Inspiration

So i thought a very different prototype before basically an AI assistant with smart financial advices but it required me trying to time the market which felt a red flag so i made discussions with my elder brother and some of my friends to evolve what mha-finance is today.

What it does

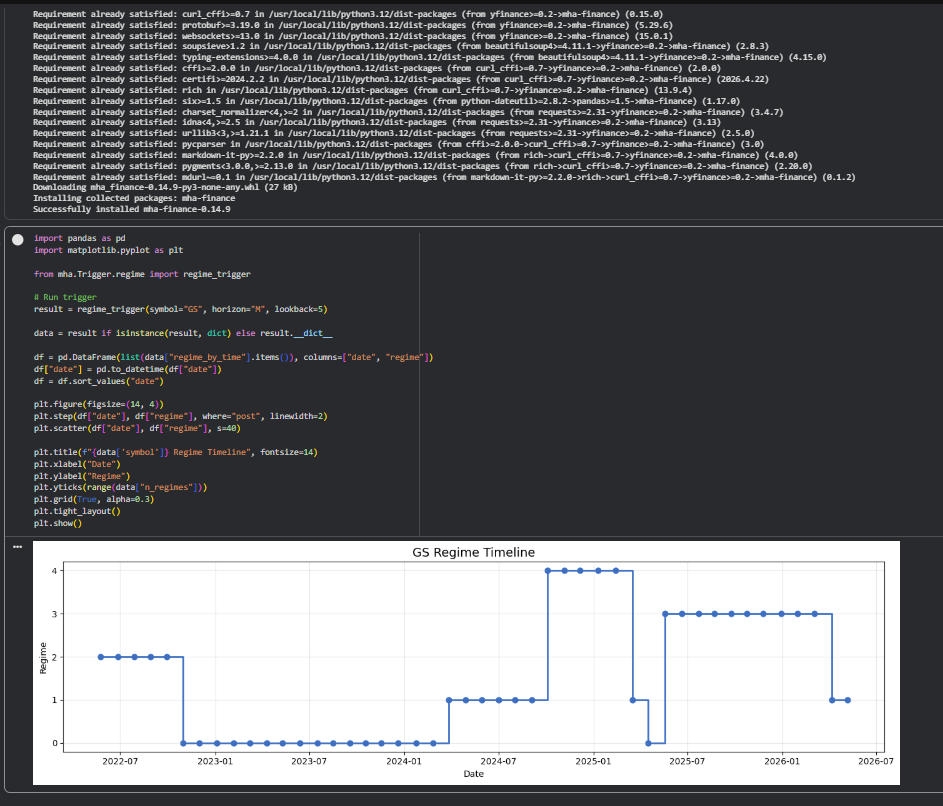

mha-finance is a Python framework for statistical analysis of financial markets on multiple time horizons. The project is not about price prediction or trading signals, but it’s rather meant to assist the users to better understand the market behavior through descriptive analysis.

Framework supports return analysis, volatility characterization and market regime analysis of historical financial data. Our straightforward trigger-based API enables users to analyze assets on weekly, monthly or annual horizons and generate understandable statistical summaries for research, learning and exploratory financial analysis.

How we built it

mha-finance is a Python modular framework that allows us to conduct statistical analysis on multi-horizon financial time series data. This project draws its ideas from areas of finance, statistics, and reproducible software development, offering descriptive analytics in the form of returns, volatility, and market regimes.

While developing this framework, we primarily used languages like Python, with frameworks including Pandas, NumPy, scikit-learn, and yfinance. We adopted the approach of building an analytically interconnected system based on the principles of modules' interdependence and triggering API for maximum usability and flexibility.

The working model of mha-finance was successfully built and tested on financial data, allowing for horizon-wise analysis of returns, volatility, and market regimes. We are now aiming at improving this framework link :- https://github.com/vkverma9534/mha-finance

Challenges we ran into

One of the biggest challenges was the direction that the project itself took. The original idea was much more prediction-oriented, but we realized that building systems around financial advice and market timing raised practical and ethical concerns. This led us to re-evaluate the project and change to a more research and descriptive framework.

Another challenge was to create statistical methods which would perform robustly across different financial time horizons and keep the framework simple and interpretable for the users.

Accomplishments that we're proud of

We are proud of having transformed an early idea into a focused, research-oriented financial analysis framework. Instead of building another prediction or trading system we moved towards building something more transparent, interpretable and statistically grounded.

mha-finance is a working, reproducible codebase for anyone to perform multi-horizon financial analysis. The framework offers modular components for return analysis, volatility characterization and market regime analysis. Usage is documented and a simple trigger-based API is described in the README.

What we learned

Building mha-finance has taught us a lot about financial concepts such as returns, volatility, market regimes and the challenges of understanding financial behavior at different time horizons. We also gained practical experience in building and deploying reproducible analytical frameworks rather than isolated scripts or prototypes.

Another important learning outcome was the ability to structure an interdependent codebase with modular analytical components that can work together cleanly, but still be extensible and maintainable for future development.

What's next for mha-finance

We plan to further improve mha-finance as a reproducible and research-oriented financial analysis framework. Future development will include richer statistical diagnostics, improved visualization utilities, support for extended horizons, and more modular analytical tools for experimentation and custom workflows.

Further, we want to develop the framework to be easier to use by students, researchers, and developers that want to understand financial behavior through descriptive and interpretable systems rather than predictive systems only.

Built With

- ewma-volatility-estimation

- git

- modular-trigger-based-apis

- numpy

- pandas

- python

- rolling-window-estimation

- scikit-learn

- statistical-modeling

- time-series-analysis

- unsupervised-regime-characterization

- yfinance

Log in or sign up for Devpost to join the conversation.