-

Our solution

-

Current problem

-

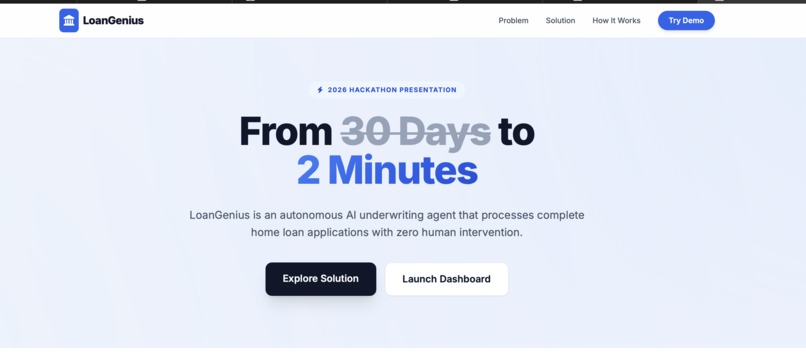

LoanGenius: AI powered loan underwriting agent

The Story of LoanGenius

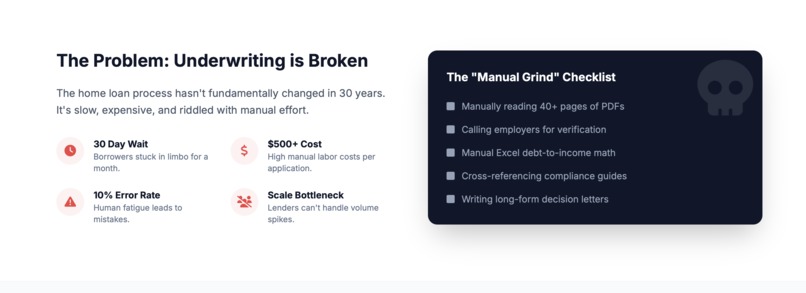

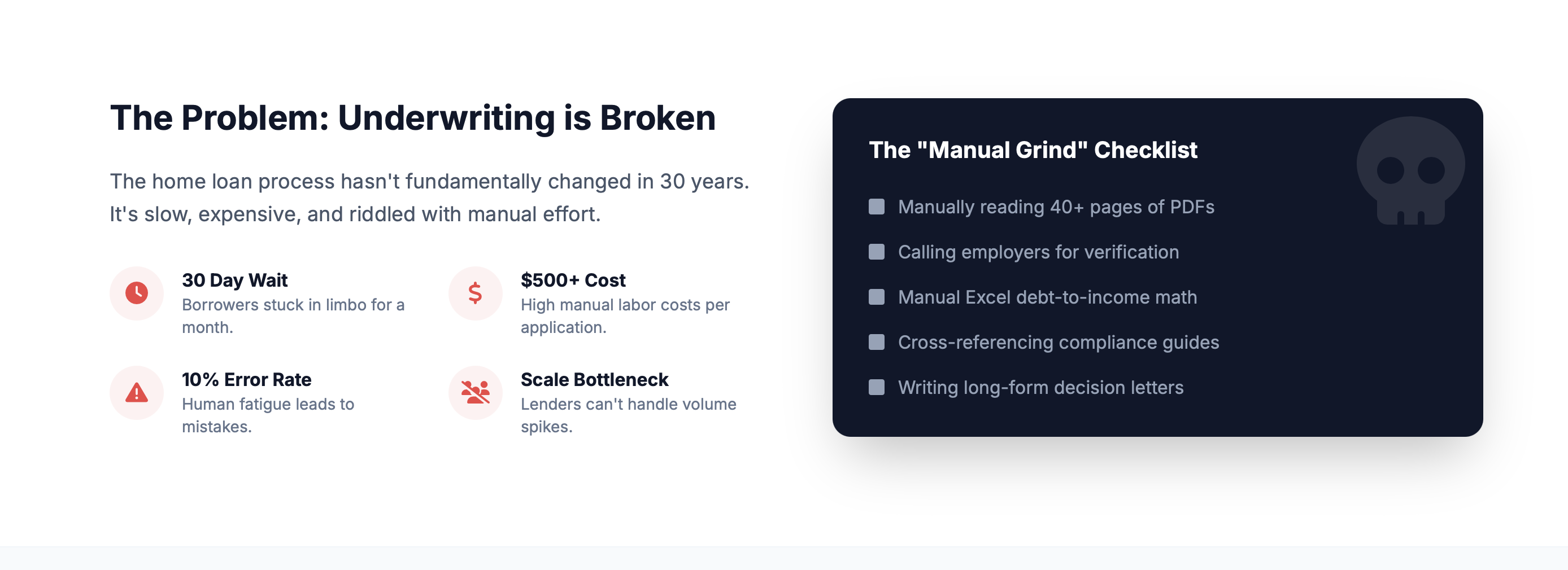

The Problem: The 30-Day "Black Hole"

Current home loan underwriting is fundamentally broken. It’s a manual, grueling process that hasn't changed in decades:

- ⏳ The Wait: Borrowers are stuck in limbo for an average of 30 days.

- 💸 The Cost: Lenders spend over $500 per application just on manual labor.

- 📉 The Errors: Humans get tired. Manual "stare and compare" document reviews lead to a 5-10% error rate.

- The Manual Grind: Underwriters spend hours on the phone verifying employment and cross-checking paper checklists for compliance.

- The Inconsistency: The same application can get two different decisions from two different people.

In short, it’s a slow, expensive, and inconsistent mess that causes borrowers to lose their dream homes and lenders to lose millions in operational waste.

🌟 The "Aha!" Moment

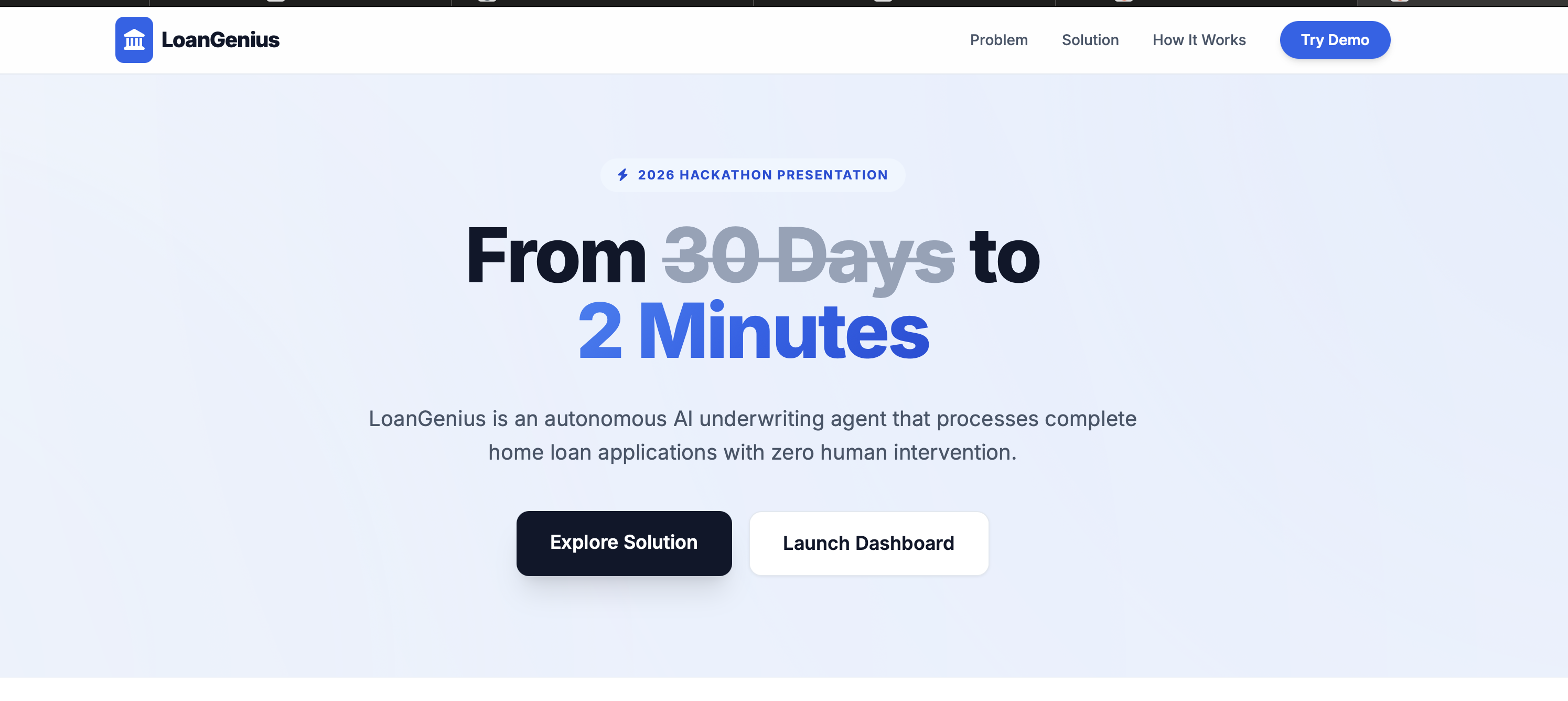

We realized that it’s 2026—AI can write code, generate art, and drive cars, yet we’re still waiting a month for a human to read a PDF.

Our "Aha!" moment was realizing we could build a fully autonomous agent that doesn't just assist humans, but actually replaces the manual grind. We saw a future where a borrower could upload their files and get a compliant, auditable, and verified decision in 2 minutes instead of 30 days.

How We Built It (The Digital Underwriter)

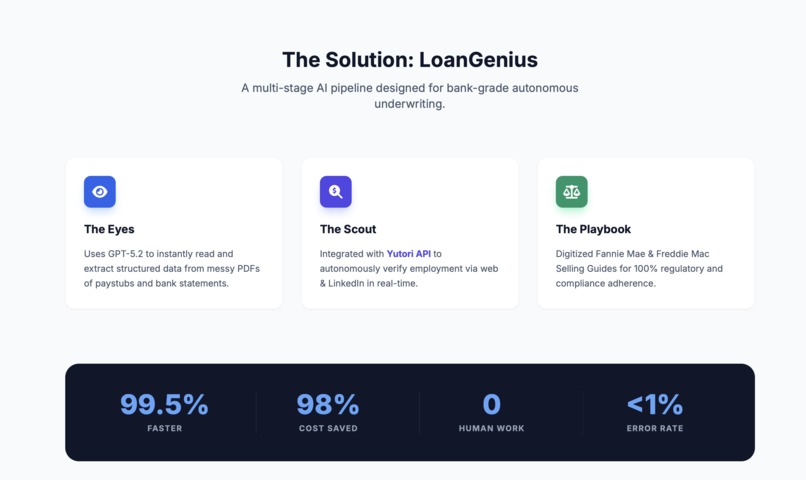

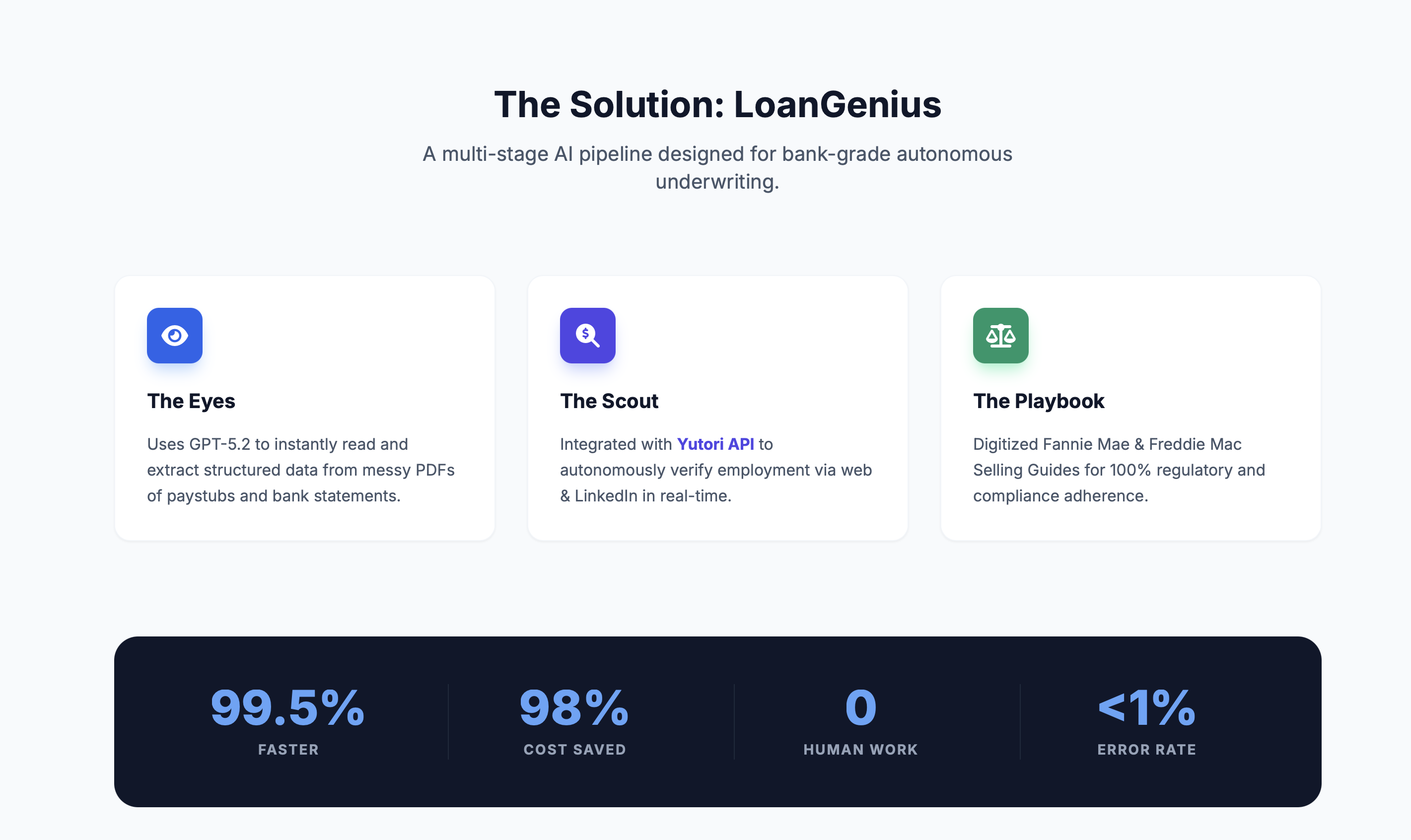

We built LoanGenius as a multi-stage AI pipeline designed for total autonomy:

- The Eyes (OpenAI): We used GPT-5.2 to act as the agent's eyes. It reads messy PDFs of paystubs, bank statements, and credit reports, instantly extracting the financial data needed for a decision.

- The Scout (Yutori API): To solve the "manual verification" problem, we integrated the Yutori API. Instead of a human calling an employer, our agent autonomously scouts the web and LinkedIn to verify employment in real-time.

- The Playbook (Fannie Mae): We digitized the Fannie Mae and Freddie Mac Selling Guides. Our agent follows these industry "playbooks" to the letter, ensuring 100% regulatory compliance.

- The Narrator (Claude): We used Anthropic Claude to turn raw data into a professional, human-readable underwriting report so the decision is always explainable.

The Math Behind the Magic

To ensure the agent makes objective, bank-grade decisions, we implemented standard mortgage formulas:

Debt-to-Income (DTI) Ratio: [ DTI = \frac{\text{Monthly Debt Payments}}{\text{Monthly Gross Income}} ] Our agent enforces the strict 43% limit for Qualified Mortgages.

Loan-to-Value (LTV) Ratio: [ LTV = \frac{\text{Loan Amount}}{\text{Property Value}} ]

Risk Scoring: The agent calculates a weighted risk score ($R$) to ensure the loan is a safe bet: [ R = 10 \cdot \left( 0.4 \cdot \frac{\text{Credit}}{850} + 0.3 \cdot \text{Income Score} + 0.3 \cdot \text{Equity Score} \right) ]

Challenges We Faced

The road to 2-minute underwriting wasn't easy:

- Noisy Data: Teaching an AI to read a blurry, scanned bank statement from a home printer was our biggest technical hurdle. We had to refine our extraction logic to handle "noisy" text without losing accuracy.

- Trust & Transparency: Lenders won't trust a "Black Box." We had to build a system that doesn't just give a "Yes," but actually cites the specific guidelines and verification sources it used.

- Real-Time Scouting: Web-based verification takes time. We had to engineer a live "Processing Dashboard" so users can watch the agent work its way through the verification steps in real-time.

LoanGenius: Moving from 30 days to 2 minutes. From $500 to $10. From a black hole to total clarity.

Built With

- anthropic

- mongodb

- openai

- typescript

- yutori

Log in or sign up for Devpost to join the conversation.