-

-

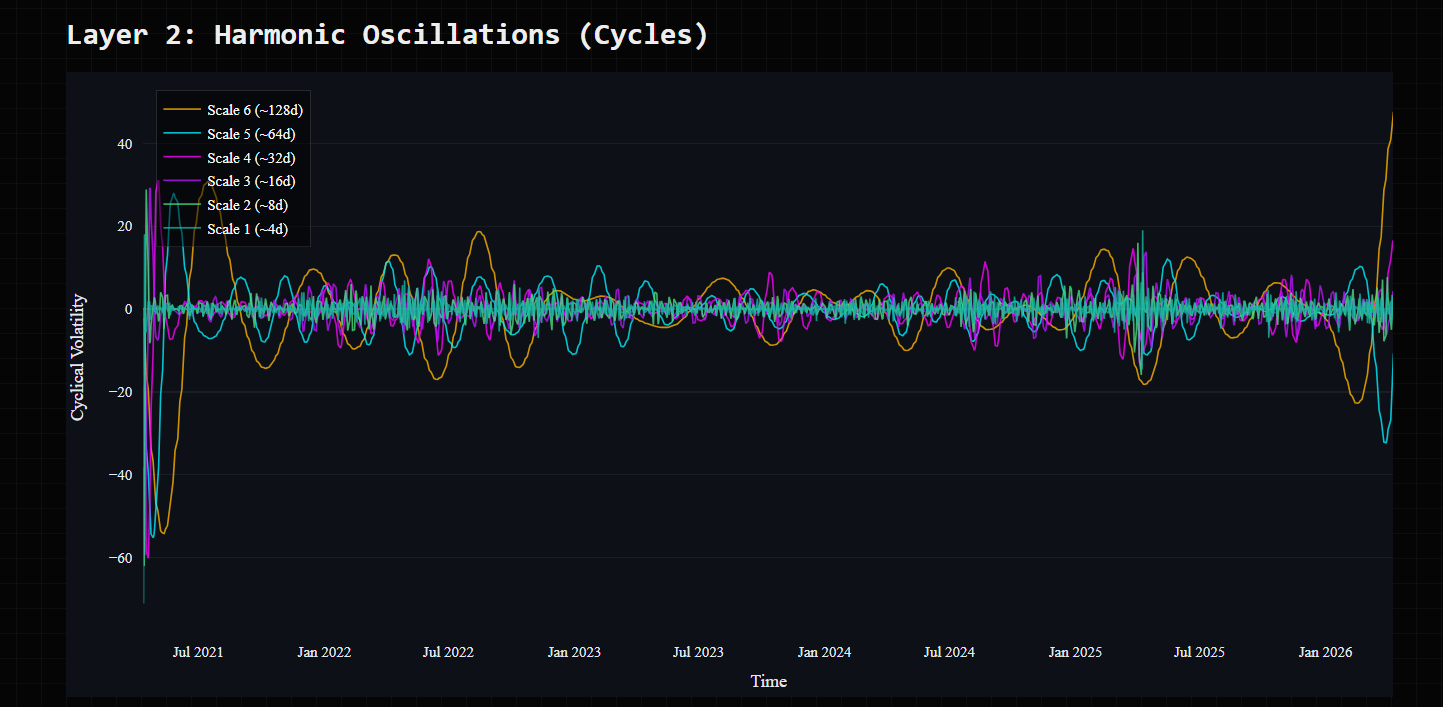

Decomposed Signal into different time periods

-

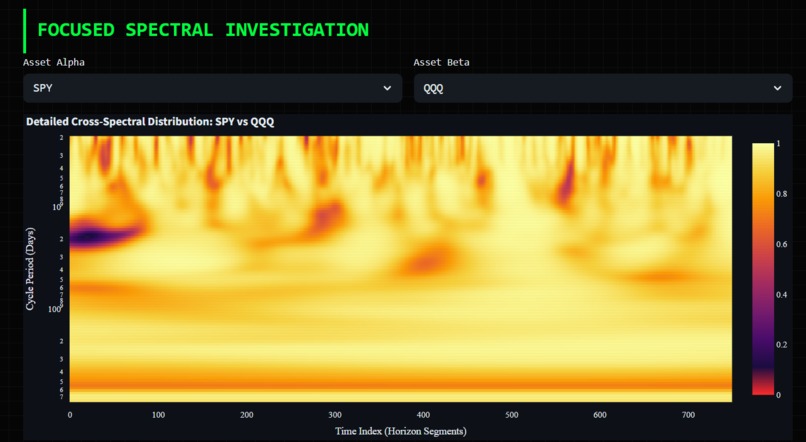

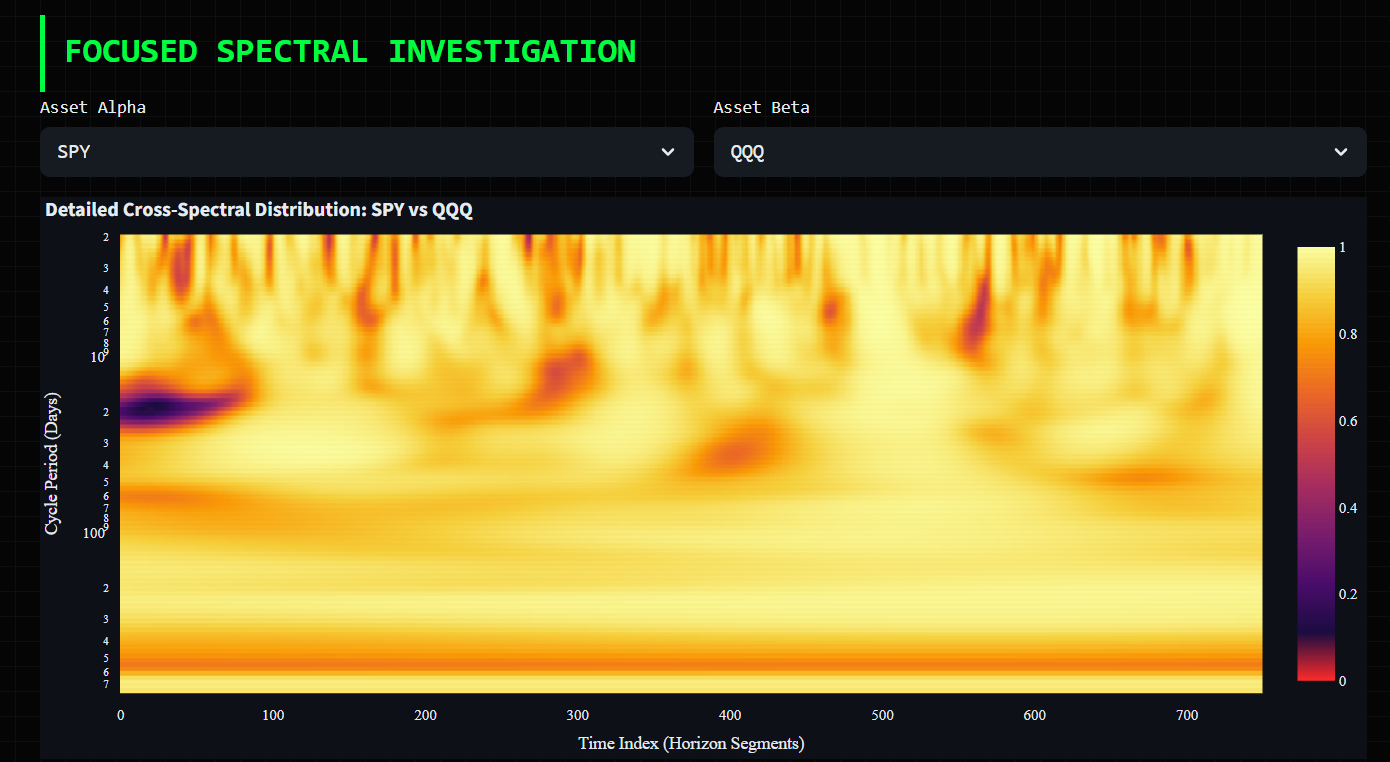

Correlation heat map of two assets

-

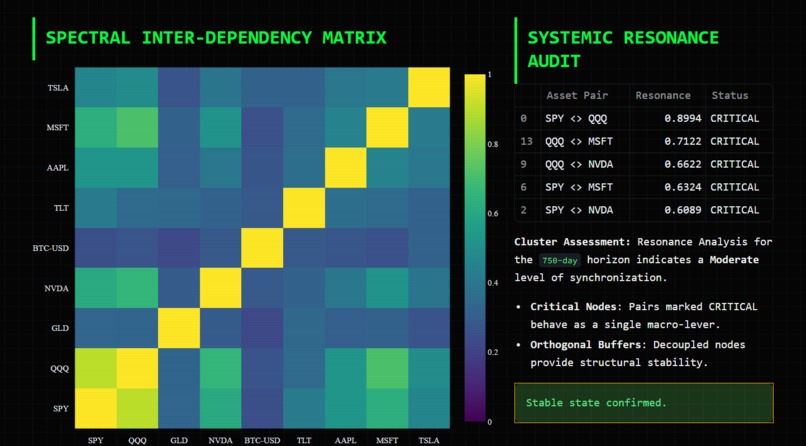

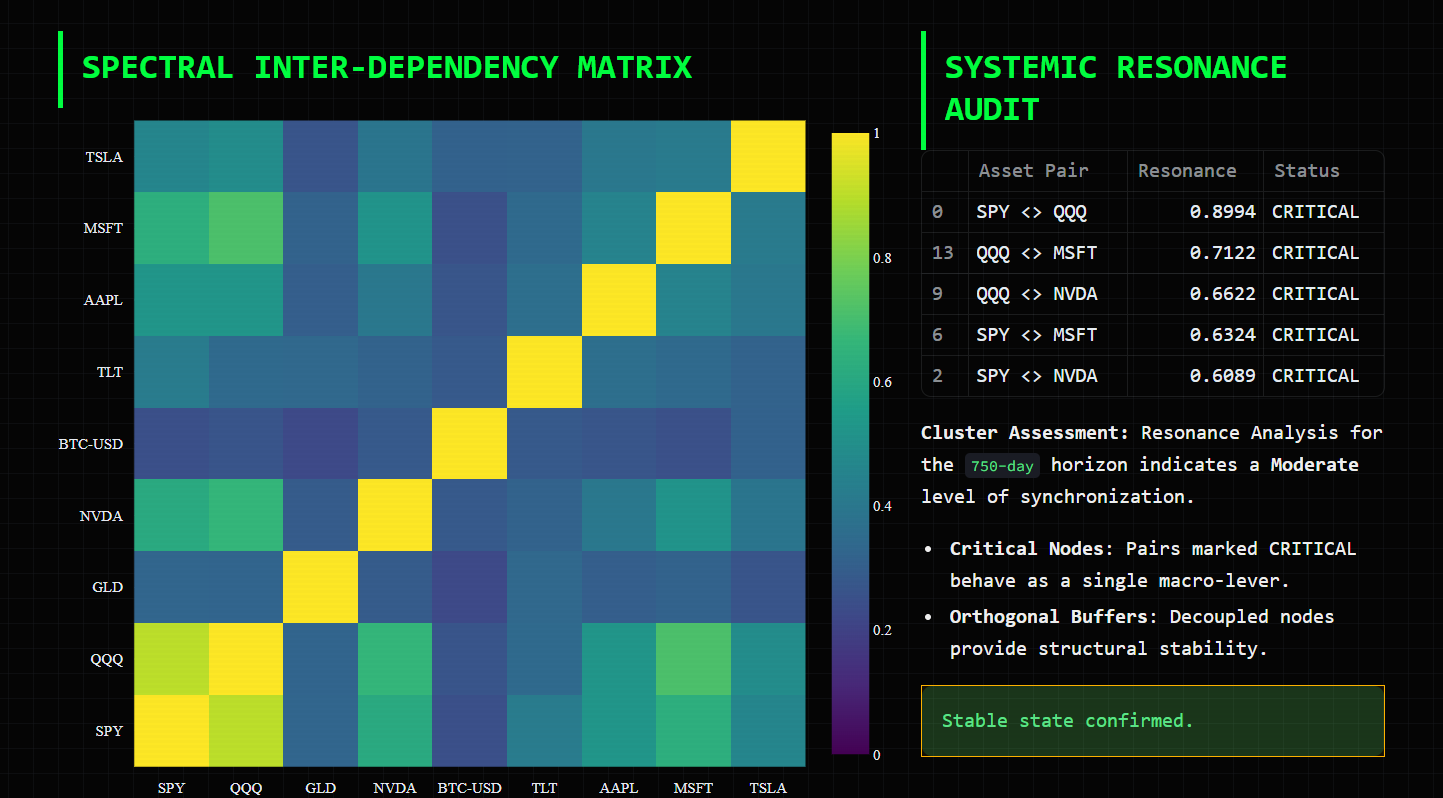

Asset correlation heatmap

Please read the 'docs' in the GitHub Repo for the full technical and algorithmic breakdown. I'm using this space as more of a qualitative journey, and the technical execution is there. Thank you!

This is also my first time properly doing a Devpost hackathon, which wasn't local and run through Devpost.

Additionally, whilst the video is long, I have sped it up to be within the time period, and I hope this is acceptable

Inspiration

As an engineer, I specialize in analyzing the hidden rhythms of the physical world. When I turned my attention to finance, the vast majority of market participants rely on Time-Domain indicators like Moving Averages or RSI. From a DSP perspective, these are essentially primitive low-pass filters that introduce significant phase lag, the temporal delay between a market event and its signal detection. In modern, high-frequency regimes, this lag is the difference between alpha and liquidation. I was inspired by the realization that I could use my refined DSP skills to shift analysis into the Frequency Domain, decomposing price action into its constituent "Market DNA" to identify structural shifts before they manifest in lagging, reactive indicators.

What it does

The Market DNA Engine is a tactical command center providing Institutional Spectral Intelligence. It utilizes Multiresolution Analysis (MRA) to slice raw price action into orthogonal frequency bands, separating the underlying "Macro Drift" from the "Stochastic Noise." Unlike traditional tools, it provides clinical Execution Playbooks, dynamic if/then protocols based on a "Spectral Stance" score that weights momentum across multiple scales. By integrating Spectral Granger Causality and Cross-Wavelet Coherence, the engine identifies the direction of information flow between assets, allowing traders to trade laggards based on the real-time signatures of leaders.

How I built it

The project was architected on a modular Python-based Spectral Pipeline." I used PyWavelets and ssqueezepy to handle the heavy mathematical lifting of Wavelet Decomposition and Synchrosqueezing.

- Decomposition Engine: I implemented Daubechies (db4) for temporal precision and Symlets (sym8) for phase symmetry, ensuring the extracted rhythms were both sharp and synchronized.

- Intelligence Layer: A custom-weighted momentum engine that aggregates "force" across scales (Structural, Quarterly, Monthly, Weekly) to generate a unified regime classification.

- HUD Design: The Slate-Carbon Tactical HUD was built using Streamlit and Plotly, designed for high-density data visualization and low-latency decision mapping, utilizing JetBrains Mono for maximal numerical legibility.

Challenges we ran into

The primary challenge was the Financial Non-Stationarity problem. Unlike acoustic or mechanical waves, market signals aren't stable; their frequencies and phases shift constantly. Bridging our theoretical engineering knowledge to the messy reality of "Applied DSP" required a steep learning curve. I had to account for "Market Ecology", how the entry of a large participant can distort the spectral signature. Furthermore, working within an extremely compressed time frame forced us to prioritize high-fidelity signal alignment over simple feature bloating, ensuring that every calculation served a direct execution goal.

Accomplishments that I'm proud of

I'm particularly proud of our Spectral Information Transfer Delta. Successfully quantifying "Information Flow" using Geweke measures—and seeing it accurately identify leading indicators like BTC driving broader market sentiment—was a major technical validation. We are also proud of the Spectral Forecast (T+14) vector, which uses first-order derivative extrapolation of the structural baseline to project a "Market Future" that accounts for both trend and cyclical phase-lock.

What we learned

This project reinforced the engineering principle that "Context is King." We learned that a signal’s relevance is entirely dependent on its frequency band; volatility on a 5-minute scale is noise to a macro trend, but a signal to a scalper. We also learned how to militantly defend against Spectral Decay (overfitting). By hardcoding Out-of-Sample (OOS) Validation and Kelly Criterion sizing into our backtesting logic, we ensured that our "alpha" was robust and statistically significant, rather than just an artifact of in-sample curve fitting.

What's next for Market DNA

Market DNA is moving toward a Fully Autonomous HFT Cluster. We are currently researching the integration of Deep Learning models that can "self-correct" the wavelet depth based on shifting market volatility regimes. Our roadmap includes expanding the "Portfolio Sync" engine into a global resonance map, handling hundreds of assets to identify systemic contagion points before they trigger macro market shocks. You can also hook up different API's for live data, or larger sets (this feature has been built in for scalability, just not used)

Log in or sign up for Devpost to join the conversation.