Inspiration

We wanted to know if you could measure the moment public attention outruns the media, and whether that gap predicts anything about asset prices during major world events.

What it does

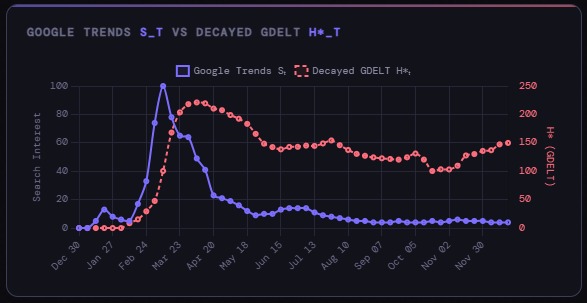

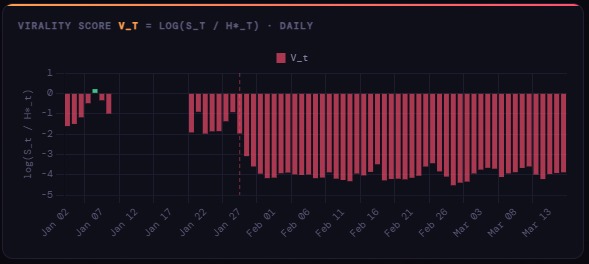

It takes three data sources , GDELT news headlines, Google Trends search interest, and asset prices, and computes a daily Virality Score that captures whether the public is searching for something more than journalists are writing about it. We tested it across four events: the COVID crash, the GameStop squeeze, the DeepSeek shock, and the Bitcoin bull run.

How we built it

Python for data processing and statistics, Chart.js for interactive dashboards, and a custom decay model (exponentially weighted headline stock) that lets you tune how fast media memory fades using a live λ slider.

Challenges we ran into

The three data sources never align perfectly, GDELT is daily, Google Trends was monthly for Bitcoin, and stock markets are closed on weekends while crypto never is. Getting a clean merged pipeline across four different events with different frequencies and time windows took most of the work.

Accomplishments that we're proud of

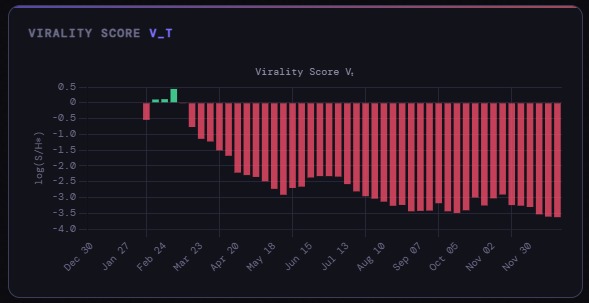

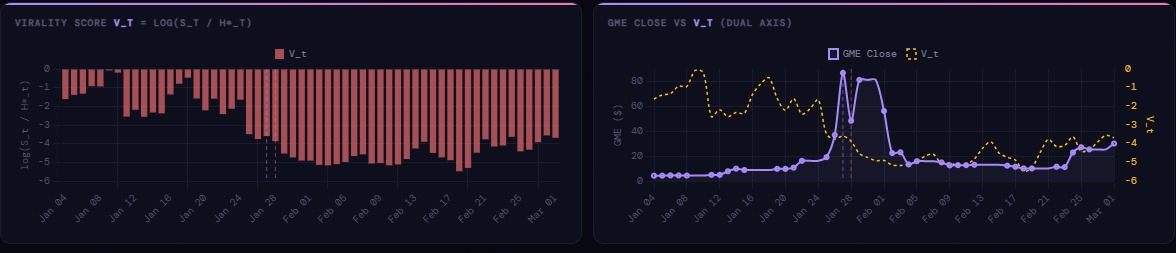

Finding that positive virality almost never occurs for mature assets is a genuinely surprising result we didn't expect going in.

What we learned

Markets move before the signal turns positive. Vt is a trailing indicator, by the time public attention visibly outpaces headlines, the price has already moved. Saturation is the normal state for high-coverage assets like Bitcoin.

What's next for Metal Cooler

Extend to daily Google Trends for Bitcoin to catch the brief positive-V windows within bull runs, add more assets and crises for cross-event comparison, and explore whether the rate of change of Vt (rather than its level) has predictive power with further analysis.

Built With

- api

- python

Log in or sign up for Devpost to join the conversation.