-

-

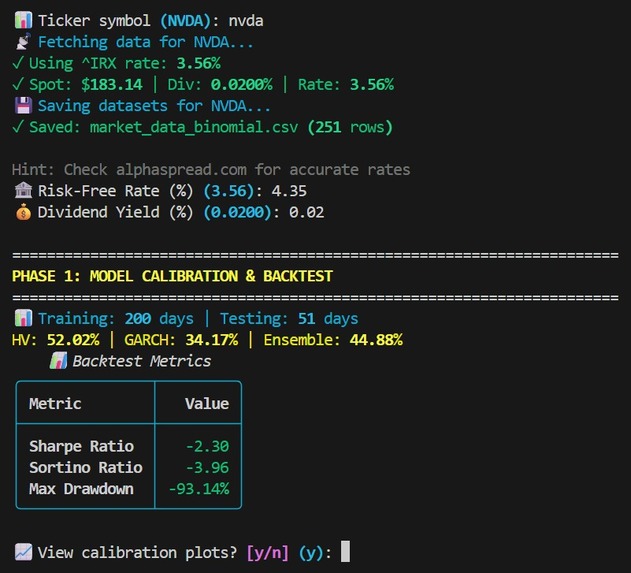

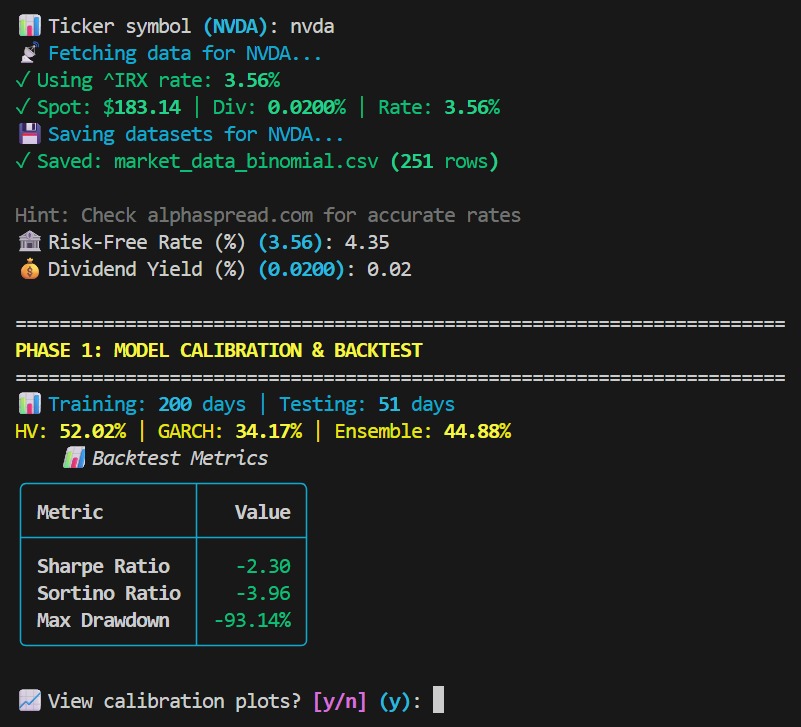

Institutional-grade model calibration and backtest metrics in action.

-

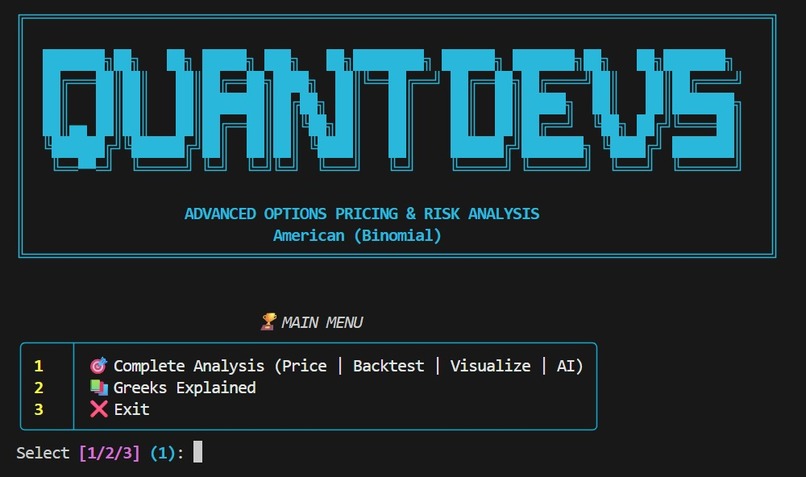

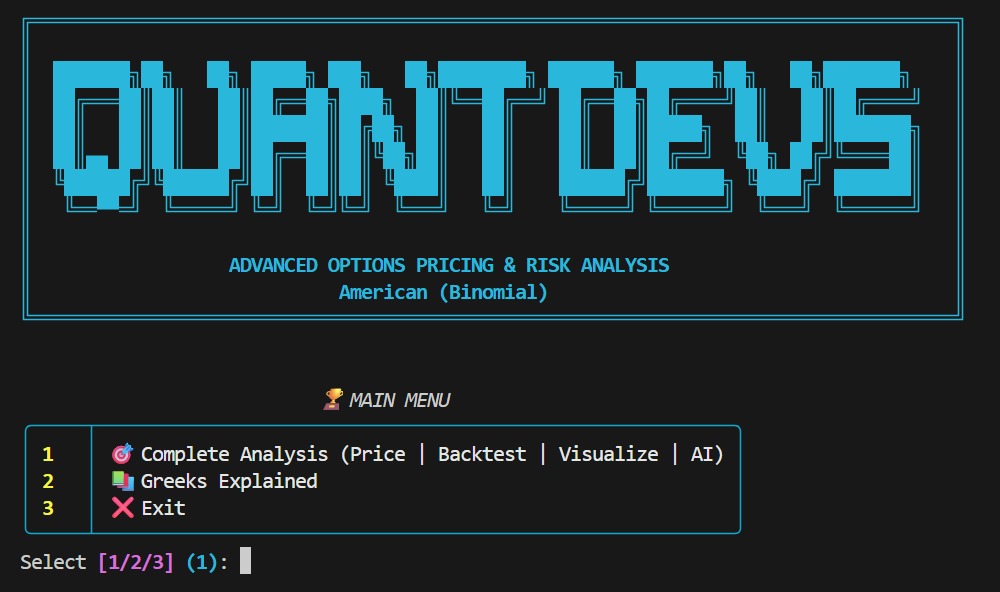

The sleek, terminal-based main menu of the QuantDevs pricing engine.

-

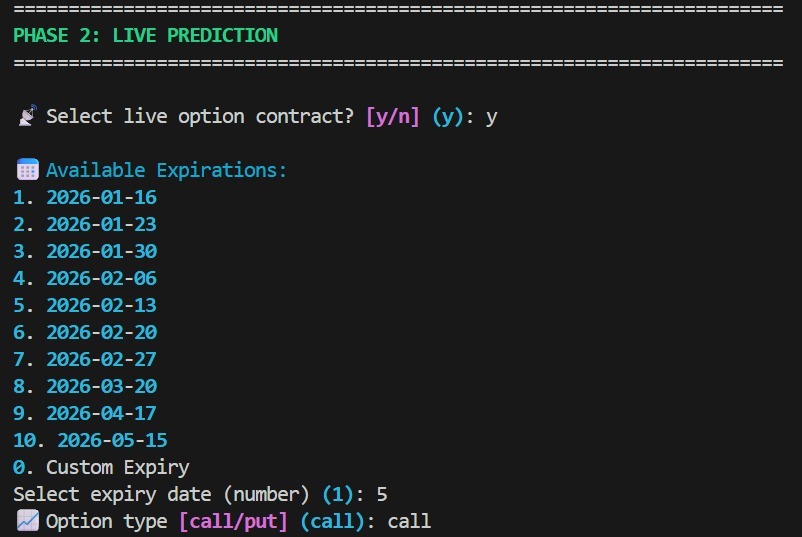

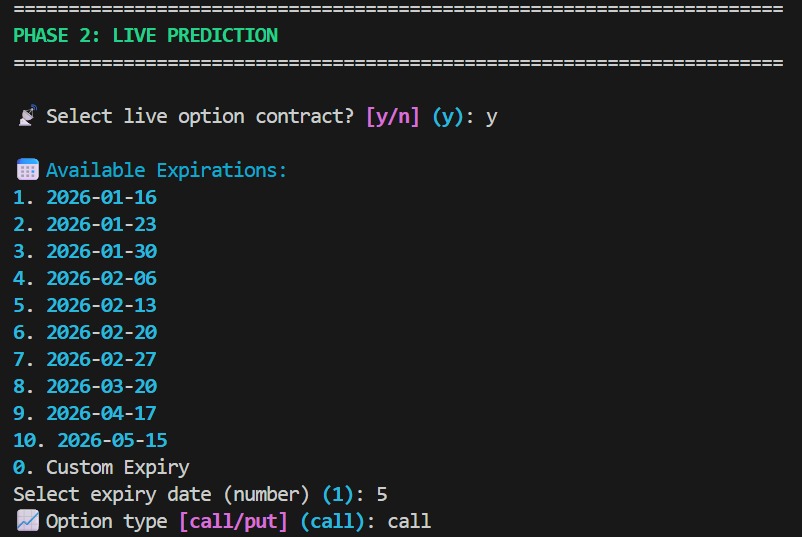

Fetching live options chain data for real-time market analysis.

-

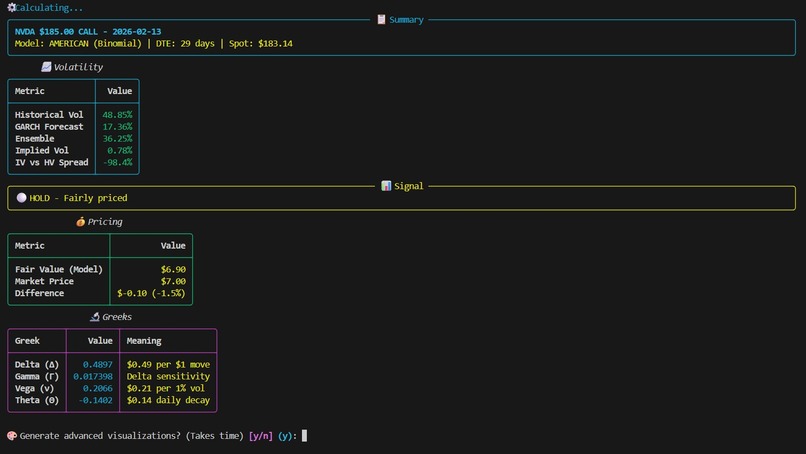

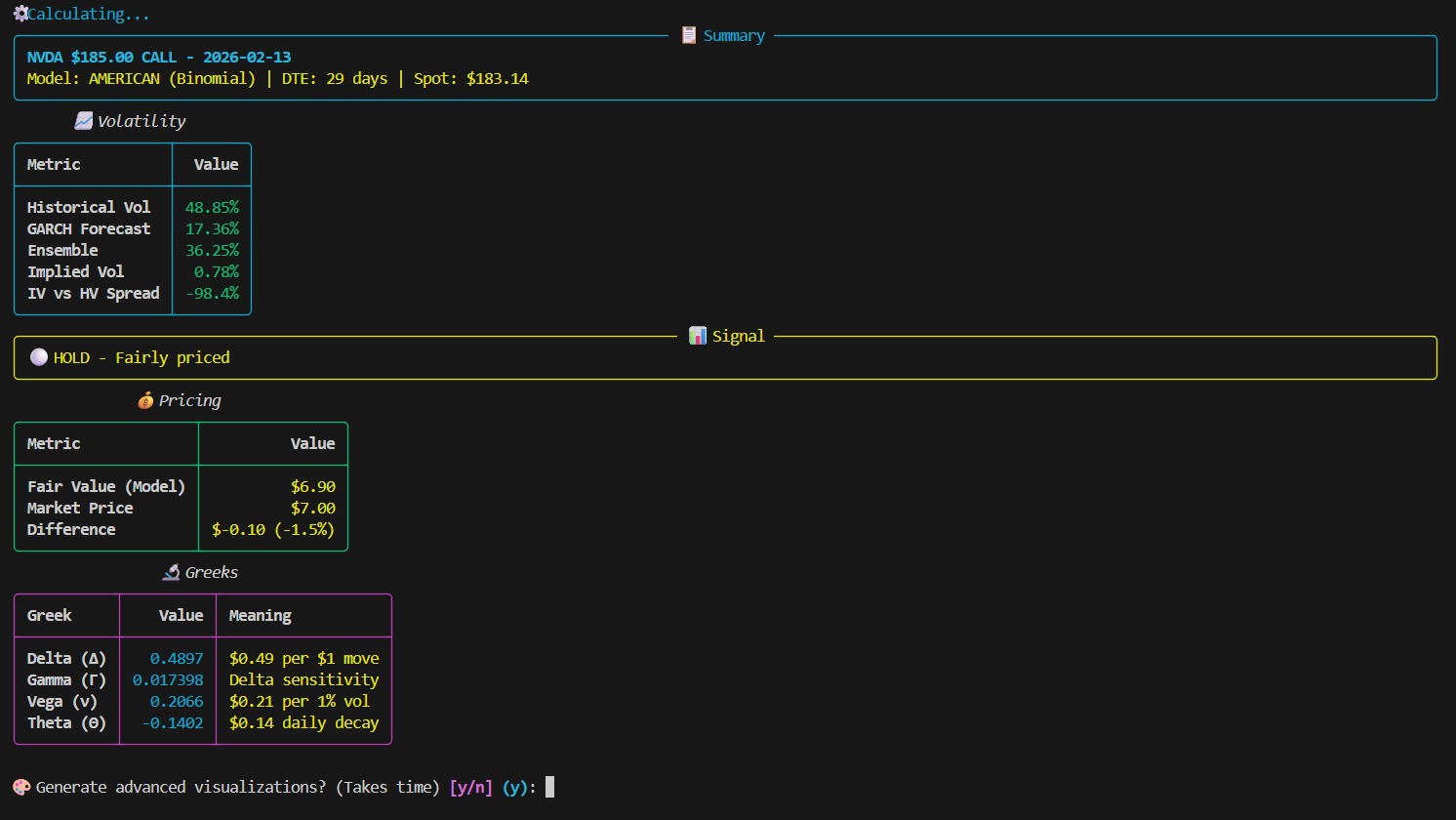

Instant fair value pricing, volatility analysis, and dynamic Greeks.

-

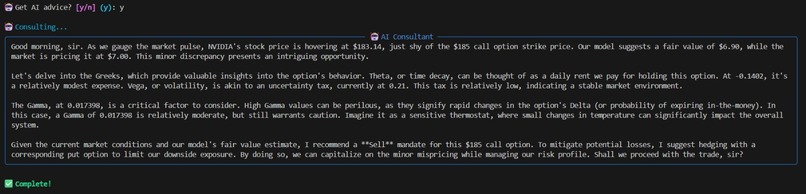

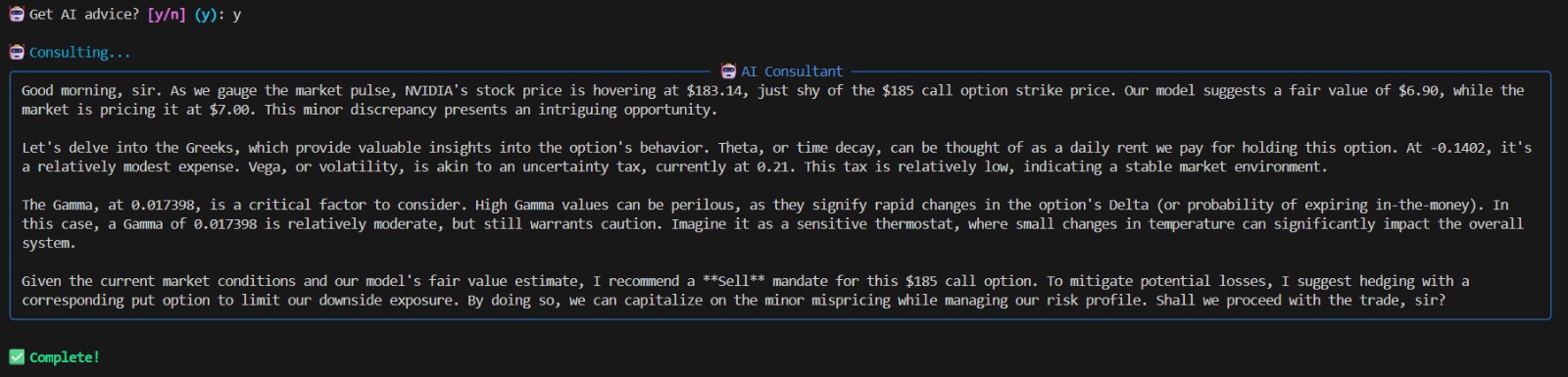

LLaMA-powered AI generating actionable strategic investment memos.

-

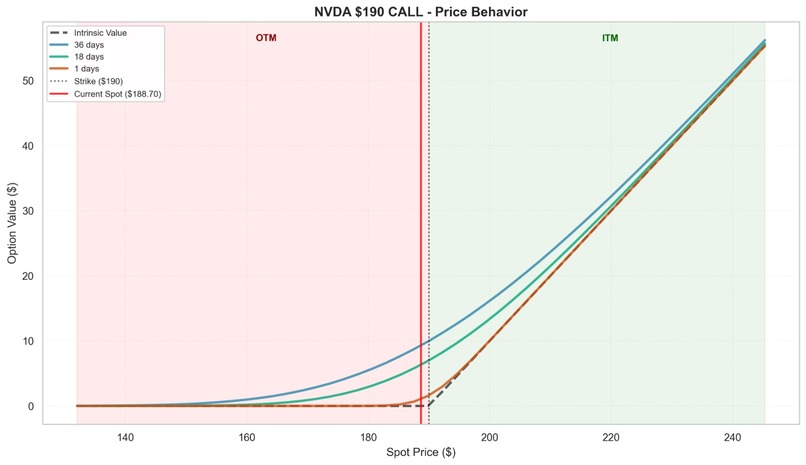

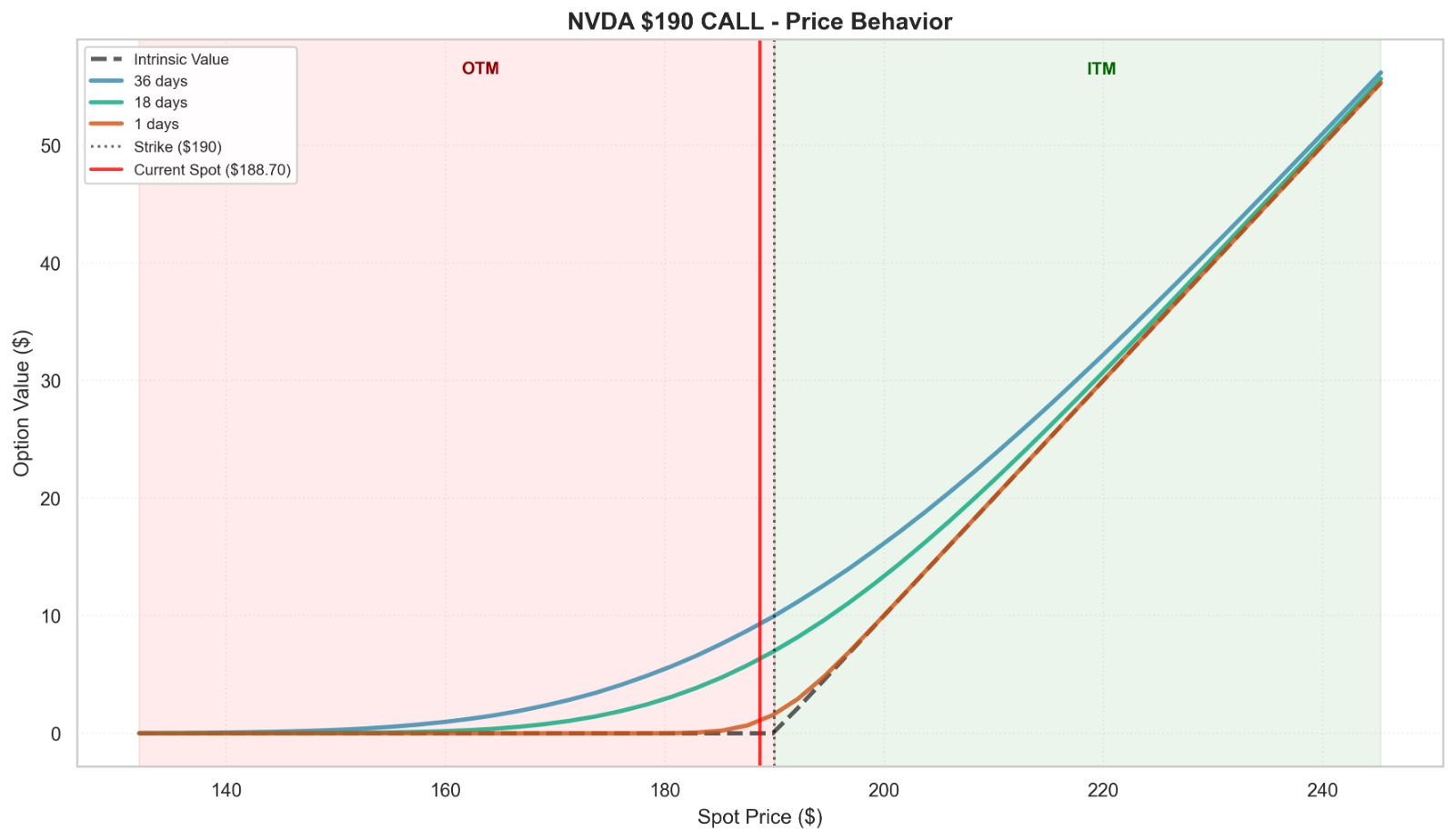

Option price behavior and intrinsic value convergence mapped across moneyness zones.

-

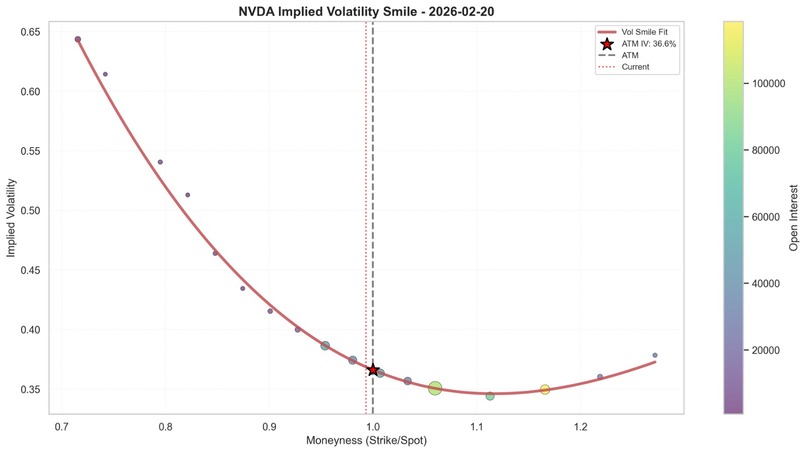

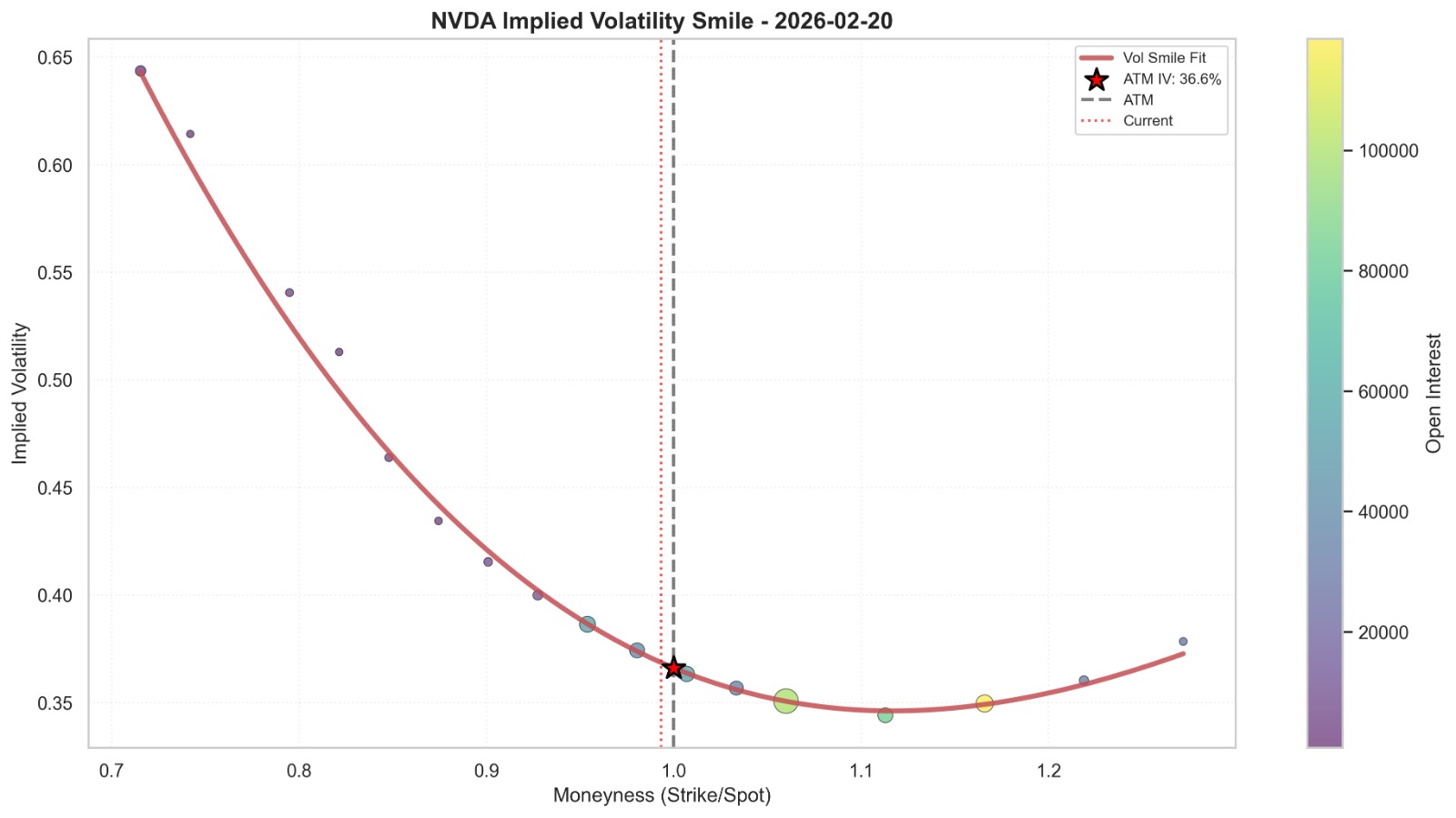

Implied Volatility Smile capturing market-priced tail risk across various strikes.

-

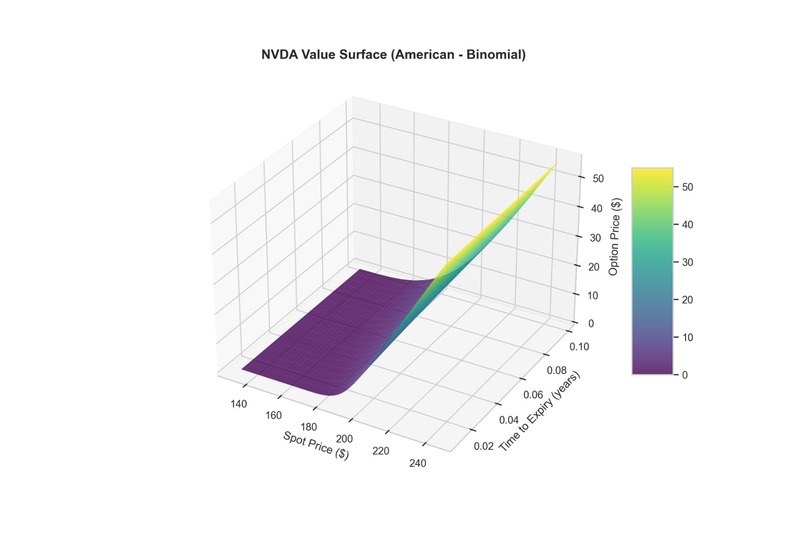

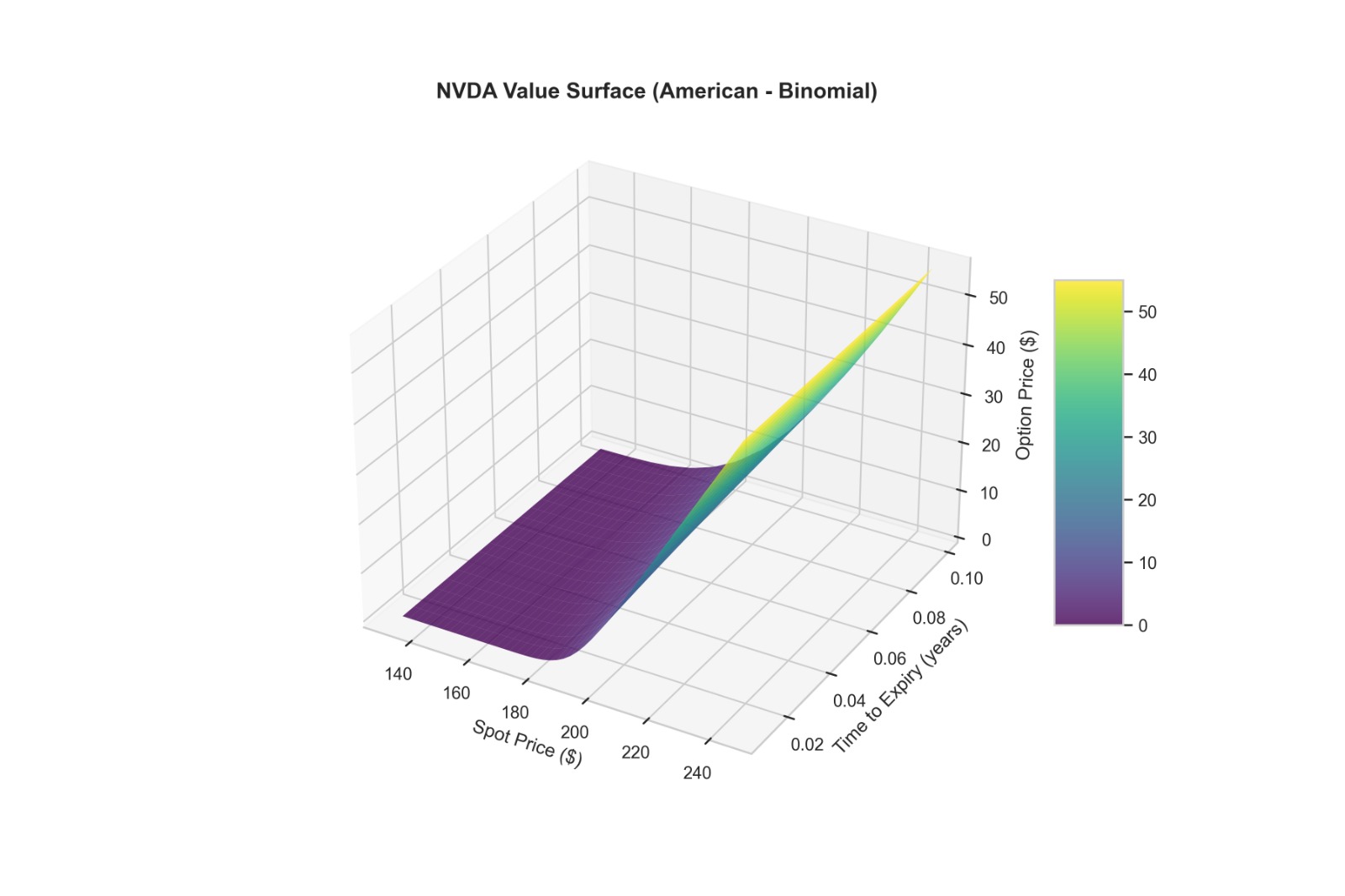

A 3D American Binomial value surface mapping option price against time and spot movements.

-

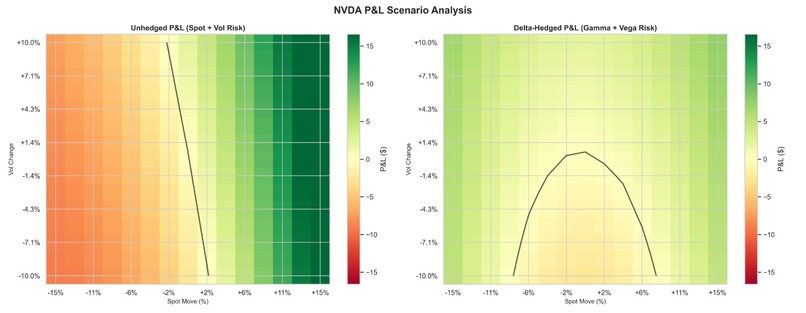

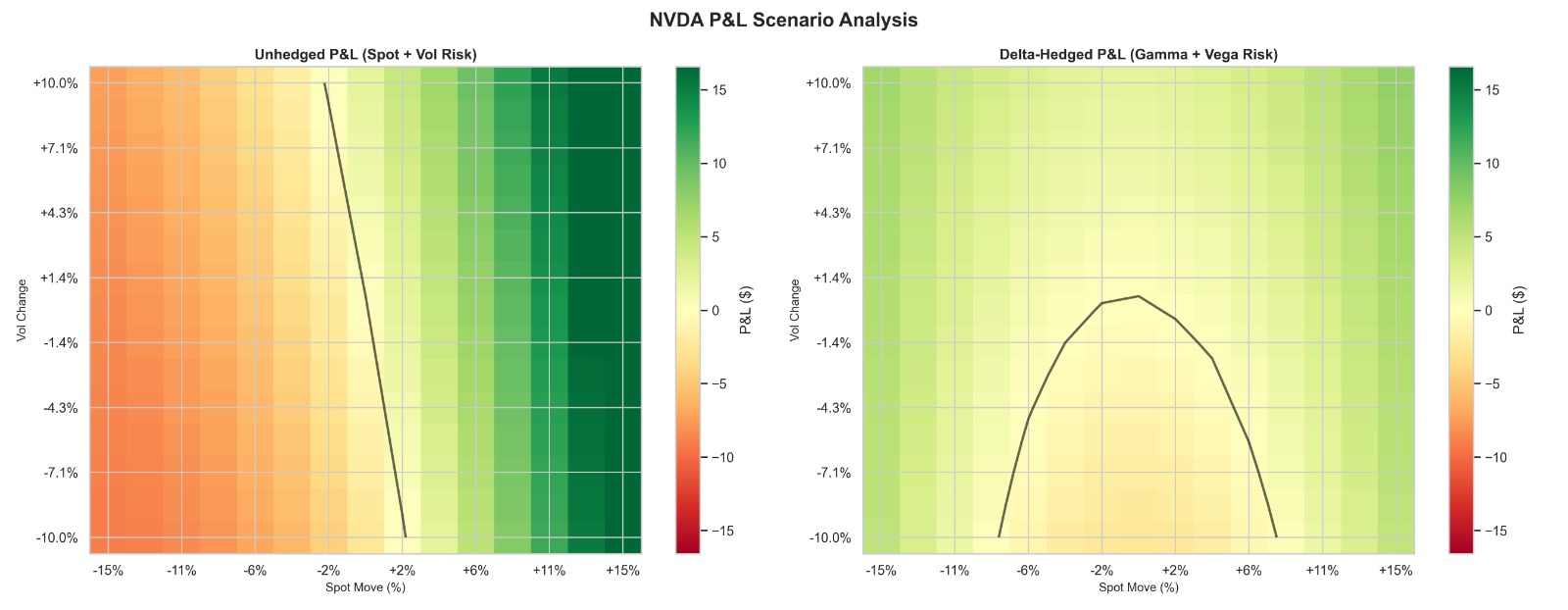

Scenario stress-testing: Unhedged directional risk versus Delta-hedged stability.

-

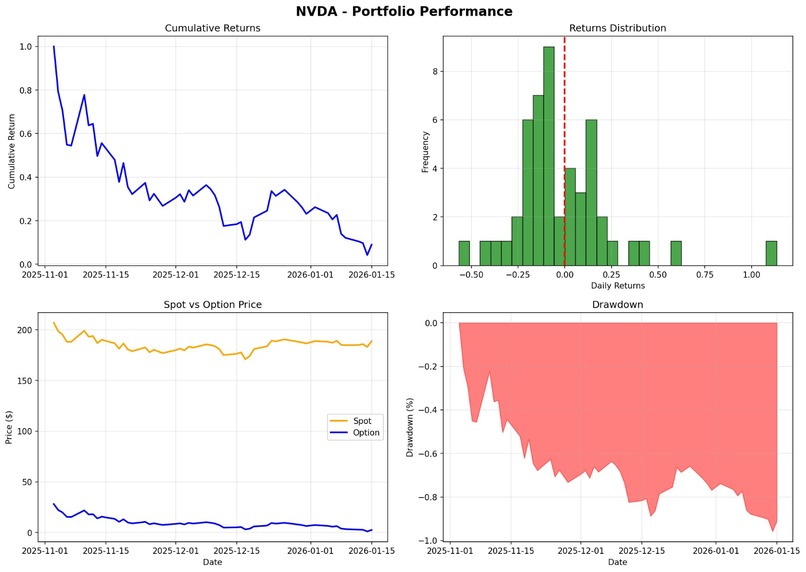

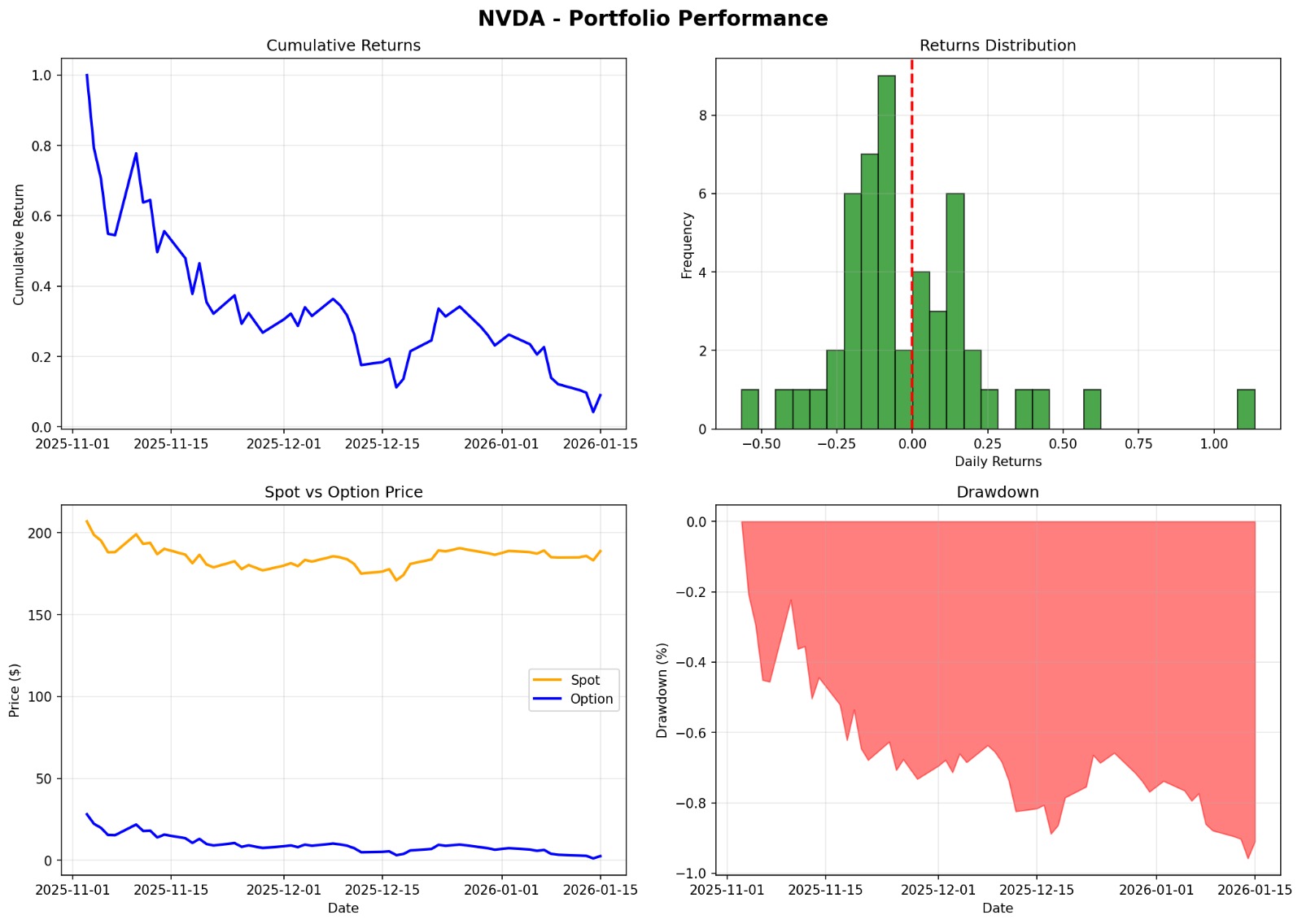

Comprehensive backtest performance tracking cumulative returns and maximum drawdown.

-

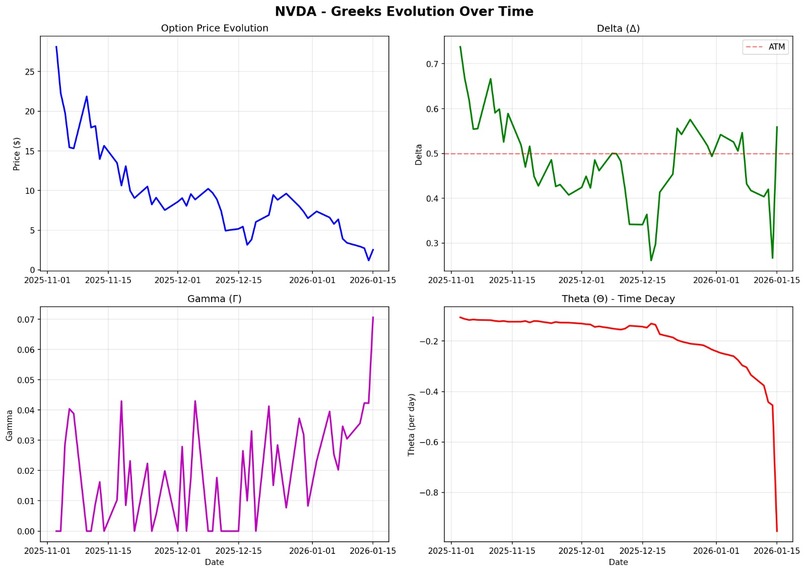

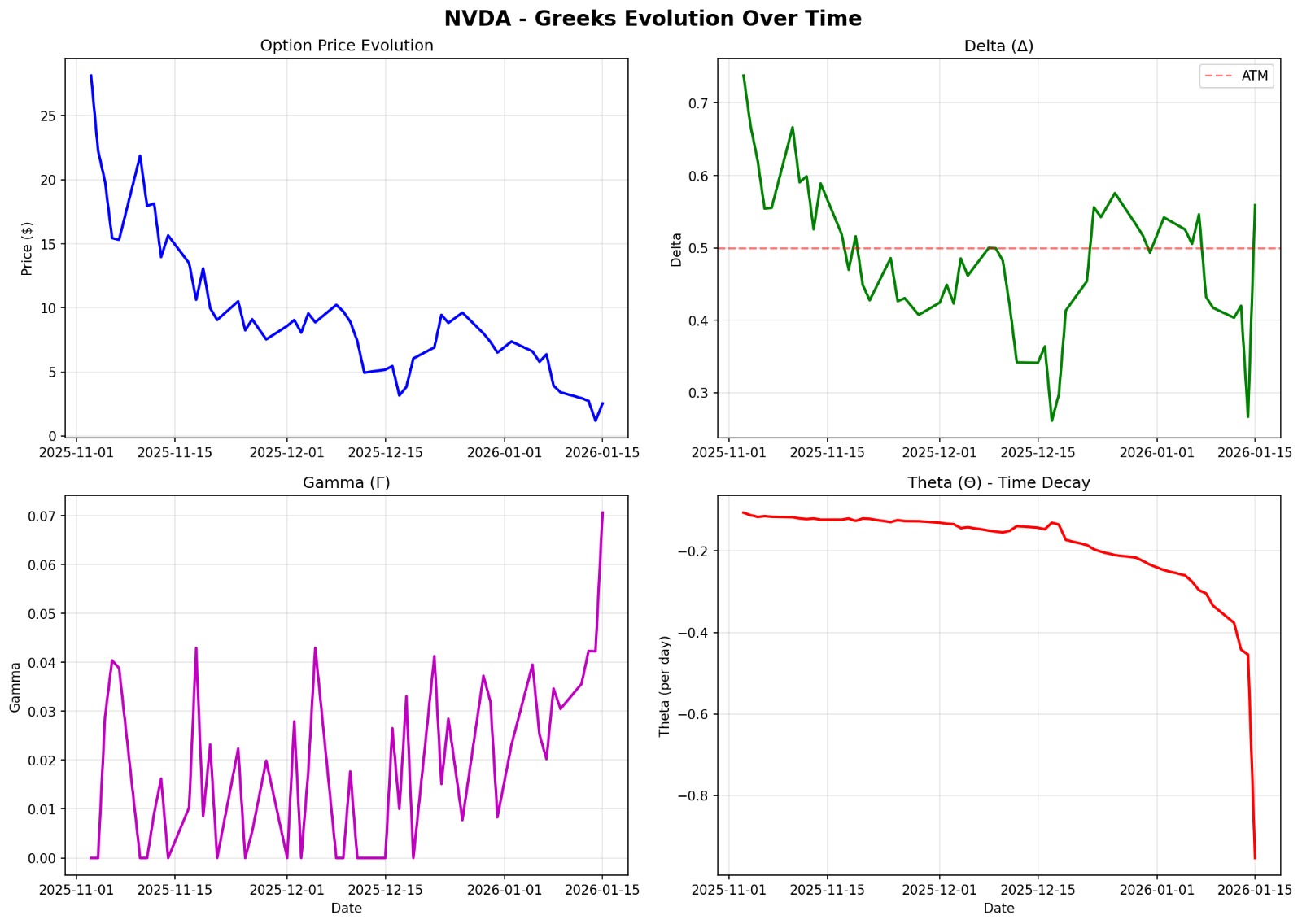

Historical evolution of the option's price, Delta, Gamma, and Theta over time.

-

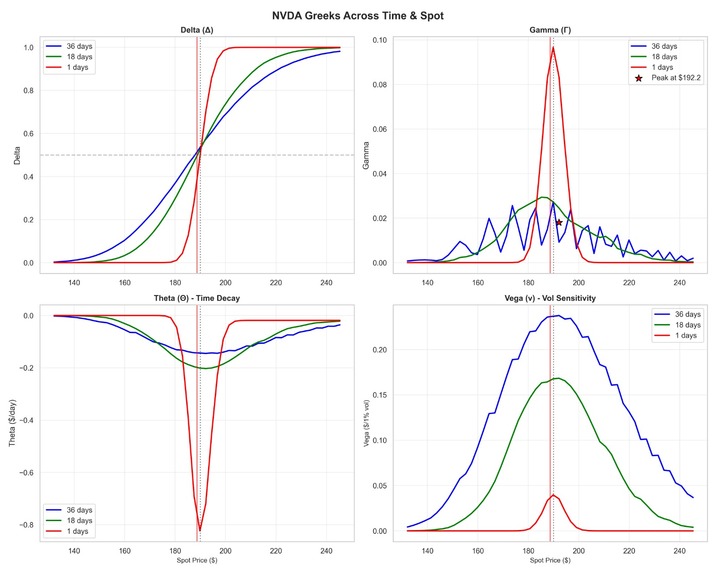

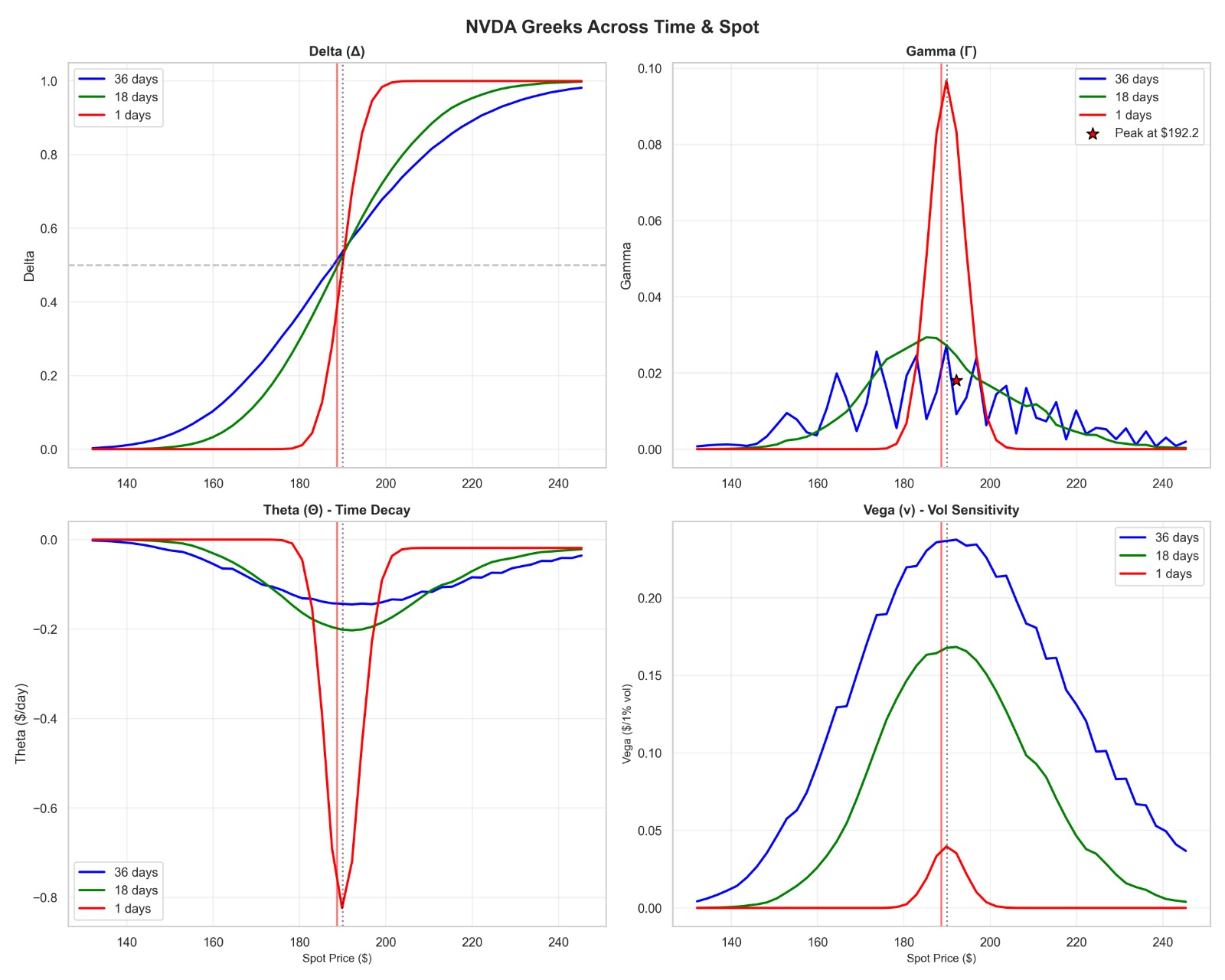

Dynamic multi-maturity modeling of Greeks across varying spot prices.

Inspiration

Quantitative finance has long been a domain reserved for institutional desks and proprietary trading firms — equipped with expensive Bloomberg terminals and black-box pricing engines that retail traders and students rarely get access to. Our team's academic interest in quantitative finance led us to ask a straightforward question: why doesn't a rigorous, open, and accessible options analytics tool exist for everyone?

Options trading is inherently mathematical, yet most retail-facing platforms strip away the very depth that makes informed decision-making possible. We wanted to build something that bridges that gap — a tool grounded in financial theory, powered by modern computing, and usable without a Bloomberg subscription.

What it does

Q-tool is a full-stack Options Pricing & Risk Analysis Engine that brings institutional-grade quantitative analytics to a single, unified terminal interface.

At its core, Q-tool enables:

- American Options Pricing using the Cox-Ross-Rubinstein (CRR) Binomial Tree model, which correctly handles early exercise — something the simpler Black-Scholes framework cannot do

- Greeks Calculation — Delta, Gamma, Theta, and Vega — computed numerically against the Binomial model using finite difference methods

- Volatility Analysis using a blended ensemble of 252-day Historical Volatility and EWMA (RiskMetrics λ=0.94) forecasting, producing an internally consistent "model volatility" for pricing

- IV Rank Signal Generation, classifying the current volatility regime (Low / Mid / High) and generating structured Buy, Sell, or Hold signals based on mispricing between model fair value and market price

- Implied Volatility Smile Visualization, fitting a weighted cubic curve to live option chain data filtered by liquidity (volume, open interest, bid-ask spread)

- Realized Volatility Cone Validation, an institutional-grade technique that flags and replaces suspect market IV values before they contaminate the pricing engine

- Put-Call Parity Checking to verify internal model consistency across calls and puts

- Scenario P&L Heatmaps showing both unhedged and delta-hedged P&L across a grid of spot moves and volatility shifts

- AI-Powered Trade Recommendations via Groq's LLaMA 3.3 70B model, which synthesises pricing signals, Greeks, volatility regime, and fair value analysis into a structured consulting memo in plain language

How we built it

Q-tool was built entirely in Python, with a deliberately lean dependency stack chosen for speed and numerical precision.

- NumPy & SciPy form the mathematical backbone, handling log-return calculations, statistical bounds, and the numerical plumbing underpinning the Greeks

- Numba (JIT compilation) is used to compile the core Binomial Tree pricing function to native machine code via

@jit(nopython=True), making the tree traversal fast enough for real-time interactive use - Pandas & yfinance handle live market data ingestion — spot prices, full option chains, dividend yields, and the 3-month T-bill rate (^IRX) for the risk-free rate

- EWMA (Exponentially Weighted Moving Average) following the RiskMetrics standard (λ=0.94) provides a volatility forecast that weights recent returns more heavily than the simple historical estimate

- Newton-Raphson with bisection fallback is used for implied volatility solving — fast convergence in normal conditions, numerically robust at the boundaries

- Groq API (LLaMA 3.3 70B) powers the AI consulting layer, taking structured trade analytics as input and generating a plain-language investment memo targeted at non-technical portfolio managers

- Matplotlib & Seaborn produce a full suite of professional visualizations: Greeks evolution, value surfaces (3D), IV smile curves, scenario heatmaps, and backtested P&L

- Rich drives the terminal UI — tables, panels, progress indicators — making the tool feel polished despite being a CLI application

Challenges we ran into

The most significant challenge was model accuracy and data quality — specifically, making sure the pricing engine operated on clean, validated inputs rather than noisy market data.

Market-reported implied volatility from option chains is frequently unreliable: stale last-prices on illiquid strikes, zero-volume contracts with meaningless IV values, and data that sits far outside any statistically plausible range. We solved this by implementing a Realized Volatility Cone validation layer — any market IV that falls outside the statistical bounds of recent realized volatility is automatically replaced with the EWMA estimate before it reaches the pricing model.

A second layer of difficulty was numerical stability near expiry and at extreme moneyness. Binomial Greeks computed via finite differences become noisy as time-to-expiry approaches zero or as strikes move deep in- or out-of-the-money. Getting Vega, Theta, and Gamma to behave correctly across the full parameter space required careful step sizing and boundary condition handling.

Accomplishments that we're proud of

Building a fully functional, end-to-end options analytics engine within a hackathon timeframe is what we are most proud of.

Q-tool is not a prototype that prices one option in isolation. It is a cohesive system where live market data flows through a validated volatility layer, feeds a Numba-compiled pricing engine, produces a full Greeks suite, runs scenario analysis, renders professional visualizations, and concludes with an AI-generated consulting memo — all from a single terminal session. Getting every component to work together reliably, on real market data, under time pressure, is a genuine technical achievement.

The IV Rank-based signal generation is also something we feel goes beyond the standard hackathon submission — it reflects how institutional desks actually think about options, distinguishing between regime-driven decisions (sell premium in high-vol environments, buy in low-vol environments) and pure mispricing trades.

What we learned

Building Q-tool deepened our understanding of quantitative finance in ways that academic study alone does not.

Implementing the CRR Binomial Tree from scratch — and then JIT-compiling it — forced a precise understanding of the tree's structure, the risk-neutral probability derivation, and exactly why American options require backward induction rather than a closed-form solution. Computing Greeks numerically through finite differences revealed how sensitive these measures are to step size, and why vega and theta near expiry require special handling.

On the data side, we learned how much of professional quant work is actually data cleaning and validation rather than model building. The RV Cone validation layer was not in the original plan — it emerged as a necessity when we saw how badly raw yfinance IV data behaved on illiquid strikes.

We also learned how to architect a multi-module analytical system with clean interfaces between components, allowing parallel development and reliable integration under a tight deadline.

What's next for Q-tool : Options Pricing & Risk Analysis Engine

Q-tool was built under hackathon constraints, but the vision extends well beyond that.

We intend to evolve it into a fully-fledged quantitative trading platform — one that a serious retail trader or a quant researcher can rely on day-to-day. The roadmap includes:

- A web-based interface, moving from the terminal to a full browser-accessible platform so no local setup is required

- Expanded pricing models — the Heston stochastic volatility model and Finite Difference Methods for more accurate vol surface calibration

- Broker API integration to connect analysis directly to execution within the same platform

- Live portfolio tracking with real-time P&L, aggregated Greeks across positions, and margin monitoring

- Backtesting infrastructure so strategies can be validated against historical data before deployment

- Expanded asset coverage beyond equities into index options, futures, and other derivatives

The goal is a platform where quantitative rigor and practical usability coexist — something that does not currently exist in the open-source ecosystem at this depth.

Log in or sign up for Devpost to join the conversation.