inspiration most investment apps tell you what to buy. none of them tell you why it makes mathematical sense. we got tired of watching retail investors in india chase tips on telegram and lose money on stocks that looked good on paper but were statistical disasters in disguise. portfolioiq was born from one question: what if a student with 10,000 rupees could think like a quant fund?

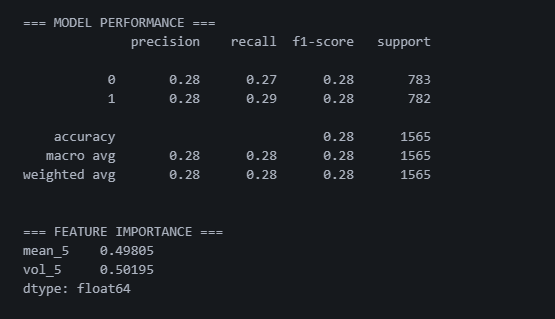

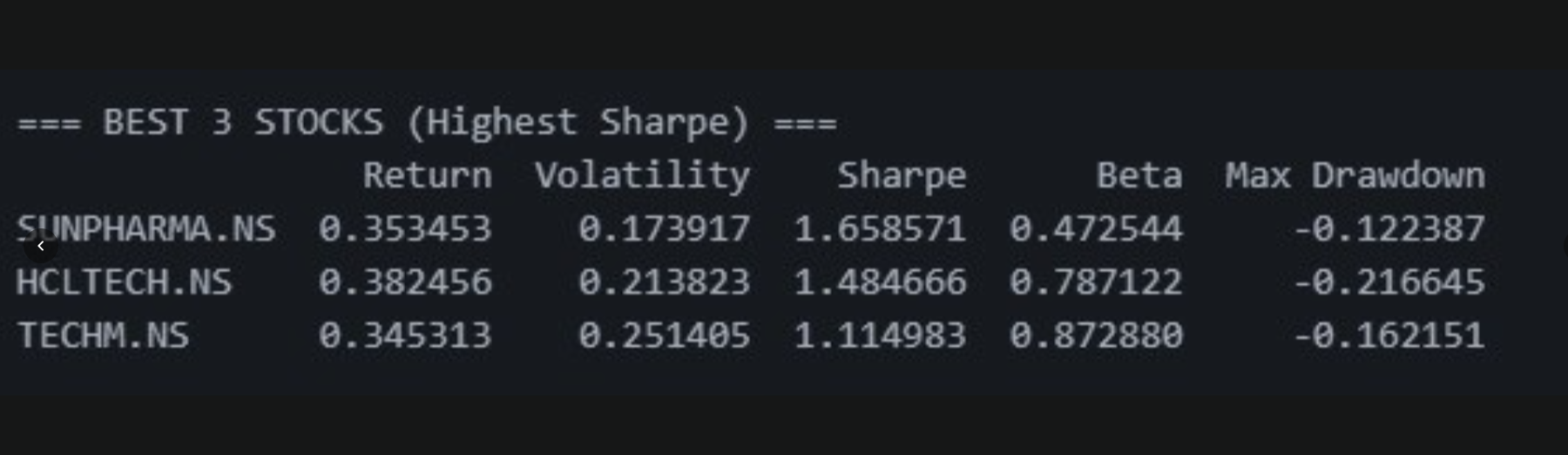

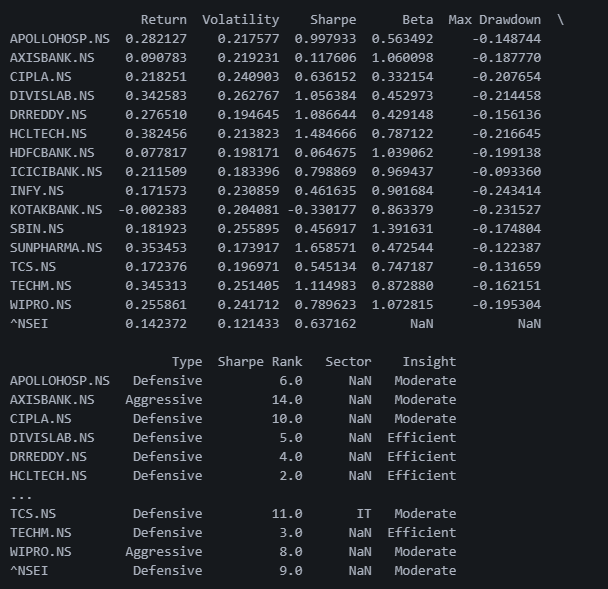

what it does portfolioiq doesn't recommend stocks. it interrogates them. feed it any nse universe and it tears each stock apart - sharpe ratio, beta, max drawdown, sector efficiency - then builds you two portfolios: one honest equal-weight baseline, and one ruthlessly optimized. it shows you exactly which stocks it threw out and why, in plain language. the dashboard doesn't hide behind pretty charts - it makes you confront the math.

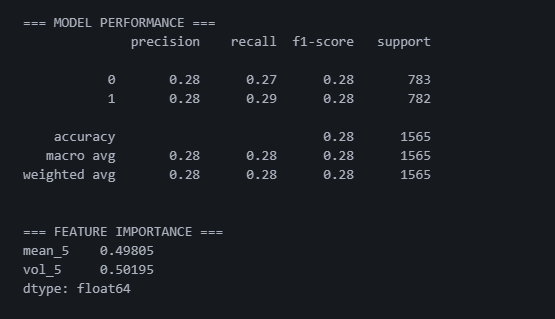

how we built it we didn't reach for a framework first. we started with raw yfinance data and asked: what does a quant actually compute? every metric - sharpe, beta, drawdown - was implemented from first principles in python before we touched any visualization. the frontend was built only after the analytical engine was airtight. data pipeline first, ui second. always.

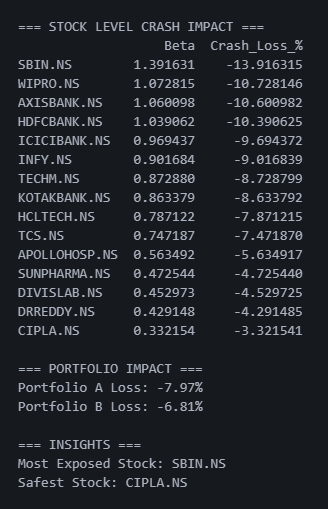

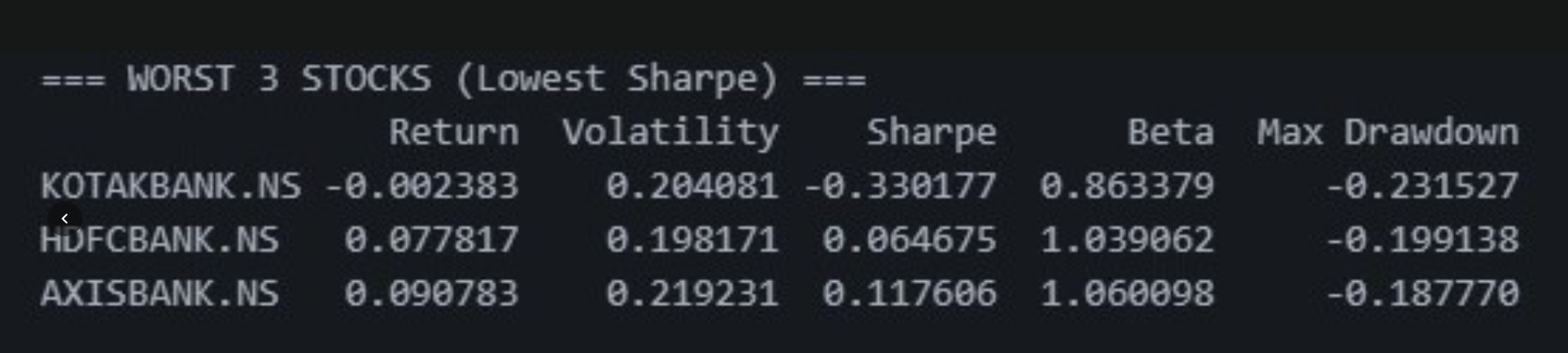

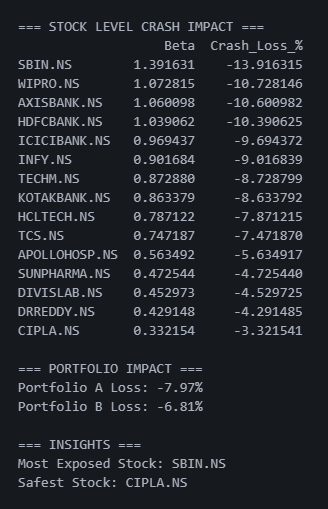

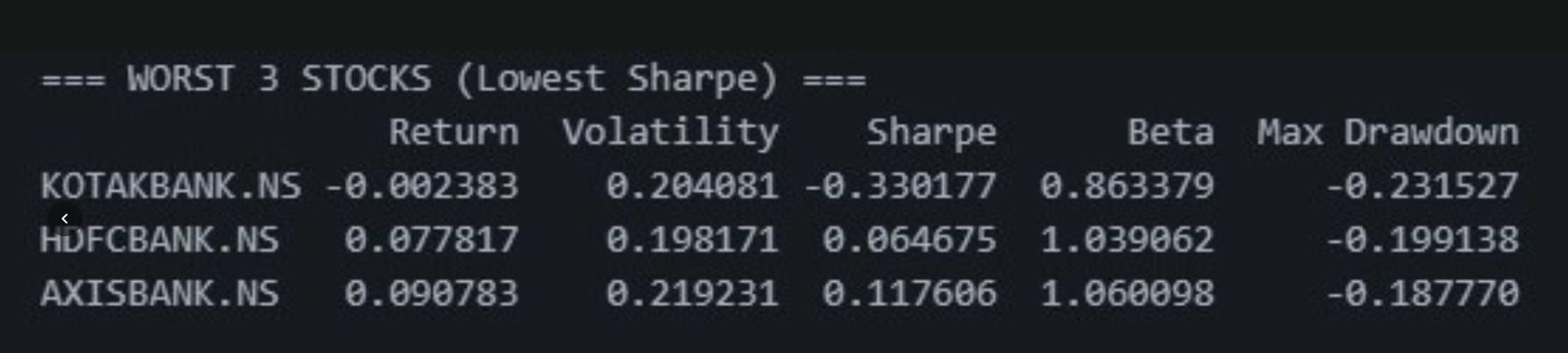

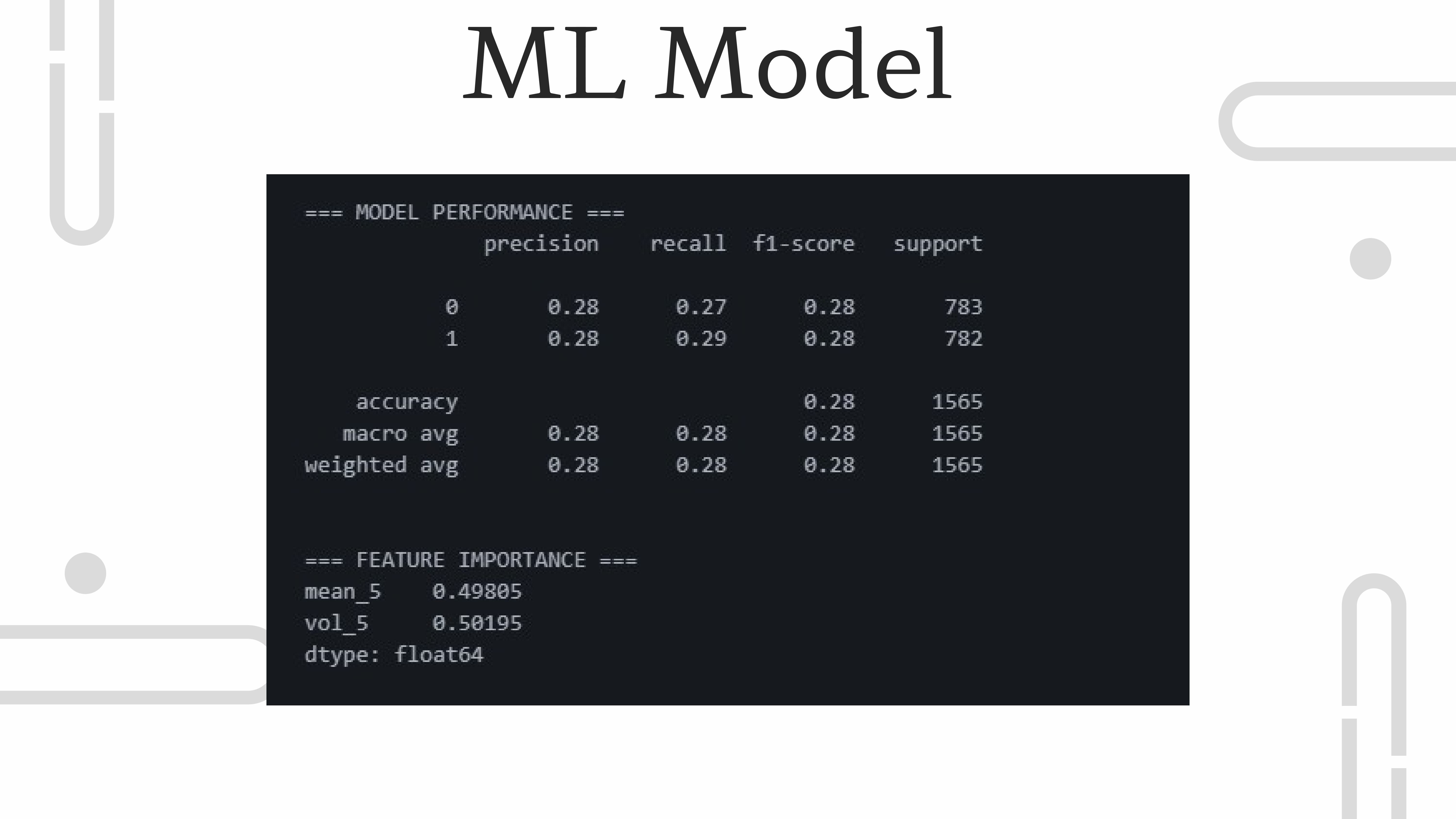

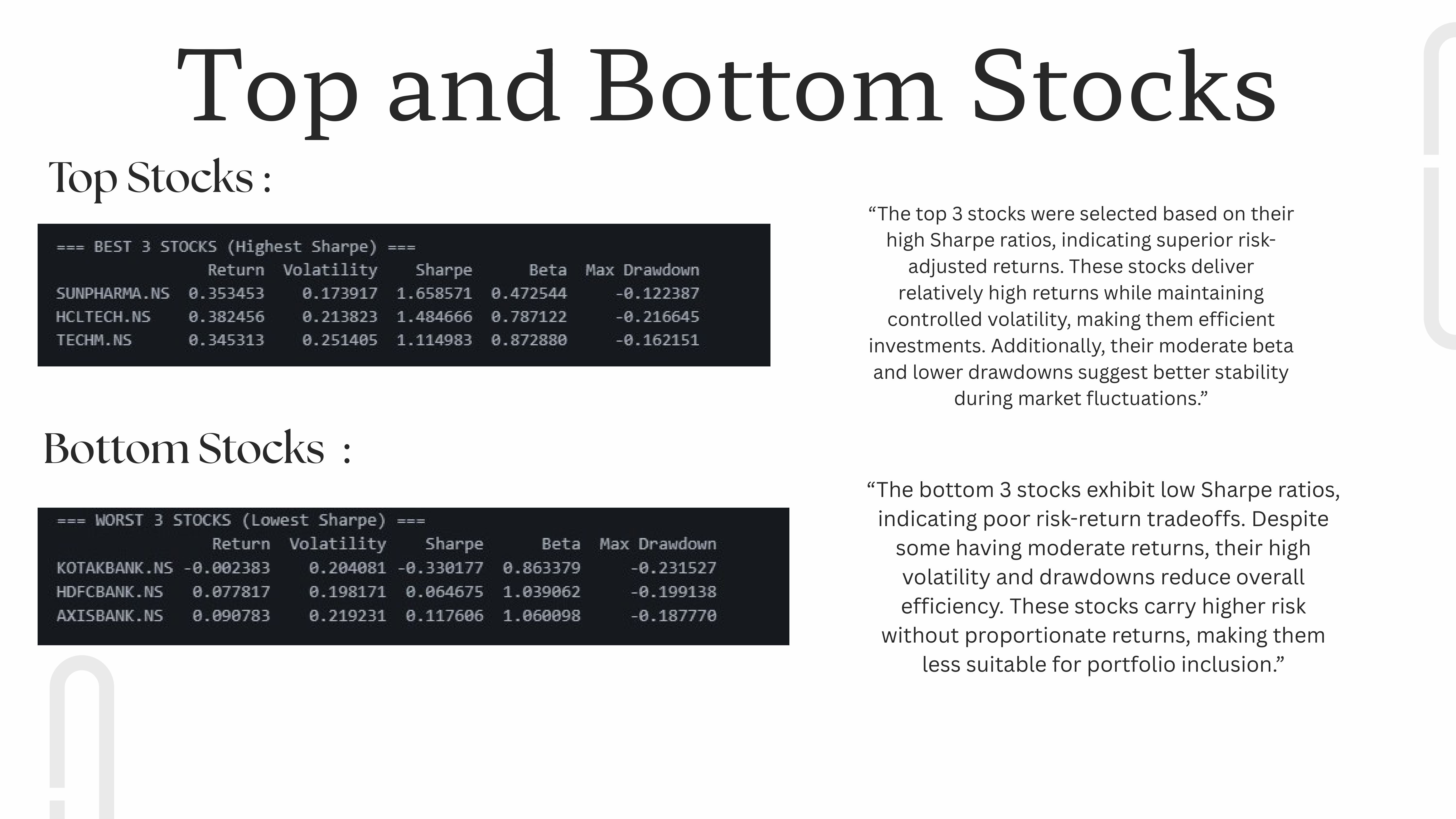

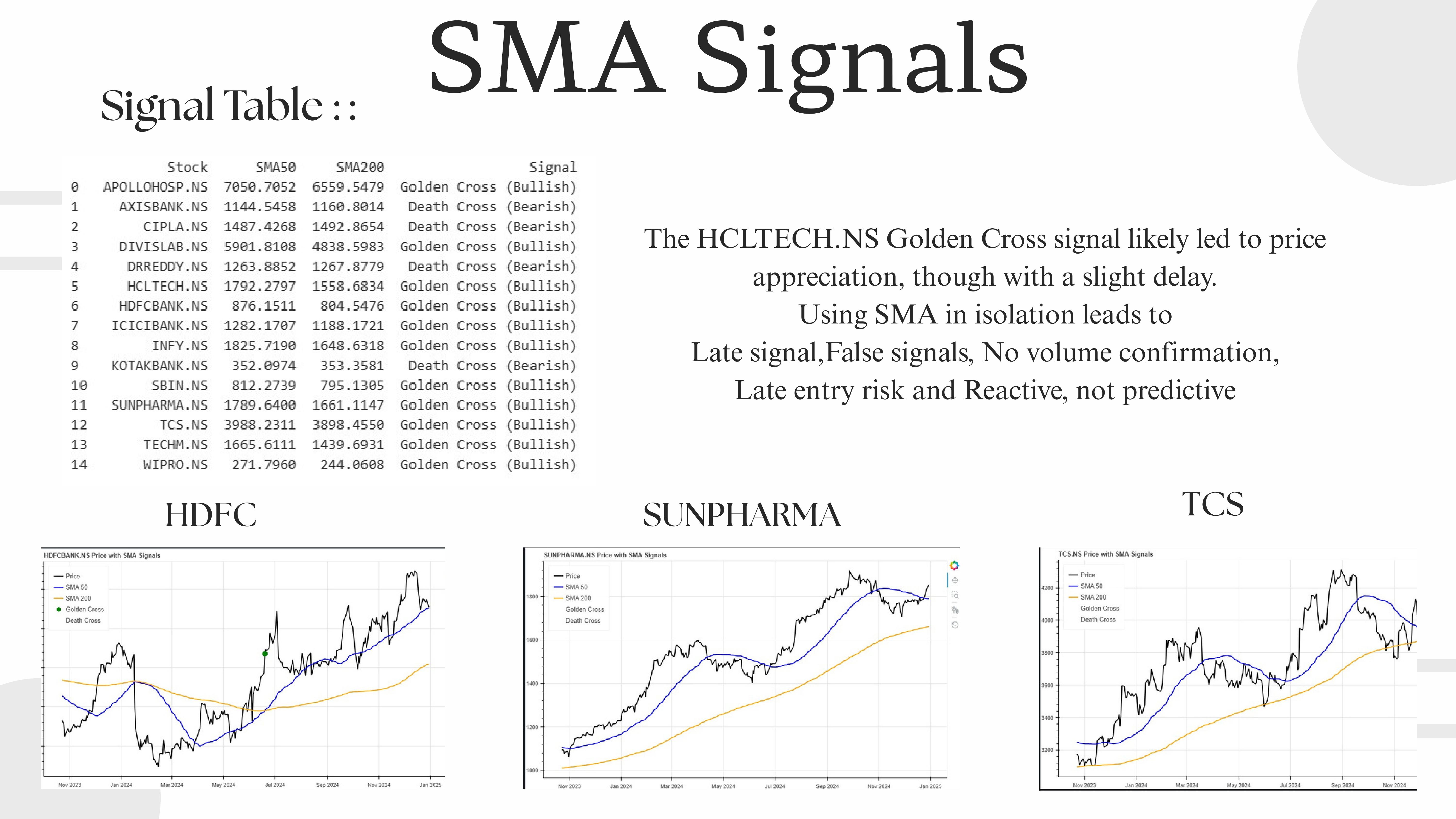

challenges we ran into sector sharpe aggregation broke three times before we realized we were averaging ratios instead of computing them from pooled returns - a subtle but catastrophic mistake. kotakbank taught us that a stock can look visually fine on a price chart while being a statistical corpse underneath. trusting the numbers over the chart was harder than it sounds.

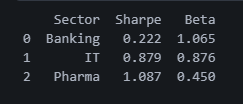

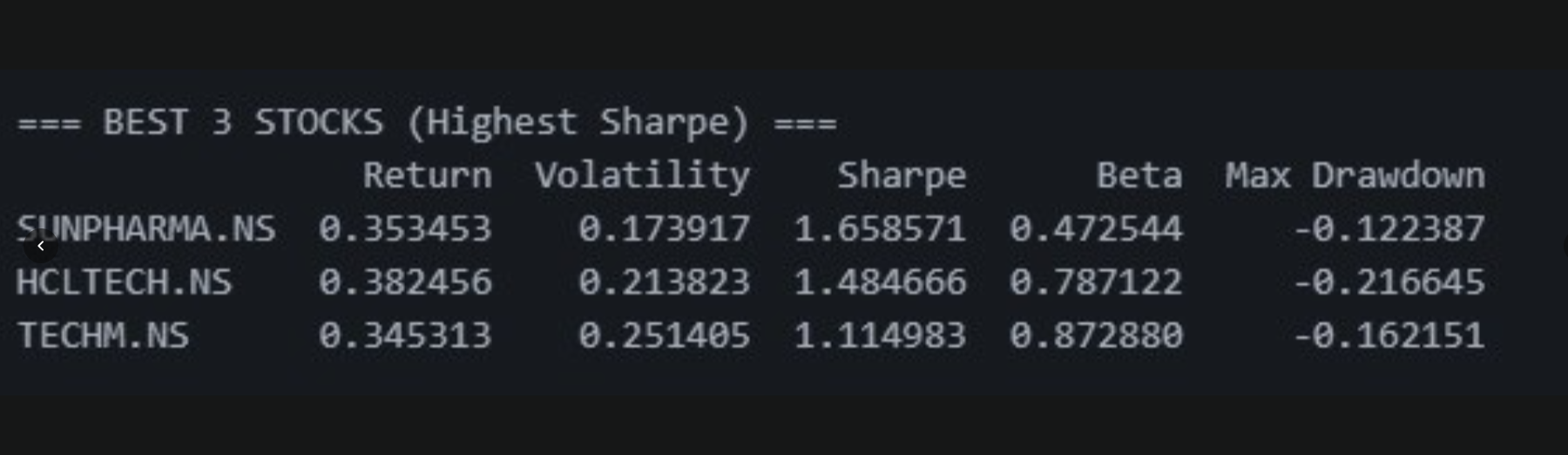

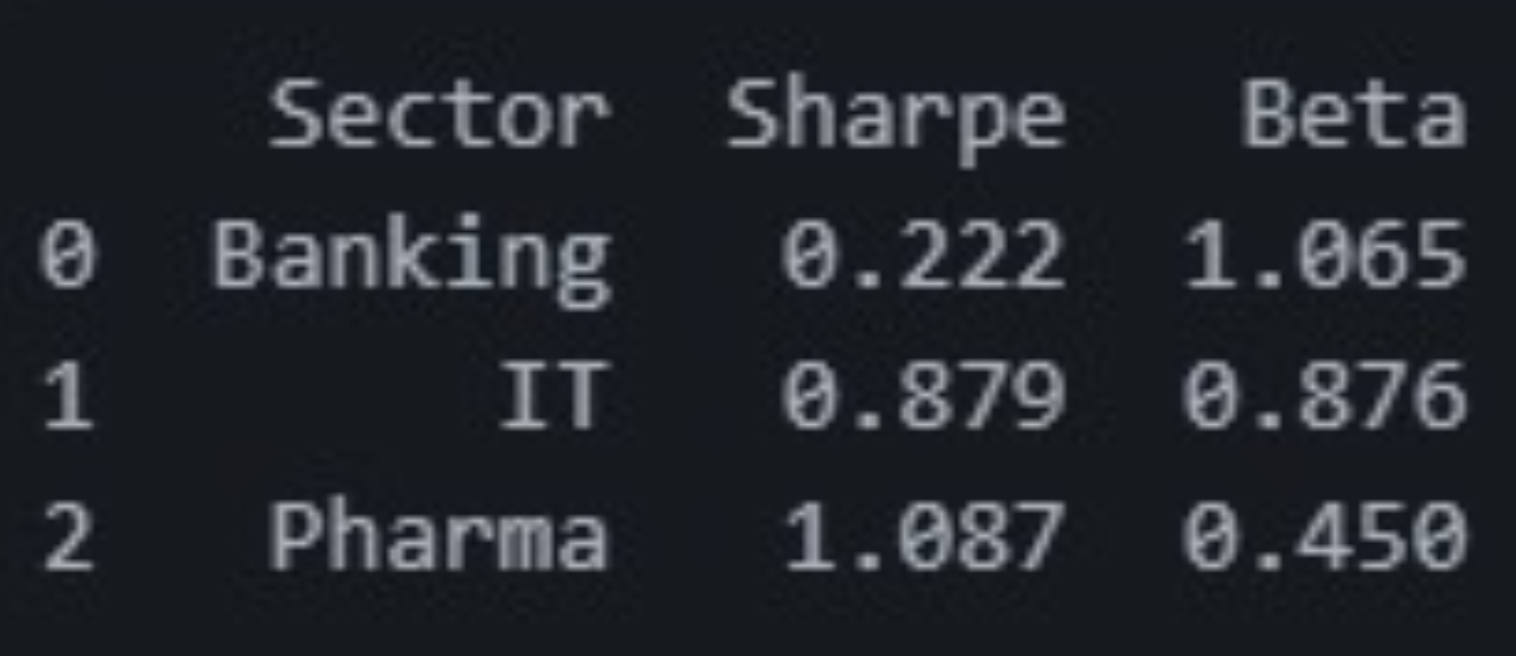

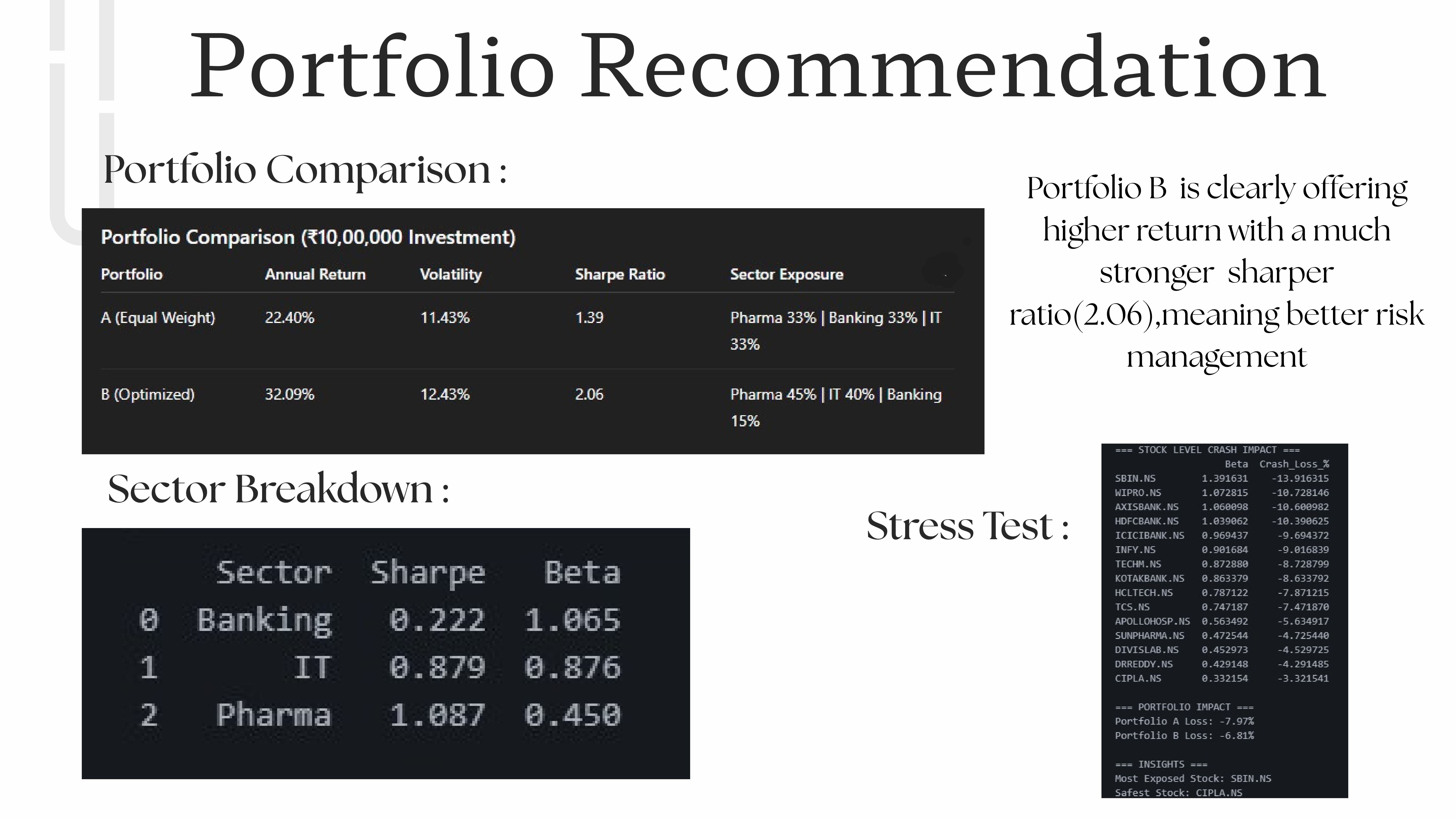

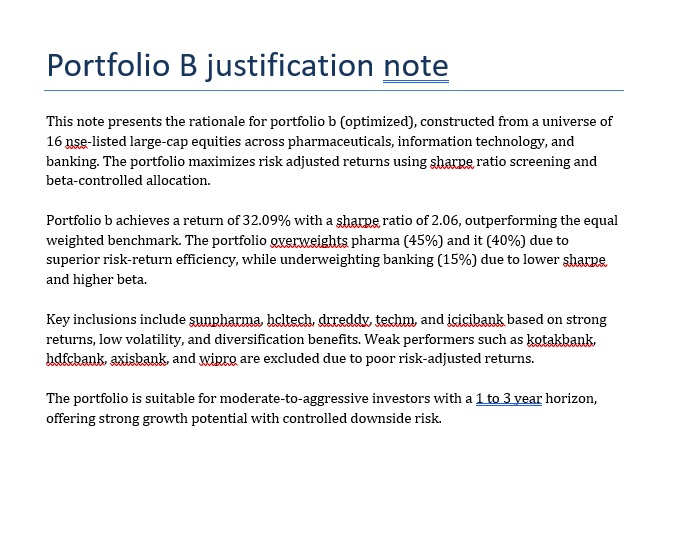

accomplishments that we're proud of portfolio b's sharpe of 2.06 against portfolio a's 1.39 - that gap didn't come from luck. it came from correctly underweighting banking (sector sharpe: 0.222, beta: 1.065) and overloading pharma (sector sharpe: 1.087, beta: 0.450). every allocation percentage has a derivation behind it. we're proud that nothing in this project is arbitrary.

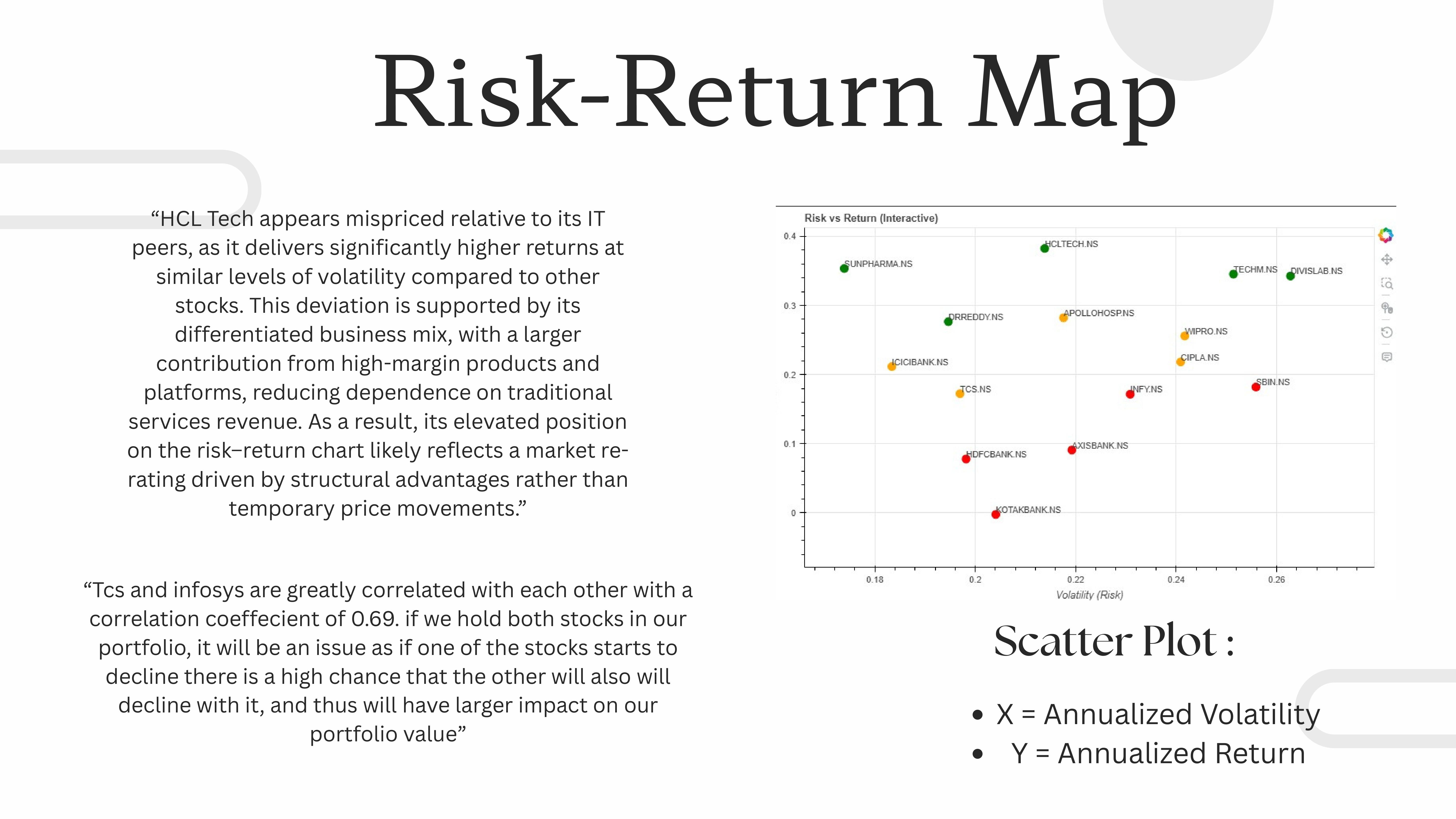

what we learned a negative sharpe ratio isn't just bad performance - it means the stock is actively destroying risk-adjusted value and you'd have been better off in a fixed deposit. kotakbank's -0.33 sharpe was our biggest lesson: regulatory events are quantifiable risk, not just news headlines. we also learned that equal weighting is a form of intellectual laziness disguised as fairness.

what's next for portfolioiq live nse feeds. a rebalancing engine that tells you when a holding's sharpe has decayed below threshold and triggers a swap recommendation. monte carlo simulation for drawdown forecasting. and eventually - a natural language interface where a first-year college student can type "i have 50,000 rupees and i don't want to lose more than 15%" and get a mathematically defensible portfolio back in seconds. the goal was never to build another stock screener. it was to make quant finance accessible without dumbing it down.

Log in or sign up for Devpost to join the conversation.