Inspiration

Decentralised Finance (DeFi) has been experiencing significant growth, and Uniswap V3 plays a pivotal role in this ecosystem. The introduction of "Concentrated Liquidity" allows Liquidity Providers (LPs) to set upper and lower price ranges for their liquidity, improving capital market efficiency. However, this innovation introduces impermanent loss challenges, necessitating the exploration of advanced quantitative techniques. Our mission was sparked by the recognition that impermanent loss was limiting the full potential of liquidity providers' investments. This critical issue could not be overlooked, inspiring us to seek and implement a solution.

What it does

Our project addresses the impermanent loss issue by employing a comprehensive strategy. We utilize a hybrid ARIMA-GARCH model to predict future pool prices, estimate impermanent loss in a forward-looking perspective, and optimize LP returns. The strategy involves asset selection, model selection, and a hedging strategy using options on Deribit as well as an innovative LP strategy.

How we built it

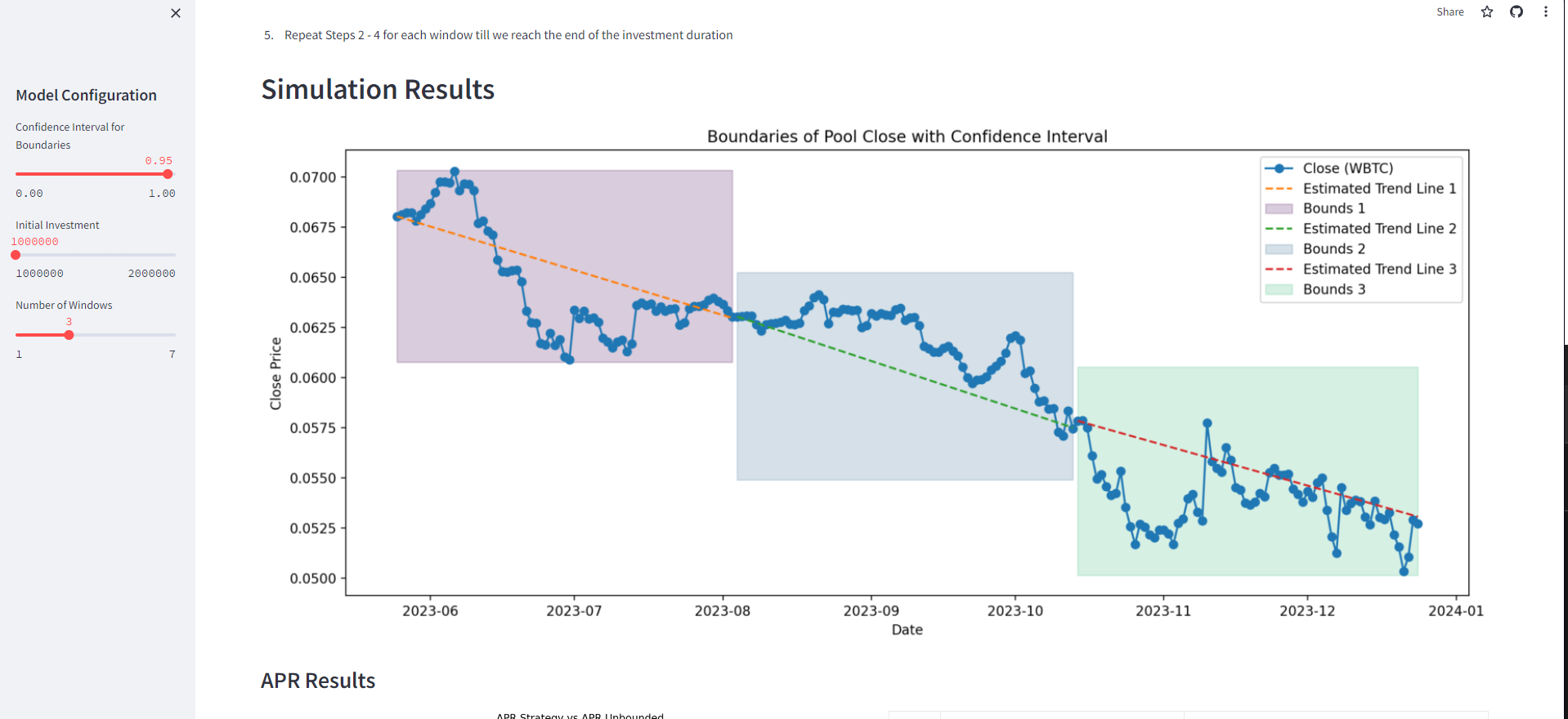

We initiated the project by selecting assets with a high correlation, focusing on the WBTC/ETH token pairing. We then applied a hybrid ARIMA-GARCH model to predict daily Uniswap pool close prices, providing a foundation for estimating impermanent loss. Our hedging strategy involves achieving a gamma-neutral position through long put and call options on Deribit. Using our existing models, we deduced that we can incorporate both our volatility calculations as well as Futures contract pricing to derive a data-driven boundary for LPs to set. This then served as the foundation of our strategy "Hang On Tight", aiming to generate handsome returns for all.

Following Phase 1, we successfully set up our backtesting engine that was able to simulate our LP investment and strategy at the same time. We used Black-Scholes Merton estimation of Historical Option Premiums as well as historical futures data in order to price our premiums and estimate future prices, giving us the tools to set up our "Hold On Tight" strategy

Challenges we ran into

- Balancing impermanent loss mitigation with optimal returns

- Integrating a GARCH model to account for varying volatilities

- Formulation of Strategy

- Creating optimal combinations of call and put options for our strangle hedging strategy

- Initialising Backtesting Engine

Accomplishments that we're proud of

- Successful implementation of a hybrid ARIMA-GARCH model In-depth analysis of impermanent loss and development of a hedging strategy Walk-forward validation of the model with satisfactory performance metrics Formulation of innovative hedging and investment strategy Setting up of Backtesting Engine and Dashboards Performance metrics against benchmark for further analysis

What we learned

-The importance of considering impermanent loss in LP strategies

- Application of advanced quantitative techniques in the DeFi space

- Integration of options for hedging purposes

What's next for Project Whales

Moving forward, we plan to:

- Validate the hedging and investment strategy through historical backtesting

- Further optimize the hedging strategy by fine-tuning options combinations

- Develop an analytics dashboard for risk-level customization and strategy evaluation, similar to Dune Analytics

- Conduct comprehensive simulations and backtesting to refine and enhance the overall strategy

We're invigorated by the potential benefits our project will deliver to liquidity providers and investors, fueling our enthusiasm for the boundless opportunities that lie ahead. This venture is more than a team effort; it's a mission to elevate and prosper the whole DeFi community, paving the way for enhanced benefits and success for everyone involved.

Built With

- coingecko

- graphql

- jupyter

- poolfish

- python

- statsmodels

- tensorflow

Log in or sign up for Devpost to join the conversation.