-

-

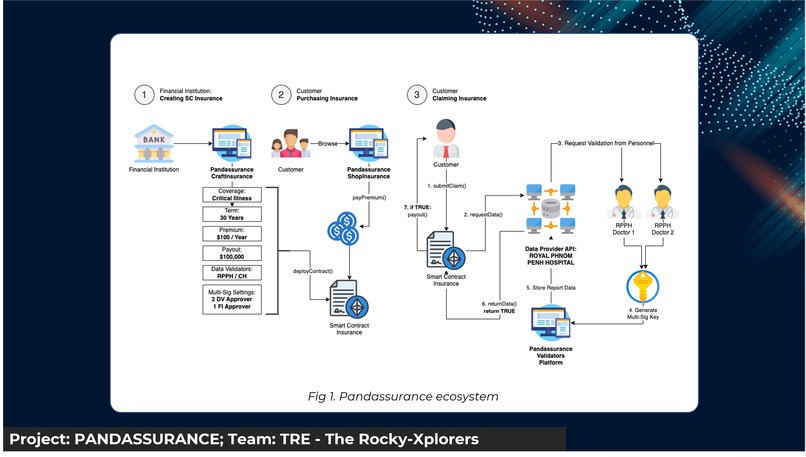

Fig 1. Pandassurance ecosystem

-

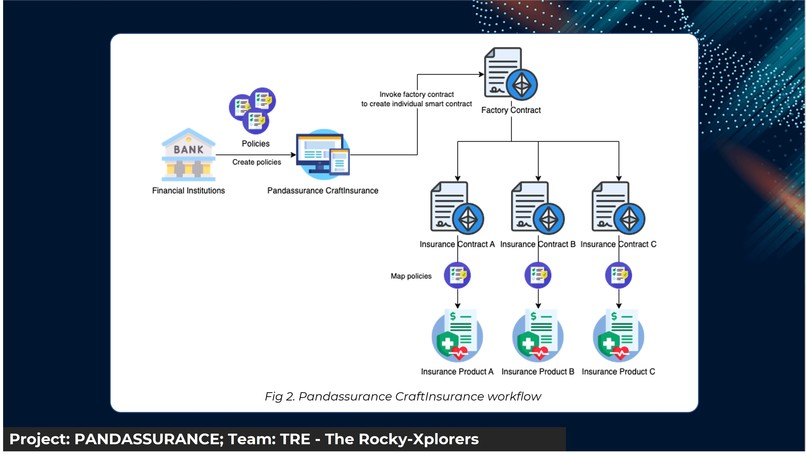

Fig 2. Pandassurance CraftInsurance

-

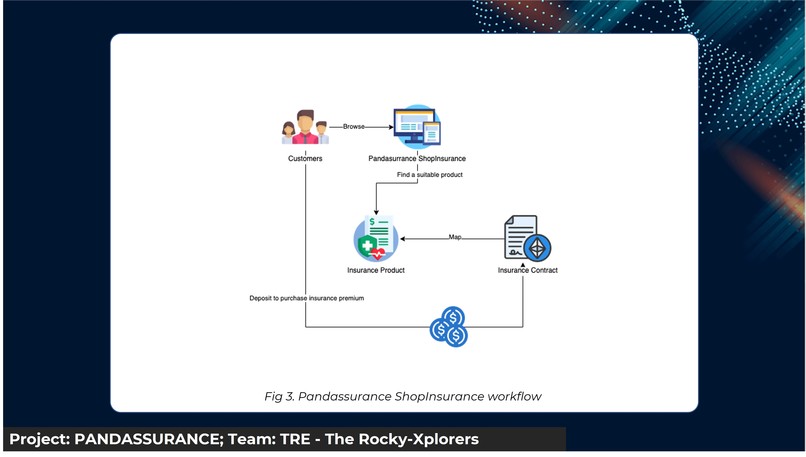

Fig 3. Pandassurance ShopInsurance

-

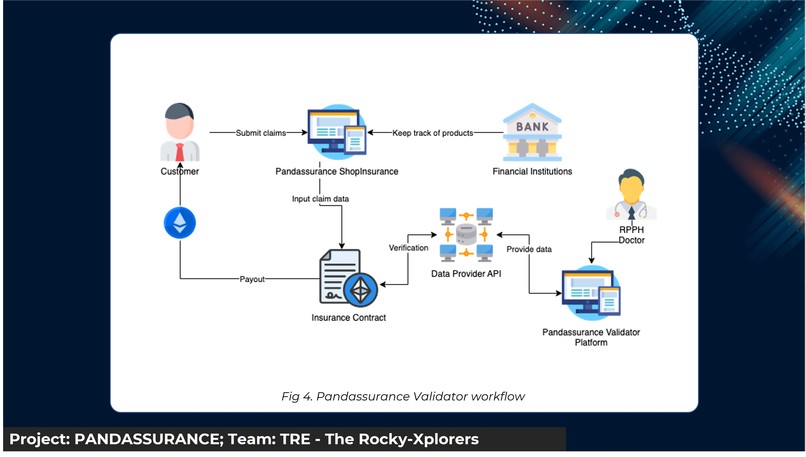

Fig 4. Pandassurance Validator Platform

-

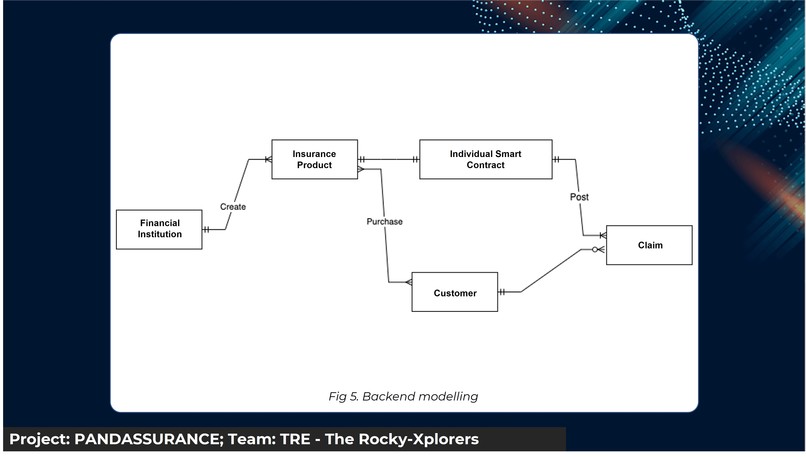

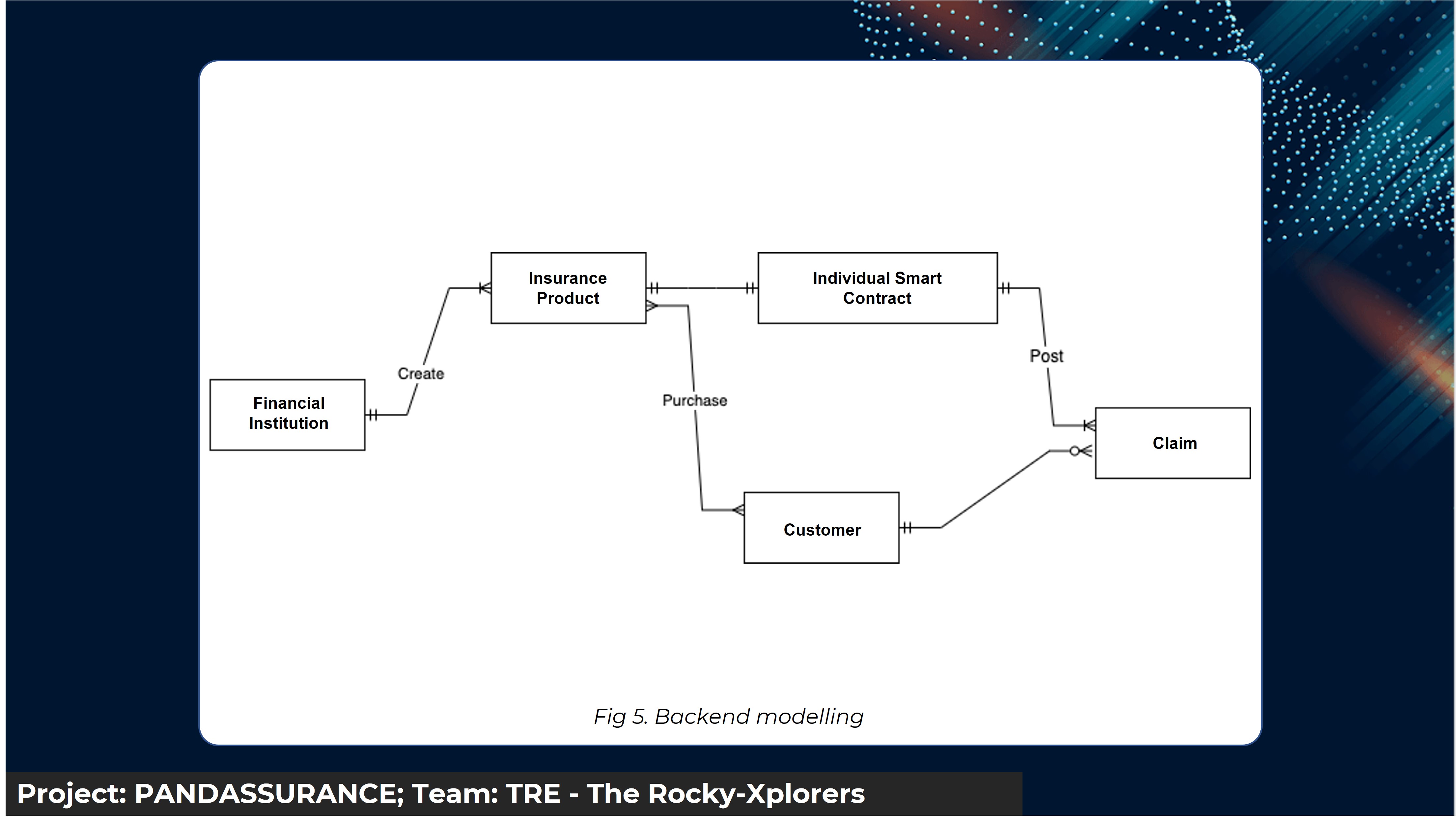

Fig 5. Backend Modelling

Inspiration

The insurance industry generates multi-trillions in annual revenue however it faces numerous challenges, including increasing costs and deterioration of trust in customers. In less developed countries, these challenges are multiplied with consumers lacking credit history and fears of fraud, which accounts for Cambodia’s Insurance Industry being only 1% of the country's GDP (lagging significantly behind the global average of 9.5%). Hence by leveraging on Blockchain’s potential of driving efficiency and increasing transparency, we hope we could tap on this available market potential to create new insurance processes and a business model that is built on the blockchain to address multiple pain points: manual claims review and processing, use of middleman complex assessment, and fragmented data sources.

Insurance is a business structure that requires the coordination and cooperation of many different intermediaries with varying incentives. Naturally, in such a structure, it would require the trust of different parties, from the provider to the insured to the authenticators of the claims. By incorporating blockchain smart contracts, we hope to automate claim submission, allow a more efficient exchange of information, remove middlemen, and reduce overall administrative costs. With this, we hope to enhance customer experience and establish a reliable system.

Goals

Our goal is to

- explore the use case of blockchain and the integration of smart contracts in the area of insurance

- gain a deeper understanding of how the insurance industry can adopt blockchain and smart contracts to streamline their operations and systems, reduce costs, and manage risk

- improve customer experience

Solution

Our solution is to enable any financial institution to quickly design and deploy insurance products. Smart contracts would be the underlying technology that enables us to build a more trust-less insurance ecosystem. In our example, we would like to demonstrate how smart contract insurance is made possible for policies covering critical illnesses.

Fig 1. Pandassurance ecosystem

Sample workflow

The function of our platform will require three key stakeholders: Financial Institutions, Data Providers and Clients

Here is a sample workflow of a critical illness insurance product:

- Financial Institutions set up their insurance products in a smart contract on the insurance creator platform.

- Clients browse the available insurance products which are displayed in the form of an insurance catalogue.

- When the client submits a claim, our data-providing partners (hospitals) will validate the claims.

- Upon confirmation of all necessary conditions, the smart contract is triggered and the payout is distributed to the insured.

Platforms

We have three platforms that support our solution.

Pandassurance CraftInsurance

This platform is used by financial institutions to create their insurance policy. This is also where they will configure and design the insurance policy to a varying number of multi-signature requirements and conditions for triggering the payout.

Here is the user flow for a financial institution creating a policy for critical illness:

- Financial Institutions are given the flexibility to create their customised insurance products, simply by indicating policies and pricing plans.

- These details will then be encoded into smart contracts that will be deployed on the Ethereum blockchain. The smart contracts will aid in the automation of reconciliation and claim processing.

- When clients submit their claims for their purchased insurance, the smart contracts will execute the verification logic based on the provided policies and our external data providers.

- Upon verification, the payout will be distributed to the clients. The use of smart contracts aims to facilitate transparency and produce an auditable trail in any of the claim processing processes to deter fraudulent acts and build trust for clients in our insurance products.

Fig 2. Pandassurance CraftInsurance platform

Pandassurance ShopInsurance

This platform is for the clients to view and purchase the insurance provided by financial institutions.

Here is the user flow for a client purchasing and claiming a critical illness insurance product:

- Customers set up an account using our platform

- A standard Know Your Customer (KYC) check would then be performed on the consumer to validate their identity. This could be done in the form of getting the consumer to enter their personal details, followed by them taking a video holding their identification card to authenticate the user.

- Once logged in, the various insurance products offered will then be displayed and made purchasable by the clients.

- The client acknowledges that they have read through the terms and payout conditions for the insurance product they have selected from the platform.

- The client purchases the insurance which they have chosen and a smart contract would be created on the blockchain.

- When the client wants to make a claim, doctors would serve as validators and authenticate the information and condition of the client. This process could optionally be a multi-signature feature where the digital signature from multiple stakeholders (from the medical and/or bank side) is required to validate the smart contract.

- When all required signatures have been received, the smart contract is triggered and the payout is distributed to the insured.

Fig 3. Pandassurance ShopInsurance platform

Pandassurance Validator Platform

This platform is used by trusted organisations to provide documents or data regarding a claim. The multi-signature wallet concept requires multiple validators within the same organisation. This configuration can be customised according to the needs of the contract created by the financial institutions.

Here is the user flow for a data provider validating claims for critical illness:

- A notification of the request for data is prompted by the customers to the data provider.

- The data provider submits the document to support the claim and signs the contract.

- Depending on the contract, there may be other stakeholders who are required to sign the contract.

- The smart contract activates on the completion of the pre-defined conditions set by the financial institutions.

Fig 4. Pandassurance Validator platform

Challenges of the solution

One potential issue we identified is the risk of false payouts triggered by malicious actors or hacking incidents, in which fake data is provided to our smart contract. An example is a doctor that acts with malicious intent would send fake reports of the clients, which would trigger the approval of the contract. To address this, we have implemented a multi-signature feature that allows banks to customise the number of signatures required for data validation according to the specific insurance product and its associated risks.

For example, a low-paying and low-risk insurance product may require only one signature from the data provider, while a high-paying or high-security product may require additional signatures from the data provider and/or the bank's own personnel. This added layer of security will ensure the integrity of the payouts and protect against fraudulent activity.

What's next for our project

For future iterations, as our platforms and system gain a solid foundation of customers and processes. By incorporating CoinGecko's API, we can scale our product to be able to serve the needs of many around the world, by allowing for real-time currency conversion of prices. This would provide increased reach and scalability for our platforms.

We could also explore a model where data APIs from trusted sources are integrated to replace the middleman of physical data validators. This would allow for a truly automated and transparent process for customers. This platform could then easily be scaled to include other areas of insurance beyond medical and car coverage with such an approach.

Since fears of fraud are one of the primary concerns in the insurance industry, additional layers of security we could consider would be to require our data providing partners to stake ETH to sign up as one of our data providing partners. In this case, if they are detected to commit fraud, the ETH they have staked would be forfeited into our payout pool. We could also potentially include a function to generate a set data provider within our reputable partners (of reasonable distance from the user), using their claim ID and seed we generate on the server side. In this case, users would then be unable to collude directly with the validator, hence reducing the risk of fraud.

Built With

- css

- express.js

- figma

- hardhat.js

- html

- javascript

- mongodb

- node.js

- solidity

Log in or sign up for Devpost to join the conversation.