Inspiration

We tried to imitate and replicate the systematic quantitative research pipeline and the standard practices in industry.

How we built it

We divided ourselves into factor researchers and model researchers.

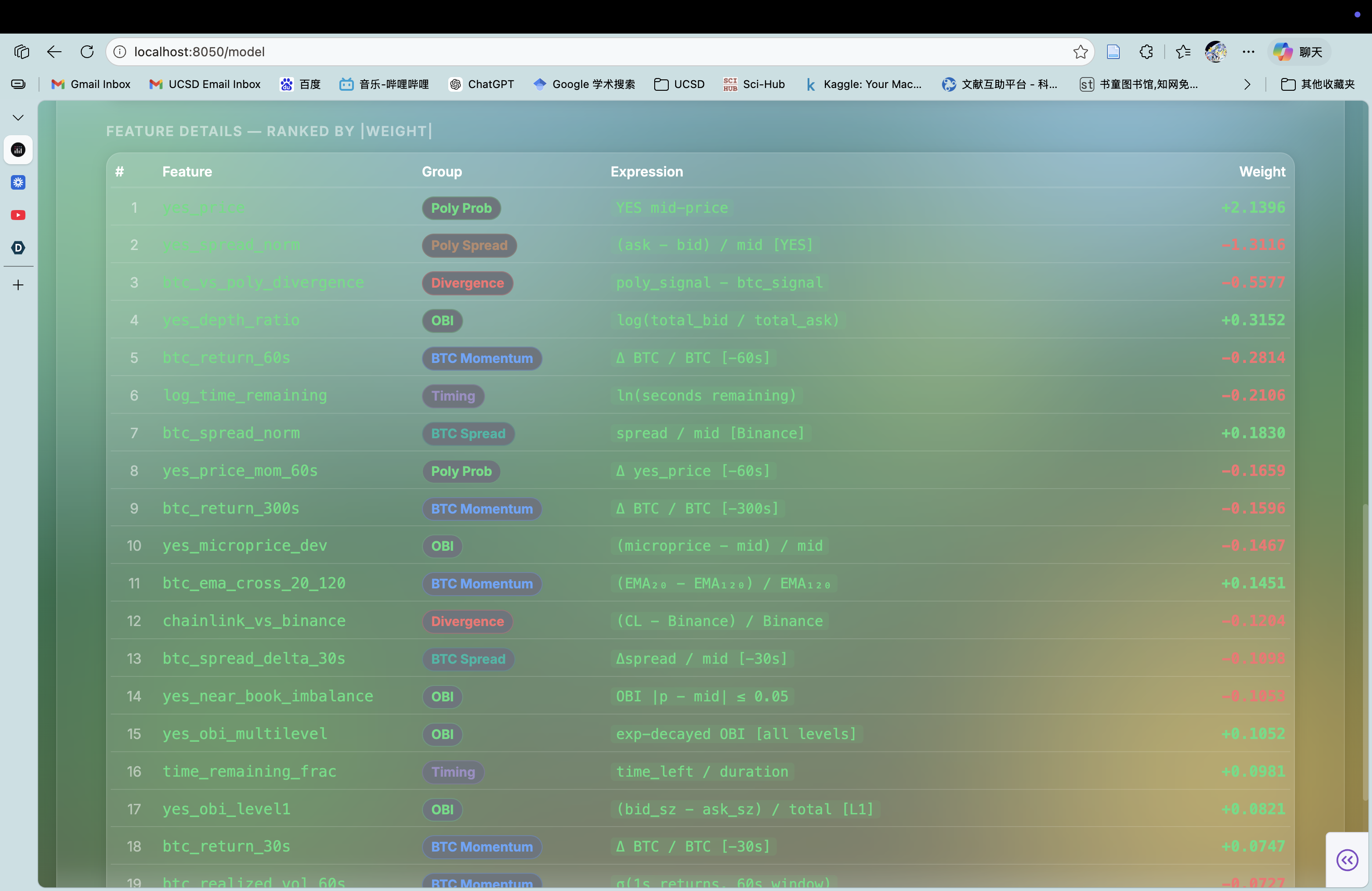

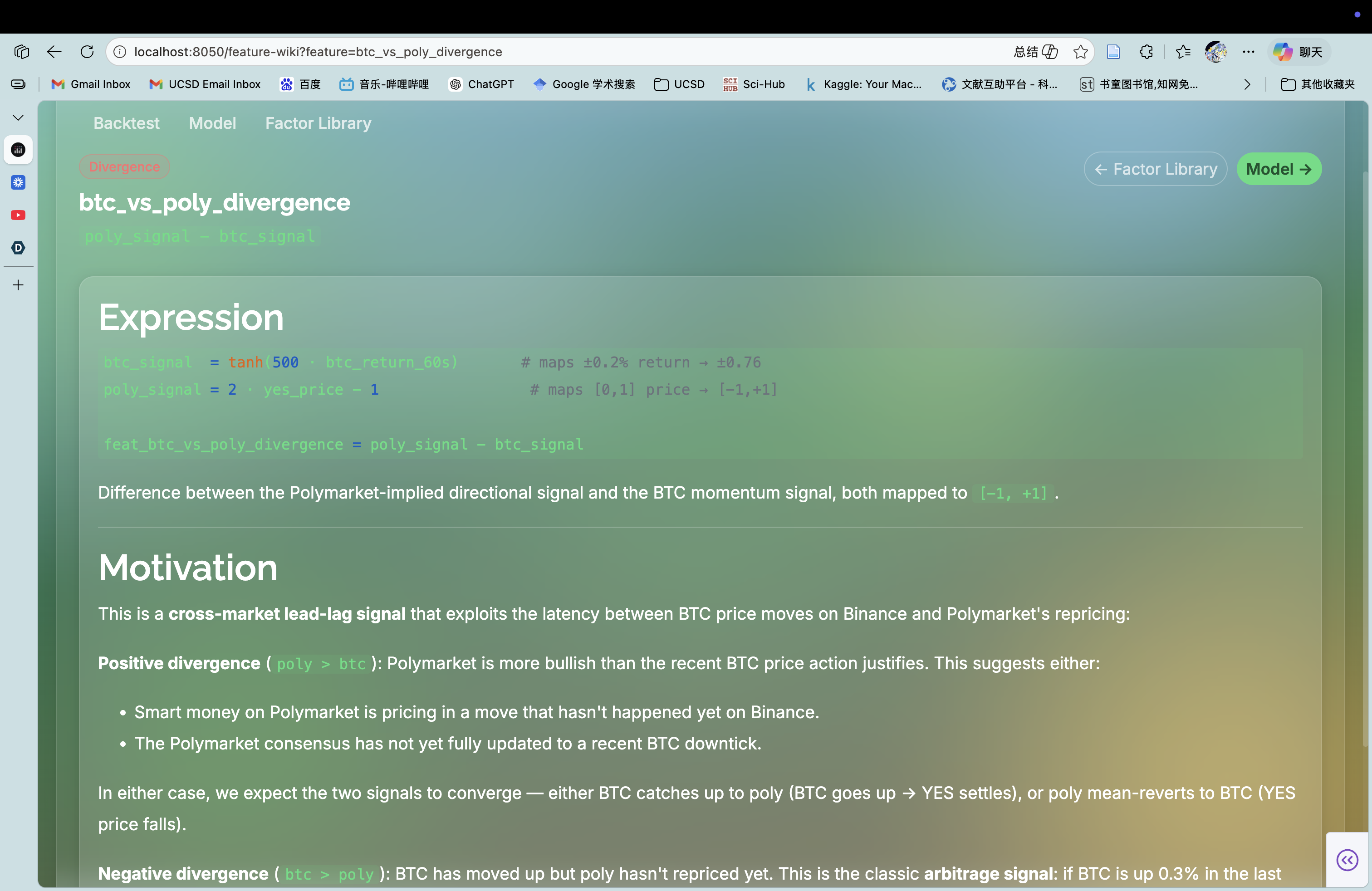

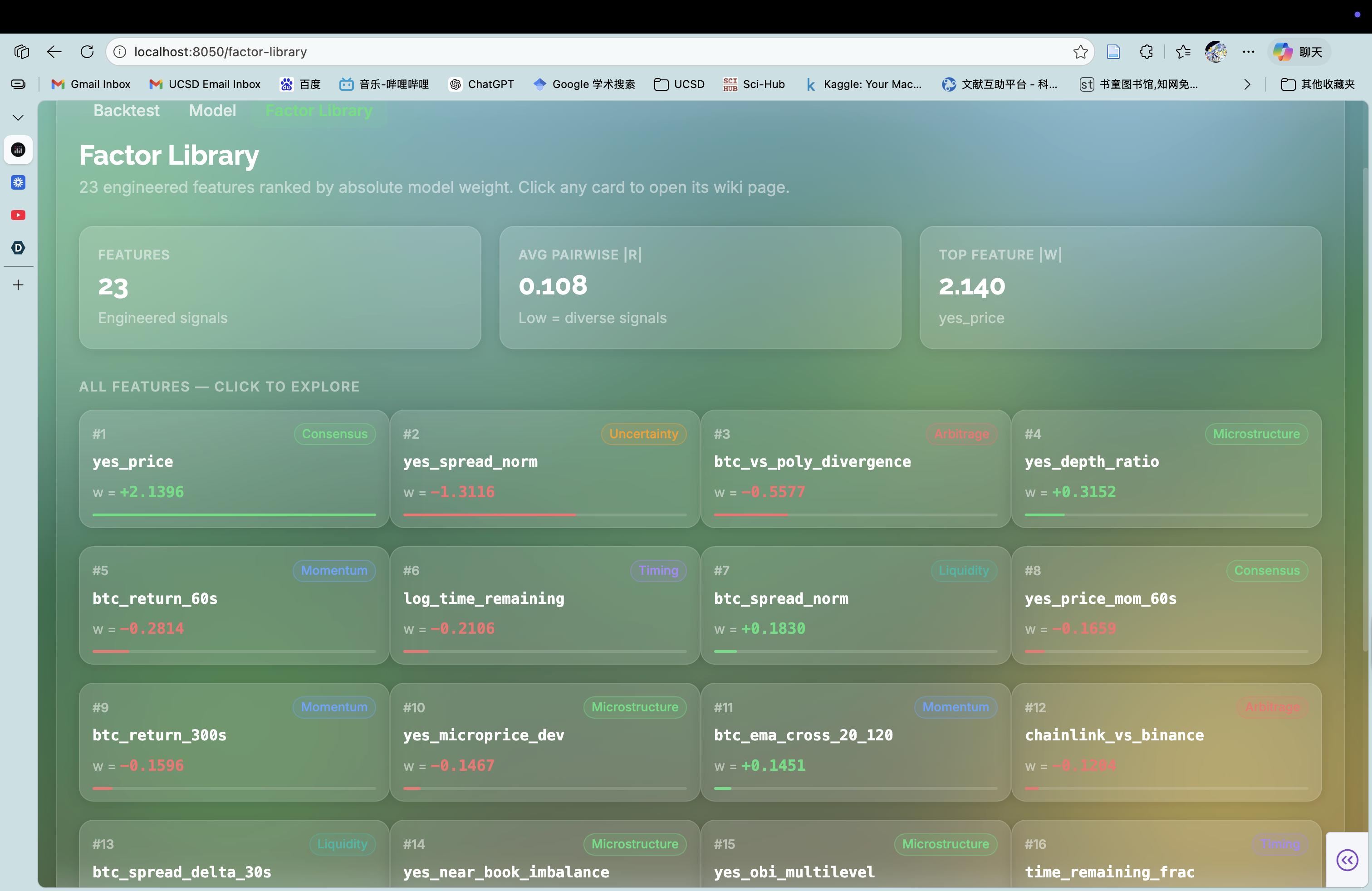

- Factor group: utilizes knowledge about Bitcoin market's microstructure, to construct predictive features of the future price of Bitcoin, as well as its direction of movement

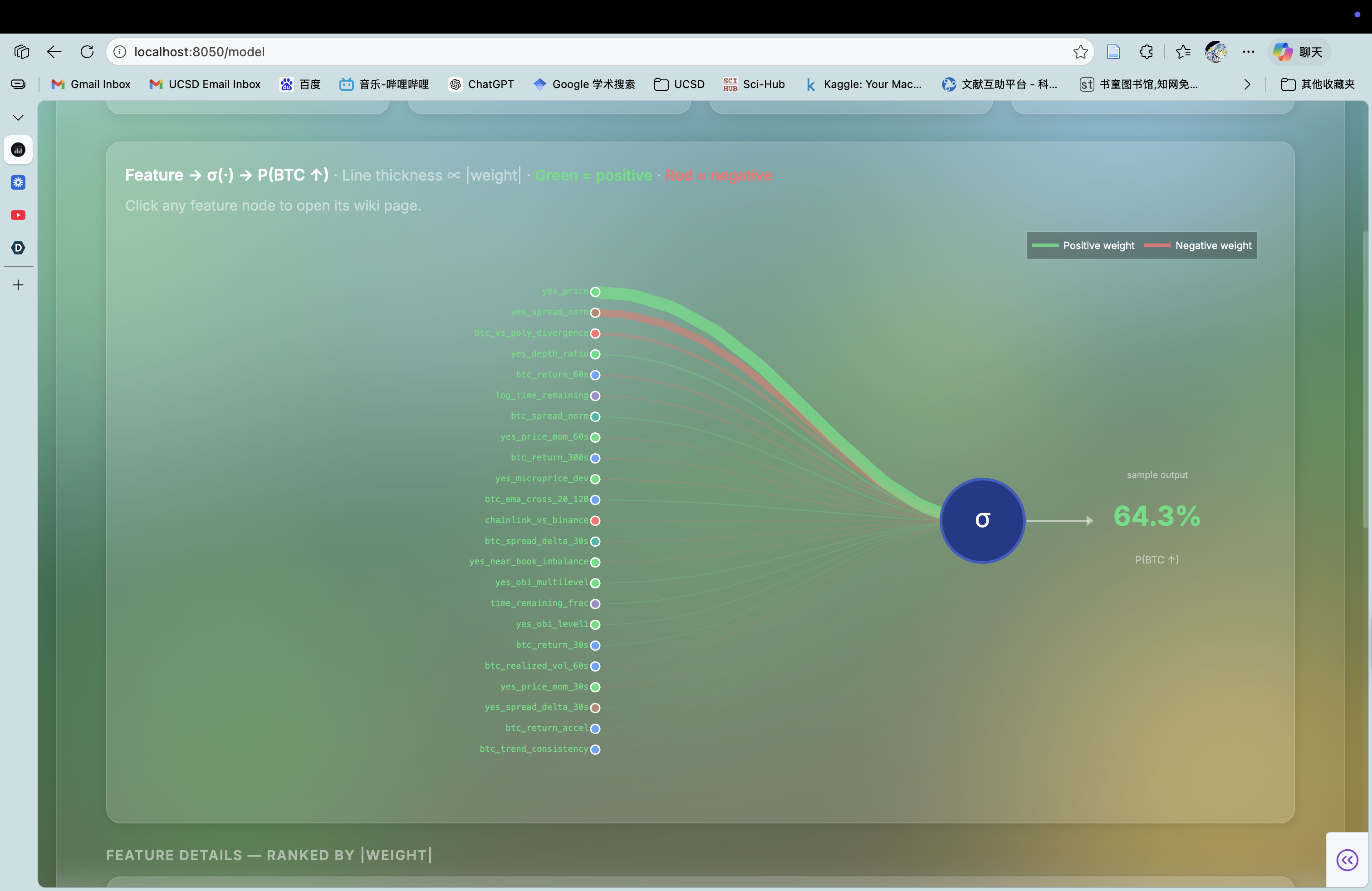

- Model group: research different model architectures that can combine the individual signals from different features, and produce a comprehensive signal that can generate alpha

What it does

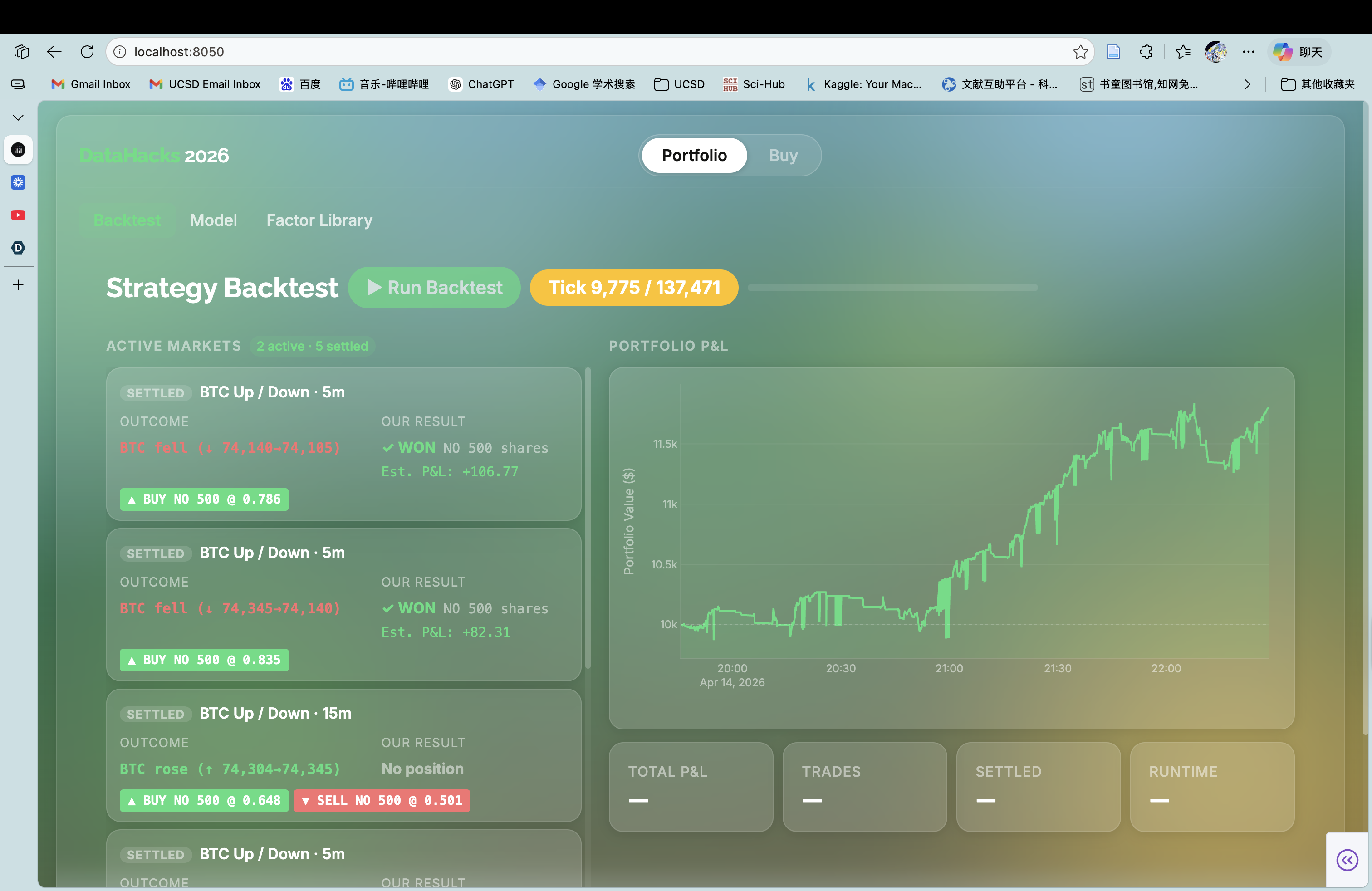

At each time tick, we

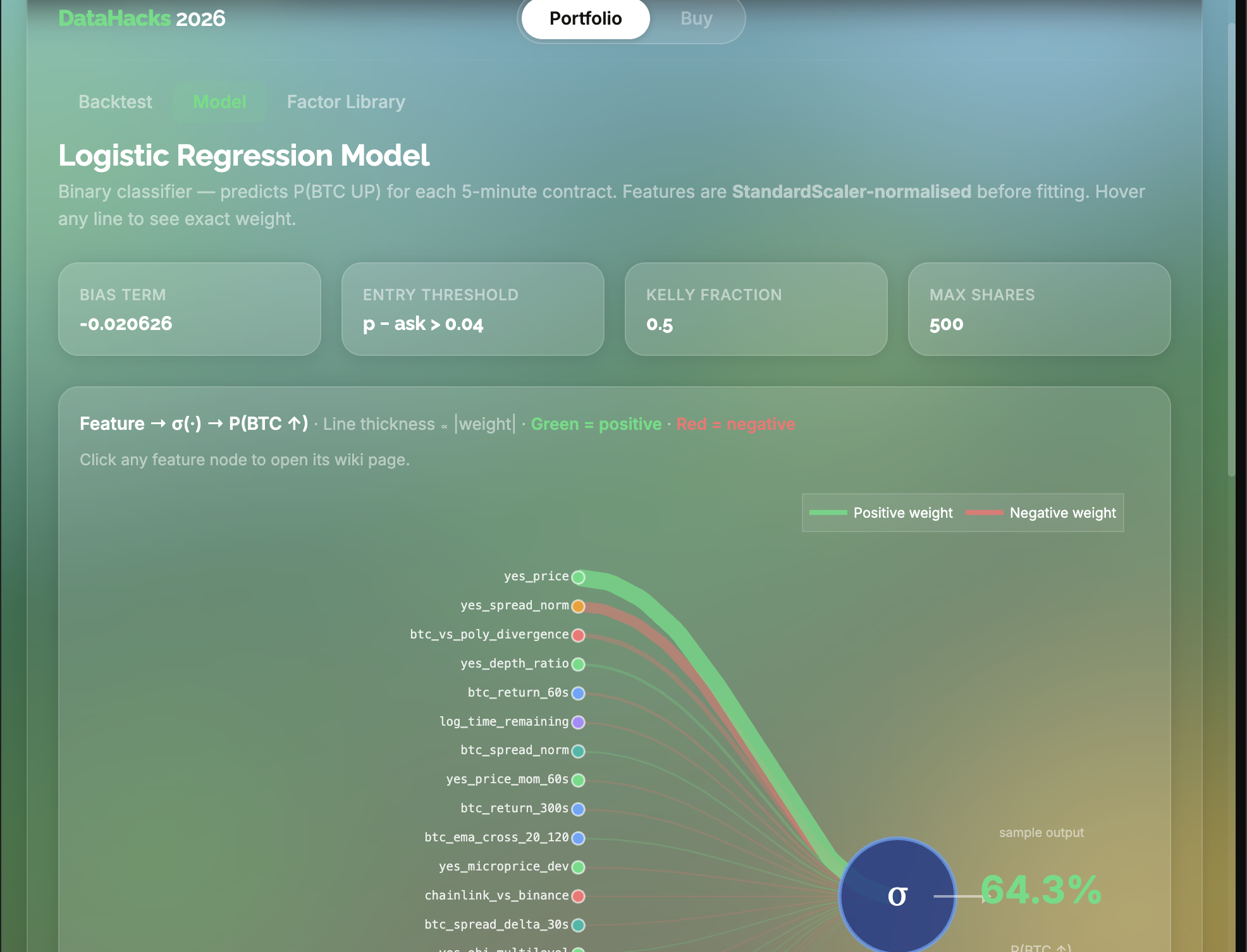

- Use accumulated historical data to estimate probability of Bitcoin price going up

- Compare our estimation with implied probability of current market

- Execute orders based on half Kelly criterion + considering trading slipperage

Accomplishments that we're proud of

We've constructed a model that achieves 100%+ performance during backtest using validation data. However, we've dropped this model because of its over-reliance on the polymarket_yes_price, which makes it non-robust since its prediction doesn't primarily utilize information from the real Bitcoin market, but only the Polymarket prediction market.

What we learned

Decorrelation between factors are important, since otherwise a single underlying signal can have over-influence on the prediction.

What's next for Seeking Alpha

We are planning to implement this system in real life. We've looked into APIs to get real-time order book data from Polymarket and to submit orders.

- We anticipate challenges surrounding latency, execution, and slipperage, but we are confident we can solve them and tackle forward

He")

Log in or sign up for Devpost to join the conversation.