-

-

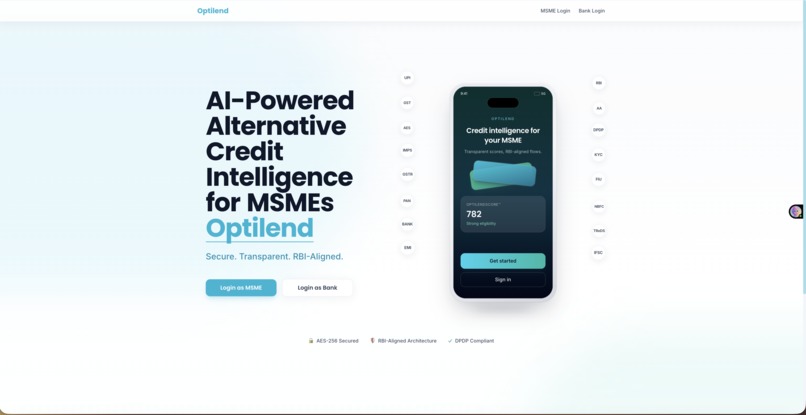

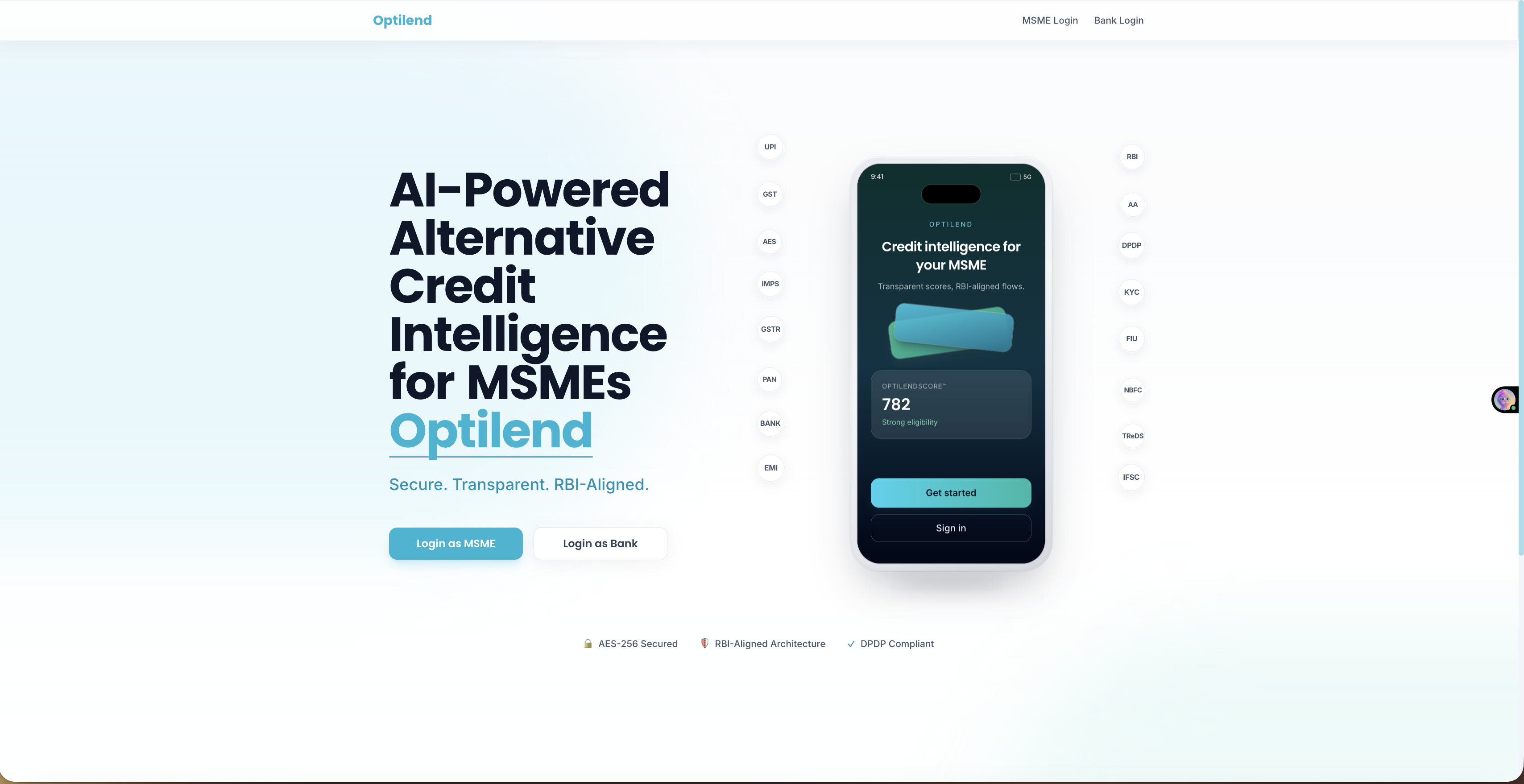

hero page

-

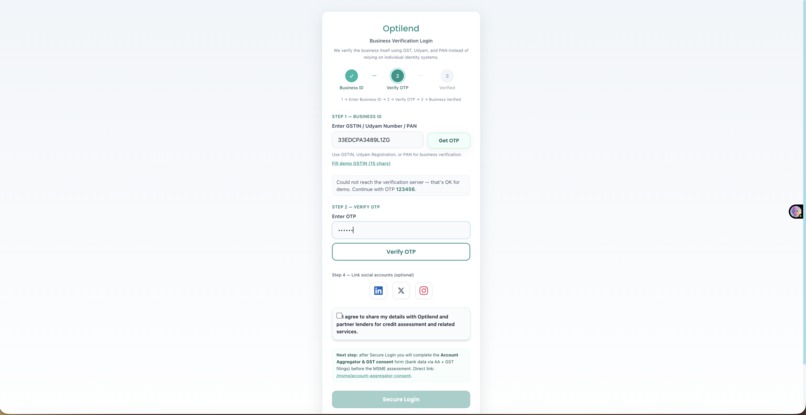

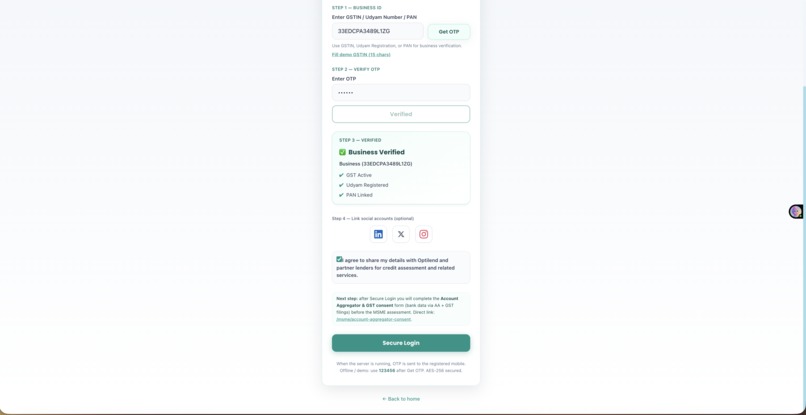

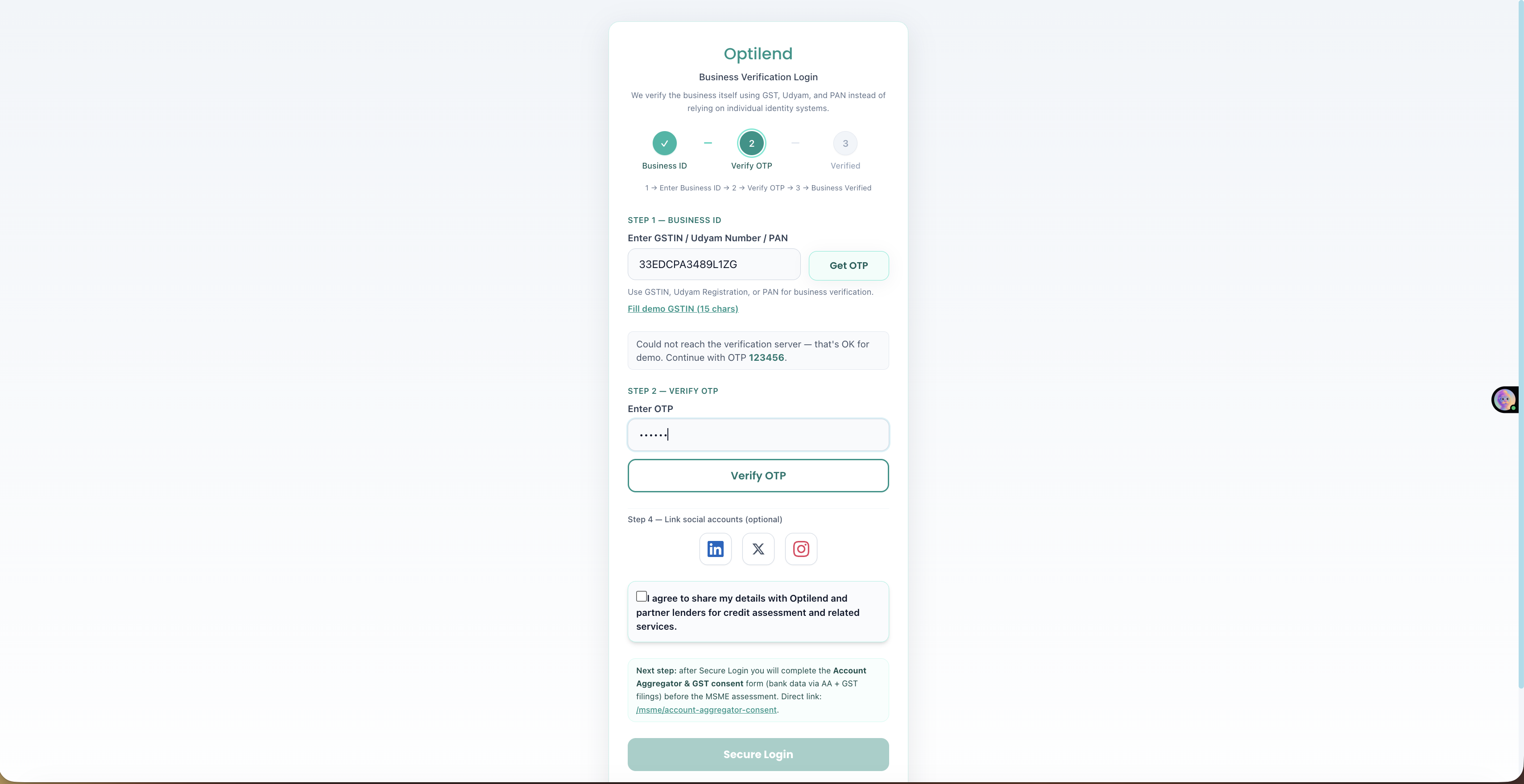

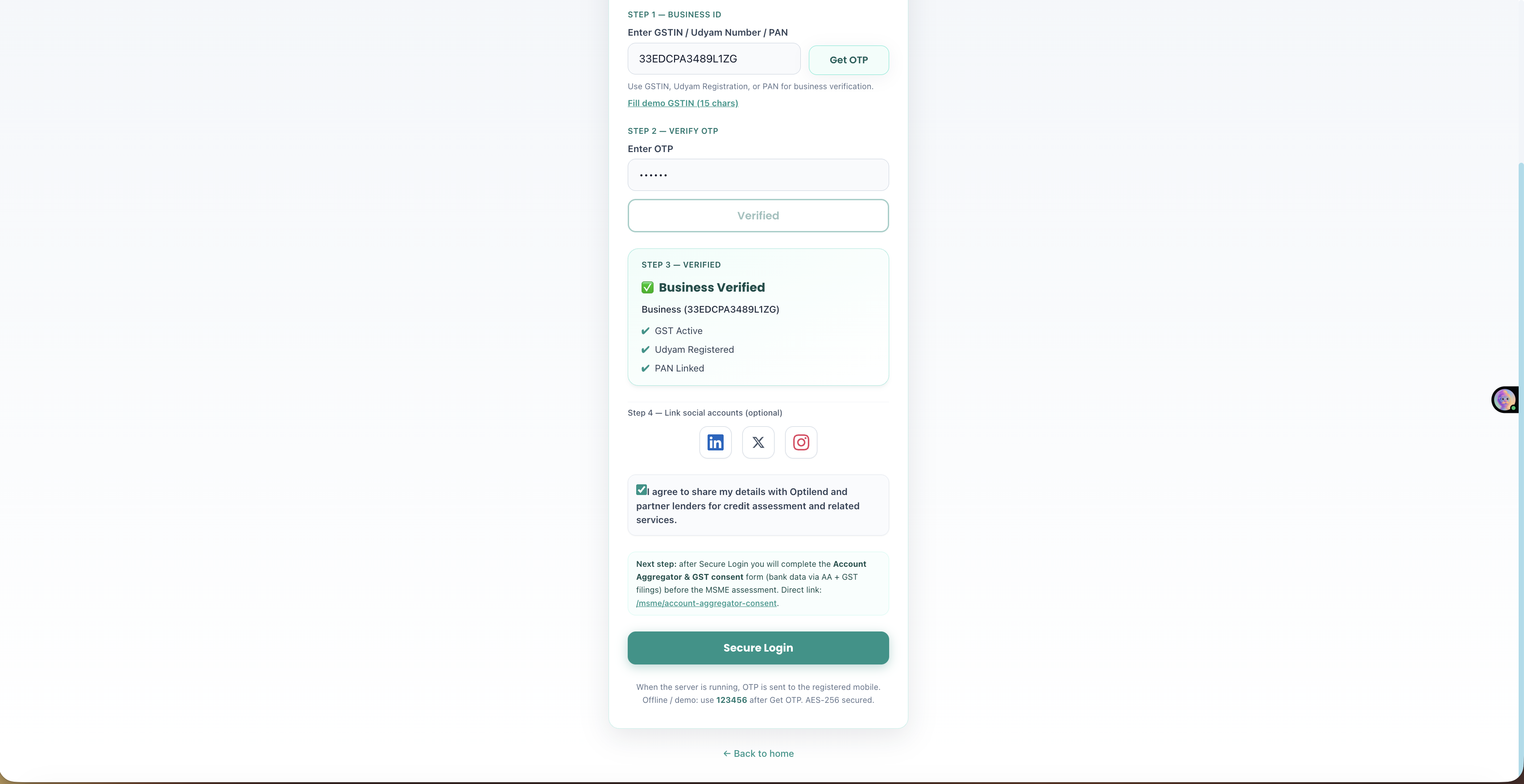

logging as MSME

-

verify GST number through GST verification API

-

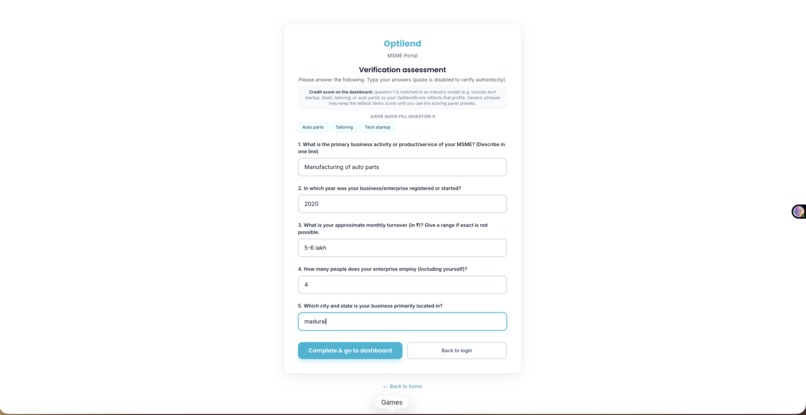

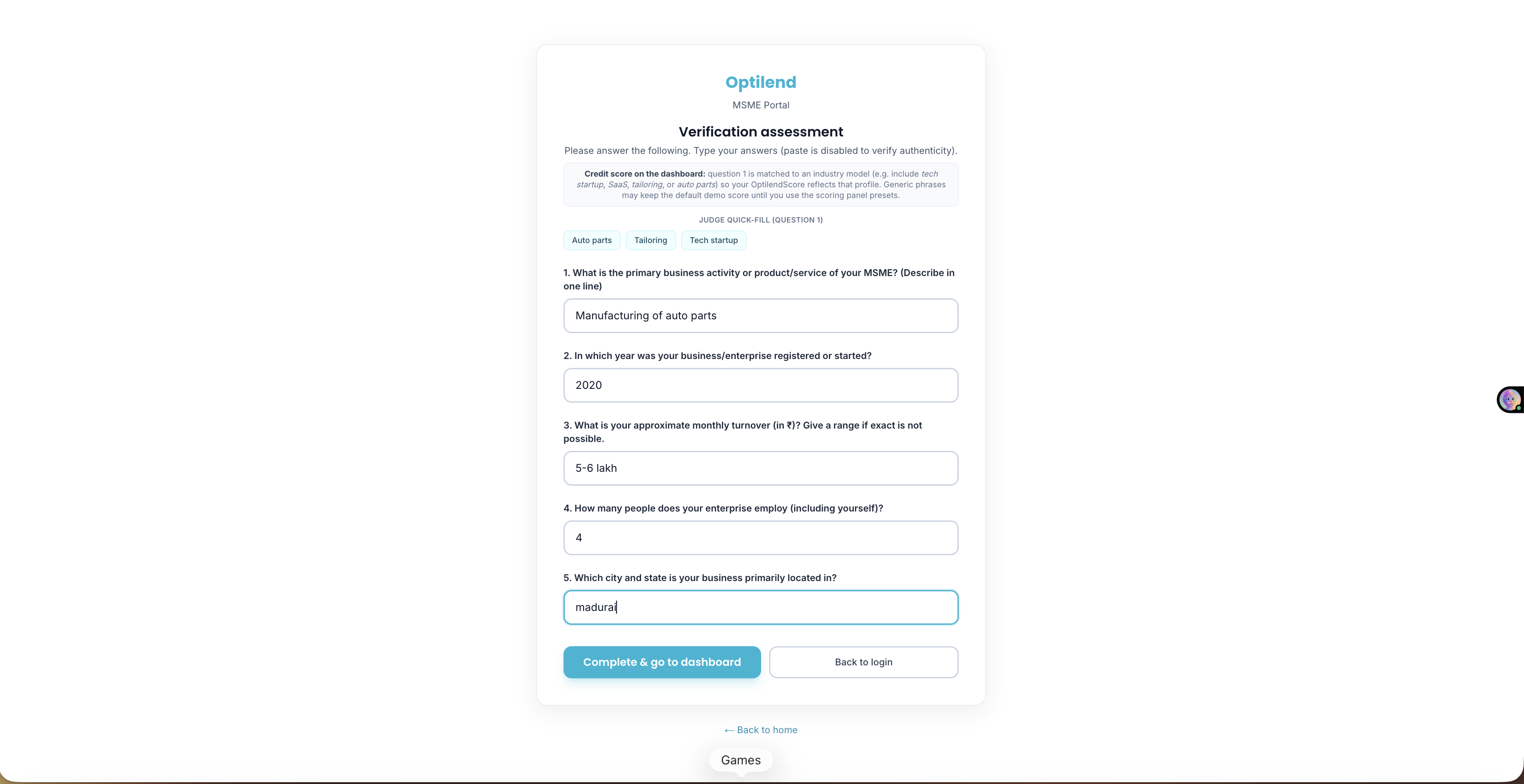

Assessment for tier 1 scoring

-

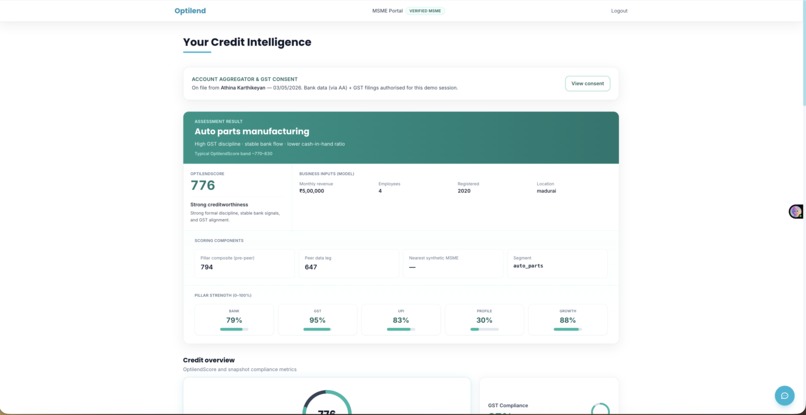

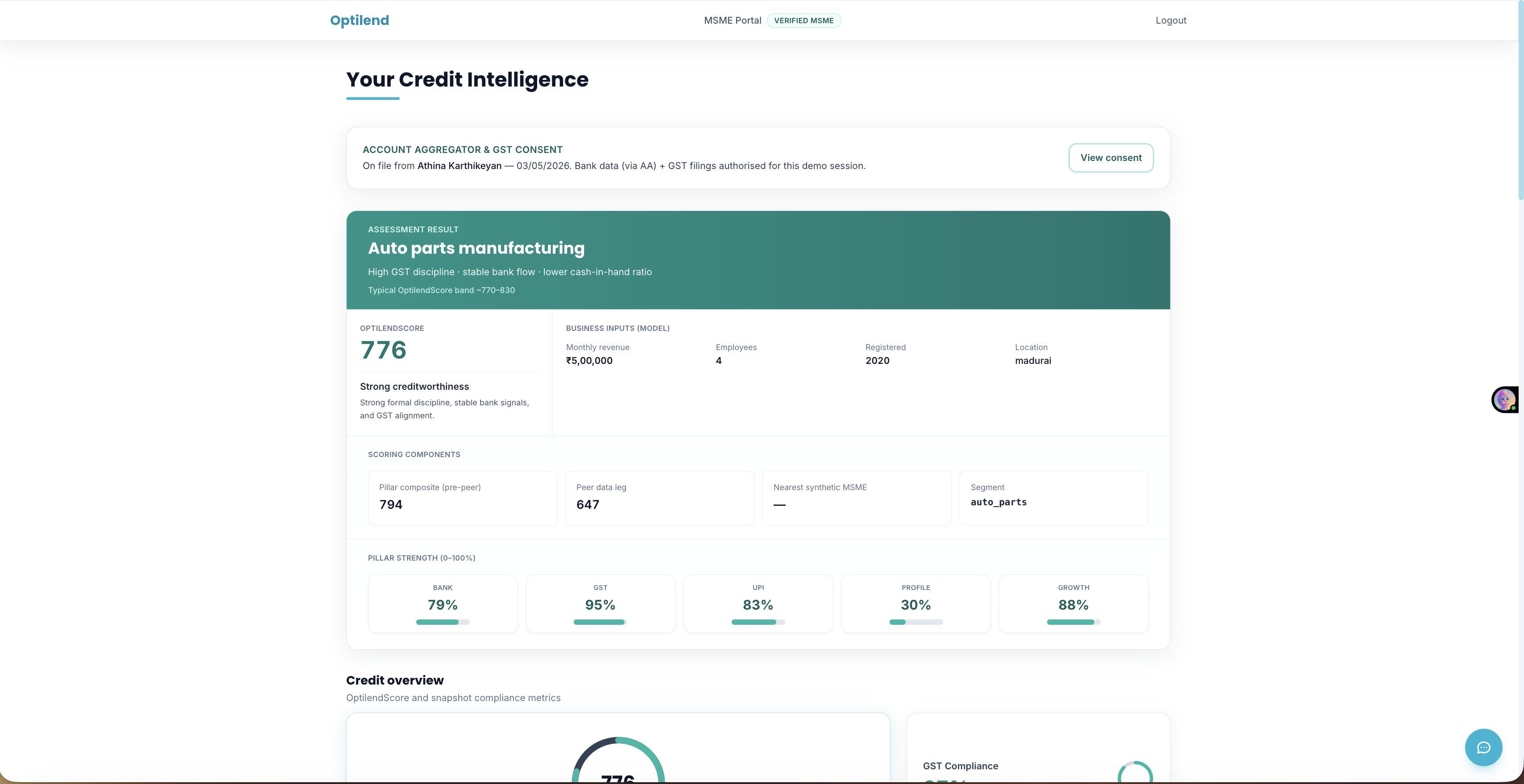

tier 1 scoring result

-

personalised credit scoring

-

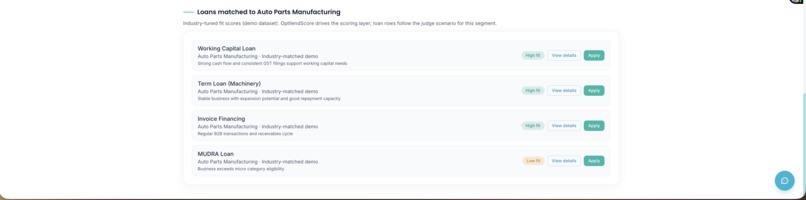

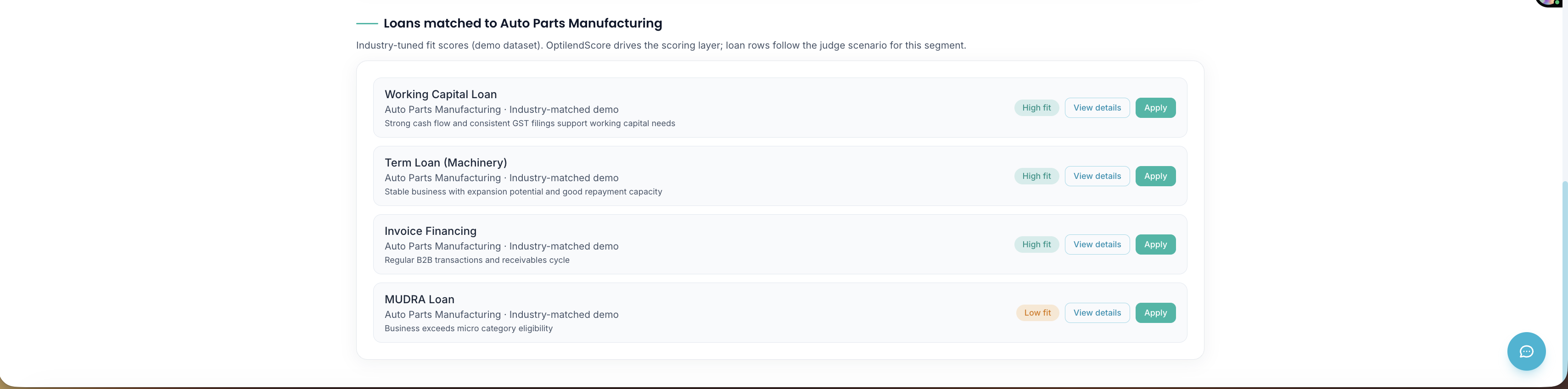

Loan recommendation(data scraping) as per credit score

-

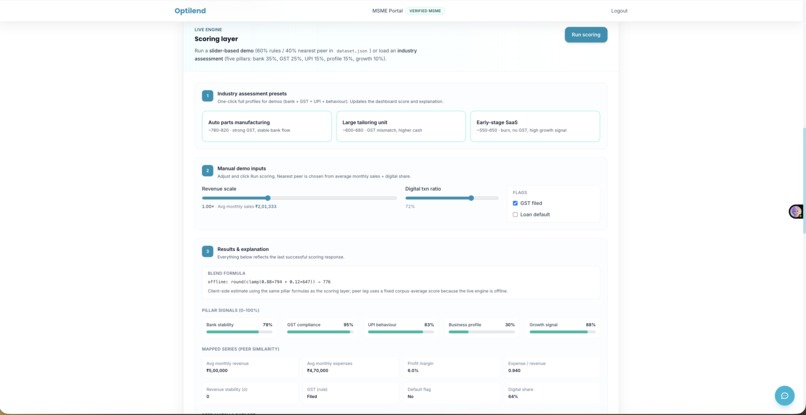

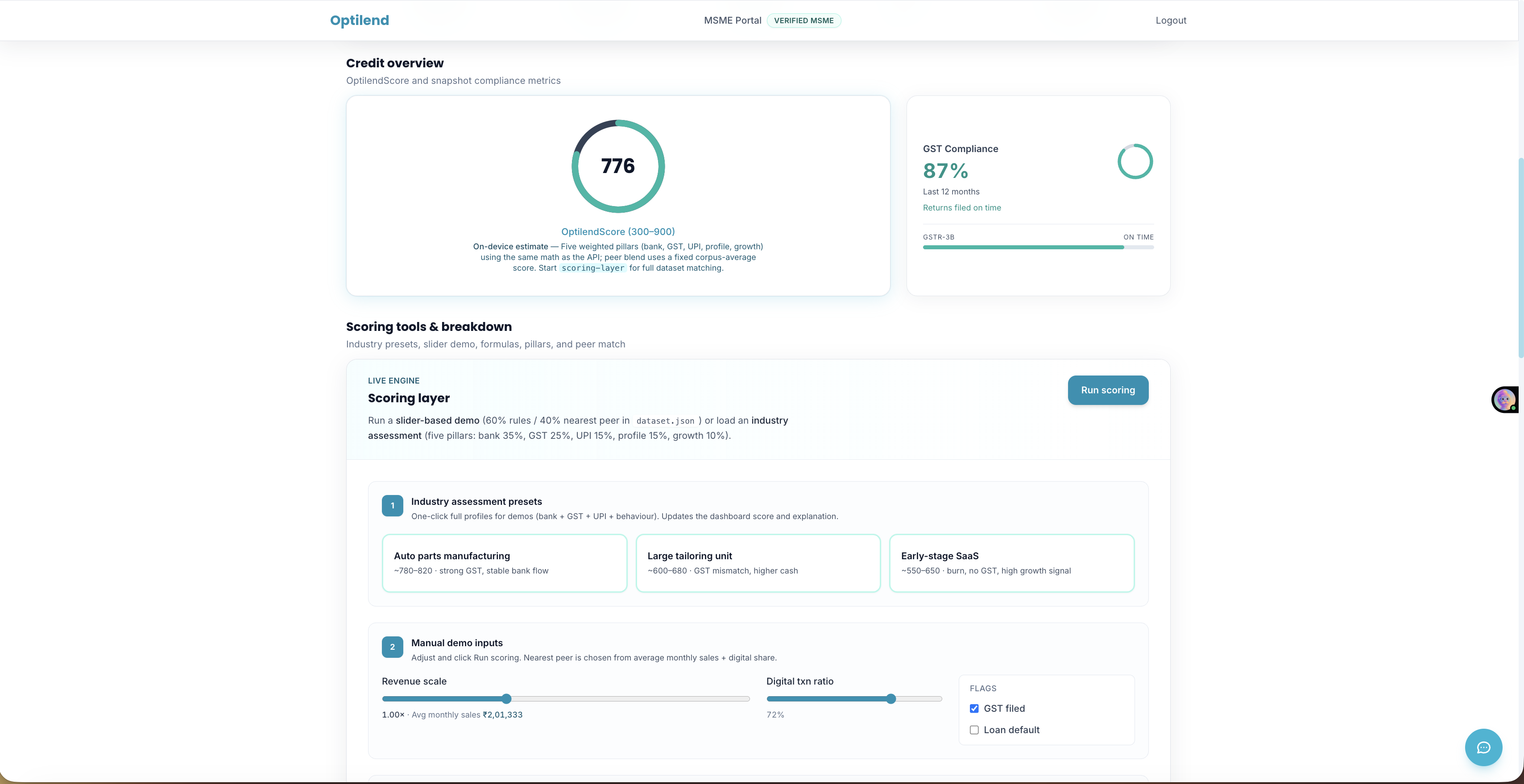

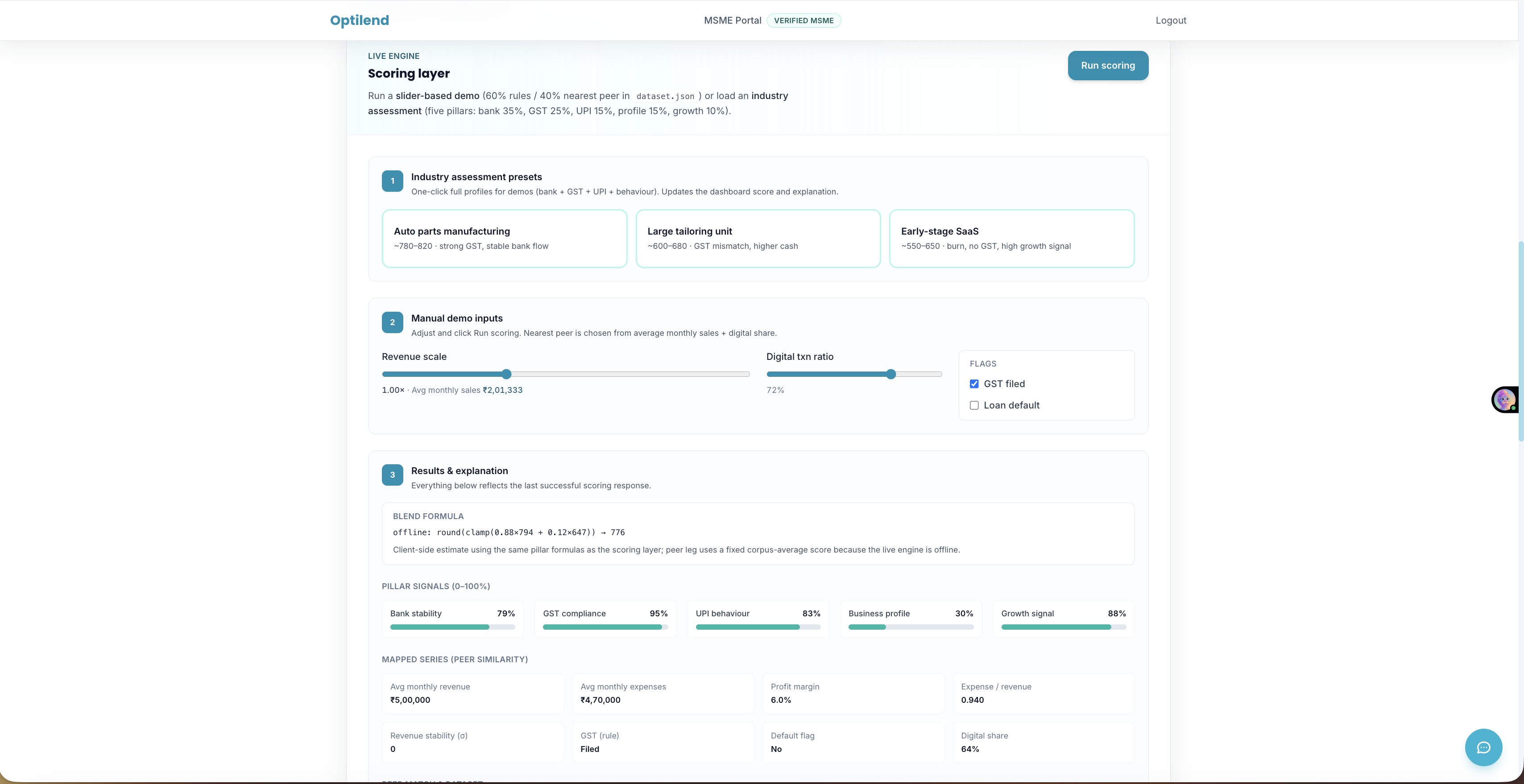

parameter adjustment as per user needs

-

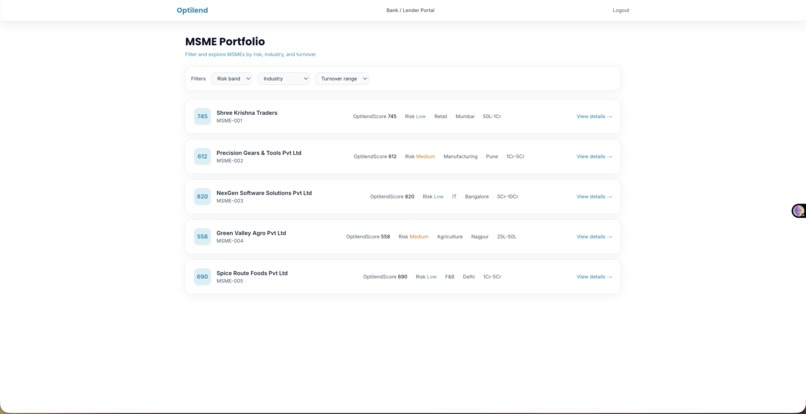

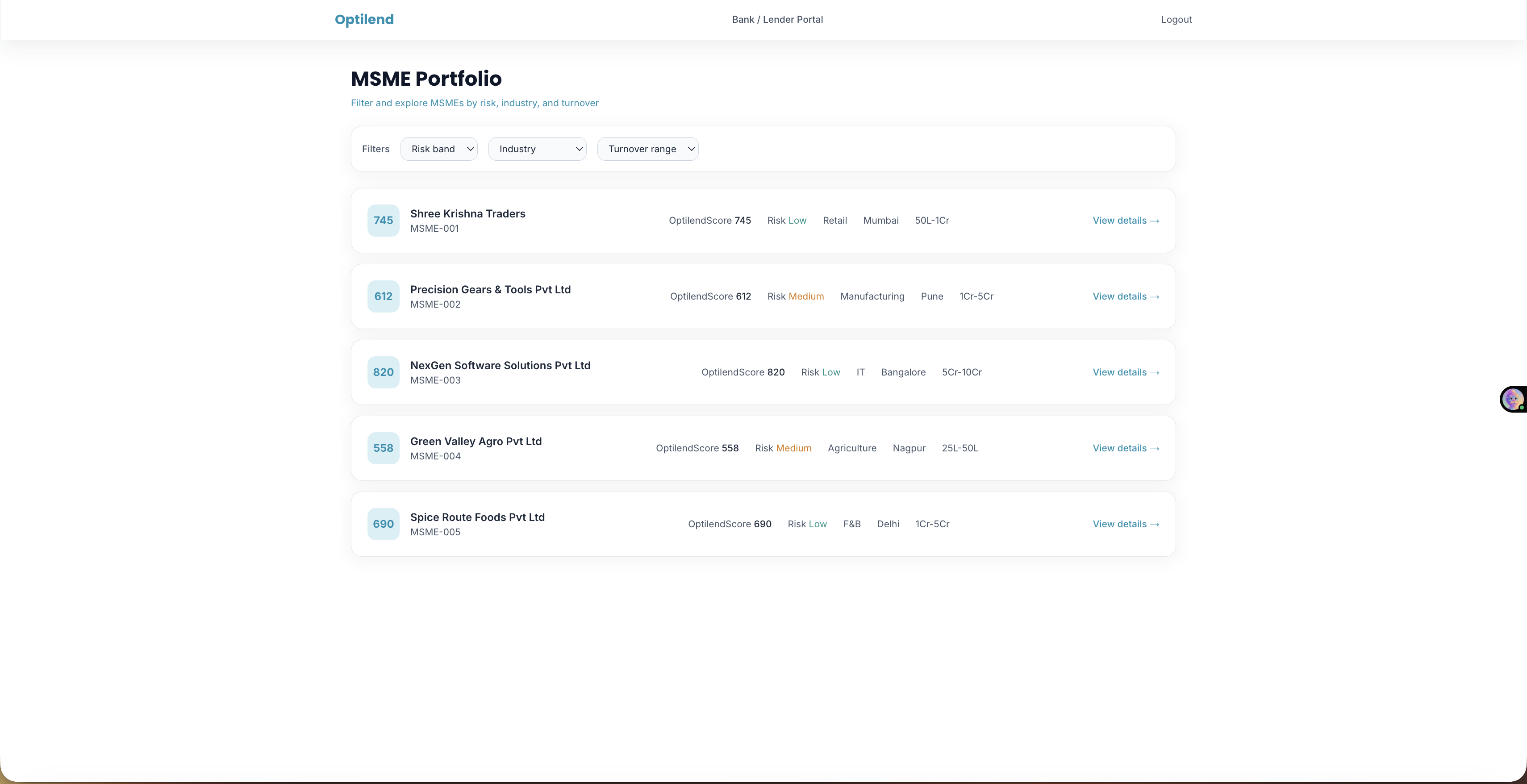

MSME portfolio

-

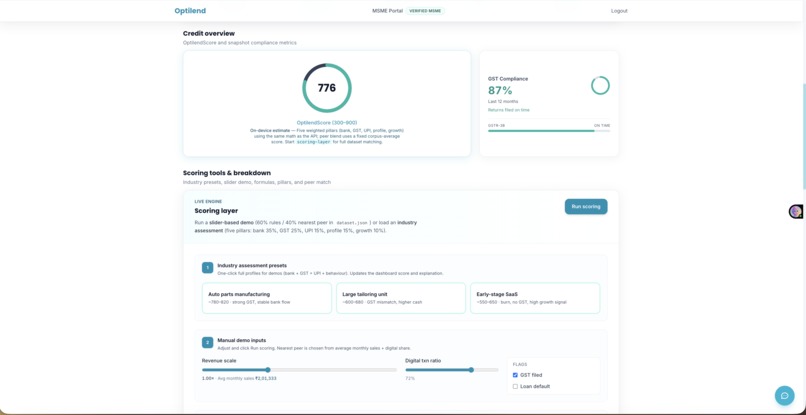

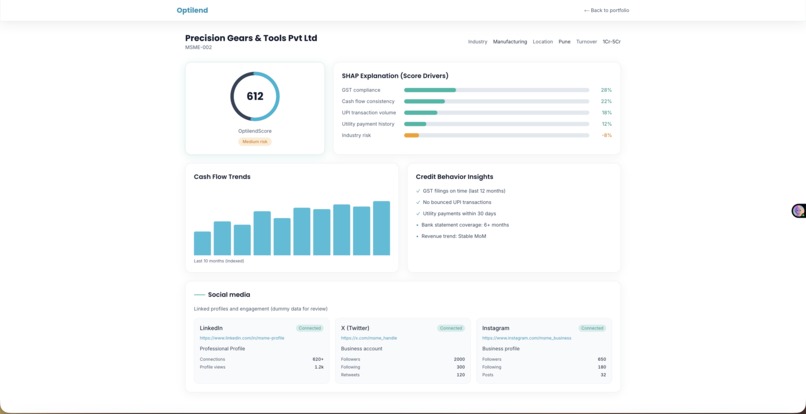

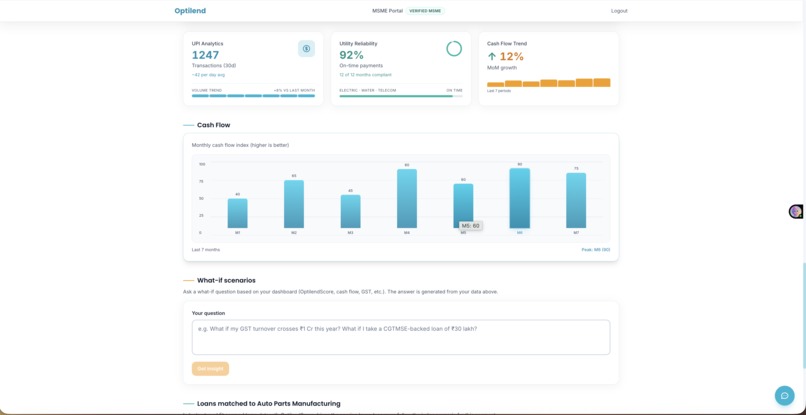

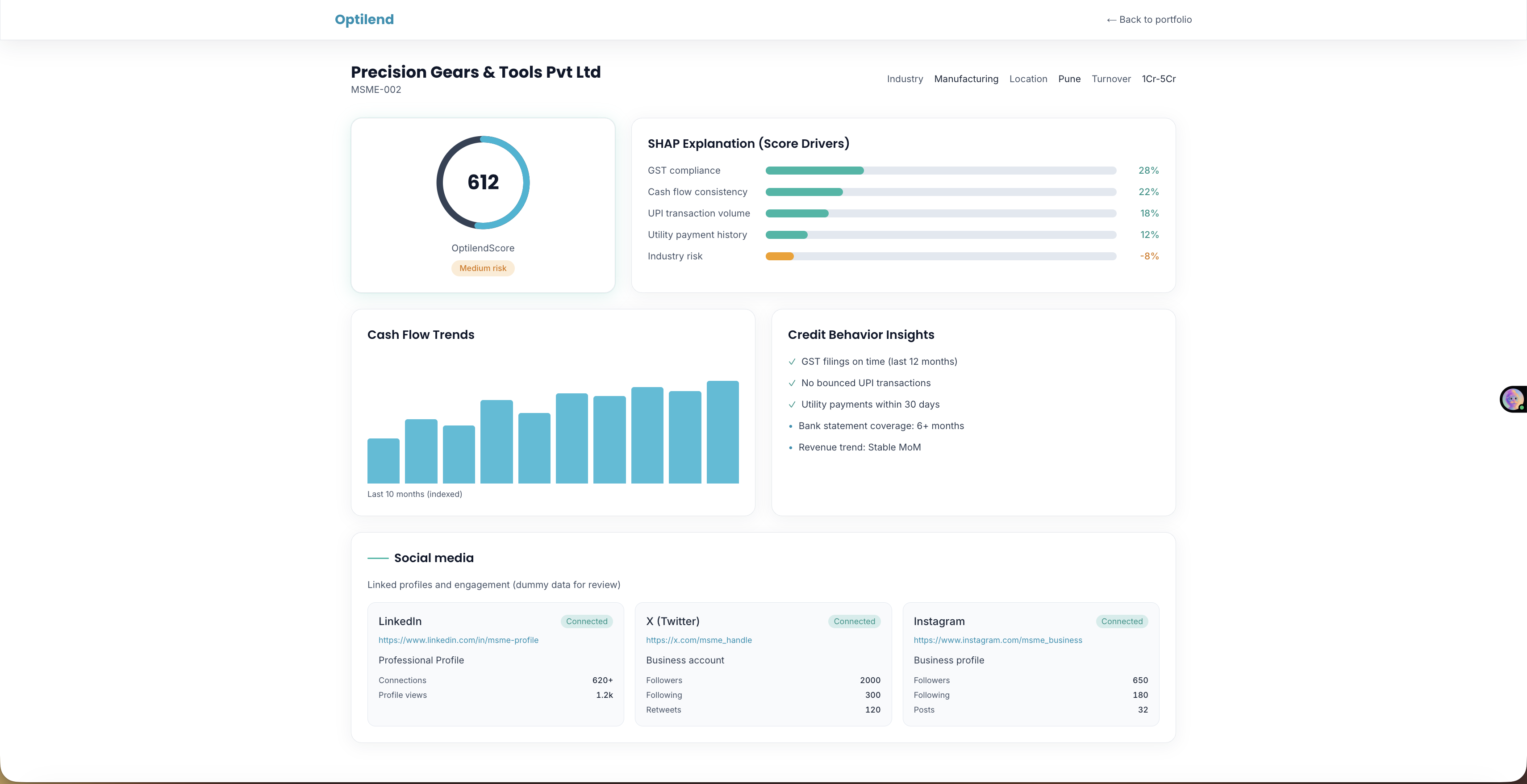

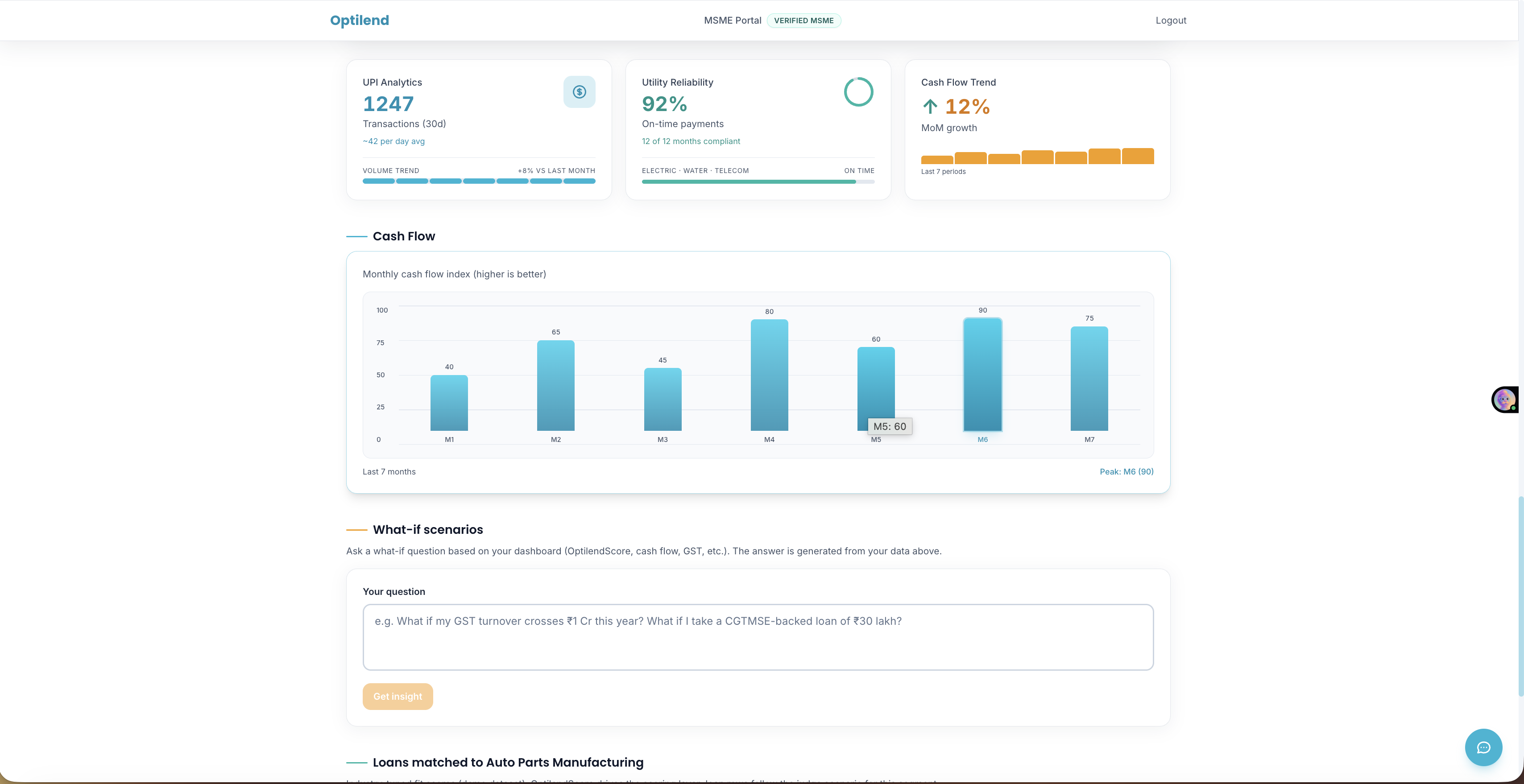

SHAP explanation and analytics dashboard

-

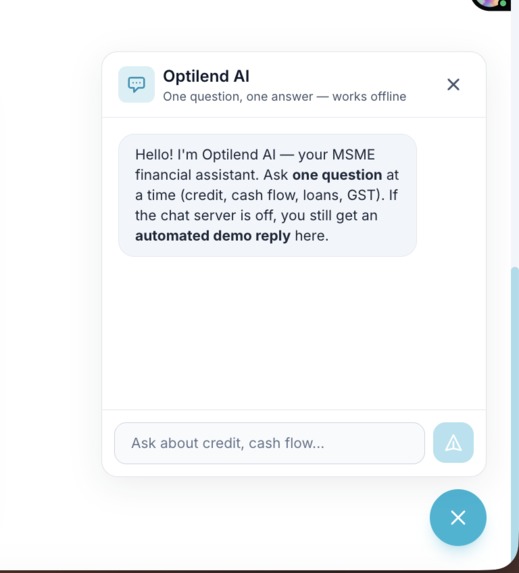

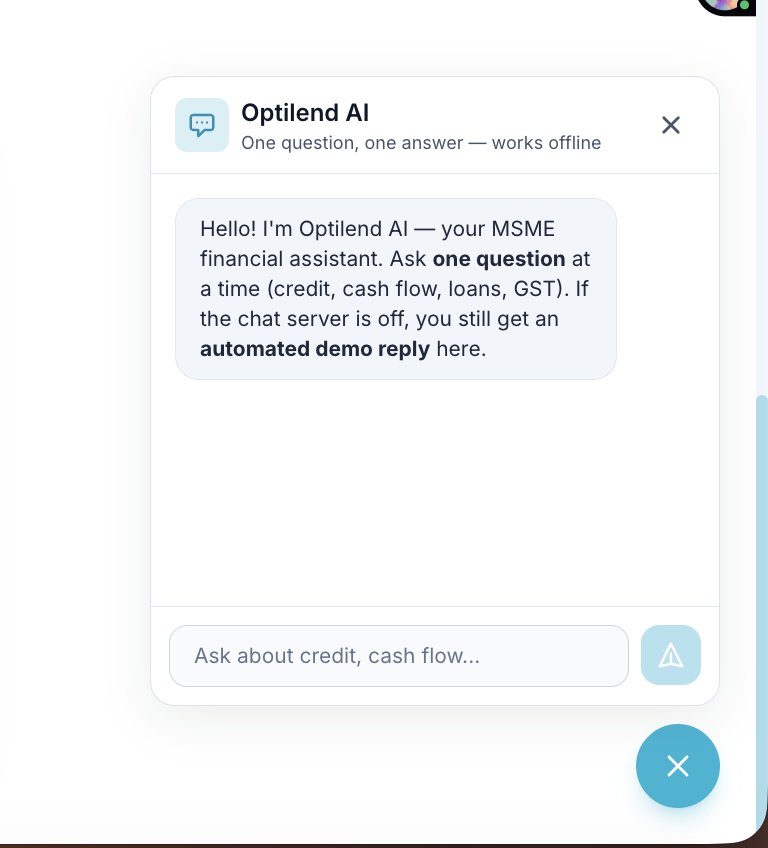

AI chat bot

-

Logging in as bank

-

social media presence of MSME's

-

cash flow-UPI,GST and hot cash-Full analytics dashboard

Optilend — Reimagining MSME Credit with Explainable AI

Inspiration

MSMEs contribute significantly to economic growth, yet many struggle to access formal credit. The issue is not always financial risk, but lack of structured financial visibility.

Traditional credit systems rely heavily on CIBIL scores, which:

- Ignore real-time cash flow

- Overlook GST and digital transactions

- Disadvantage businesses with limited credit history

What if businesses could be evaluated based on how they operate today, rather than their past borrowing history?

What We Built

Optilend is an AI-powered alternative credit intelligence platform that evaluates MSMEs using real business signals.

Instead of relying only on credit history, the system analyzes:

- GST filings (compliance and revenue consistency)

- Bank transactions (cash flow stability)

- UPI and digital payments (behavioral reliability)

- Growth trends (business trajectory)

- Business profile (structure and scale)

The system generates:

- A credit score between 300–900

- A risk classification

- Explainable insights for lenders

How It Works

Scoring Overview

The scoring system combines rule-based financial logic with data-driven peer comparison.

Pillar-Based Scoring

We compute normalized scores across five pillars:

| Pillar | Code | Weight |

|---|---|---|

| Bank Stability | B |

35% |

| GST Compliance | G |

25% |

| UPI Behavior | U |

15% |

| Business Profile | P |

15% |

| Growth Trends | Gr |

10% |

The pillar score is:

$$S_{\text{pillar}} = 0.35B + 0.25G + 0.15U + 0.15P + 0.10Gr$$

Peer-Based Adjustment

We use a synthetic dataset of MSMEs to find the nearest similar business based on:

- Revenue

- Digital transaction ratio

This gives a contextual peer score $S_{\text{peer}}$.

Final Score

The final score combines both components:

$$S_{\text{final}} = \text{round}(0.88 \cdot S_{\text{pillar}} + 0.12 \cdot S_{\text{peer}})$$

This ensures the score is personalized, explainable, and context-aware.

System Architecture

| Layer | Technology |

|---|---|

| Frontend | React, TypeScript, Tailwind CSS |

| Backend | Node.js (Express) |

| Database | Supabase (PostgreSQL) |

| AI | Google Gemini |

| Security | AES-256 encryption |

Security Design

The system follows a consent-first architecture aligned with the RBI Account Aggregator framework.

Key principles:

- Explicit user consent before accessing data

- Encrypted data transmission using AES-256

- No hardcoded keys — environment variables / KMS used

Security is implemented as a foundational layer, not an afterthought.

Key Features

- [ ]Explainable credit scoring

- [ ] Peer-based contextual evaluation

- [ ] Real-time financial signal analysis

- [ ] Risk breakdown for lenders

- [ ] Scenario simulation ("what-if" analysis) (in progress)

Challenges

Limited Real Data Access

Due to privacy constraints, real MSME data was not available.

Solution: Built a synthetic dataset simulating realistic financial behavior.

Explainability vs. Complexity

Highly accurate black-box models were considered. Transparency was prioritized instead.

Solution: Hybrid model combining rules + similarity matching.

Weight Calibration

Determining pillar weights required careful reasoning.

Solution: Iterative tuning based on financial logic and scenario testing.

Security Implementation

Ensuring strong encryption without overcomplicating the system.

Solution: AES-256 with secure key management via environment variables.

What We Learned

- Credit scoring requires trust and transparency, not just accuracy

- Explainability is essential for adoption in financial systems

- Privacy and consent must be embedded at the ==core==

- Real-world problems require combining technology + finance + policy thinking

Impact

Optilend enables:

- MSMEs to access fair, data-driven credit evaluation

- Banks to reduce risk through better insights

- A shift toward inclusive, transparent lending

Future Work

- [ ] Integration with real Account Aggregator APIs

- [ ] Use of anonymized real-world datasets

- [ ] Machine learning-based scoring enhancements

- [ ] Deployment as a scalable SaaS platform

Final Thought

Optilend redefines creditworthiness by shifting focus from static scores to dynamic business behavior.

It transforms lending from:

| From | To |

|---|---|

| Guesswork | Data-driven decision-making |

| Opacity | Explainability |

| Exclusion | Inclusion |

Scalability & Future Improvements

Optilend is architected to scale from a prototype to a production-grade financial platform.

Infrastructure Scalability

| Dimension | Current State | Future State |

|---|---|---|

| Data | Synthetic MSME dataset | Live Account Aggregator APIs |

| Scoring | Rule-based + peer matching | ML-enhanced scoring models |

| Deployment | Prototype | Multi-tenant SaaS platform |

| Users | Single lender | Banks, NBFCs, fintech partners |

| Geography | India-focused | Emerging market expansion |

Technical Roadmap

- API Layer — Expose scoring engine as REST APIs for third-party lender integration

- ML Upgrade — Replace static weights with trained regression/ensemble models on real data

- Real-time Scoring — Event-driven pipeline for live UPI/bank feed analysis

- Multi-tenancy — Role-based dashboards for banks, NBFCs, and borrowers

- Audit Trail — Immutable logging for RBI compliance and explainability audits

Business Scalability

- Lender Partnerships — Plug-and-play SDK for banks and NBFCs to embed Optilend scores

- White-labeling — Platform can be rebranded and deployed by financial institutions

- Tiered Pricing — SaaS model with per-assessment or subscription pricing

- Data Network Effect — More assessments → richer peer benchmarks → better scores over time

The more MSMEs assessed, the smarter and fairer the scoring engine becomes — creating a compounding improvement loop.

Built With

- aes-256-encryption

- api-testing-&-debugging

- asynchronous-processing

- component-based-architecture

- consent-driven-data-architecture

- control

- data-normalization-techniques

- data-pipeline-design

- environment-variable-based-key-management

- explainable-ai-(xai)

- express.js

- feature-engineering-pipeline

- git-&-github

- google-gemini-api

- hybrid-scoring-engine-(rule-based-+-similarity-matching)

- javascript-(es6+)

- middleware-architecture

- modular-backend-architecture

- natural-language-generation-(nlg)

- nearest-neighbor-search

- node.js

- postman

- query-optimization

- react

- react-hooks-(state-management)

- relational-data-modeling

- responsive-ui-design

- restful-api-design

- scalable-api-design

- secure-data-handling

- statistical-feature-extraction

- supabase-(postgresql)

- synthetic-msme-dataset-(dataset.json)

- tailwind-css

- typescript

- vercel

- version

- vite

- weighted-scoring-model

Log in or sign up for Devpost to join the conversation.