe ratios, and outputs ranked trading signals through a FastAPI backend — every signal then passes through Senso as a hard risk gate (enforcing spread thresholds, position limits, and volatility rules) before Overmind logs the outcome, compares predicted vs realized alpha, and continuously tightens the agent's decision policy across cycles. A React dashboard ties it all together with five live-polling panels, giving traders real-time visibility into signals, risk status, and the agent's measurable improvement over time — all the way down to a natural language feedback input that folds trader intent directly back into the agent's strategy.

Challenges we ran into

The hardest problem wasn't building any single module; it was making four components within 4 hours. Getting Senso and the Claude decision engine to agree on a risk contract was trickier than expected: confidence scores needed to map cleanly onto hard thresholds without the risk layer killing legitimate signals. The self-improvement loop presented its own challenge — Overmind needs resolved outcomes to learn from, but a hackathon doesn't give you days of live trading history, so we seeded it with historical scenarios to demonstrate measurable accuracy gains from cycle 1. Kiro and Kiro-cli were instrumental in getting past the initial integration barriers — we went from zero to a working build in under 30 minutes.

Accomplishments that we're proud of

Shipping such a large project in a tight time frame. Throughout the process, we are proud to have prioritized:

Reliability and Currency of Data (Yahoo Finance, Ghost)

Simplicity of Interface (React, Next.js)

Constant Improvement (Overmind)

Feedback-focused Adaptation (Senso + Overmind)

These facets help our agent succeed and most effectively adapt to match the user and current market. We hope to continue reinforcing these facets after the hackathon.

What's next for QuantMind

We're just scratching the surface of what the architecture can support. Next steps include expanding coverage to a broader universe of equities, adding options flow and macro indicators as signal inputs, and introducing multi-agent parallelism so QuantMind can run specialized sub-agents per sector simultaneously. The self-improvement loop also becomes dramatically more powerful with more time and data — we're excited to see where the accuracy metrics land after 30 real trading days.

Log in or sign up for Devpost to join the conversation.