Inspiration

A year ago, our team went through the homebuying process ourselves — and it was brutal. Drowning in paperwork we barely understood, waiting weeks for underwriting decisions, constantly asking "what

happens next?" and never getting a clear answer. We dealt with the jargon ($\text{DTI}$, $\text{LTV}$, $\text{PMI}$), the back-and-forth document requests, and the anxiety of not knowing where our

loan stood. After closing, we looked at each other and said: there has to be a better way. That firsthand pain inspired Nexus Lending — we built the platform we wish we'd had when buying our home.

## What it does

Nexus Lending is an AI-powered mortgage platform that serves both sides of the loan process:

For borrowers:

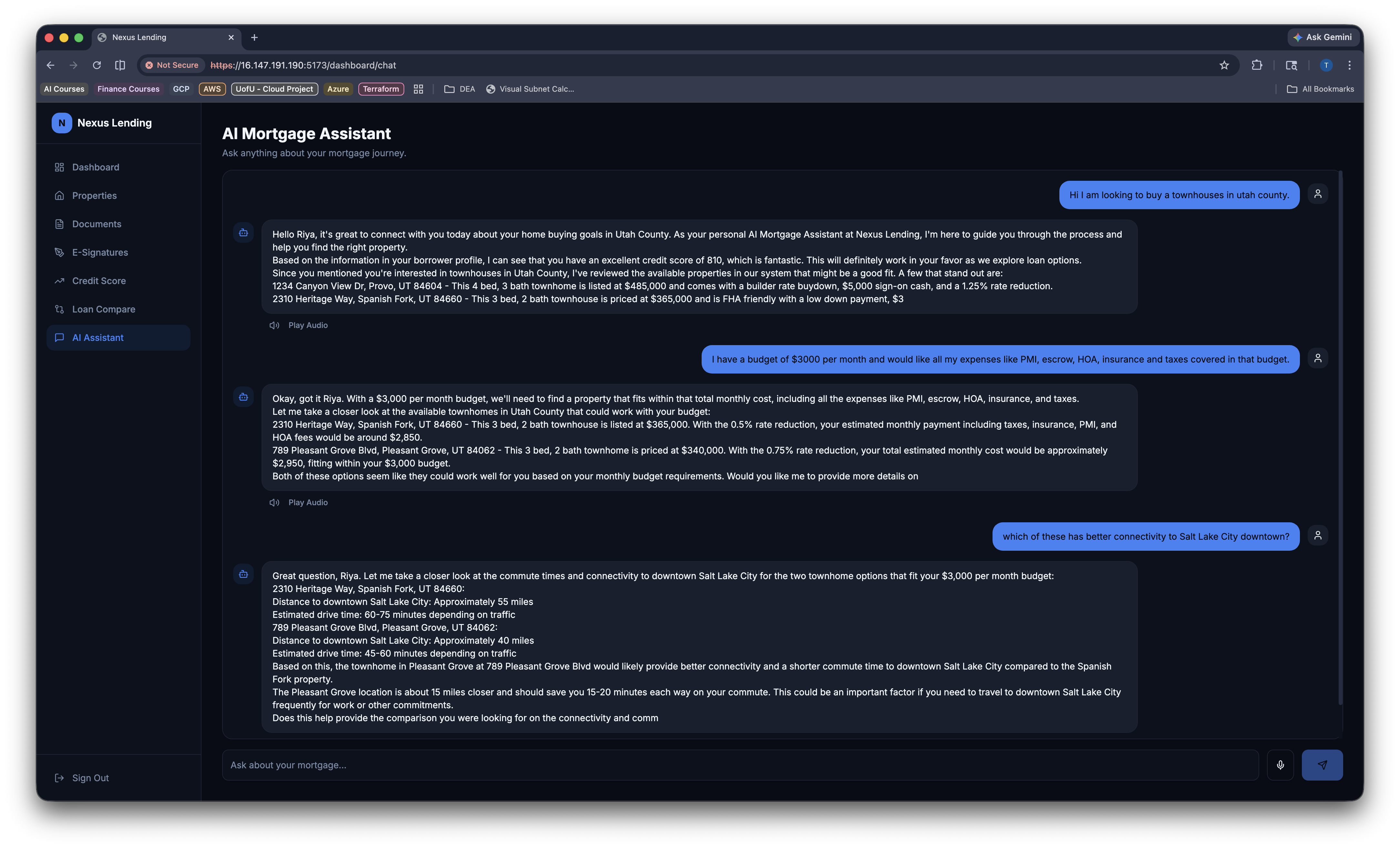

- A 24/7 AI mortgage advisor (chat or voice) that explains complex concepts in plain language

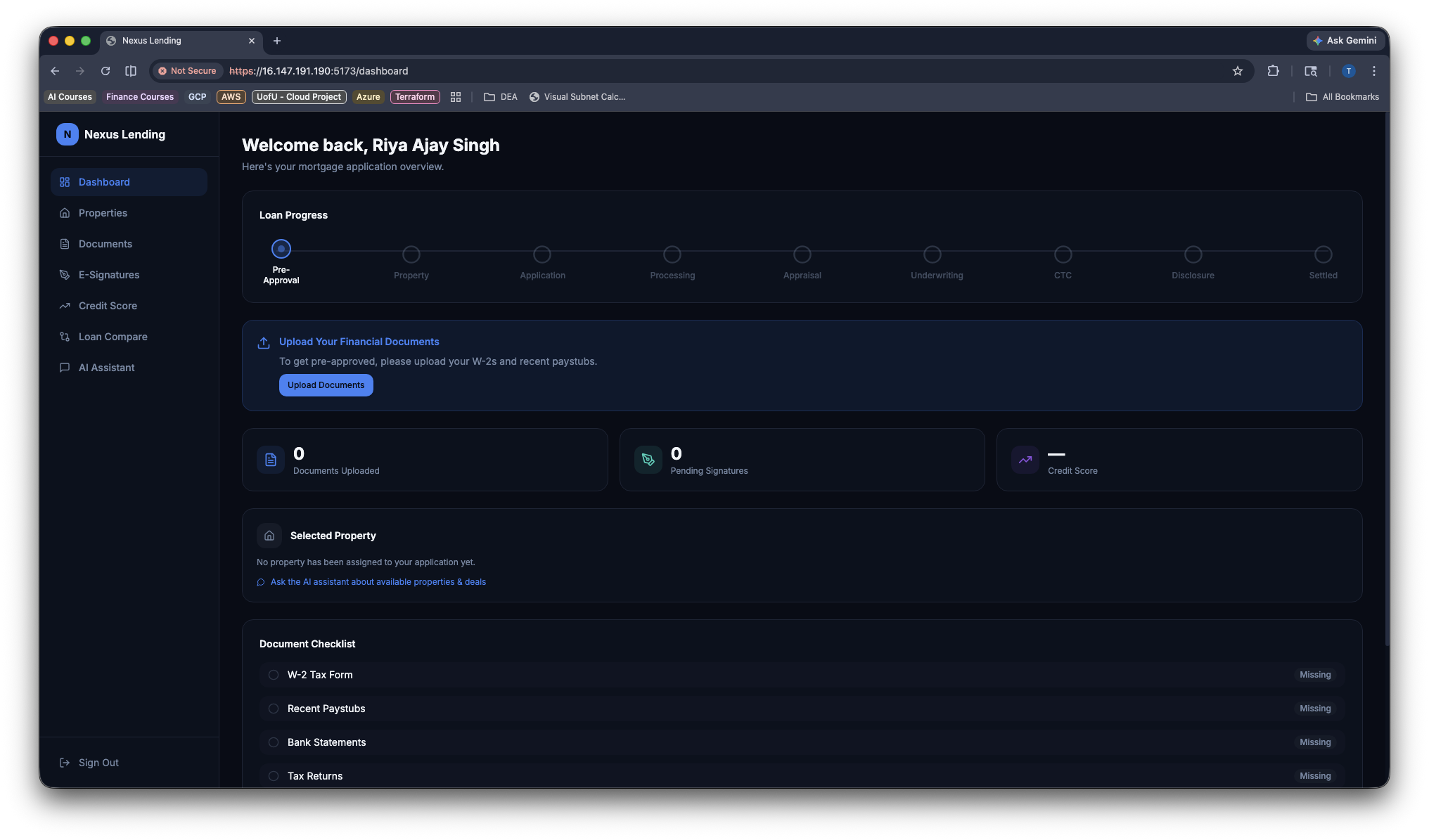

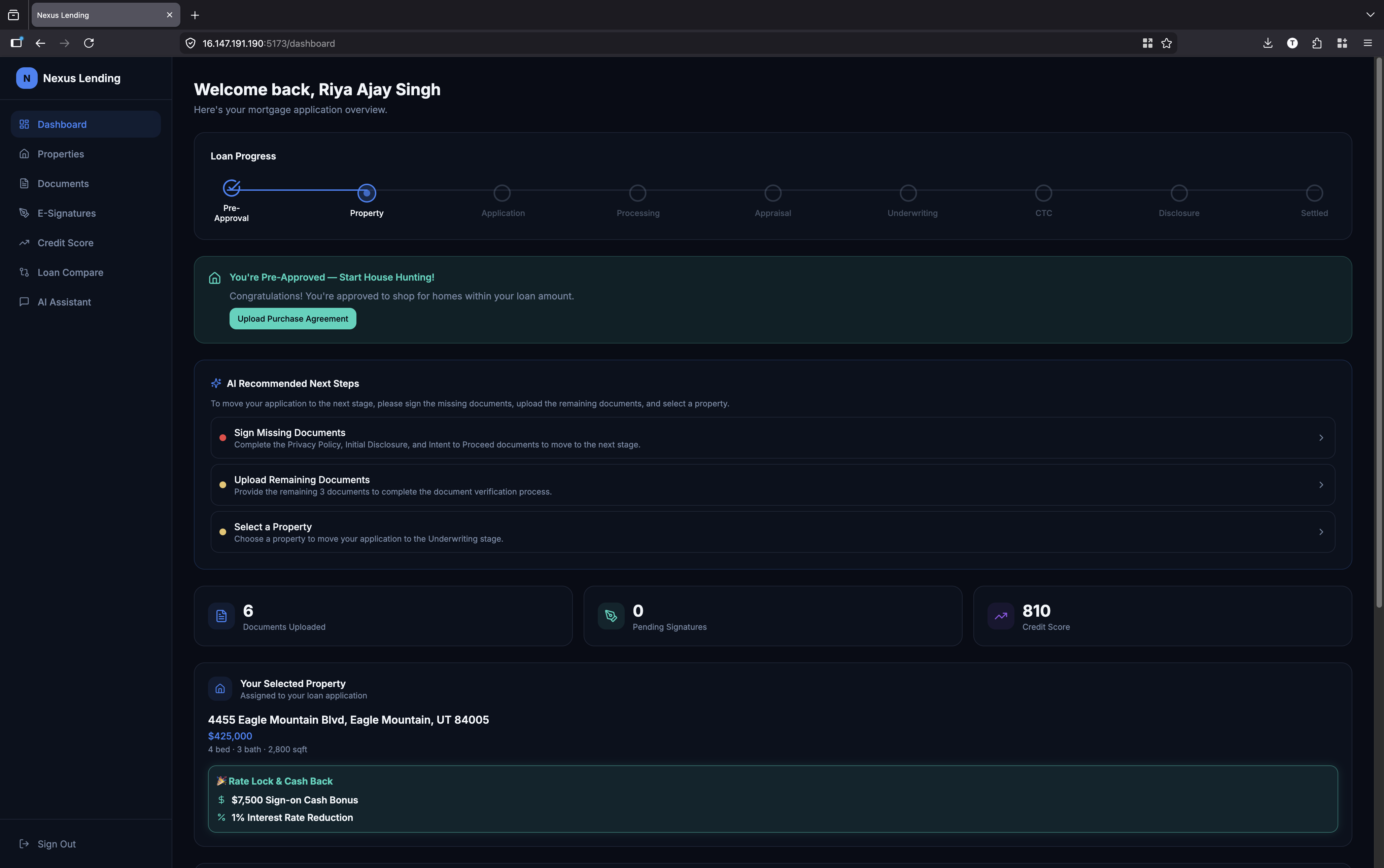

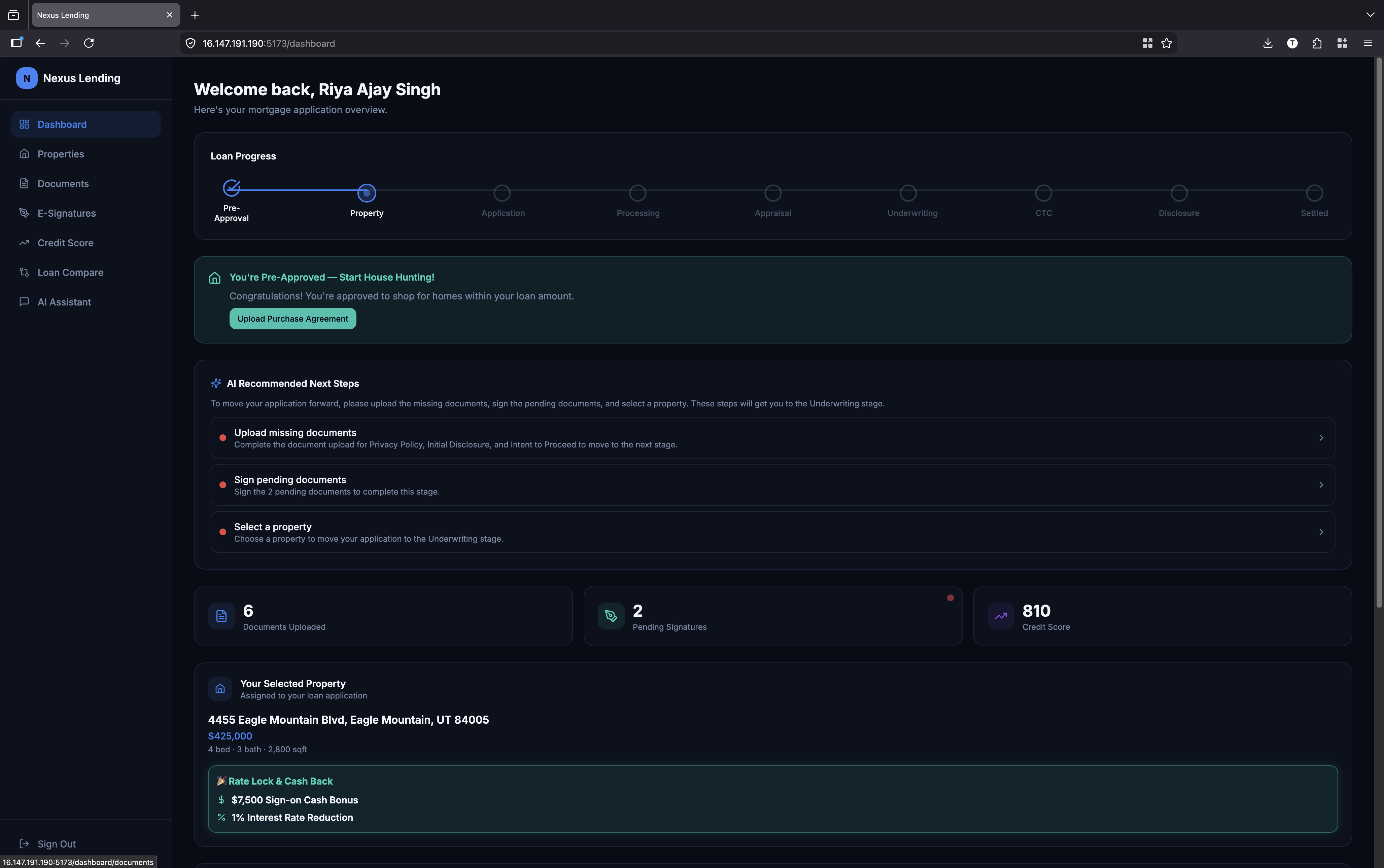

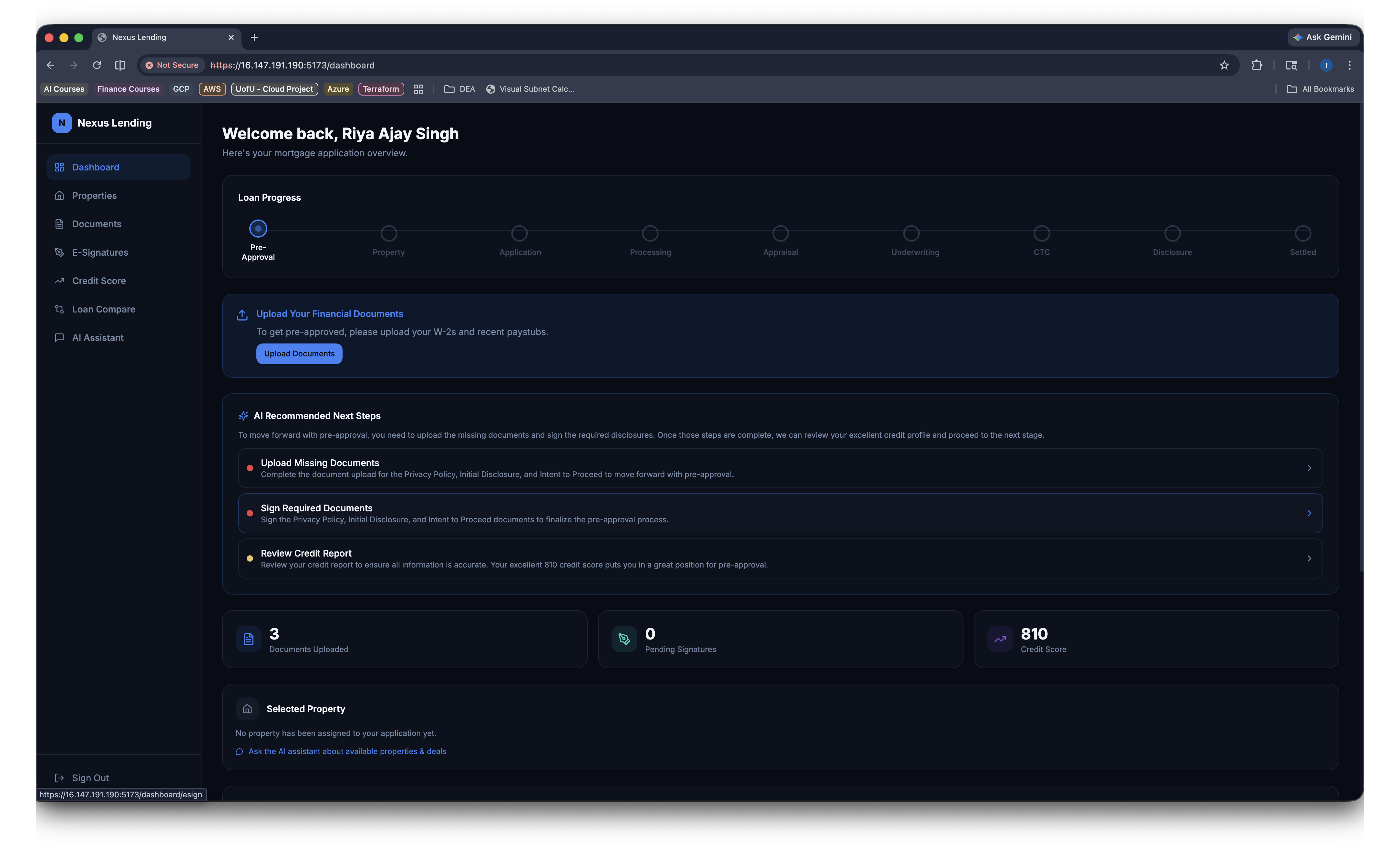

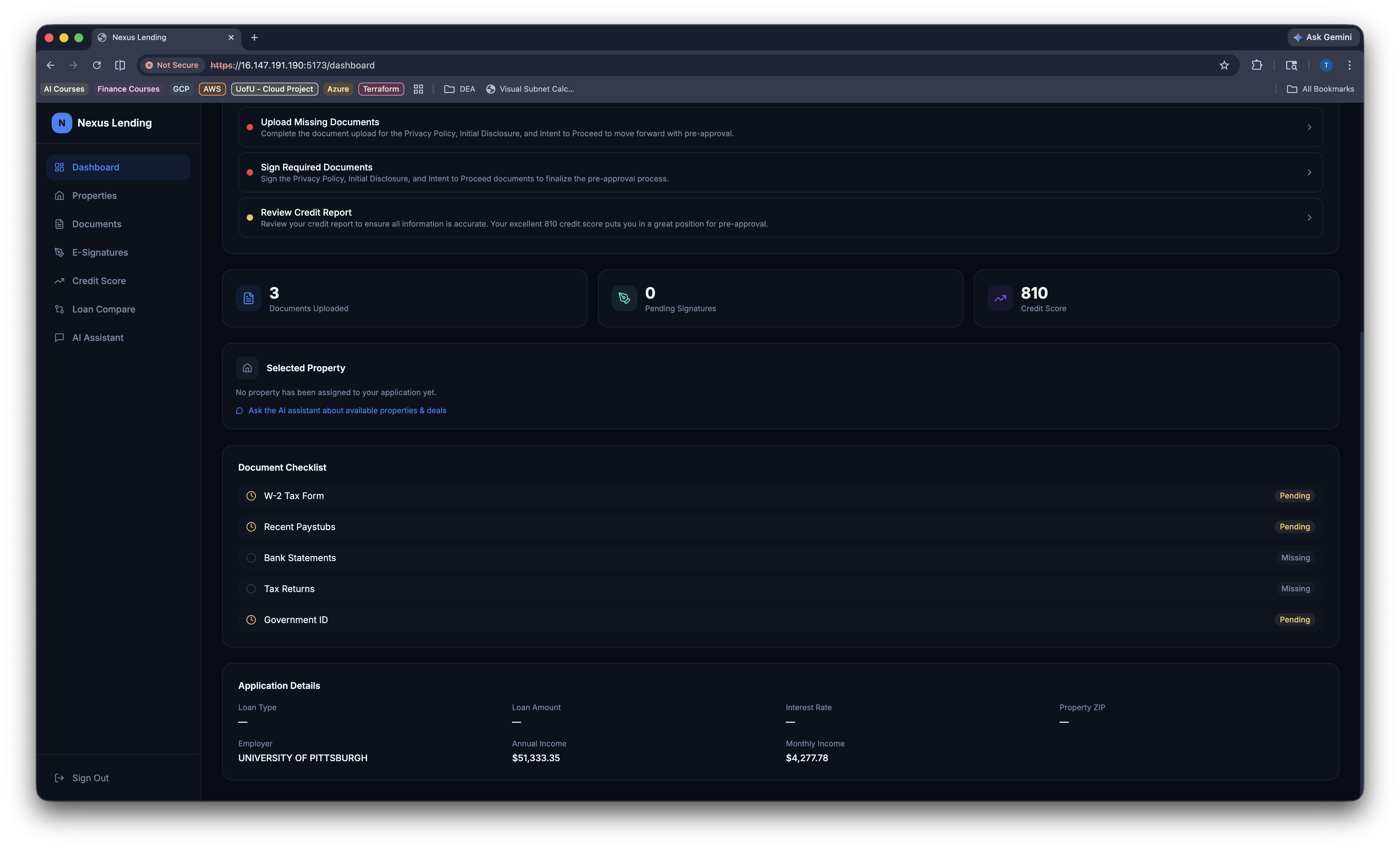

- A visual 9-stage closing timeline so they always know where they stand

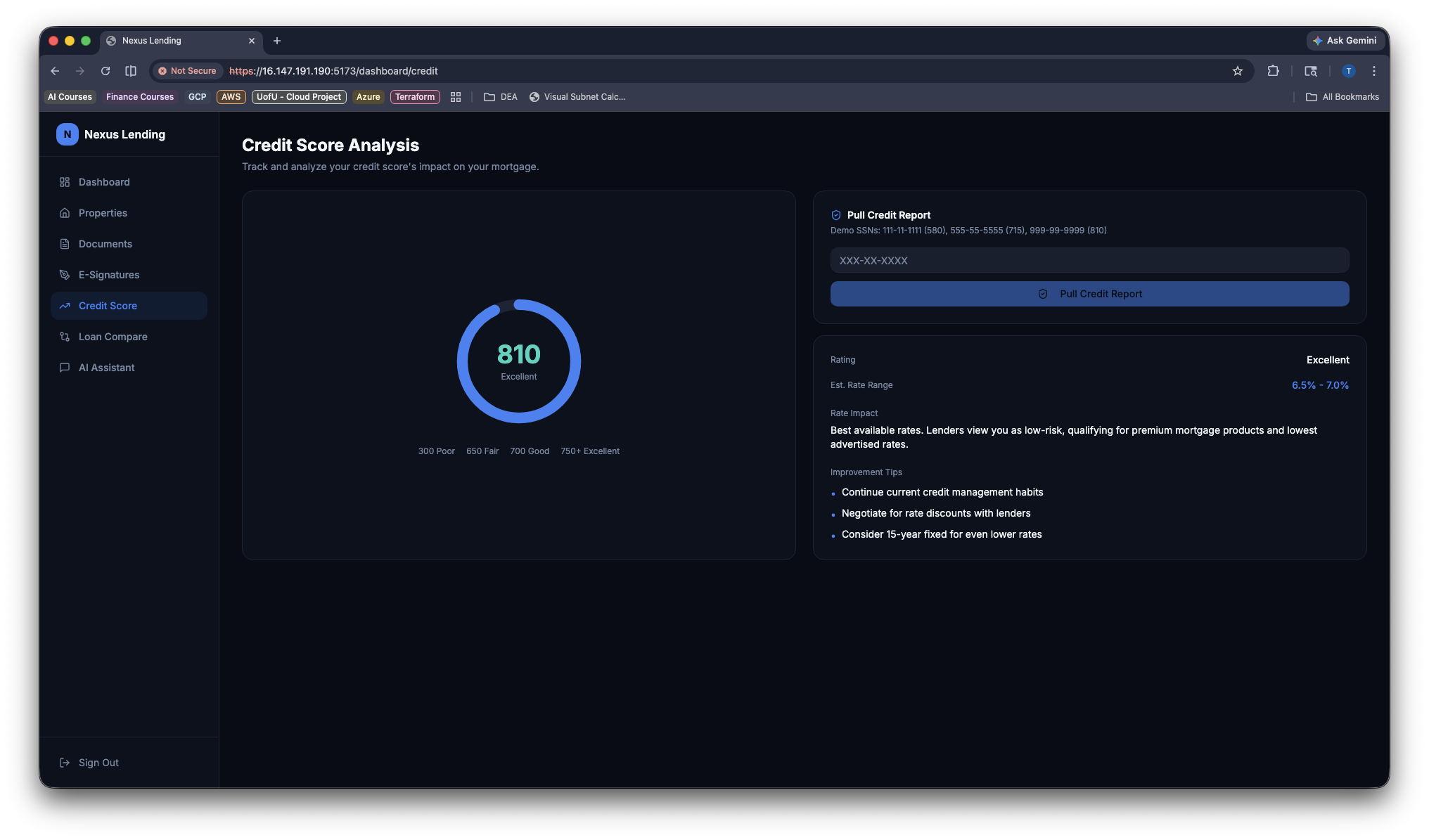

- AI-powered credit analysis with estimated rates and specific improvement tips

- AI-recommended next actions — no more guessing what to do next

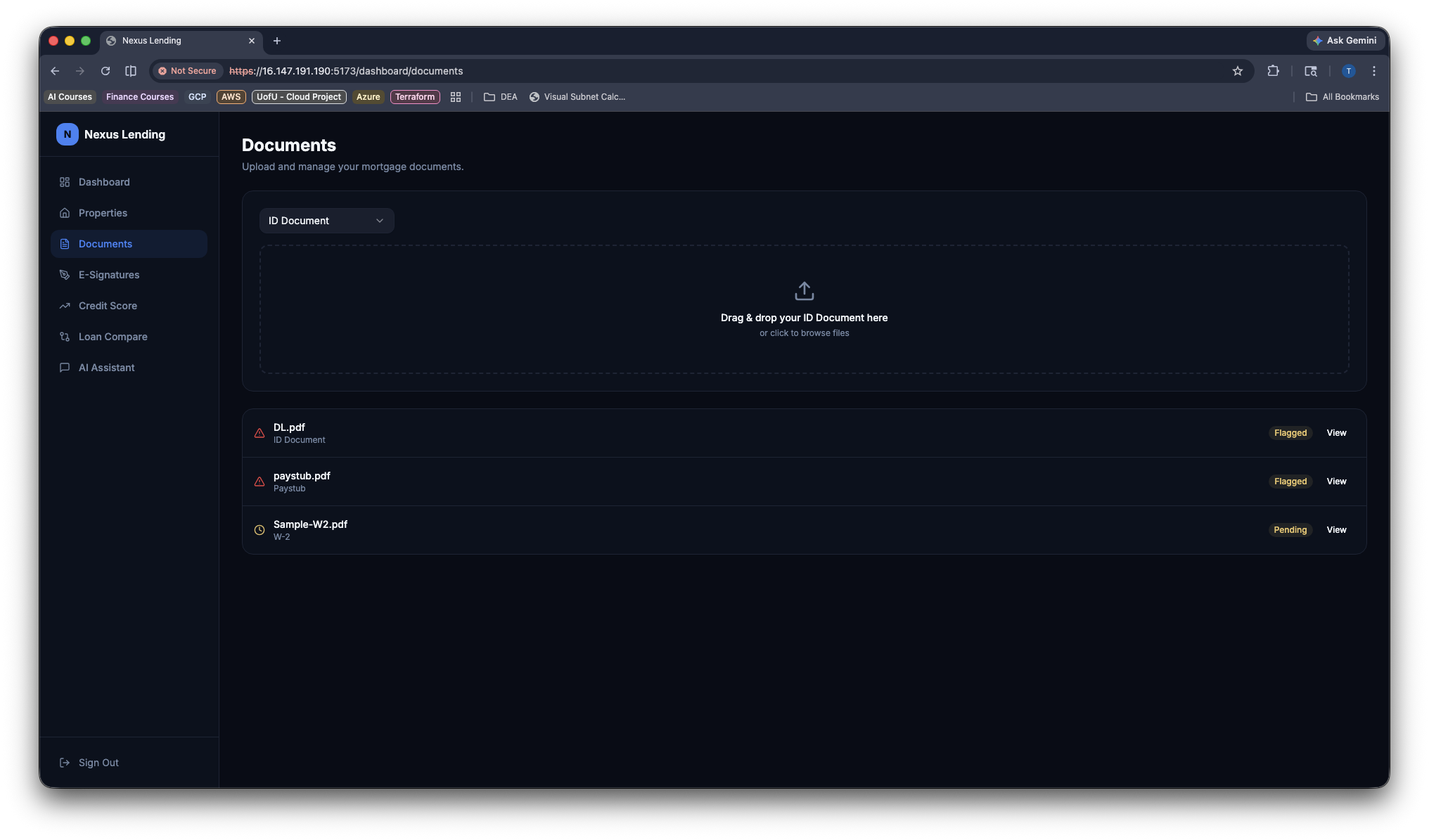

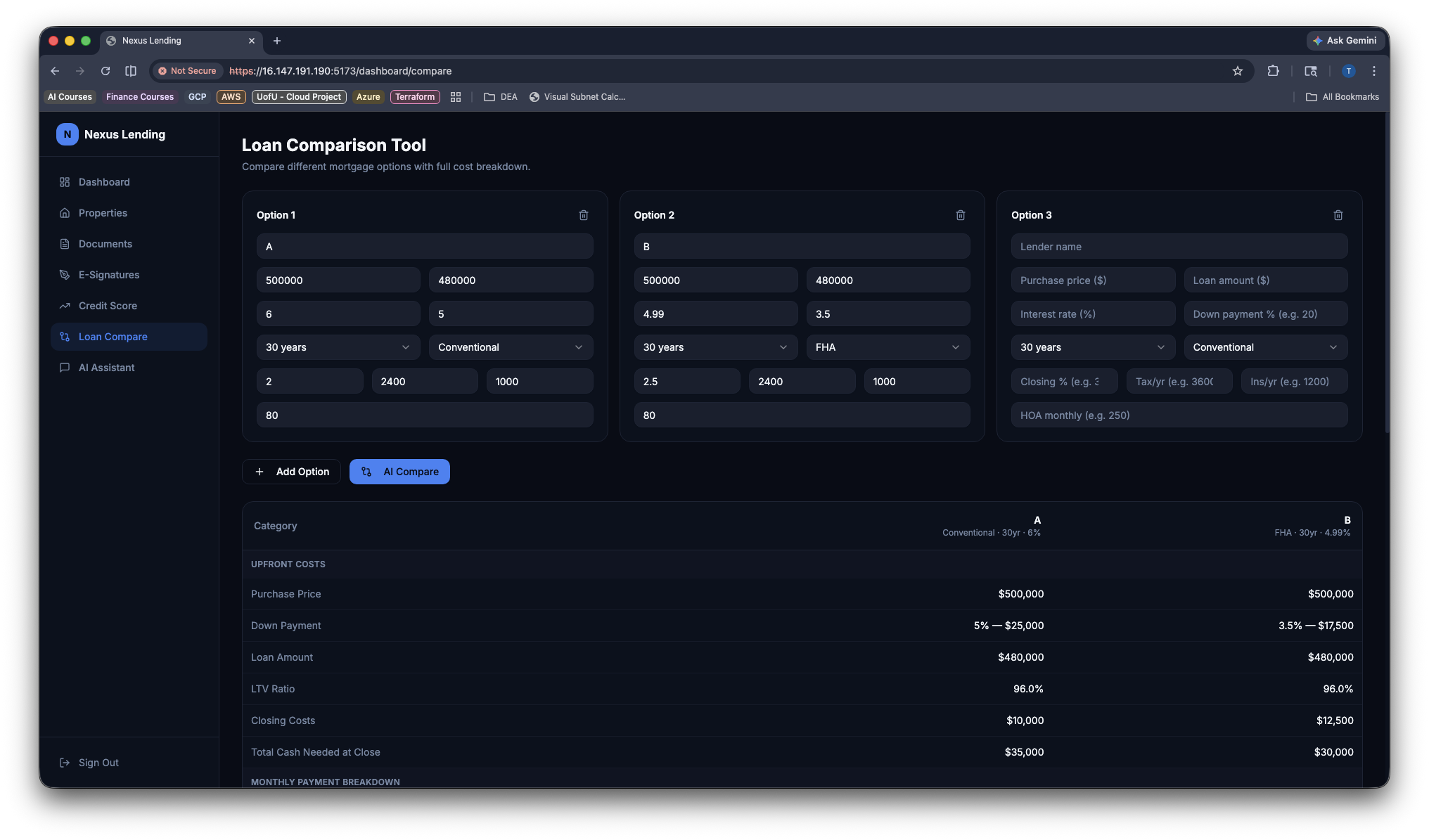

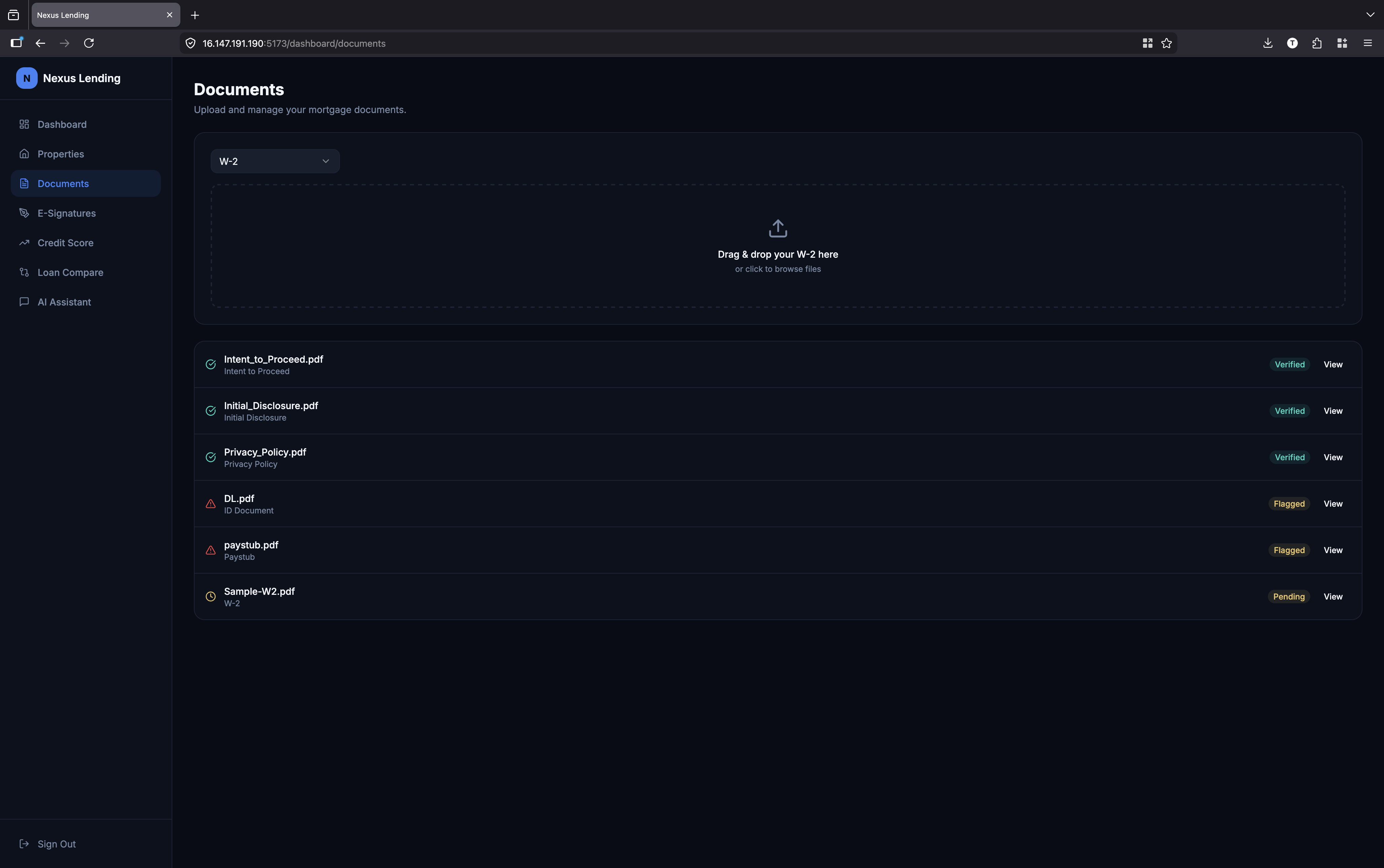

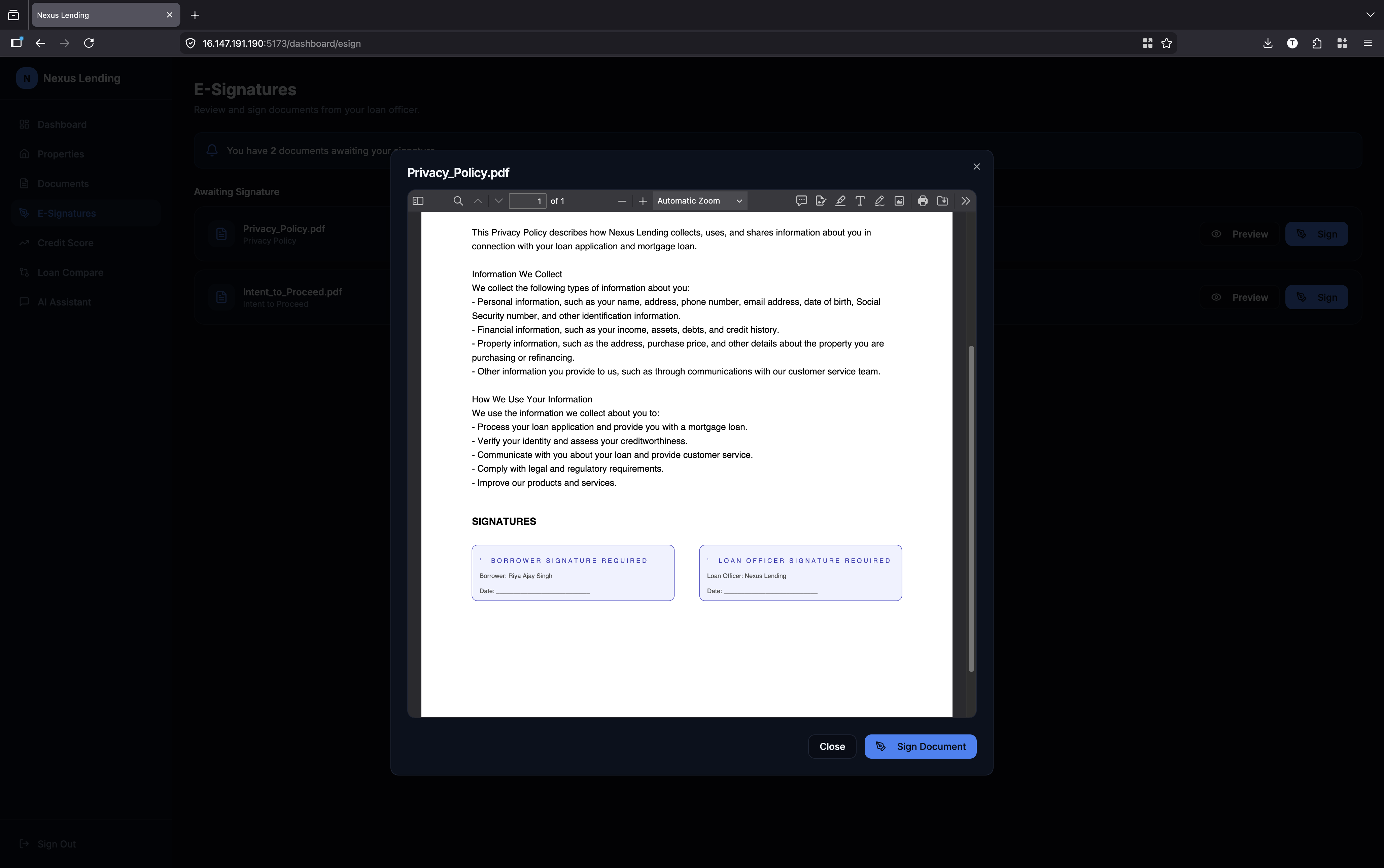

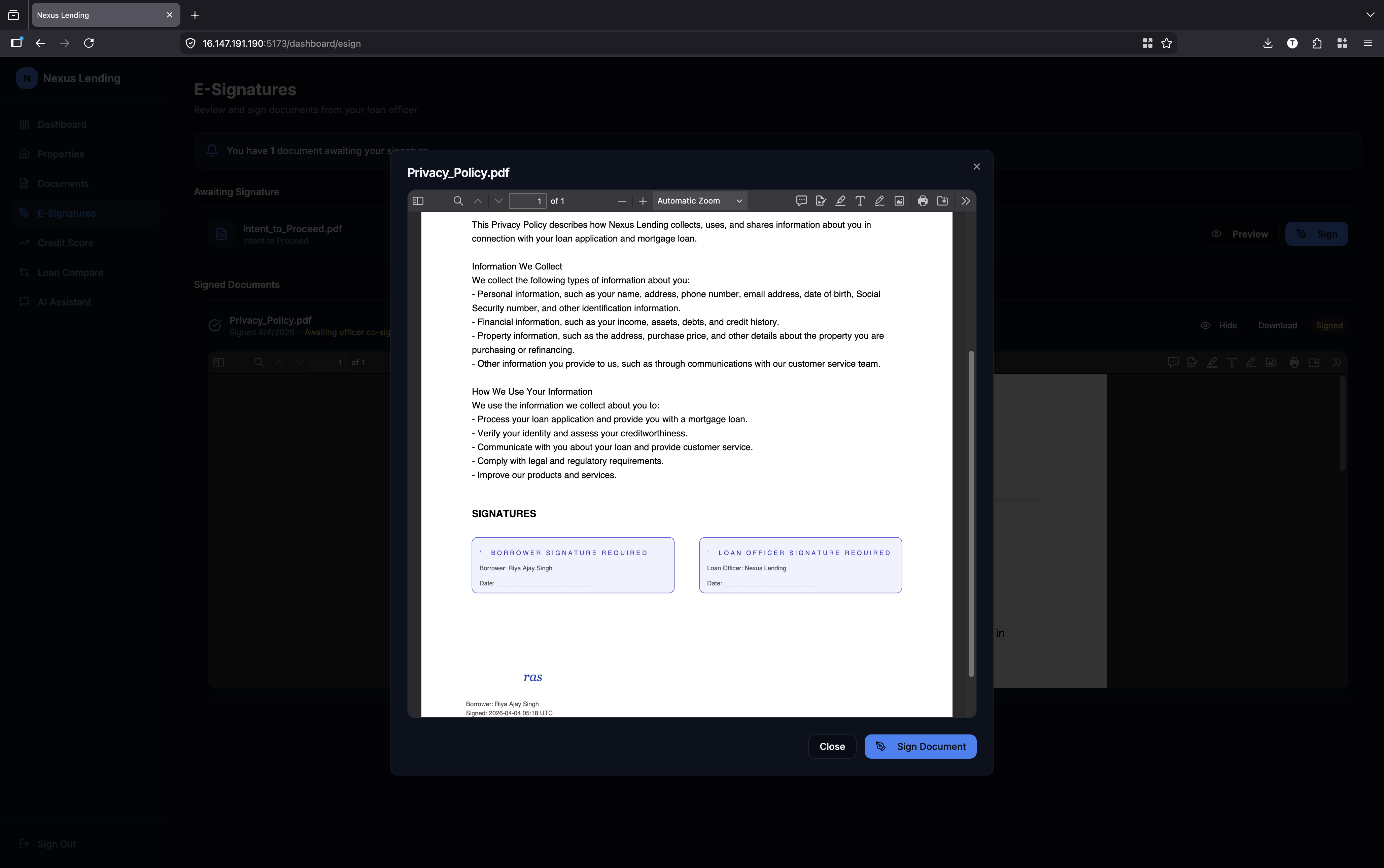

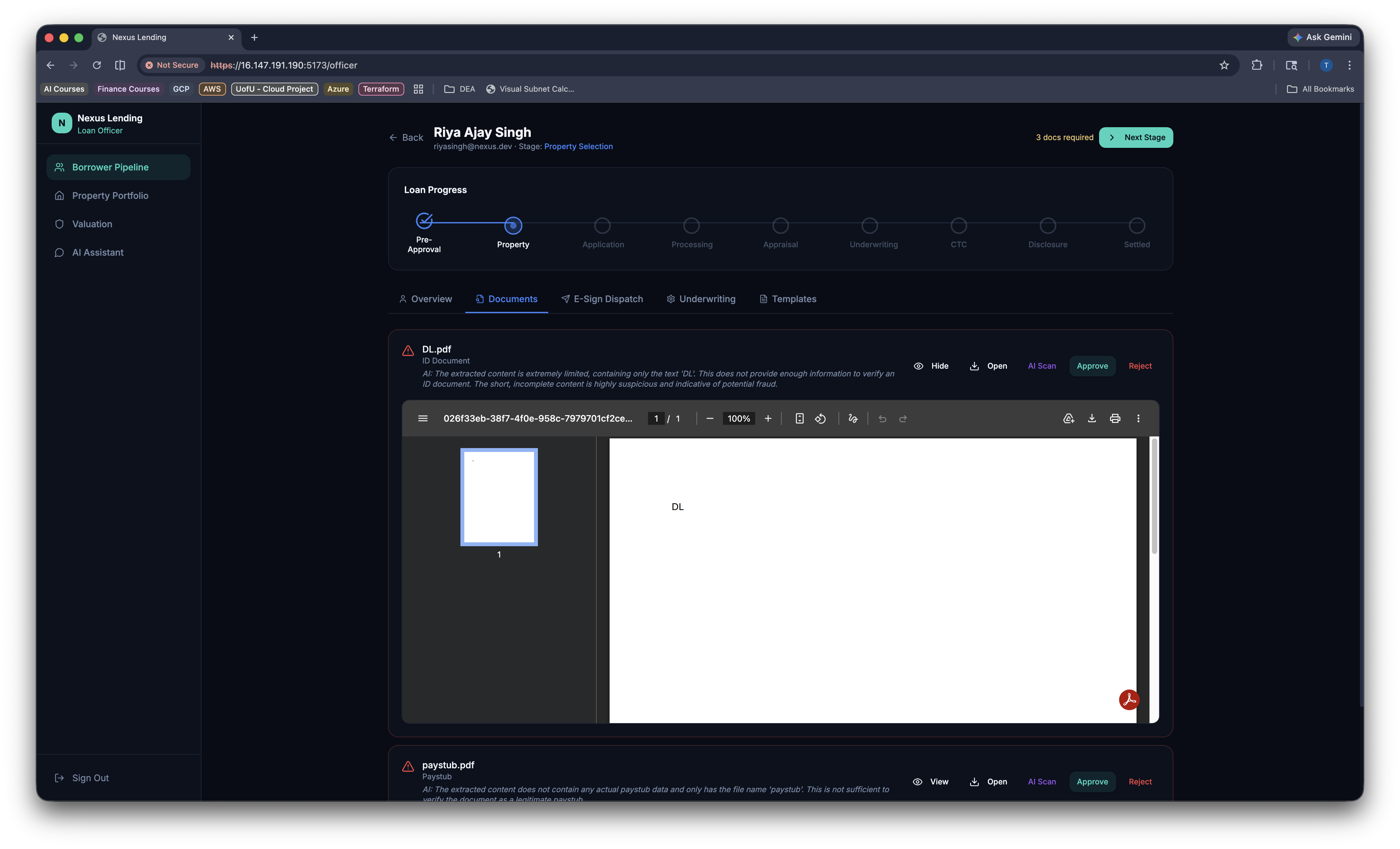

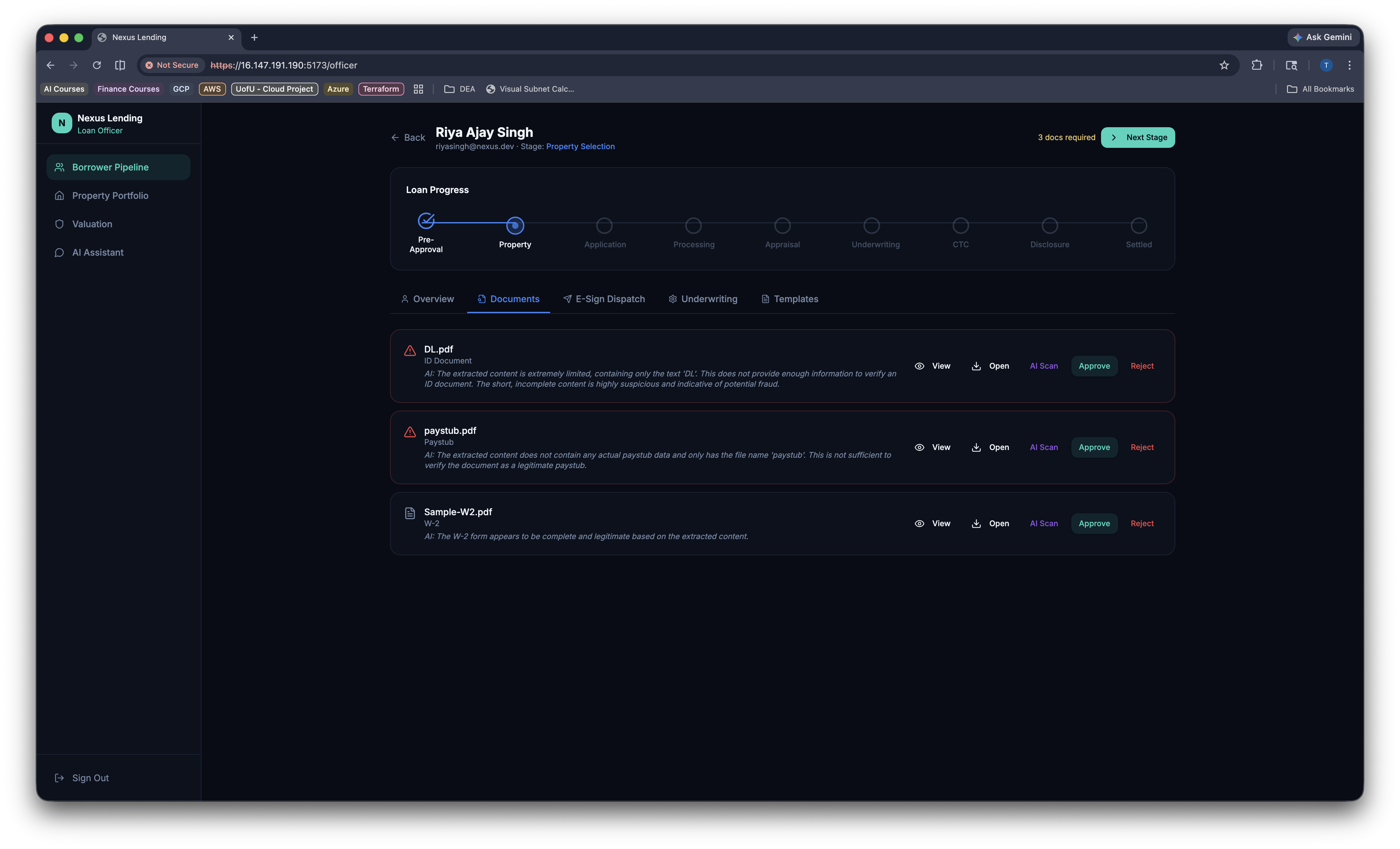

- Document upload with e-signature support

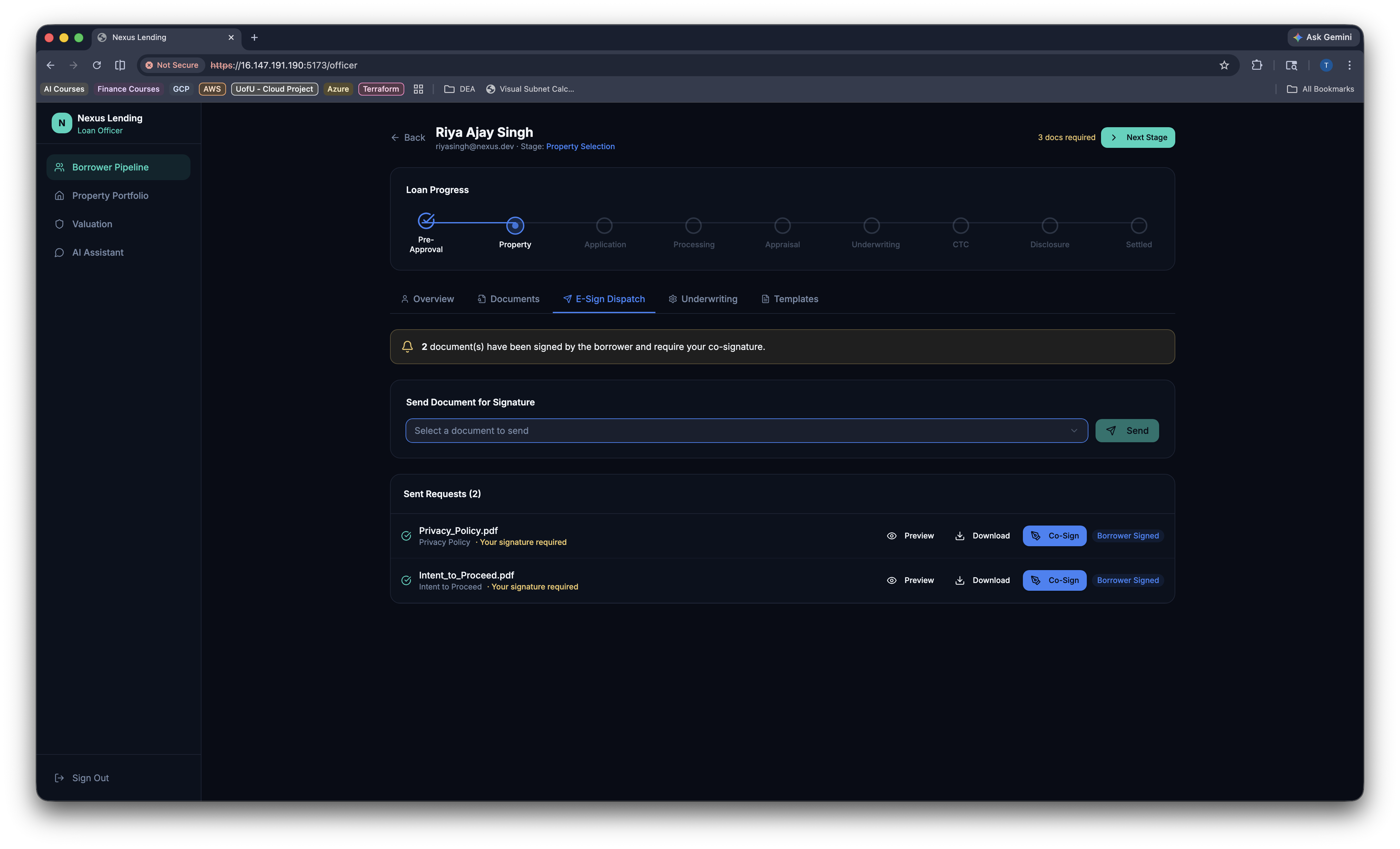

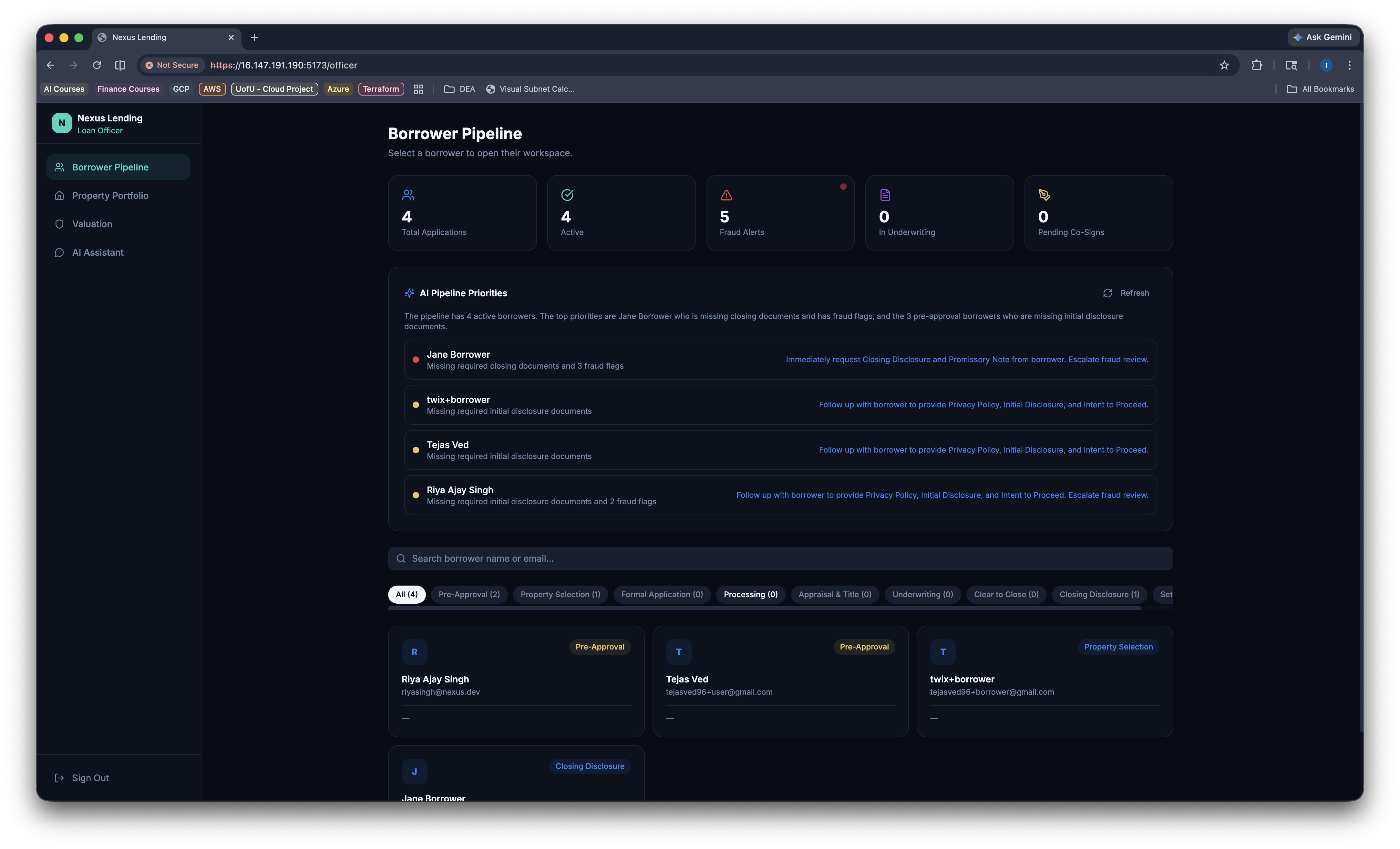

For loan officers:

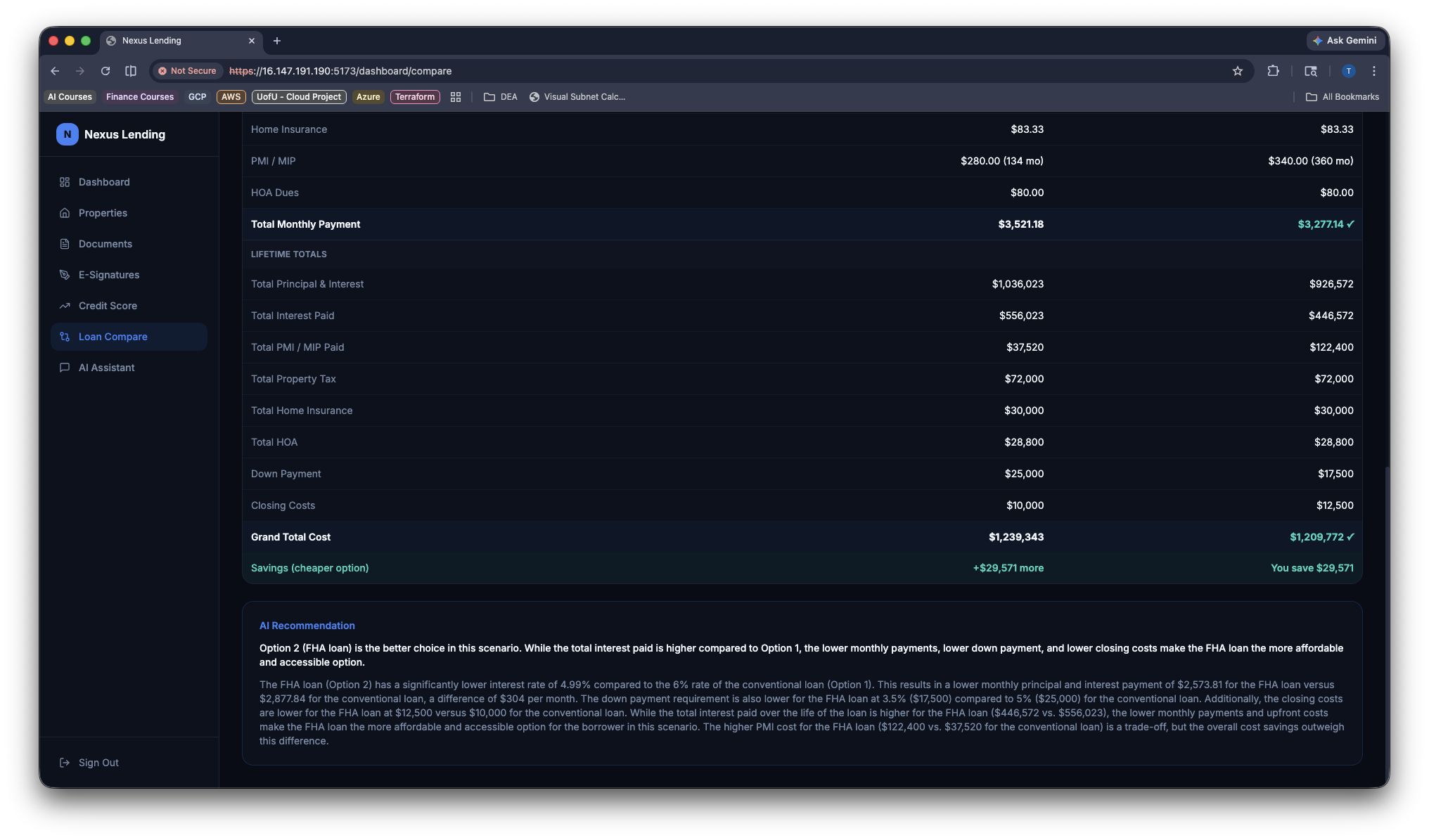

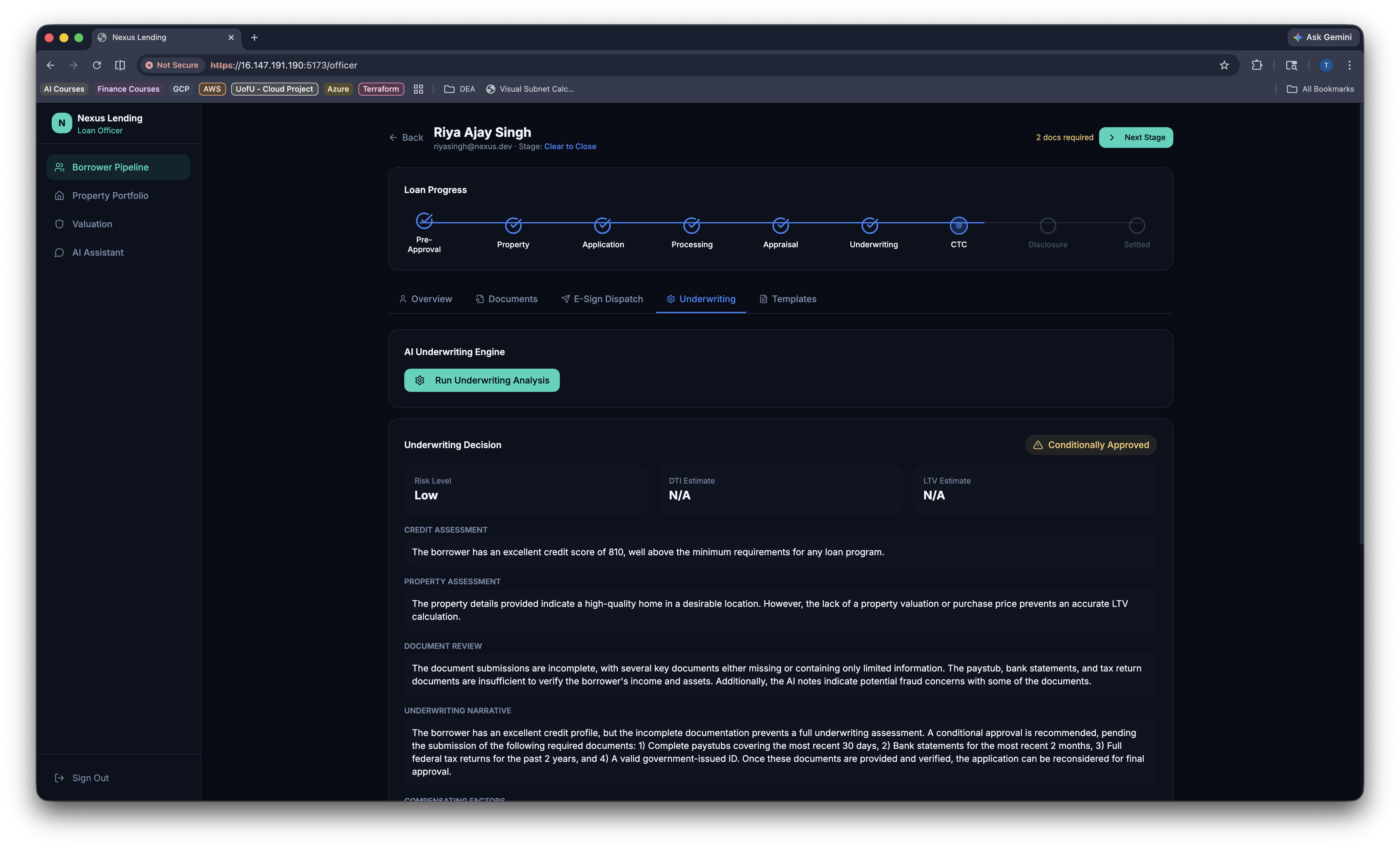

- One-click AI underwriting that calculates $\text{DTI} = \frac{\text{monthly debts}}{\text{gross income}}$ and $\text{LTV} = \frac{\text{loan amount}}{\text{property value}}$, assesses risk, and

delivers a structured decision (Approved / Conditionally Approved / Denied) in seconds

- AI document fraud detection that scans uploads and returns a confidence score $\in [0, 100]$

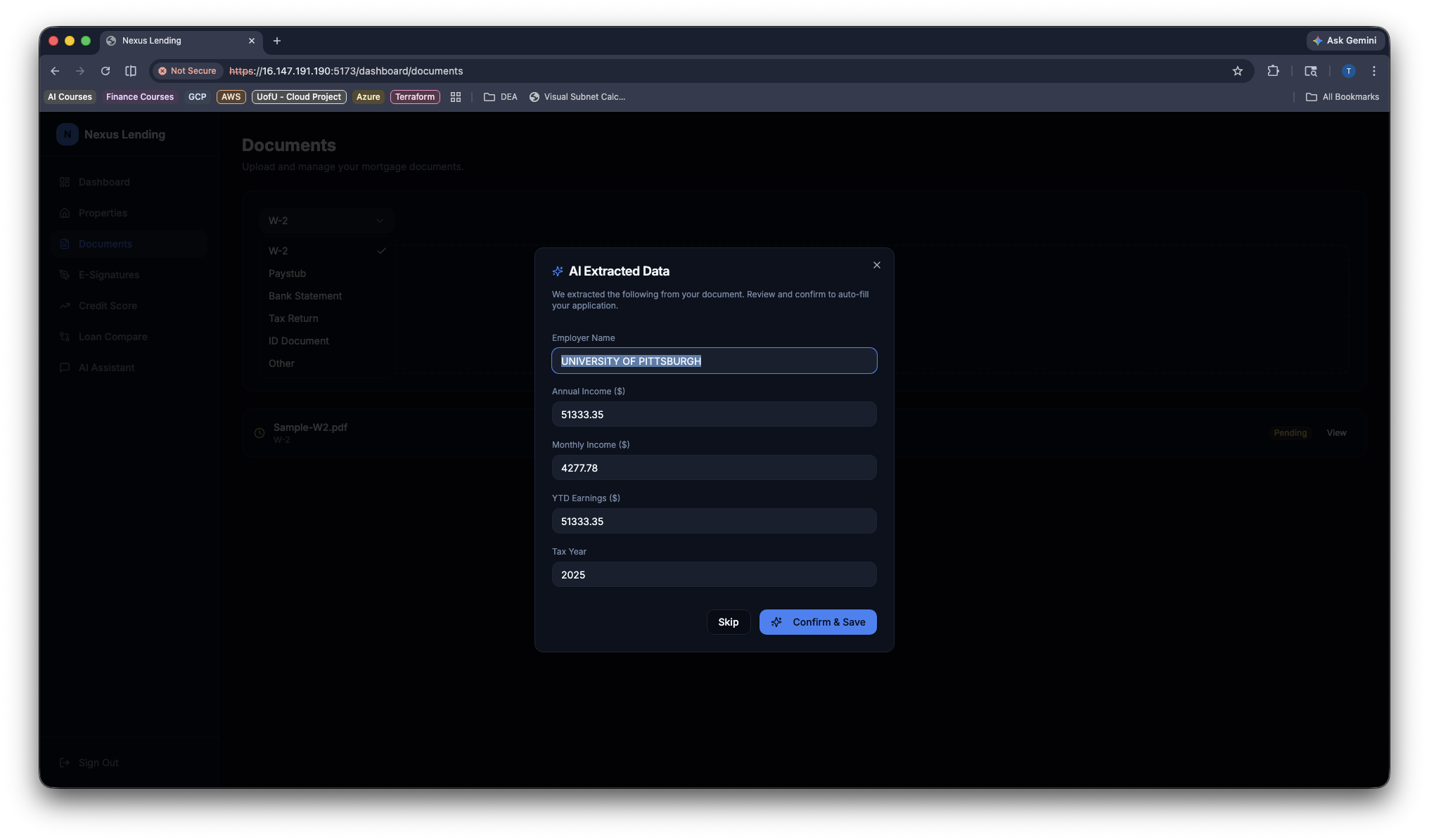

- AI data extraction from W-2s, paystubs, bank statements, and tax returns

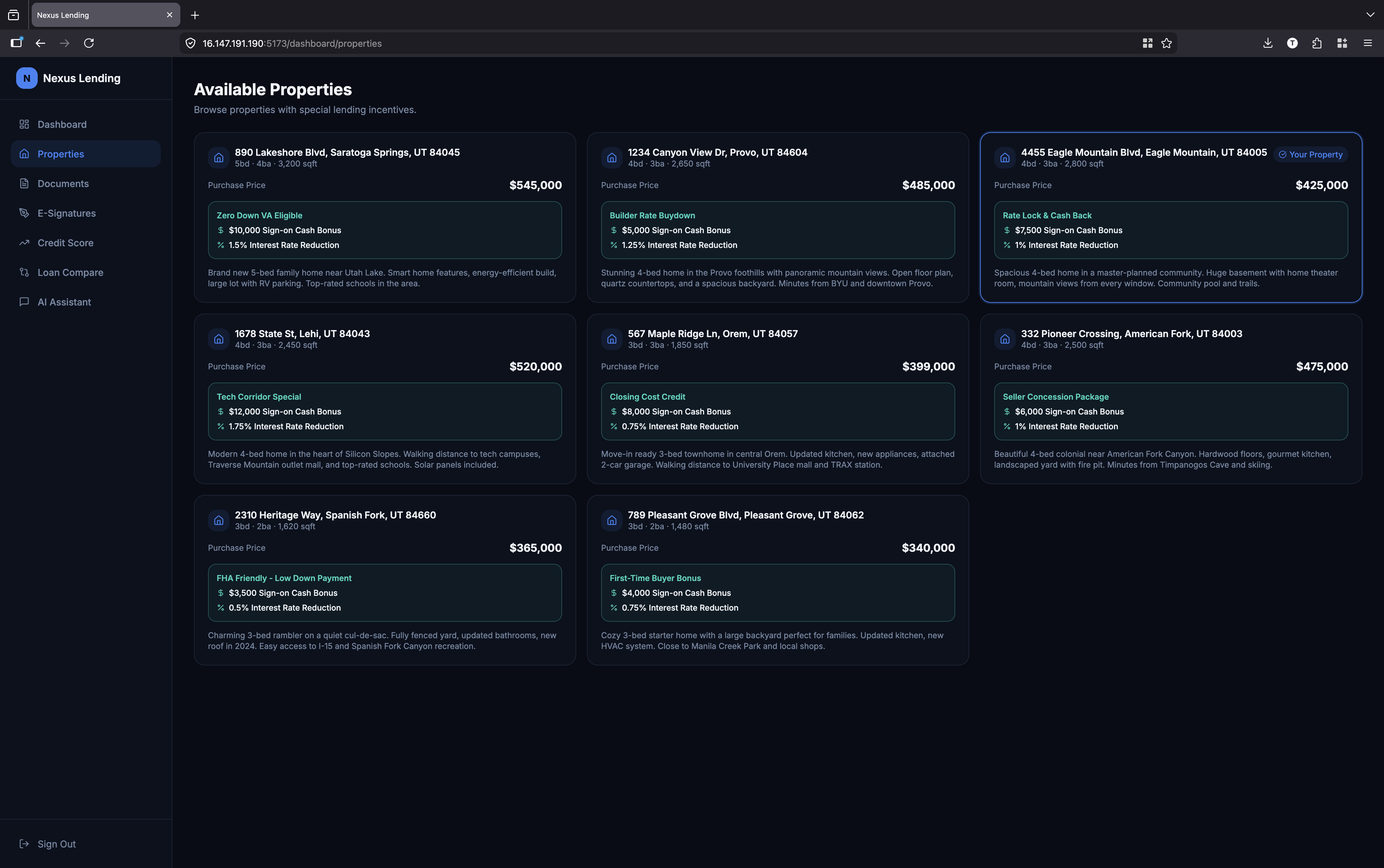

- Property valuation with real FEMA disaster data for environmental risk assessment

- AI compliance checking against RESPA, TRID, and fair lending regulations

## How we built it

We built a multi-agent architecture with 5 specialized AI agents, each defined by a modelfile with its own system prompt, temperature, and parameters:

| Agent | Temp | Role |

|-------|------|------|

| Mortgage Assistant | $0.7$ | Conversational guide for borrowers |

| Credit Analyzer | $0.3$ | Credit scoring and rate estimation |

| Underwriting Engine | $0.2$ | Automated loan decisions |

| Officer Assistant | $0.4$ | Knowledge base for loan officers |

| Property Valuation | $0.5$ | Market analysis with real FEMA disaster data |

Tech stack:

- Frontend: React 18, Vite, TailwindCSS, Radix UI, Framer Motion

- Backend: FastAPI, Python, Uvicorn

- Database: PostgreSQL via Supabase (+ Auth + Storage)

- AI: AWS Bedrock with Claude 3 Haiku

- External APIs: OpenFEMA (disaster data), Zippopotam (geocoding)

- Deployment: AWS EC2

The document pipeline ties it all together: upload a W-2 → AI extracts income data → AI scans for fraud → extracted data feeds into the underwriting engine → structured decision generated in

seconds.

## Challenges we ran into

- Structured JSON from LLMs is fragile. Claude sometimes wraps responses in markdown code fences or adds explanatory text. We built a robust parsing layer with regex fallbacks to reliably extract JSON from agent responses.

- Multi-agent coordination. Each agent needs different context — the underwriting engine needs credit data, documents, and property info all at once. Assembling the right prompt with the right

data for each agent was a design challenge. - Real API integration under time pressure. FEMA's API has its own schema quirks. Parsing disaster declarations and feeding them into an AI prompt in a useful format took more iteration than

expected.

- Balancing precision vs. personality. Too low a temperature and the borrower assistant sounds robotic; too high and the underwriting engine hallucinates conditions. Finding the right $T$ for

each agent required real testing.

## Accomplishments that we're proud of

- Full AI underwriting in seconds — what traditionally takes hours of manual review, our system handles with a single click, producing structured decisions with risk levels, conditions, and

compensating factors. - 5 specialized agents, not just one chatbot. Each agent is purpose-built for its domain with tuned parameters, not a generic wrapper around an LLM.

- Real data, not fake data. Our property risk assessments pull actual FEMA disaster declarations — grounding AI analysis in fact, not hallucination.

- End-to-end document pipeline. Upload → extract → fraud scan → underwrite, all automated and connected.

- Dual-persona platform. Borrowers and loan officers each get a tailored experience designed for how they actually work.

## What we learned

- Temperature is a design decision, not a default. Setting $T = 0.2$ for underwriting and $T = 0.7$ for chat made a dramatic difference in output quality for each use case.

- Grounding AI in real data changes everything. Plugging in FEMA's API took our property assessments from "plausible-sounding" to genuinely useful.

- Structured output unlocks automation. JSON responses (not paragraphs) let us build real pipelines where one agent's output feeds into another's input.

- The mortgage industry is ripe for disruption. Having lived through the pain ourselves, we saw just how many manual steps can be automated without sacrificing accuracy.

## What's next for Nexus Lending

- Integration with credit bureaus and MLS for real credit pulls and live property listings

- Multi-language support to make homeownership accessible to non-English speakers

- Broker and realtor portals to bring more stakeholders onto a single platform

- Mobile app for borrowers to track their loan progress and chat with AI on the go

- Agent-to-agent orchestration — letting agents collaborate autonomously, where the document agent triggers underwriting without human intervention

Built With

- aws-bedrock

- aws-ec2

- claude-3-haiku

- fastapi

- framer-motion

- google-web-speech-api

- javascript

- openfema-api

- postgresql

- python

- radix-ui

- react

- reportlab

- supabase

- tailwindcss

- vite

- zippopotam-api

Log in or sign up for Devpost to join the conversation.