-

The homepage of the mobile app, where refugees and migrants can monitor their score, apply for lease guarantees, & update personal profiles

-

Input recent financial information that we use to generate a credibility score

-

Securely share personal and financial profiles with potential landlords via email, or revoke access at any time

-

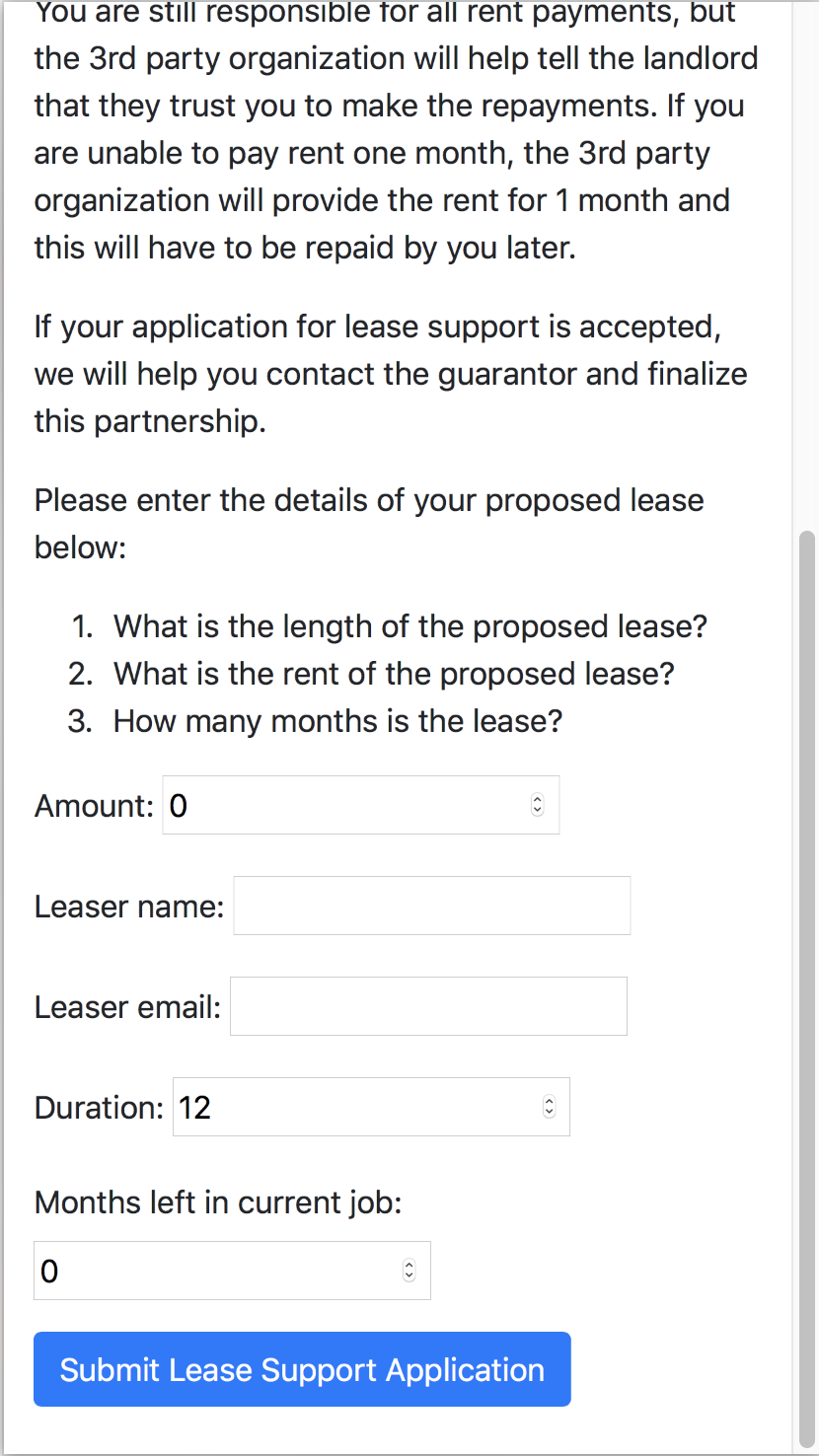

Apply to lease agreements directly in the webapp, with an explanation of the significant contractual terms and financial details

-

A web interface for lease guarantors and financial backers for refugees and migrants

-

The administrative portal considers individuals' credit history in a unique, risk-conscious but compassionate context

Overview

Refugees and migrants with some ability to earn income still cannot access housing leases because of insufficient proof of financial credibility.

Credit/Ability is a mobile website that allows refugees to input their (often short-term) employment, income, and payment histories since they’ve been in their new host country. We use this information to compute a credibility score—if it’s high enough, indicating sufficient financial responsibility and ability to get and pay for a lease over a lease period (e.g., 12 months), we work with organizational backers to provide a lease guarantee that puts refugees on the same footing as others looking for long-term housing.

Our website has interfaces for all three critical stakeholders:

- The primary focus is on the mobile website available to refugee and migrant users. With this mobile site, they have unique financial agency and the ability to update, share, and easily revoke access to their credibility score and financial history. When they use our app to apply for a lease guarantee for a specific time period and rent payment amount, their profile and financial history is shared with a potential guarantor—an organizational backer.

- Administrators from organizational backers have an interface that shows each applicant’s credibility history details (including employment, income, and financial histories), credibility score, and a month-by-month probability prediction of lease payment ability that we calculate using models from real commercial banks. This provides a financing guarantee approval process that is both risk-conscious and compassionate, enabling backers to use their money more effectively and make it go further for greater impact.

- Lease providers and landlords receive a website link via email to contractual information once a backer extends a lease guarantee. App users can also send landlords one-time links that authorize viewing of a private profile page containing credibility scores and basic financial information.

Future

- A user’s credibility score grows with them as they gain footholds in their host country and can provide access to more financial opportunities in the near future, more quickly and effectively than a traditional commercial lender’s credit score.

- For deployment, we hope to work with faith-based organizations that provide resettlement services, like the International Union of Superior Generals (IUSG) and Catholic Charities USA, for onboarding locally at trusted points of contact where migrants and refugees already receive language, employment, and housing support.

- We hope to re-implement our probabilistic repayment/default models using more sophisticated machine learning algorithms that will become more accurate over time, with every new user and lease guarantee extended.

- Potential future features of the app include financial literacy advice, connections with local essential service providers, and live support chat. A future financing feature we have explored is group-based insurance for a group of 5-10 friends’ leases or perhaps loans, in which risk of rent payment failure or loan default may be distributed across 5-10 group members, much like how microfinance institutions use social bonds to lend to groups with extremely low default rates.

The credibility score details:

- To calculate credibility scores, we verify recent employment, income, and payment history information and using algorithms similar to those used by commercial banks but with a focus on short-term income and solvency, we compute a credibility score on a scale from -100 to +100 for users, where 0 represents no verified financial history in a host country.

- For verification, we work with a third-party verification service like those used by Airbnb to verify ID. If documentation, like paystubs or work agreements, are available, we ask that users upload them; if not, we require an official contact point (e.g., phone number for a real restaurant listed on Yelp) at a bonafide business that we can call as a reference to verify users’ recent financial history.

- Since family and friend networks are important in establishing strong resettled communities, users can send individuals who know them and who can verify their financial history a one-time link to create a recommendation. These recommendations can attest to the user’s responsibility and finances.

Inspiration

On the first night in Rome before VHacks, our team visited a local church that helps refugees and migrants resettle in Rome. We heard from many refugees that even for the ones that are lucky enough to be earning some income and could pay for stable housing, they are unable to convince landlords to rent to them. Due to the informal and often inconsistent nature of job opportunities, insufficient or lack of financial documentation or credit history, and negative perceptions from local landlords, refugees and migrants often cannot prove to landlords that they are capable of being reliable tenants and are often left homeless. Across Europe, some estimates suggest that over 2/3 of the refugee population are homeless. We were especially taken by this problem: even those who work hard and reach the cusp of becoming fully self-reliant cannot access basic services like housing, fundamentally because of a lack of trust.

We wanted to address that gap in credibility—how to reduce the mistrust and risk of extending housing leases to refugees and remove a major barrier limiting them from successfully integrating into their new home countries.

Credit/Ability seeks to build users’ credibility and de-risk the provision of critical services like housing

Formal financial credit histories are often inaccessible to vulnerable populations like refugees and migrants, as they cannot account for the short-term, variable nature of their employment and expenditures. Credit/Ability is a credibility scoring application that is tailored to the unique contexts of refugees and migrants—it is designed to be risk-conscious, but flexible enough to accommodate for the uncertainty and unique experiences of these users’ lives. Credit/Ability is designed to collate and verify a person's history, based on any informal/short-term employment they’ve had, payments or expenditures they’ve made, or subsidies they've received. In addition to a credibility score, refugees can also build a portfolio of verified references from former employers, landlords, or even service providers like churches to further demonstrate their reliability.

We aim to make this credibility profile sufficient to demonstrate to potential landlords that leasing to a refugee will not be a risk. To ensure initial buy-in and reduce risks for landlords, Credit/Ability will offer refugee and migrants users lease support by pairing them with a third-party guarantor that will act as a cosigner on the lease. By offering both a credibility score and a third-party guarantee, we will reduce the risk to landlords and help refugees gain access to housing independently, helping to increase their own independence over time.

Throughout our interviews with refugees before VHacks in both the US and in Rome, we constantly heard about their desires to become self-reliant and exercise their own agency. Refugees that have worked hard to integrate should not be limited simply because of an inability to prove they are credible. By building their credibility over time, they can not only gain access to services like housing, but they will also make progress in addressing the negative stereotypes that fuel mistrust of refugees.

Targeting partnerships and pilot possibilities

We aim to target faith-based organizations—especially churches and parishes—working with refugees to act as guarantors for leasing support. Many faith-based organizations have devoted significant resources to supporting integration and often serve as the most trusted service providers for many refugees, providing housing support in the form of temporary grants or shelter. By providing guarantees for the population of refugees that are becoming capable of supporting themselves, organizations can utilize their funding more effectively and make sure their resources are targeted to the most vulnerable populations. Money used to finance lease guarantees for refugees who are able to pay their rent can be reinvested for greater impact.

As many of these organizations are also service providers and trusted networks for refugees, we would also leverage them to help onboard refugees into the application. Churches are well-versed in the needs and profiles of refugees and would be able to identify those who might benefit from this service.

Our initial target markets for a pilot to test and refine our model are Italy and the United States. Refugee contexts vary significantly in different countries and we think it is important to test this model in two specific countries with vastly different regulatory frameworks, housing situations, and refugee integration challenges. We have identified two initial networks of faith-based organizations to tap into—International Union of Superior Generals (IUSG) and Catholic Charities USA—which devote resources to refugee housing. For the initial testing in Italy and the US, we propose identifying local champions such as the Archdiocese of Newark (which we are familiar with through our University) who have shown an interest in refugee resettlement and devoted resources to this issue. Tapping into these networks will be key as they can help us improve our model, scale, and replicate to other countries and localities.

Download presentation deck:

[ ](https://drive.google.com/file/d/1cbeNCXOiSHdhbY93ZXevgJZO3BdzaNUD/view?usp=sharing)

](https://drive.google.com/file/d/1cbeNCXOiSHdhbY93ZXevgJZO3BdzaNUD/view?usp=sharing)

Log in or sign up for Devpost to join the conversation.