-

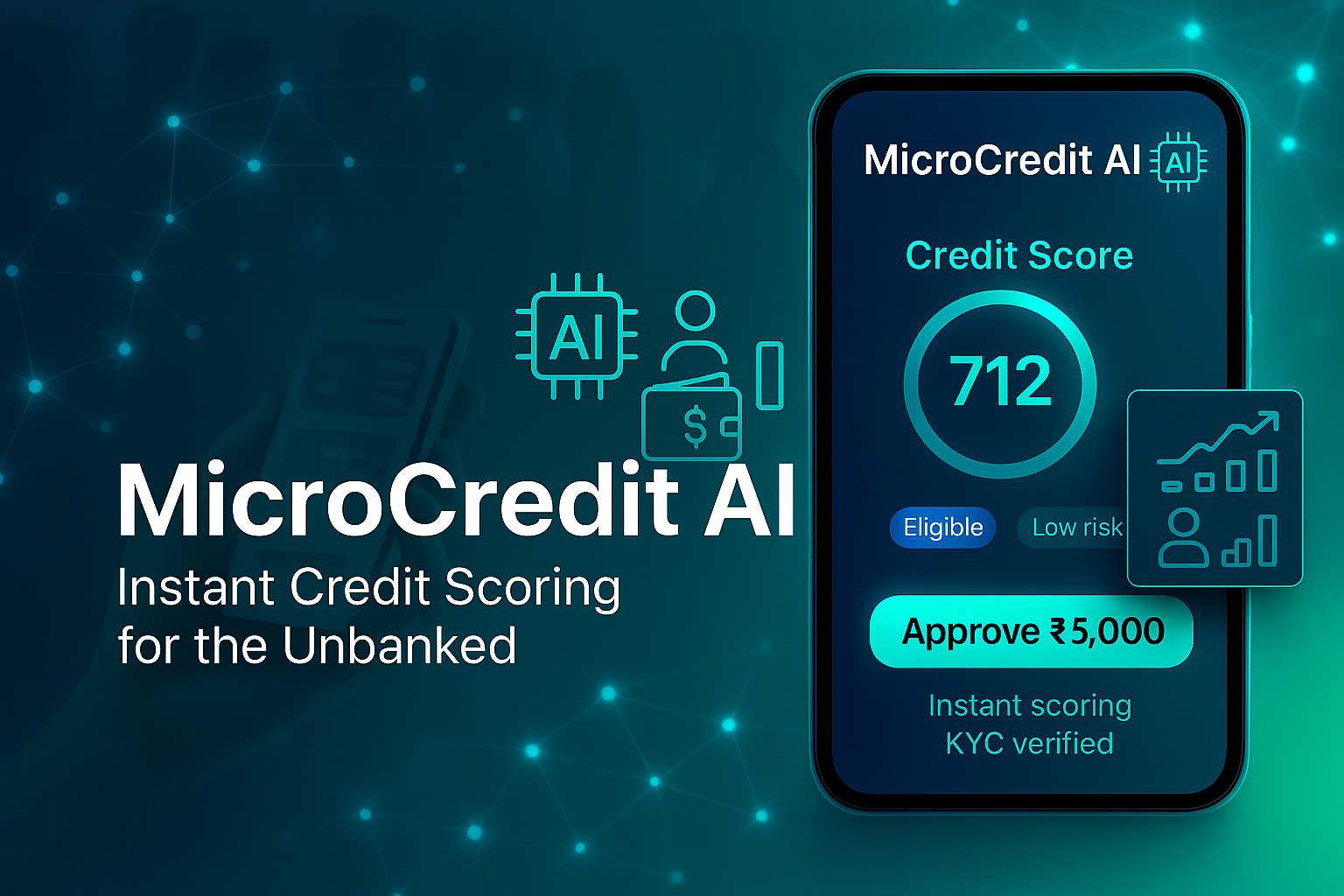

MicroCredit AI – Instant Credit Scoring for the Unbanked

MicroCredit AI – Instant Credit Scoring for the Unbanked

Inspiration

Financial inclusion remains one of the greatest challenges of our time. According to the World Bank, over 1.7 billion adults globally are unbanked, lacking access to basic financial services such as savings accounts, credit, and loans. Traditional banks often rely on historical financial data to evaluate creditworthiness, excluding millions who may have irregular income, informal employment, or no documented banking history.

Our inspiration came from bridging this gap using technology. We wanted to create a solution that empowers the unbanked by leveraging alternative data sources—mobile payments, utility bills, transaction patterns—to calculate a trustworthy, AI-driven credit score. Our goal was to make microloans accessible, fair, and instantaneous, so people in underserved communities can participate in the economy, grow businesses, or cover essential needs without relying on predatory lending.

We were also motivated by the growing role of AI and fintech in solving social problems. By combining machine learning with mobile technology, we realized we could design a system that is scalable, ethical, and impactful, ensuring financial services reach those who need them most.

What it Does

MicroCredit AI is a mobile-first application that provides instant credit scoring and microloan eligibility for individuals without traditional banking history. The system works as follows:

Data Input

Users provide minimal personal information and optional alternative data, such as:- Mobile recharge/payment history

- Utility bill payments

- Peer-to-peer digital transactions

- Employment or income sources

- Mobile recharge/payment history

AI-Powered Credit Scoring

The system calculates a credit score (0–1000) using machine learning models trained on synthetic datasets reflecting real-world behaviors of unbanked populations. Example formula:

[ \text{Credit Score} = w_1 \cdot \text{Payment History} + w_2 \cdot \text{Transaction Frequency} + w_3 \cdot \text{Debt Ratio} ]

- Payment History: Timeliness of past payments

- Transaction Frequency: Regularity and volume of financial activity

- Debt Ratio: Comparison of liabilities vs. income

Loan Decision

- Approved: Users with scores above the threshold receive a microloan offer.

- Declined: Users receive actionable recommendations to improve their creditworthiness.

- Approved: Users with scores above the threshold receive a microloan offer.

User Feedback & Transparency

The AI model provides interpretable insights so users understand why a score was assigned and what actions improve it.Impact Metrics

- Enables users to access loans in minutes, not weeks.

- Promotes financial literacy by giving actionable insights.

- Supports economic inclusion in communities traditionally ignored by banks.

- Enables users to access loans in minutes, not weeks.

How We Built It

1. Tech Stack Overview

- Frontend: React Native for mobile-first cross-platform app development

- Backend: Flask with PostgreSQL database, ensuring scalability and rapid deployment

- AI/ML Model: Python (Scikit-learn / XGBoost) for credit scoring

- Integration: Mock payment APIs (Razorpay / Paytm sandbox) for transaction simulation

- Data: World Bank microfinance datasets + synthetic transaction datasets for realistic testing

2. Architecture

The system follows a modular architecture:

[User Mobile App] --> [Backend API] --> [AI Credit Scoring Engine] --> [Database]

- Frontend: Handles user registration, data input, and result display

- Backend API: Validates input, communicates with AI engine, stores records

- AI Engine: Processes alternative data and generates credit scores

- Database: Stores user profiles, transaction histories, loan status

3. AI Model Development

- Dataset: Simulated 10,000+ user profiles based on real-world alternative data patterns

- Features: Payment timeliness, transaction frequency, income estimates, bill payment consistency

- Model Choice:

- Logistic Regression for interpretability

- XGBoost for improved accuracy

- Logistic Regression for interpretability

- Evaluation Metrics: Precision, recall, F1-score to ensure fair classification

4. UI/UX Design

- Clean, simple interface for low-literacy users

- Step-by-step onboarding: input → credit score → loan offer → tips

- Visual feedback (score meter, graphs) to make data understandable

5. Security & Privacy Considerations

- User data is encrypted at rest and in transit

- No sensitive data stored permanently

- Credit scoring is transparent and interpretable, avoiding black-box decisions

Challenges We Ran Into

Data Scarcity

- Real alternative financial data is confidential.

- Solution: Created realistic synthetic datasets reflecting common patterns of unbanked populations.

- Real alternative financial data is confidential.

Ensuring Fairness

- Risk of AI bias against marginalized users.

- Solution: Balanced dataset features, interpretable model, fairness metrics.

- Risk of AI bias against marginalized users.

Time Constraints

- Integrating AI + frontend + payment simulation within hackathon timeframe was challenging.

- Solution: Prioritized MVP with core scoring + loan offer feature, added polish later.

- Integrating AI + frontend + payment simulation within hackathon timeframe was challenging.

Model Interpretability

- Users needed understandable feedback on their credit score.

- Solution: Displayed contribution of each feature (e.g., “Late bill payments reduced your score by 50 points”).

- Users needed understandable feedback on their credit score.

Accomplishments That We're Proud Of

- Delivered a fully functional mobile prototype with AI-driven credit scoring

- Integrated mock payment systems to simulate real-world microloans

- Designed interpretable AI outputs, promoting financial literacy

- Created documentation and tutorials so judges can understand technical depth

- Positive social impact focus: product addresses a real-world inclusion problem

What We Learned

- Combining AI, fintech, and mobile development requires cross-disciplinary collaboration

- Ethical AI is crucial in financial decision-making

- Simulating datasets can effectively train AI models when real-world data is scarce

- Importance of user-friendly design for adoption in low-literacy or low-tech communities

- Hackathon teamwork: efficient planning, modular development, and communication

What's Next for MicroCredit AI

Real API Integration

- Partner with financial institutions to allow real microloan disbursement

- Partner with financial institutions to allow real microloan disbursement

Expanded Alternative Data Sources

- Include social payments, remittances, community transactions

- Include social payments, remittances, community transactions

Gamified Credit Improvement

- Reward users for timely payments and financial education

- Reward users for timely payments and financial education

Global Expansion

- Adapt models for different countries and economies, accounting for local financial behaviors

- Adapt models for different countries and economies, accounting for local financial behaviors

Open-Source AI Model

- Share interpretability methods to promote transparent credit scoring globally

- Share interpretability methods to promote transparent credit scoring globally

Appendix: AI Credit Scoring Example Formula

[ \text{Credit Score} = 0.4 \cdot \text{Payment History} + 0.35 \cdot \text{Transaction Frequency} + 0.25 \cdot \text{Debt Ratio} ]

Where:

- Payment History: 0–100 (timeliness of past payments)

- Transaction Frequency: 0–100 (regularity of financial activity)

- Debt Ratio: 0–100 (ratio of debt to income, lower is better)

Introduction & Global Context

Financial inclusion remains one of the most pressing challenges of the 21st century. According to the World Bank’s Global Findex Database, over 1.7 billion adults worldwide do not have access to formal banking services, leaving them vulnerable to economic instability, high-interest informal lending, and limited opportunities for personal and entrepreneurial growth. The lack of access to basic financial tools—such as savings accounts, loans, and insurance—creates systemic barriers, especially in developing countries and rural areas, where informal economies dominate.

The unbanked population is not homogenous. It includes small business owners in remote villages, informal workers in urban areas, migrant laborers, and students without formal credit histories. Each subgroup faces unique challenges in accessing credit:

- Small Shopkeepers: Often rely on informal loans with high interest rates due to lack of verifiable income statements.

- Freelancers and Gig Workers: Income is irregular and difficult to document, leading to rejection from conventional banks.

- Rural Populations: Infrastructure and digital access are limited, making bank branches inaccessible.

Traditional credit scoring methods rely heavily on historical financial data, such as previous loans, credit card usage, and income statements. These criteria exclude a vast majority of the unbanked population, perpetuating inequality and limiting economic mobility. This creates a compelling need for innovative, alternative approaches that leverage non-traditional data sources to assess creditworthiness.

Role of Technology and AI in Financial Inclusion

Advances in financial technology (fintech) and artificial intelligence (AI) present unprecedented opportunities to bridge the gap for unbanked populations. AI systems can analyze alternative data sources, such as mobile phone usage patterns, digital transactions, utility payments, and social financial behavior, to evaluate an individual's reliability and trustworthiness in repaying loans. Unlike traditional models, AI can process large-scale heterogeneous datasets, detect hidden patterns, and provide fast, data-driven credit decisions.

Key benefits of AI in financial inclusion include:

- Speed and Accessibility: Instantaneous credit scoring and loan approvals, accessible via mobile devices, removing geographical and logistical barriers.

- Fairness and Adaptability: Models can be designed to mitigate bias and evaluate users based on relevant alternative metrics rather than incomplete historical data.

- Scalability: Once trained, AI systems can serve thousands or millions of users with minimal incremental cost.

- Financial Literacy: Transparent AI outputs can provide actionable recommendations, helping users understand how to improve their financial standing.

Global Examples of AI in Microfinance

Several organizations have demonstrated the potential of AI in expanding financial access:

- M-Pesa (Kenya): Mobile payment systems coupled with data-driven credit scoring allow microloans to reach millions of Kenyans without traditional bank accounts.

- Kiva Protocol (Global): Leverages blockchain and mobile identity verification to facilitate loans in underserved regions.

- ZestFinance (USA & Asia): Uses AI-based underwriting to provide loans to applicants with limited credit history, reducing default risk while increasing access.

These examples illustrate how technology can transform economic inclusion, yet challenges remain. Many solutions require robust infrastructure, trustworthy data, and ethical frameworks to avoid perpetuating bias. This motivated our team to develop MicroCredit AI, a platform that leverages AI to provide instant, interpretable, and fair credit scores, enabling microloans for unbanked individuals globally.

Why MicroCredit AI Matters

Our goal is not just to build a functional app but to empower users and communities:

- Economic Empowerment: By providing access to microloans, individuals can start small businesses, invest in education, or cover essential expenses.

- Financial Transparency: Users receive clear insights into how their creditworthiness is evaluated.

- Social Impact: Supports the broader mission of financial inclusion, reducing inequality and enabling participation in the formal economy.

In summary, the combination of AI, fintech, and mobile technology presents a unique opportunity to solve a real-world economic problem. MicroCredit AI stands at the intersection of innovation and social impact, providing a scalable, ethical, and practical solution to the credit access gap for unbanked populations.

Built With

- css

- firebase

- flask

- github

- heroku

- html

- javascript

- paytm-sandbox-api

- postgresql

- python

- razorpay-sandbox-api

- react-native

- scikit-learn

- xgboost

Log in or sign up for Devpost to join the conversation.