Inspiration

During my engineering coursework, I was introduced to financial markets and derivative pricing models. While learning the theory behind option pricing, I became curious about how these mathematical models are actually implemented in real-world systems and used by traders and analysts. Most existing tools either hide the math or are too complex for learners, which motivated me to build a simple yet powerful alternative.

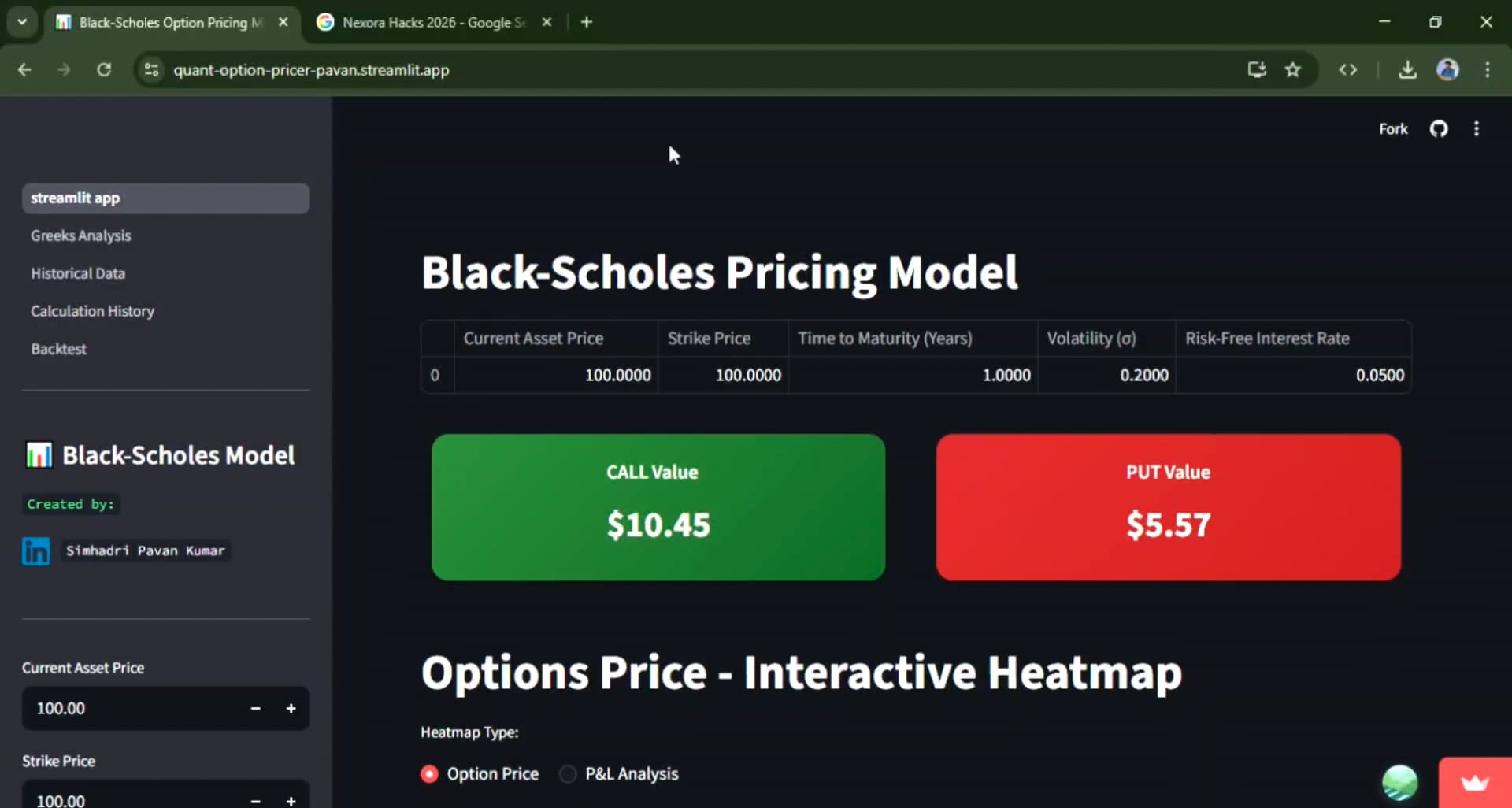

What it does

OptionLens is an interactive option pricing and risk analysis tool based on the Black-Scholes model. It calculates theoretical prices for European call and put options and computes key Greeks such as Delta, Gamma, Vega, Theta, and Rho. Users can dynamically adjust parameters like stock price, strike price, volatility, time to expiry, and interest rate to observe their impact in real time.

How I built it

I implemented the Black-Scholes formula programmatically and derived closed-form expressions for the Greeks. The backend handles accurate numerical computation, while the frontend provides an interactive interface for parameter tuning and visualization. The focus was on correctness, clarity, and responsiveness rather than overfitting or prediction.

Challenges I ran into

One of the main challenges was handling numerical stability, especially for extreme parameter values such as very low time to expiry or high volatility. Another challenge was clearly explaining theoretical pricing without misleading users into thinking it predicts exact market prices.

What I learned

This project helped me bridge the gap between financial theory and software engineering. I gained a deeper understanding of option pricing assumptions, market limitations, and how quantitative models are used as benchmarks rather than absolute predictors.

What's next

Future improvements include supporting implied volatility calculation, comparing theoretical prices with live market data, and extending the model to alternative pricing methods such as binomial trees.

Log in or sign up for Devpost to join the conversation.