-

Web UI demo

Inspiration

We wanted to demonstrate how hardware acceleration can speed up complex financial computations, making Monte Carlo simulations fast enough for real-time option pricing.

What it does

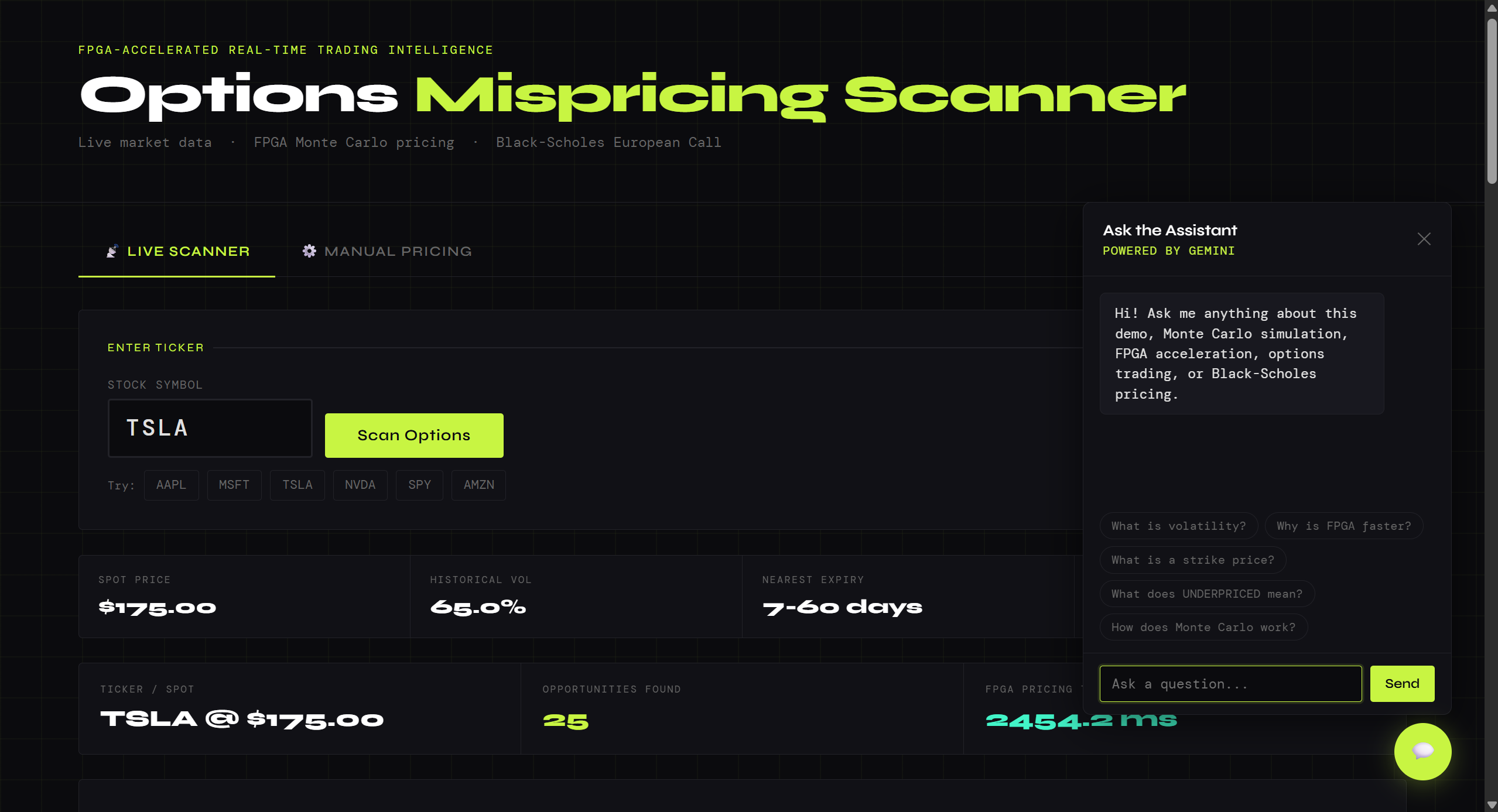

Our system prices options using Monte Carlo simulations on both CPU and FPGA, compares performance, and scans options chains to identify over- or underpriced contracts.

How we built it

We used a PYNQ-Z2 FPGA with a Monte Carlo kernel synthesized in Vivado HLS, controlled via Python and Flask. The frontend uses HTML5/CSS3 and JavaScript with Plotly for interactive charts.

Challenges we ran into

Handling large data transfers to the FPGA, ensuring numerical accuracy between CPU and FPGA, and integrating a real-time interactive frontend were some of the main challenges.

Accomplishments that we're proud of

We achieved a 22x speedup on 50,000-path simulations, created a fully functional options mispricing scanner, and built a hackathon-ready web interface with an AI assistant.

What we learned

We deepened our understanding of FPGA acceleration, Monte Carlo simulations, web-based data visualization, and integrating AI into a full-stack demo.

What's next for Options Mispricing Scanner

We plan to add implied volatility calculations, support put options, incorporate real market data, and enhance the AI assistant with conversation memory for richer interactions.

Log in or sign up for Devpost to join the conversation.