Inspiration

Prediction markets like Polymarket are fundamentally different from traditional financial markets. Prices represent probabilities, time horizons are short, and market microstructure plays a dominant role in price formation.

We were motivated by a simple but powerful question:

Can we consistently generate trading profits without predicting Bitcoin directly — purely by exploiting pricing inefficiencies and market structure?

Instead of building a black-box prediction model, we focused on designing a system that combines arbitrage, theoretical pricing, and execution-aware trading.

What it does

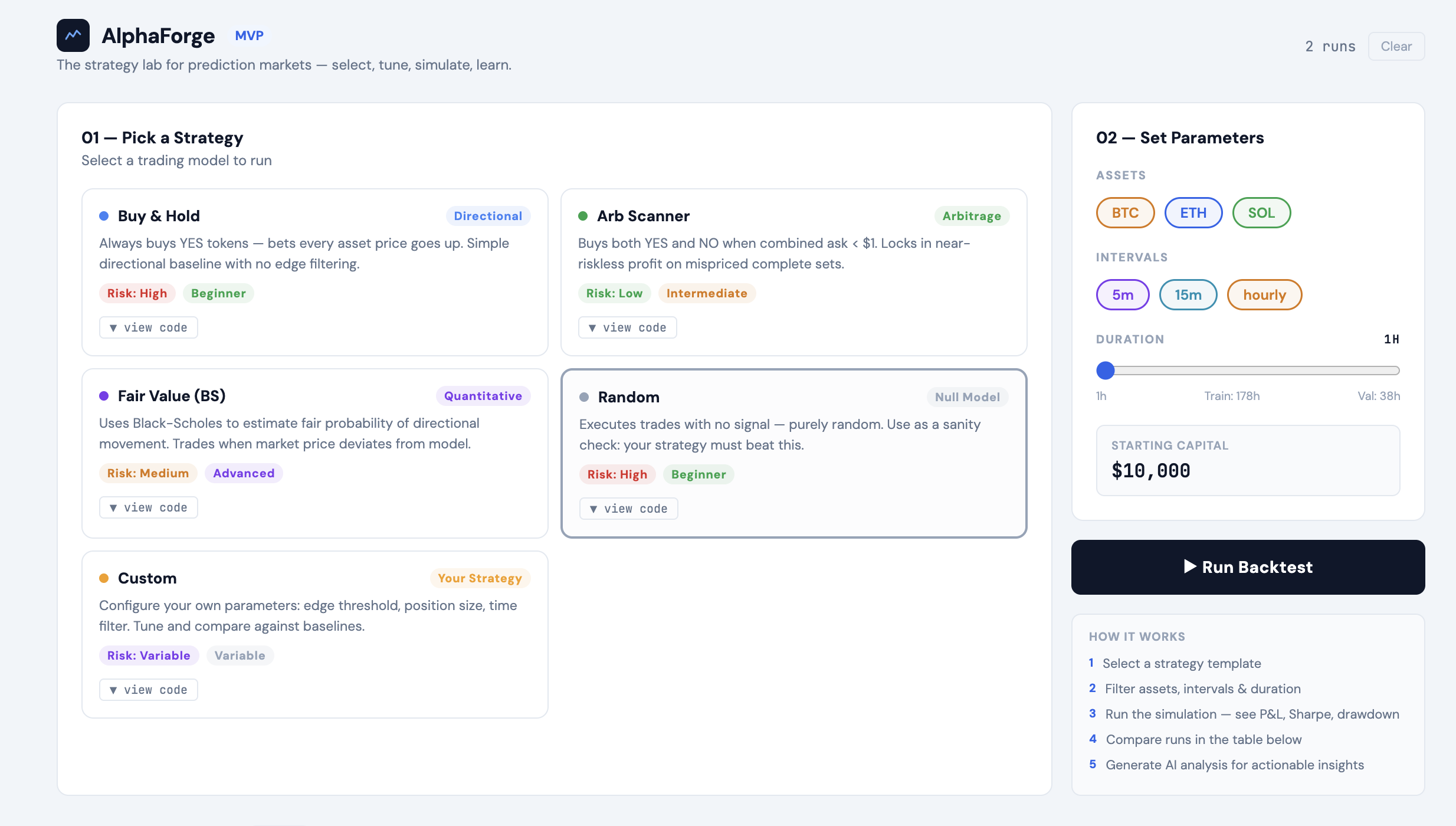

Negative Alpha is a multi-layer quantitative trading system for BTC binary options markets.

It systematically:

- Exploits arbitrage opportunities between YES/NO contracts

- Identifies fair-value deviations using a Black-Scholes-inspired model

- Trades based on real-time market microstructure signals

- Applies execution constraints and risk controls to ensure realistic performance

The system operates across multiple time horizons (5-minute, 15-minute, hourly), adapting its behavior to each regime.

How we built it

We designed a three-layer architecture, each responsible for a different source of edge:

Layer A: Arbitrage Engine

We capture risk-free opportunities when:

yes_ask + no_ask < 0.975

This guarantees a positive payoff at settlement and provides a stable baseline return.

Layer B: Late-Expiry Fair-Value Sniper

We estimate contract fair value using a Black-Scholes-inspired model, with several critical refinements:

Regime-aware trading We only enter trades in the late stage of the interval, where the model assumptions are more reliable.

Careful price initialization We record the Binance mid-price only when

time_remaining_frac > 0.85, preventing bias from mid-session initialization.Rolling volatility estimation Volatility is computed from recent log-returns over a 300-second window, allowing the model to adapt dynamically.

This layer captures systematic mispricings between theoretical probability and market quotes.

Layer C: Execution & Risk Control

To ensure realistic performance under market constraints, we implemented:

Dynamic stop-loss Exit positions when fair value drops below entry cost beyond a threshold

Liquidity guards

- Minimum order book depth

- Slippage tolerance constraints

Position sizing control

These mechanisms prevent overtrading in thin markets and control downside risk.

Interval-Specific Parameterization

Each time horizon (5m, 15m, hourly) uses its own set of parameters, including:

- Entry thresholds

- Volatility scaling

- Execution rules

This regime-specific tuning significantly improves performance compared to a single global configuration.

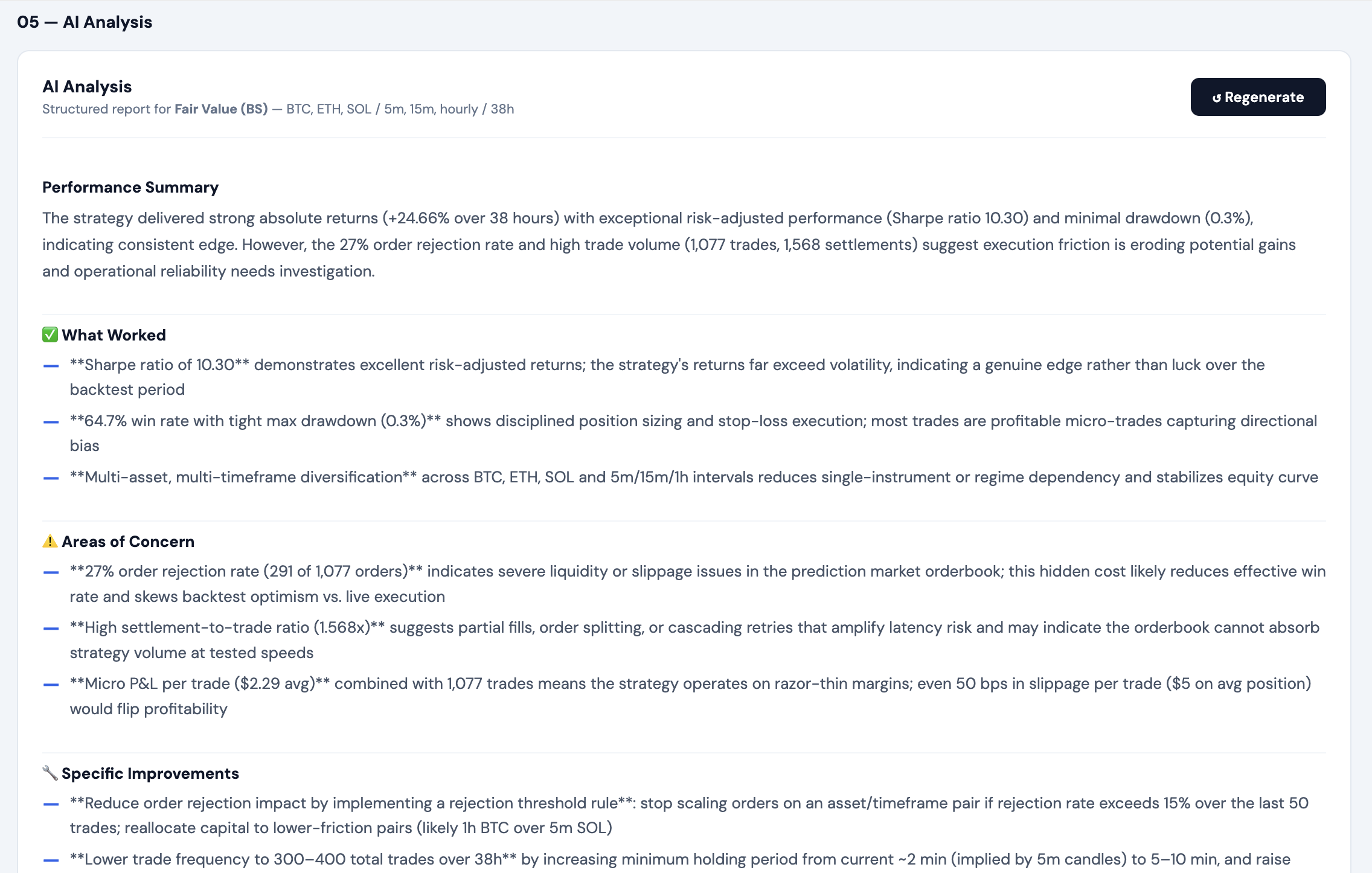

Challenges we ran into

Noisy microstructure data Order book signals are highly volatile and required careful filtering.

Model validity across time The Black-Scholes approximation breaks down early in the interval, forcing us to design a regime-aware strategy.

Parameter sensitivity Small changes in thresholds or trade size could drastically impact Sharpe ratio and drawdown.

Execution realism Without liquidity and slippage constraints, initial backtests were overly optimistic.

Accomplishments that we're proud of

- Designed a fully execution-aware trading system, not just a predictive model

- Successfully combined arbitrage, pricing models, and microstructure signals

- Built a strategy robust to real-world trading constraints

- Identified and leveraged the key insight that model effectiveness depends on time-to-expiry

What we learned

Edge comes from execution, not just prediction Even strong signals fail without proper trade execution.

Simple models can be powerful in the right regime Black-Scholes performs well when applied near expiry.

Market microstructure contains exploitable signals Order book imbalance and liquidity dynamics drive short-term price movement.

One-size-fits-all strategies fail Interval-specific tuning is essential for performance.

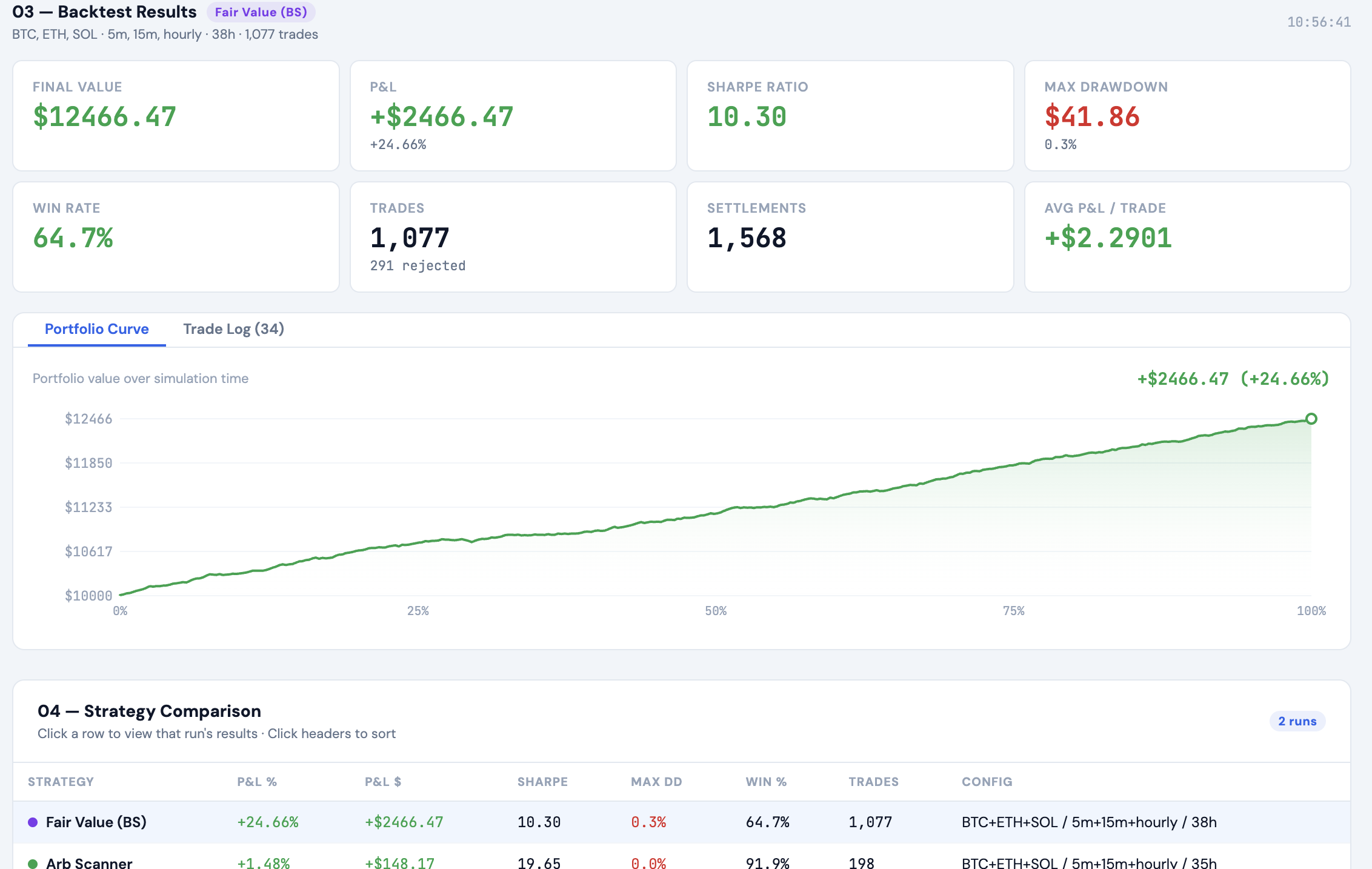

Results

Our final strategy was evaluated on a 38-hour backtest using real market data:

- P&L: +$2,513.56 (+25.14%)

- Sharpe Ratio: 24.63

- Max Drawdown: 7.58%

- Win Rate: 75.9%

- Total Trades: 1,255

Interpretation

The strategy achieves strong performance through:

- High-frequency execution with consistent edge

- Robust risk control despite aggressive trading

- Systematic exploitation of market inefficiencies

These results demonstrate that prediction markets contain persistent inefficiencies that can be captured through execution-aware strategies.

What's next for Negative Alpha

We plan to extend the system in several directions:

- Dynamic position sizing based on confidence and volatility

- Market-making extensions to capture spread in addition to directional trades

- Cross-market arbitrage between Polymarket and external exchanges

- Reinforcement learning for execution optimization

Our long-term goal is to evolve Negative Alpha into a fully adaptive trading agent capable of operating across multiple markets in real time.

Log in or sign up for Devpost to join the conversation.