-

-

Awards

-

Digital onboarding for the e-consent

-

Home screen, e-consents

-

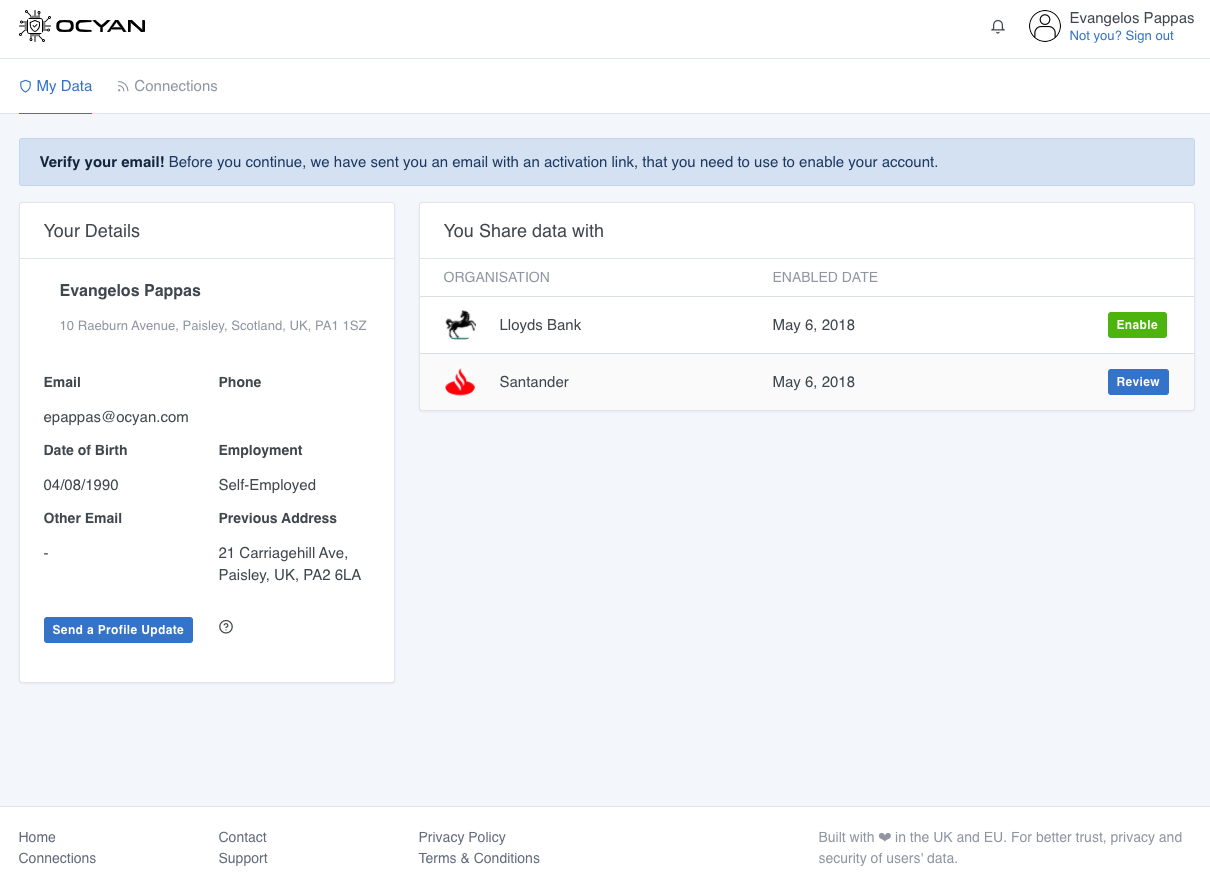

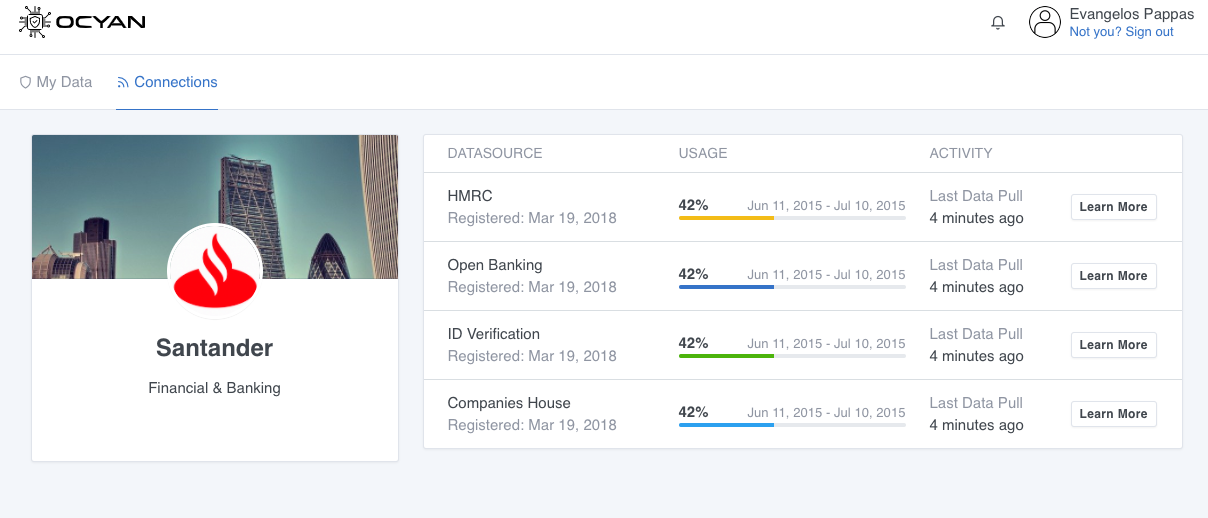

User's visibility on what data a lender uses to make a decision

-

User Journey

-

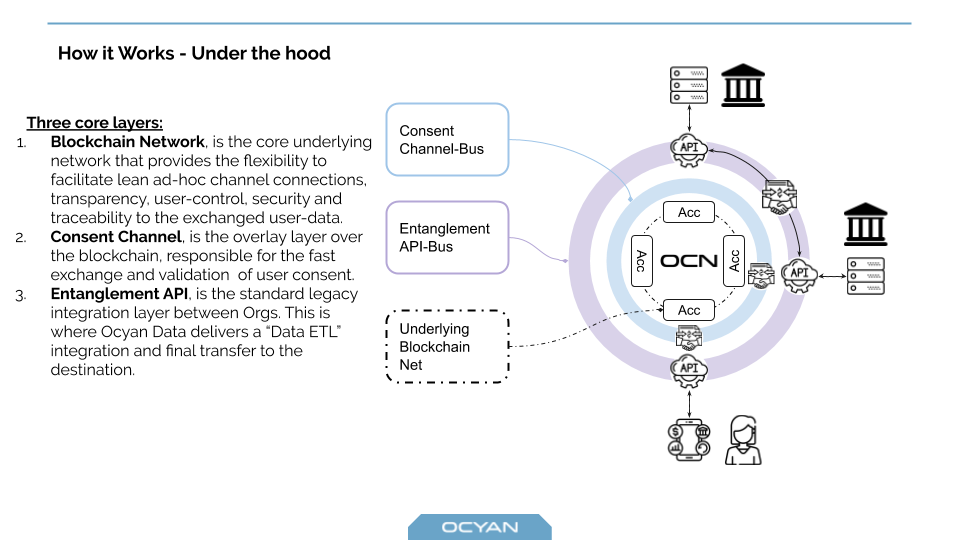

High-level Architecture

-

Solution overview

-

-

-

Inspiration

Being a team of expats, we have lived first-hand all the struggle to access credit, insurance, utility contracts and even more in the beginning of our new adventures. Let's imagine a persona that represents this segment, called Alice.

Alice is an expat from Spain, and has just moved to the UK. She's now working as a contractor for a large enterprise, earning a high-net salary.

Even though Alice has been a good person whilst living in Spain, and in the UK has a very decent amount of earnings, she's still being ranked poorly by credit bureaus and the rest of the financial ecosystem.

Alice is a user that the financial industry can’t capitalise:

- Credit Bureaus

- Marketplaces

- Lenders, Insurances, Utility providers

Even though Alice would have been a potentially great customer, for the financial ecosystem she is invisible. Unfortunately Alice, doesn’t have any visibility or ownership over her own data to know this, and the Financial enterprises neither have enough data aout Alice to make a fair decision about her.

What it does

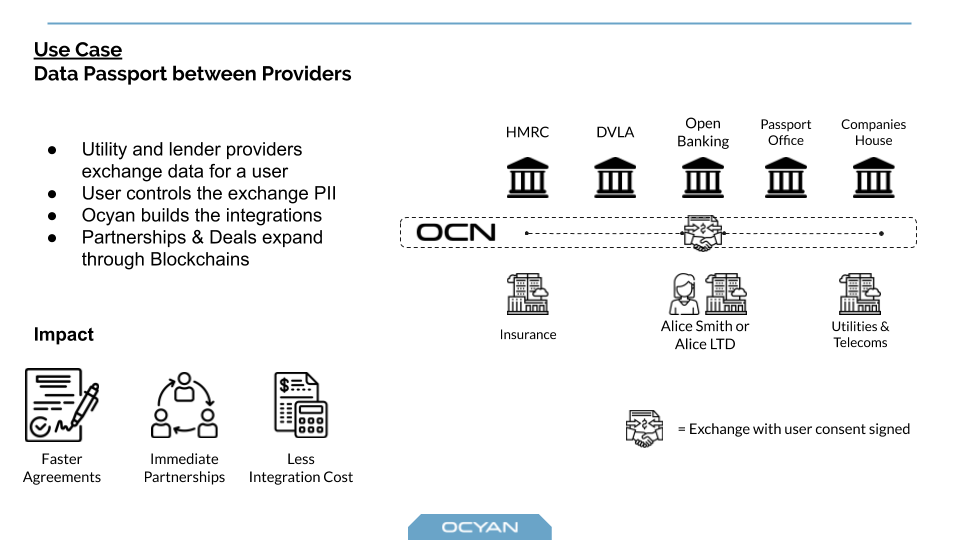

We are willing to build a comprehensive data vault for consumers, where they can connect data holders (e.g. credit bureaus, KYC companies, HMRC and Company House, Open Banking) and data consumers (e.g. lenders, insurers) in order to have better access to credit and bill’s tariffs with their explicit consent.

Data consumers need more comprehensive and accurate data about borrowing candidates from several sources. The current point-to-point solutions that create secure integrations for data exchange between partners are too costly.

Ocyan Data is a data platform, that deploys secure and trusted data connections (aka networks) between multiple parties and systems, to exchange valuable information in a compliant, trusted and resilient manner.

Why is Ocyan Data Relevant to EUvsVirus?

The main driver that is causing an economic meltdown globally and eminently to the EU, is the lack of data to make risk & compliance decisions. This is mainly based on how the legacy financial ecosystems work, they based in credit & data bureaus that are collecting data retrospectively and indirectly from the user's input.

This has been working good enough so far, but since the COVID-19 events, no one has a one-to-one interaction with the end-user on how they have been affected by the global situations.

As a result, the whole, credit, bonds, insurances and trading activity has been halted, as we don't have enough data to make fair decision for the users.

Ocyan solves this dead-end-paradox, by integrating the end-user as an active stakeholder and partner within the legacy financial settlement. Making it possible for the end user to view her data, and choose to enrich it with more data sources and real time representation of her status. Making it possible for the data consumers to make a fair and accurate decision for her profile.

Three (3) Pillars of Value

- Credit Bureaus and lenders can capitalise on a market segmentation that was invisible to them

- Credit Lenders, insurances and Telecom providers receive more qualified & holistic data to make a better & fair decision for a user through a single & lean integration

- The user receives a direct channel to notify the lenders for status updates through a single app.

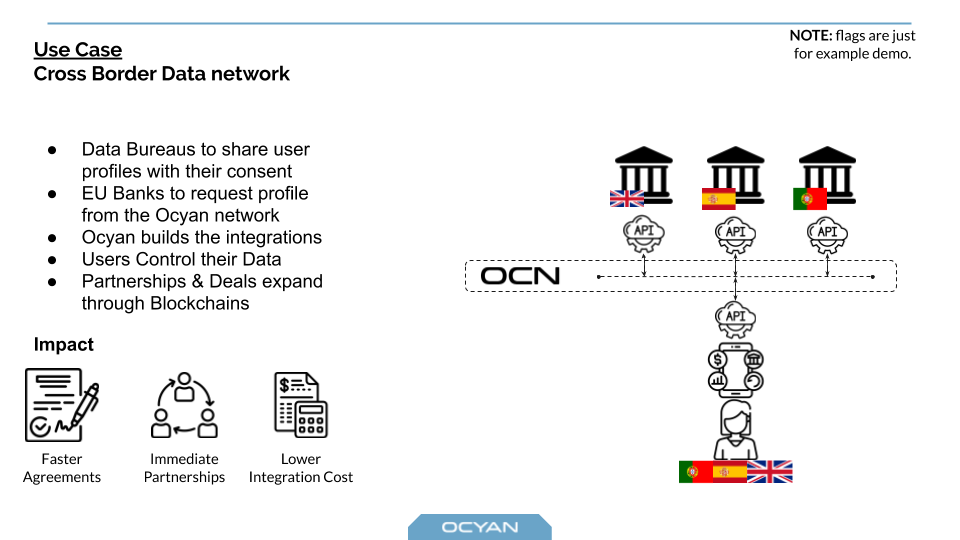

How can EU use Ocyan-Data?

Our design and decision making ha been focused and centred along side the EU ecosystem. A solution like Ocyan Data can bring an immediate first step for a pan-european "open banking" alternative for the User data, being able to operate over EU's blockchain ecosystem (EBSI).

The value of Ocyan Data after the crisis

The need for more accurate and fair data is not caused by COVID-19, but it has become eminent because of it. The EU has on its core the "free citizen movement" between their member-states, but yet for individuals to receive access to many services between countries it still feels so much alienated.

By providing the option to the users to bring their own data, we aim to solve much of this pain, and be the first step for a more pan-european integrated society.

How we built it

The platform is a mix of cutting edge technologies including the following ones:

- AWS serverless services (SQS, Cognito, SNS, SES, Lambda, DynamoDB, S3, Cloudfront)

- Blockchain (Hyperledger Fabric) & Chain Code

- Kubernetes

- ReactJS

Three core layers

- Blockchain Network, is the core underlying network that provides the flexibility to facilitate lean ad-hoc channel connections, transparency, user-control, security and traceability to the exchanged user-data.

- Consent Channel, is the overlay layer over the blockchain, responsible for the fast exchange and validation of user consent.

- Entanglement API, is the standard legacy integration layer between Orgs. This is where Ocyan Data delivers a “Data ETL” integration and final transfer to the destination.

What we did during the weekend

- Developed the UI (prototype)

- Deployed a private Blockchain (similar to EBSI)

- Developed partially the backend

- Interviews with stakeholders from our targeted accounts (from our network and Slack too)

- Presentation material & Video

Challenges we ran into

B2C target marketing: Near-prime borrowers represent a very substantial segment of the market of all adults potentially looking for credit – somewhere between 20% and 27% of all UK adults.

B2B integrations: Our domain includes Open Banking, Credit Reports, KYC, Government data and additional data sources demand.

Maintain user consent transparently: User consent is stored against transactions, and it represents the only enabler for data exchange.

How we solve the data privacy and GDPR (or similar) issues

The whole initiation of the process is expected to start when lenders, insurances and utility providers are being KYCing their customer. So through Ocyan no-one has physically more control & visibility of user's data than the user herself. The end-to-end connections are being controlled via the user through a blockchain-based digital consent.

Accomplishments that we're proud of

We have been awarded and mentioned by several important journals, plus we are happy to work and collaborate with Telefonica, our main investor and partner. See image attached.

- High skilled team within the domain industry

- awards & press releases

- collaborations with tier-1 corporates

- a product that solves our need first, and then to many other users

What we learned

We are still discovering a lot in the financial space, and we are extremely happy to understand that we can easily migrate this platform to work in other fields like insurance, utilities, healthcare and so on.

- Integrating a blockchain proposition to the enterprise production

- The market of credit lending, how they can handle the enrichment of more data

- The same data need is shared by telcos, insurance and credit industries

- BD strategies to launch a B2B2C product

What's next for Ocyan Data

Our next step would be to bring the user closer to the data producers, in order to facilitate collection and distribution of their data in real time. This should drive to a better and fairer market for every of us.

The necessities in order to continue the project

- Business & commercialisation mentorship to optimise our billing structure to something that would work for the data consumers

- Legal & Regulatory advice

- Mentorship to reach to a broder EU network

- Mentorship on how we can scale the proposition and expand it further from the UK into the EU

- Develop the project to an alpha version, which will be ready for PoCs, then for Beta that will be ready for user onboarding (4-6 months)

Product Video-Show & Presentation

- Product demo: https://youtu.be/V8PRjz1tBII

- Presentation Deck: https://docs.google.com

Built With

- amazon-ses

- amazon-sns

- amazon-sqs

- amazon-web-services

- blockchain

- cloud

- cognito

- consent

- ebsi

- hyperledger-fabric

- javascript

- kubernetes

- lambda

- python

- react

- saas

- serverless

Log in or sign up for Devpost to join the conversation.