-

-

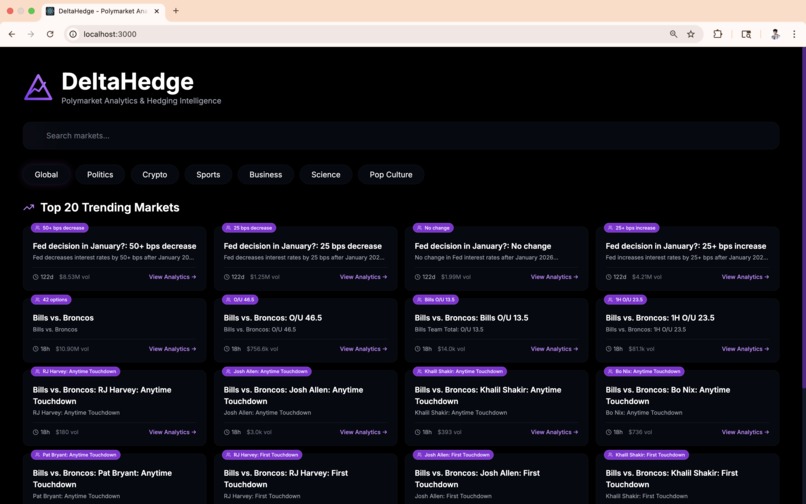

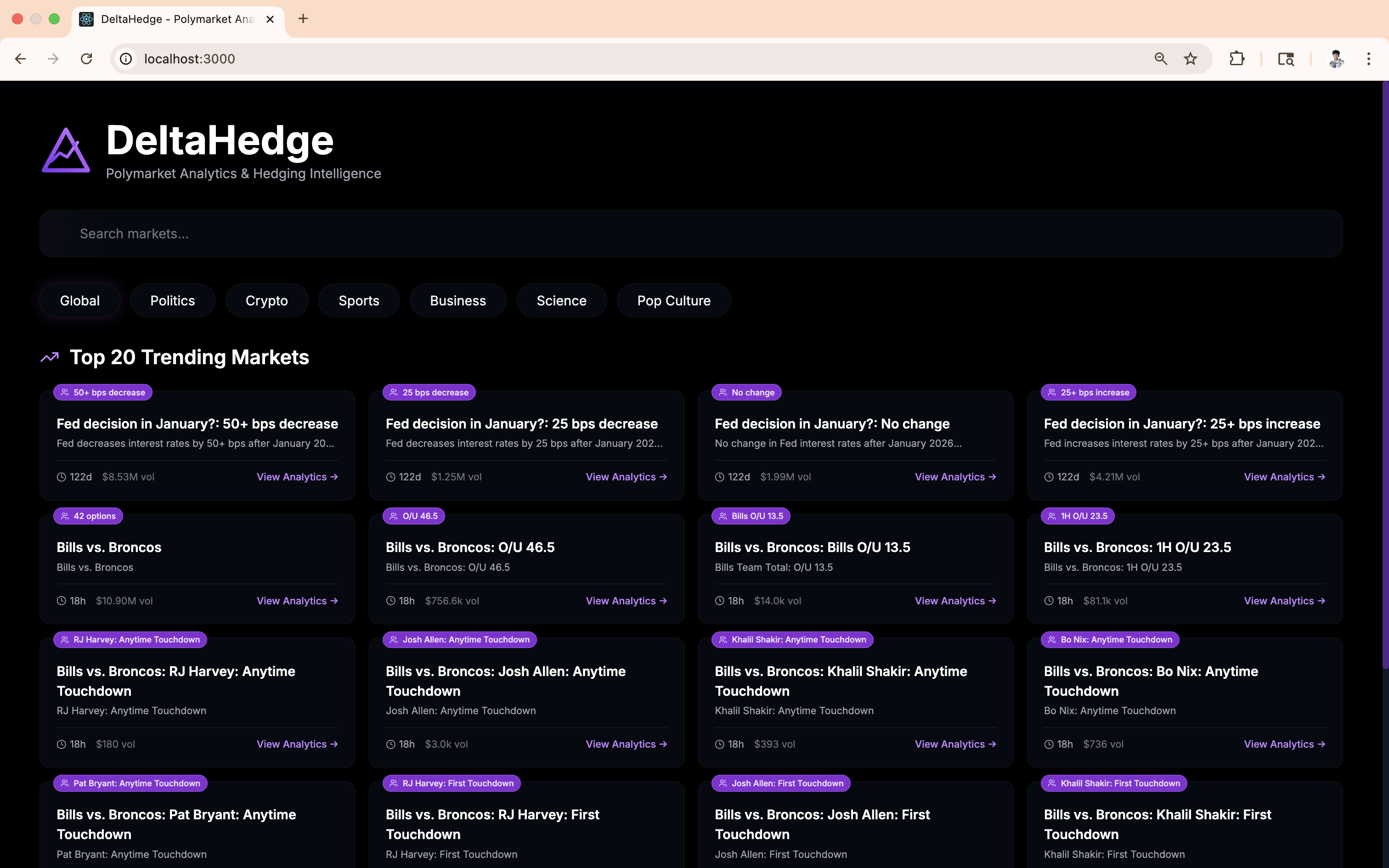

Main Dashboard

-

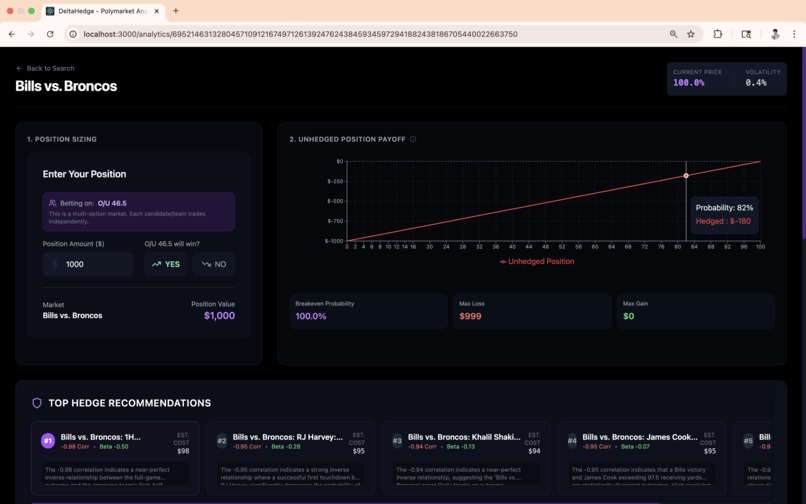

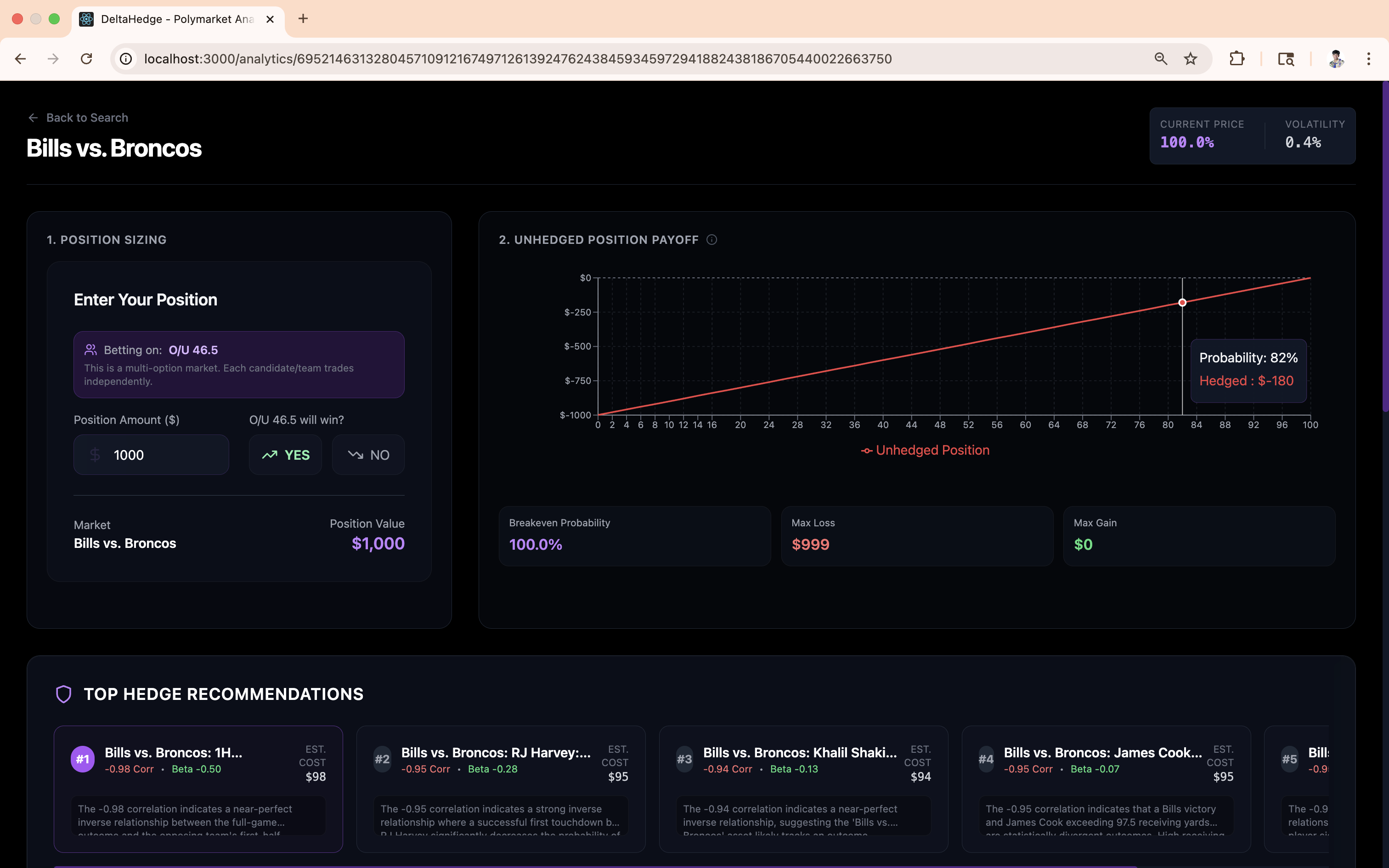

Position Sizing

-

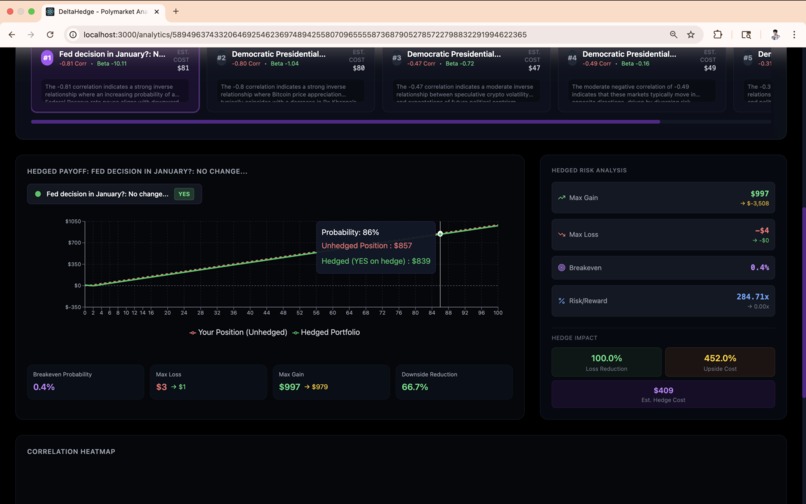

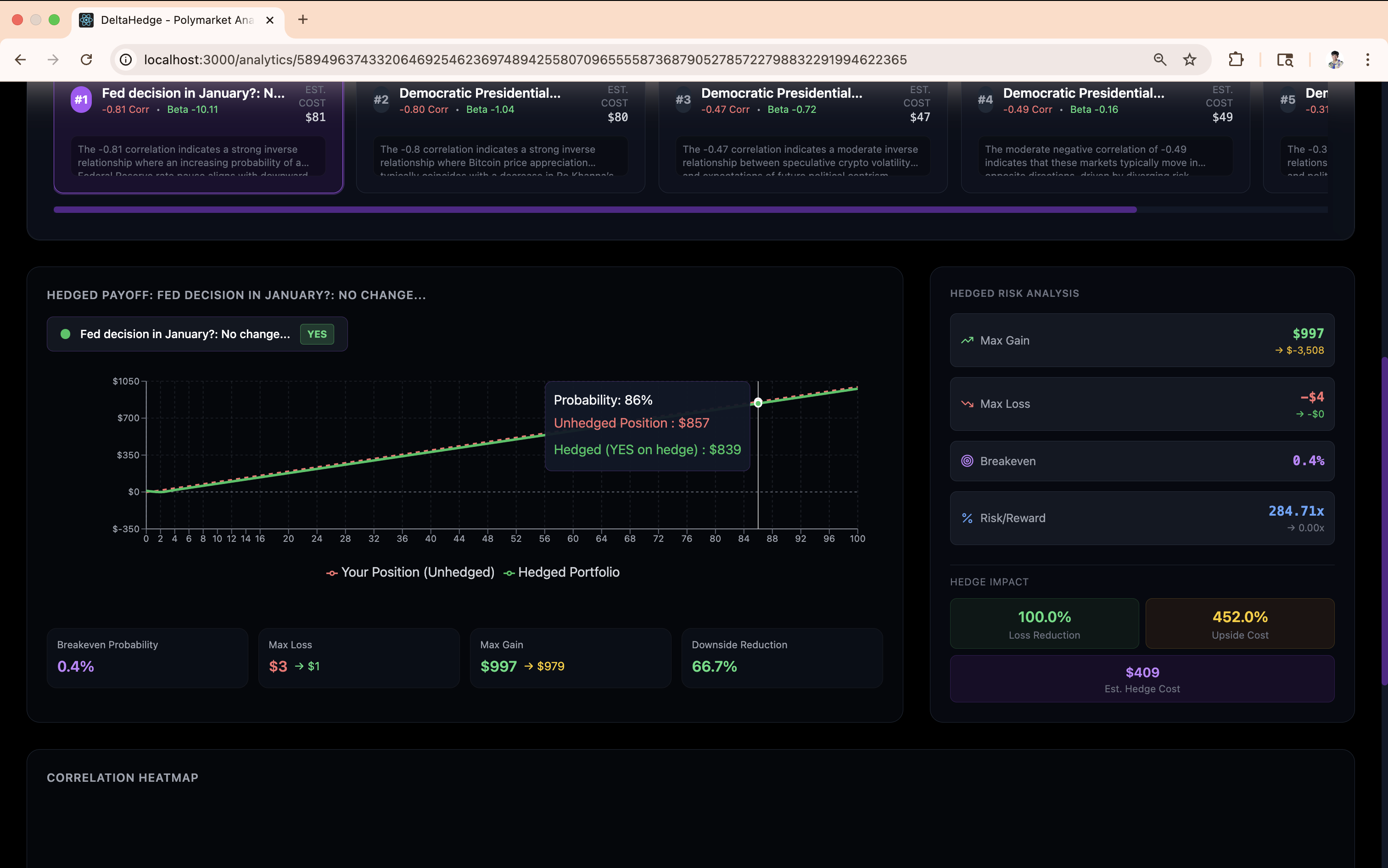

Hedged Payoff

-

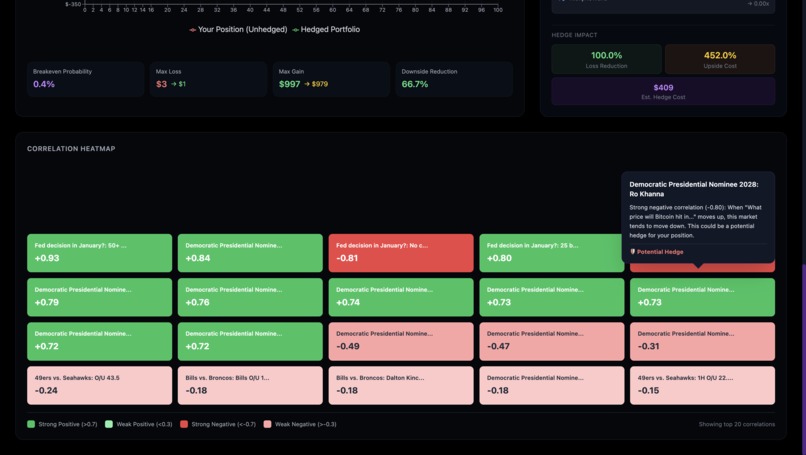

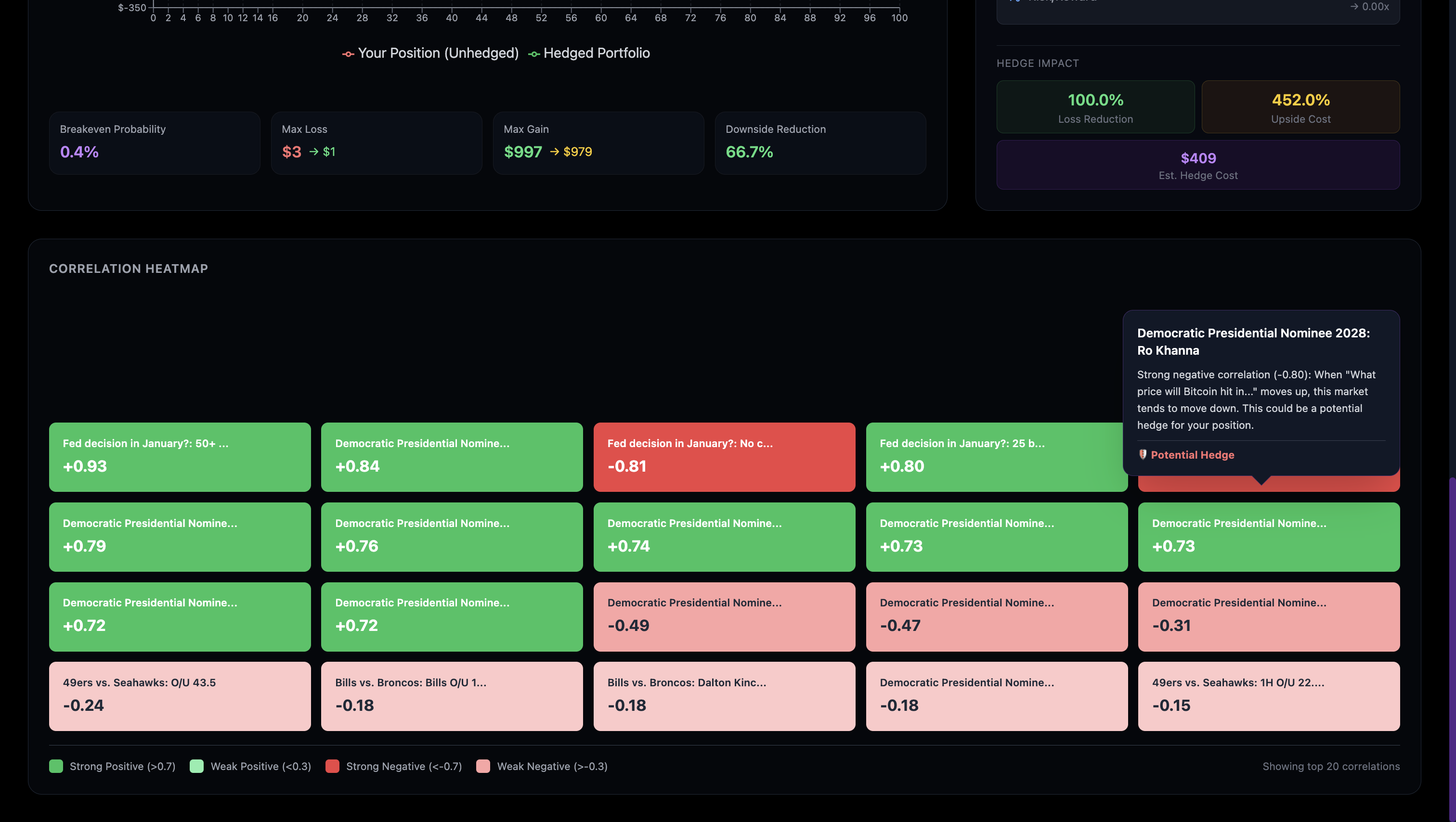

Correlation Matrix

DeltaHedge: Statistical Risk Management for Prediction Markets

Inspiration

Prediction markets like Polymarket have become a primary source for real-time sentiment on global events. However, most retail participants trade these markets in isolation. They fail to realize that a position in a political event may be 90% correlated with a position in a crypto price event, leading to unintentional over-exposure.

We built DeltaHedge to bring institutional-grade risk management tools—typically reserved for equities and derivatives—into decentralized prediction markets. Our goal is to transform prediction betting into professional prediction trading by identifying hidden correlations and providing mathematically backed hedging strategies.

What it does

DeltaHedge is a comprehensive analytical dashboard and API that provides three core layers of intelligence:

Correlation Engine

By analyzing hundreds of hours of historical price data from the Polymarket CLOB, the system identifies which markets move in sync (positive correlation) and which move in opposite directions (negative correlation).Beta-Adjusted Hedging

The platform calculates the exact amount a user should bet on a correlating market to offset their primary risk. This uses a volatility-adjusted Beta calculation to ensure the hedge is proportional to the actual risk.Contextual Alpha Agent

Using Gemini 3 Flash, DeltaHedge provides concise analytical explanations for why correlations exist, helping traders distinguish between statistical noise and macro-driven reality. Gemini Project Number: 952115765461

How we built it

DeltaHedge is built on a Python-based stack designed for high-concurrency data processing:

Backend

We used FastAPI to build a high-performance, asynchronous API that bridges raw on-chain/CLOB market data to the frontend.Data Science

We used Pandas and NumPy for time-series alignment. Because prediction markets are often illiquid, we implemented custom data-cleaning pipelines using forward-filling and back-filling to create continuous price histories for accurate correlation analysis.AI Integration

We integrated Gemini 3 Flash as a virtual trading assistant. To optimize latency and API costs, we used TokenClient to compress prompts before processing, keeping the system fast even when analyzing complex market relationships.Concurrency

We leveraged ThreadPoolExecutor to fetch historical data for 200+ markets in parallel, significantly reducing full-category analysis time.

The Mathematics of DeltaHedge

To determine the optimal hedge, we calculate the Beta ((\beta)) of a potential hedge market relative to a target position.

The Beta is defined as:

[ \beta = \rho_{t,h} \cdot \frac{\sigma_t}{\sigma_h} ]

Where:

- (\rho_{t,h}) is the Pearson correlation coefficient between the target and the hedge

- (\sigma_t) is the standard deviation of returns for the target market

- (\sigma_h) is the standard deviation of returns for the hedge market

The suggested hedge amount is then:

[ \text{Hedge Amount} = -\beta \cdot \text{Position Value} ]

Challenges we ran into

Sparse Data Handling

Unlike the S&P 500, some prediction markets may go hours without a trade. Aligning these gaps into a synchronized data frame was a major hurdle. We solved this via a multi-stage resampling + interpolation strategy.API Rate Limits

Fetching deep historical data for hundreds of tokens can trigger rate limits. We optimized session management and implemented intelligent batching to maintain throughput without being throttled.Correlation vs. Causality

We had to ensure our AI agent did more than repeat statistics. We engineered prompts to force macro-based reasoning (interest rates, election cycles, regulatory news) rather than shallow numeric commentary.

Accomplishments that we are proud of

Real-time Analysis

Reduced a 200-market correlation sweep from 30+ seconds to under 5 seconds via parallelization.Math-Driven Insights

Implemented a Beta-weighting system that works with the unique 0-to-1 price structure of prediction market tokens.Seamless AI Logic

Added prompt compression through TokenClient to maintain analytical quality while reducing token usage by ~20%.

What we learned

- We gained a deep understanding of the Polymarket CLOB (Central Limit Order Book) architecture and how to extract meaningful price signals from raw JSON responses.

- We learned that in prediction markets, negative correlation is often the most valuable tool, because it provides one of the only real ways to mitigate risk in binary-outcome exposure.

- We saw how Gemini 3 Flash can interpret statistical outliers and turn them into human-readable trading narratives.

What's next for DeltaHedge

Cross-Chain Hedging

Expand correlation discovery beyond Polymarket into on-chain options protocols like Lyra or Derive.Portfolio Health Score

Let users connect a wallet and receive a “Diversification Score” based on net correlations across their full portfolio.Automated Execution

Build a smart contract vault that automatically rebalances hedges as correlations shift in real time.

Gemini Project Number: 952115765461

Built With

- apache-echarts

- apis

- docker

- gemini

- javascript

- next.js-(react)

- numpy

- pandas

- polymarket

- tailwind-css

- thetokencompany

- typescript

- uvicorn

Log in or sign up for Devpost to join the conversation.