-

-

System Architecture

-

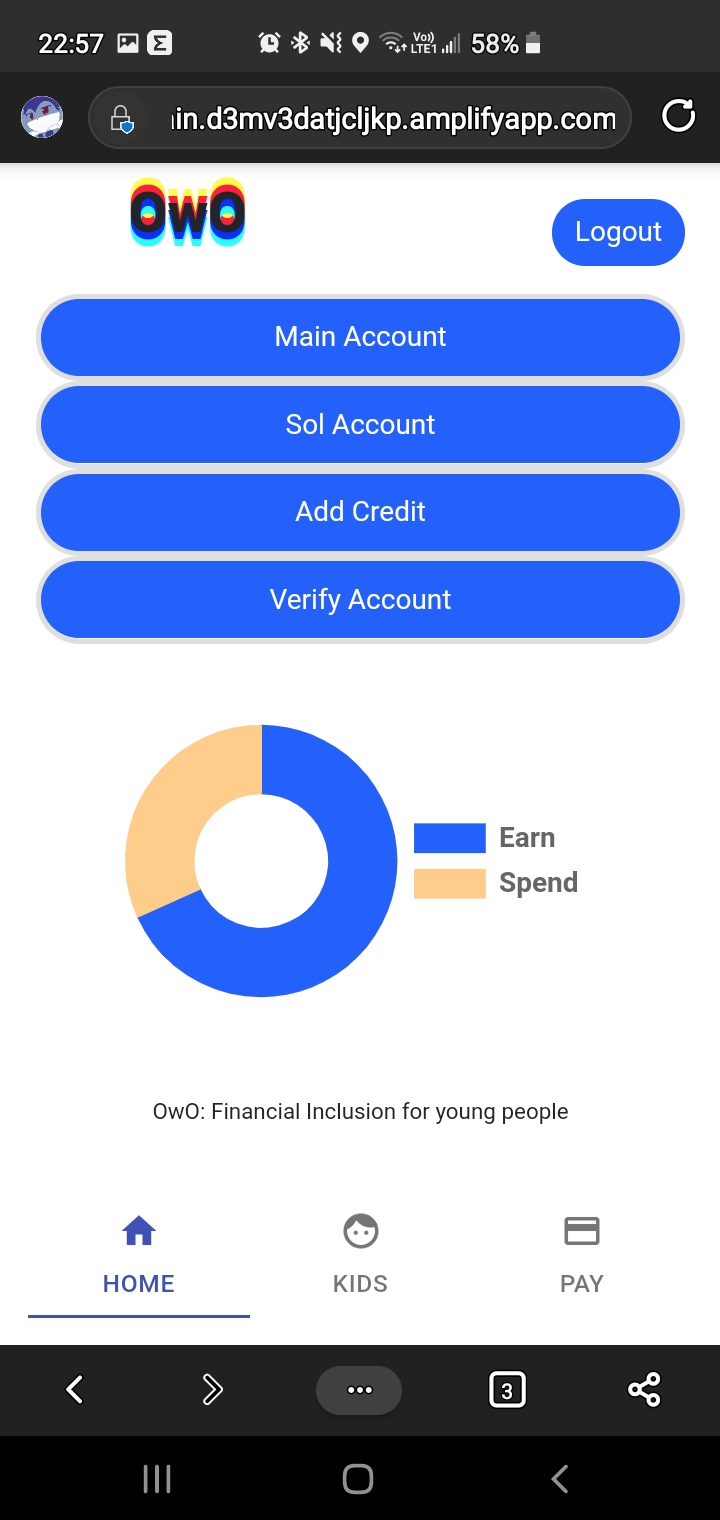

Main Dashboard

-

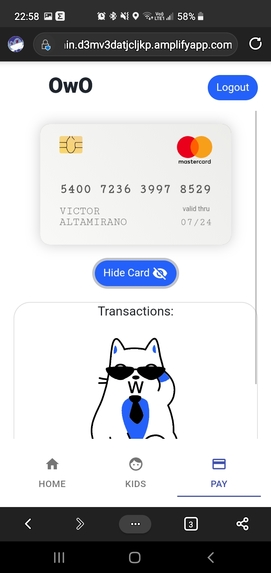

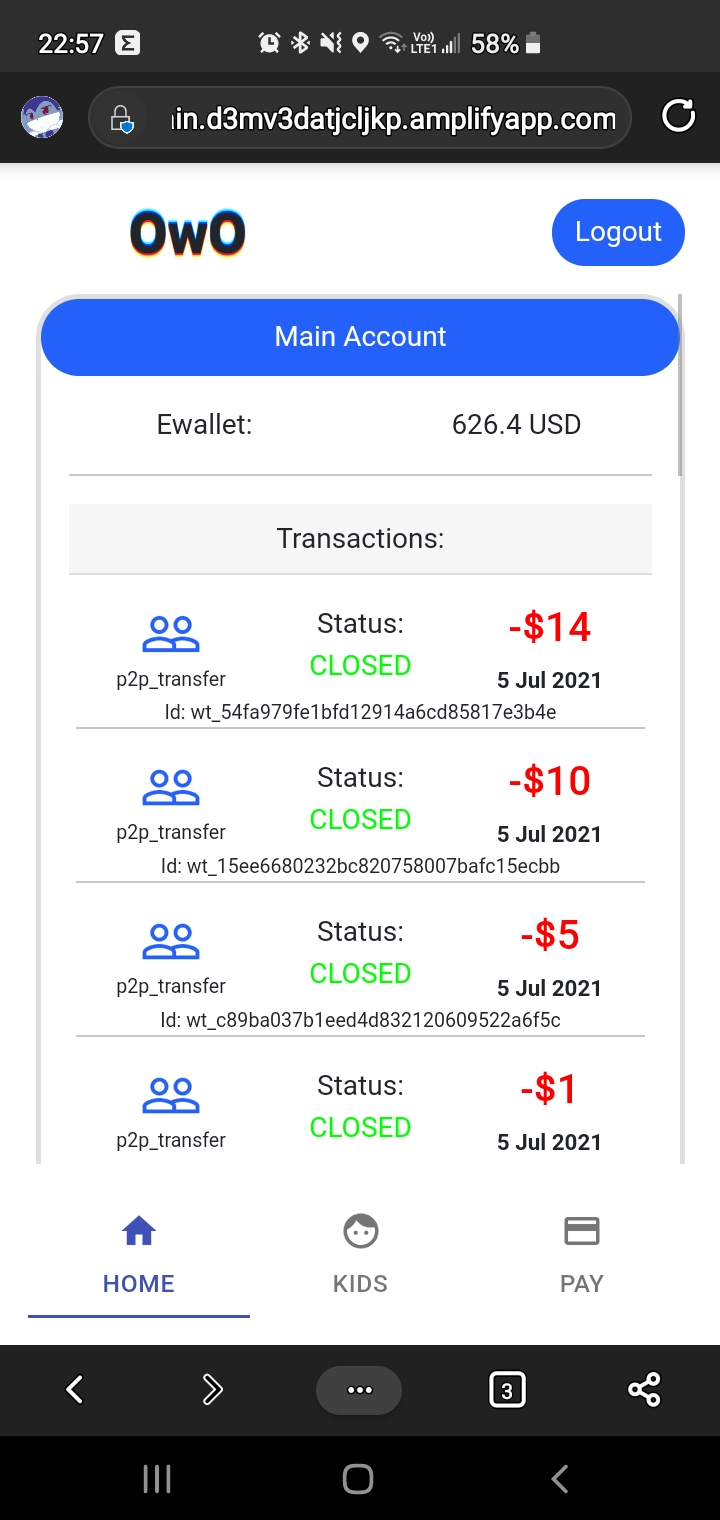

Transaction History

-

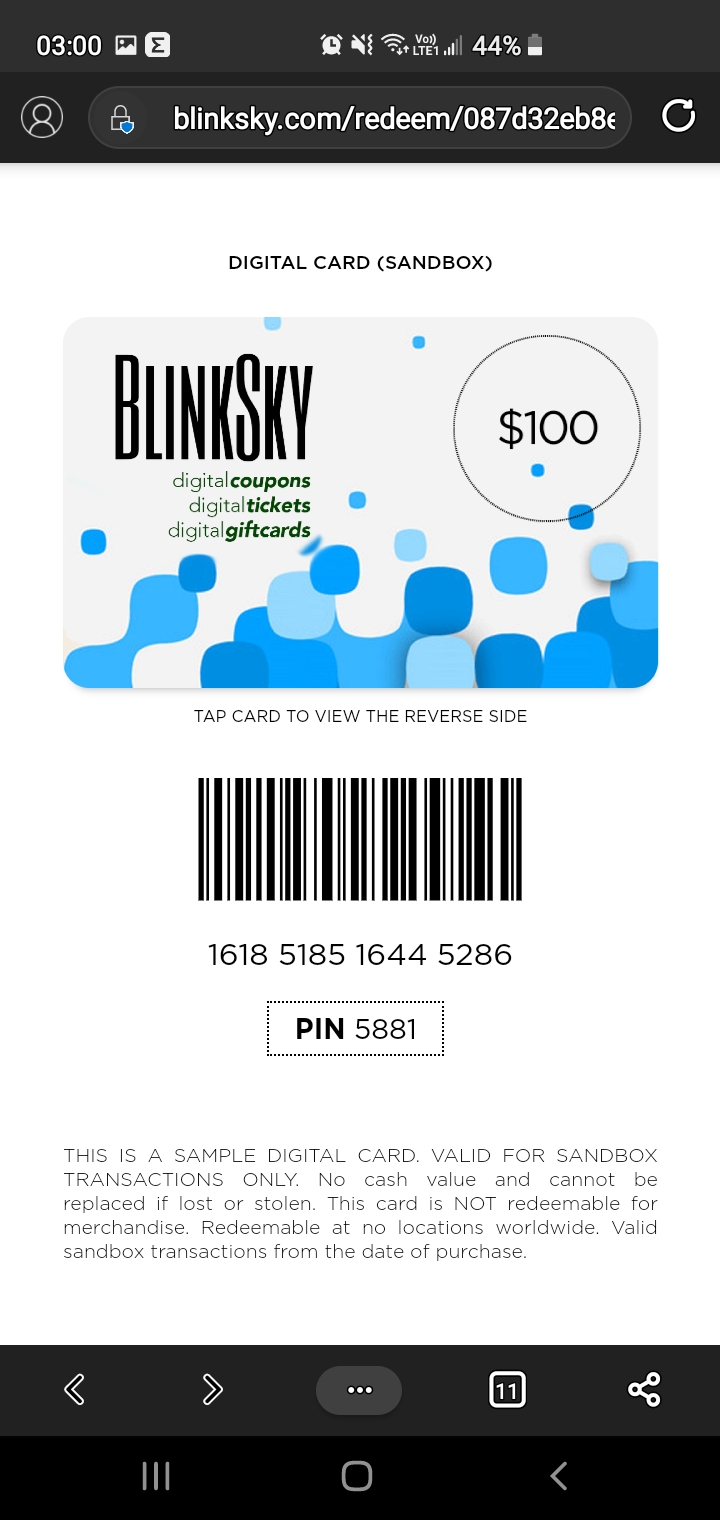

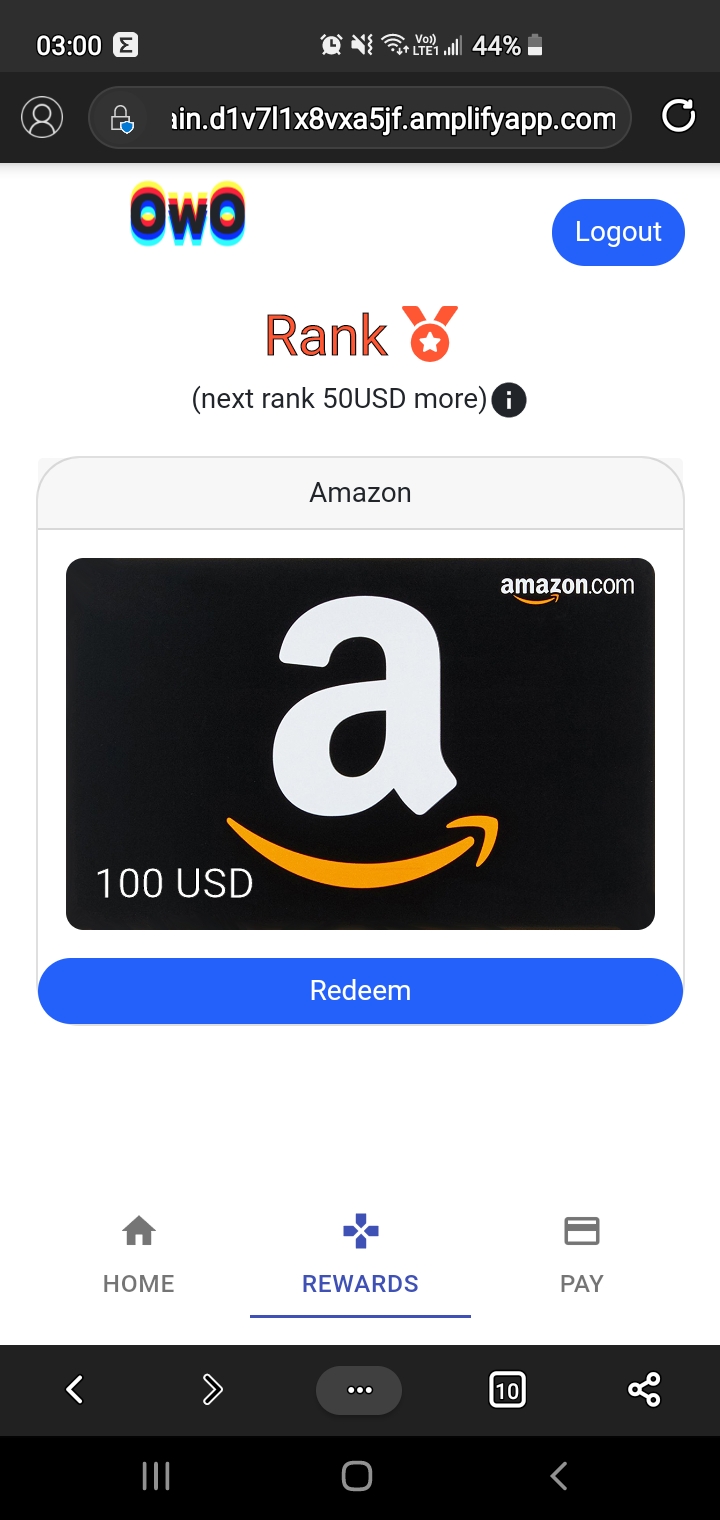

Gamifyed Blinksky rewards!

-

More rewards!

-

And More!

-

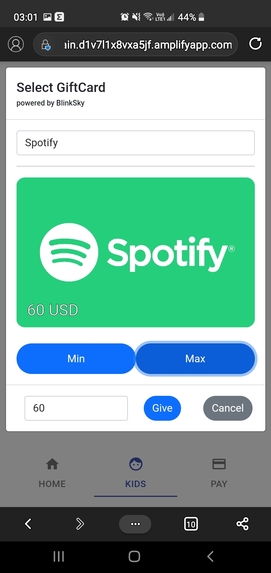

Reward selection

-

Card issuance

Introduction and inspiration

As Millennials, when our team were children we had very different interests in relation to goods and services. We mostly bought bikes, toys, board games and video games without microtransactions. We went to Gamestop or similar stores and bought our games with cash and that was it.

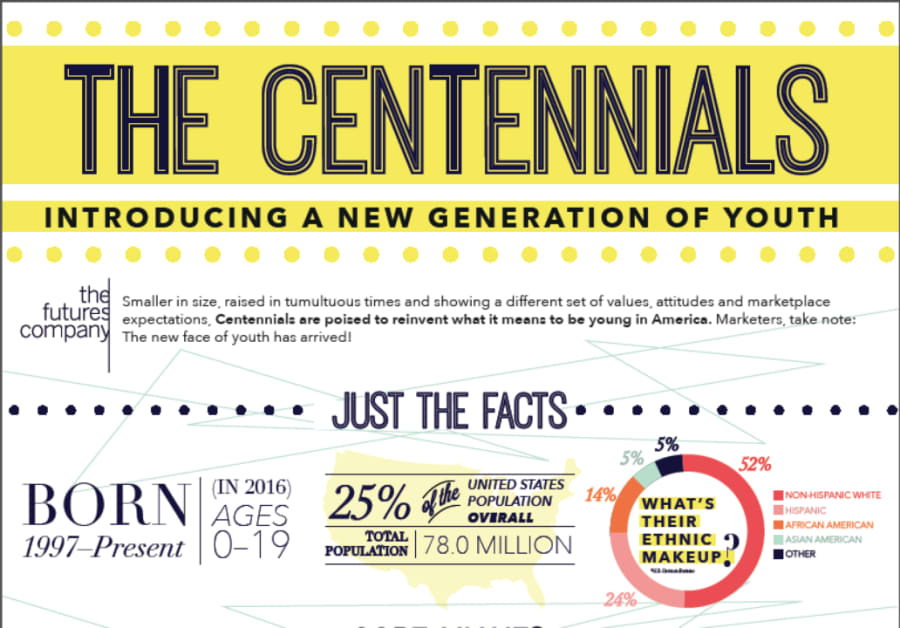

The world has changed, and a new generation has emerged that is the bigger one yet. Enter Zed Generation or Centennials.

What are their interests you may add?

90% of them consume digital content such as services like Netflix, Youtube, Spotify or Fortnite.

As the world turned into a more digitized one their interests of course are on the more digital side, instead of buying that Video Game and just playing it, theirs have microtransactions. Instead of going to a movie, they prefer to watch Netflix (also because of COVID). Instead of listening to music on the radio they want to acquire a Spotify account. And the number of digital services they want keeps on growing.

And well this is the main problem presented here.

They have a very hard time acquiring these products in a world that has sped up considerably and does not offer any financial solution that they can call their own.

For most of these they need a credit or debit card to be able to get them, which they cannot acquire because of their age and while we have prepaid cards that can be bought with cash, they are very limited and a hassle to buy.

In addition to that financial literacy is not met at a young age and they are about to join the millennials as one of the generations with a bigger debt and lack of financial literacy. Studies show that the sooner a person is involved with the financial system, the more financially literate he will become in later life. At the same time this is a huge opportunity for banks as it shows that the first card or banking system a person adopts, will remain a customer most of his life and will be its main pivot point for its financial endeavors. (1)

There is seldom any Fintech, banking solution or project willing to look at this market (which is huge) and generate a solution.

Until now....

Enter OwO

OwO is a platform that connects Centennials and their interests with the financial world. We have two main aspects to this application, a Parent side and a Kid's or youngster side.

Firstly, the parent is the one in charge of user creation and provides its child with both capital and limits on how to use said capital. In addition to freezing the child's account if he or she deems so.

Secondly, we have the child side where he will get a gamified experience and a virtual card where he will be able to spend, save his capital in his or her interests which are primordially digital. This in addition to rewards given by these same interests in tandem with the whole experience.

Why on mobile?

Regrettably, Cell Phones have much more penetration than even banks or any other financial apparatus. It is the ideal platform as Centennials pass a lot of time glued to their phones.

Extra feature! Solana Blockchain integration

We have crypto transferences with the Solana Blockchain for the parent account. Solana is an excelent blockchain for transferences with very low fees.

How we built it

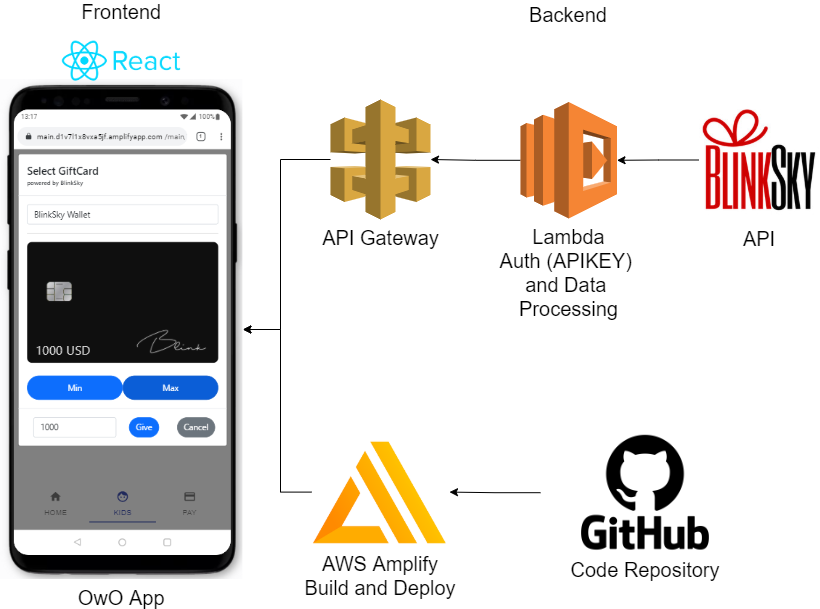

The image above is the system's architecture. You can see that all of our development is scalable thanks to the management of AWS and Rapyd, due to its ability to handle customer requests. The mobile web app is done in React, using AWS's ecosystem as a bridge between our deployment and the application. In the same way this serves as a bridge between Rapyd's APIs and the Solana Blockchain in the following way:

Usage of Blinksky APIs

We have extensive documentation on how we used every single one of the API's employed in the solution in this part of our github:

https://github.com/altaga/OwO-Blinkathon#owo

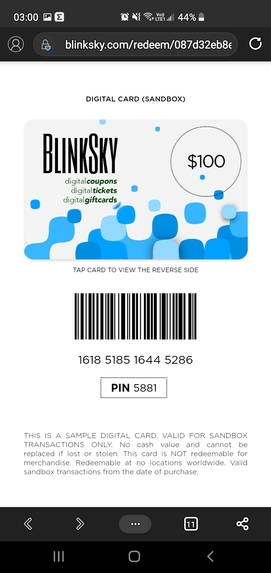

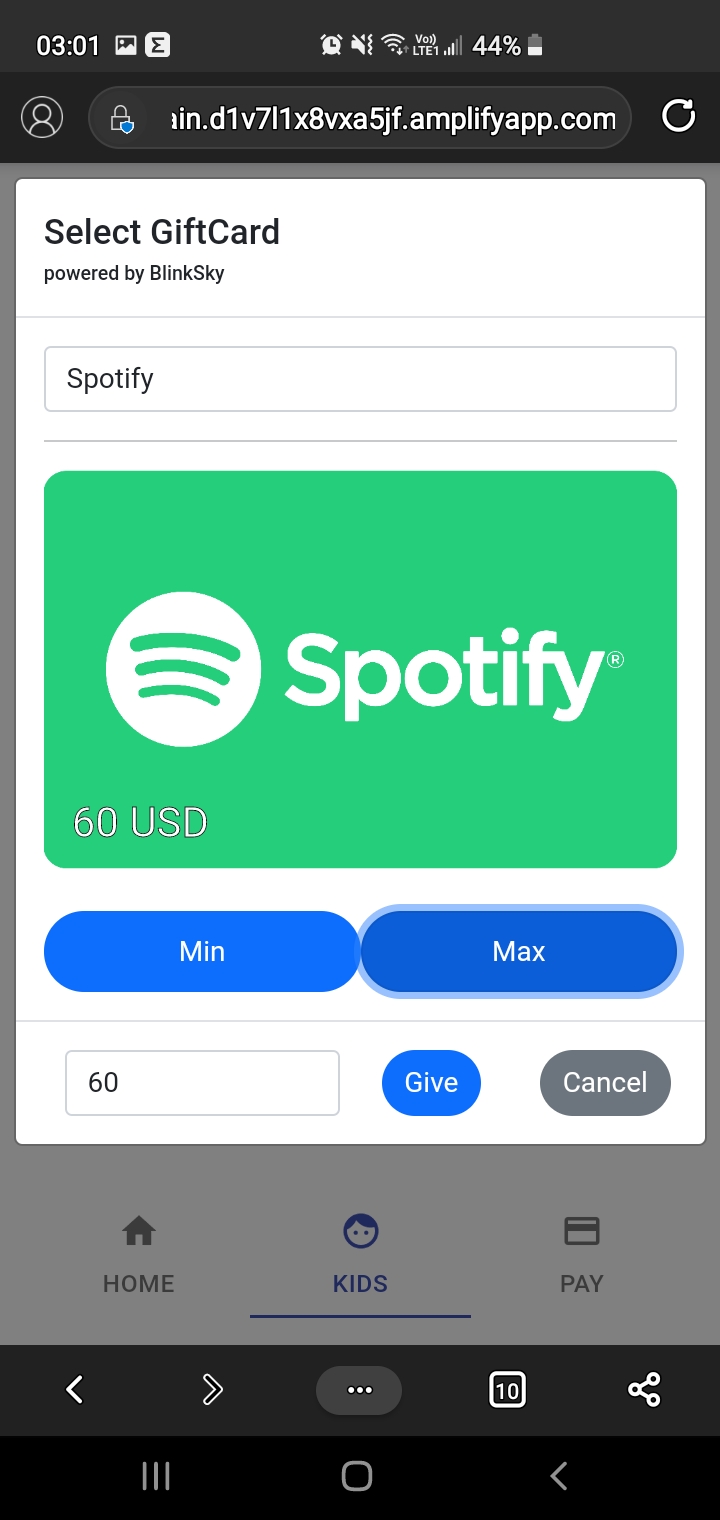

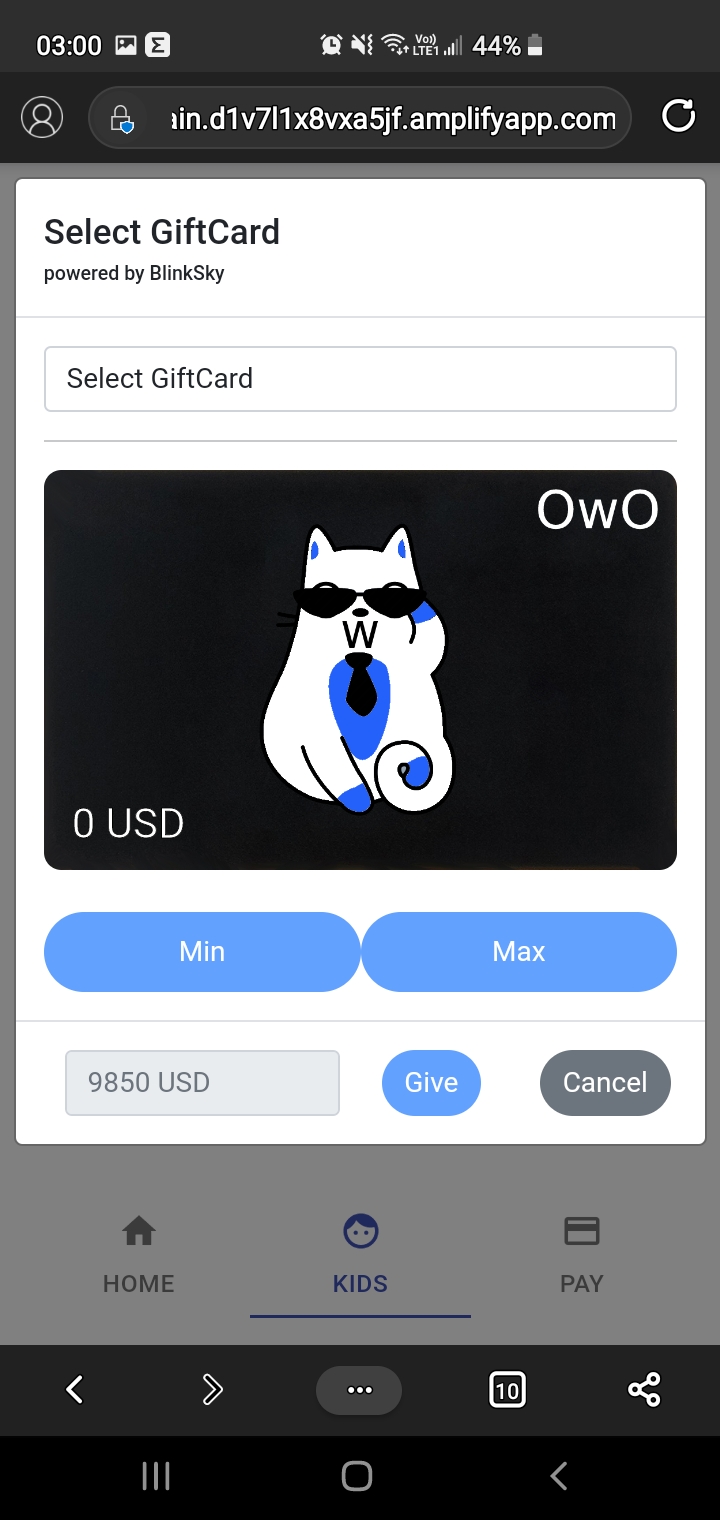

One of the most important parts of our solution is how we employ Blinksky's gift cards as rewards for accumulating points in the OwO system:

Test it yourself

Webpage:

https://main.d1v7l1x8vxa5jf.amplifyapp.com/

To test it follow the instructions presented here:

https://github.com/altaga/OwO-Blinkathon/blob/main/TEST.md

Hopefully you like the application!

Final Conclusions

Banks and financial institutions are wasting a huge opportunity when they do not provide a product for these upcoming generations. While we know that immediacy is important and the bigger spenders are those of older generations, several of the biggest companies nowadays (such as Netflix and Spotify) have shown that small subscription based payments are here to stay and most in this new generation are in need of a financial product of this kind. I think this functional prototype has the potential to cover that niche and we are excited to continue developing the idea and the project.

References:

(1)https://financialopticshq.com/blog/consequences-of-financial-illiteracy/

(2)https://www.inphantry.com/from-millennials-to-centennials-the-passing-of-the-torch/

Built With

- amazon-web-services

- blinksky-apis

- rapyd

- react

- solana

Log in or sign up for Devpost to join the conversation.