-

-

sign up

-

log in

-

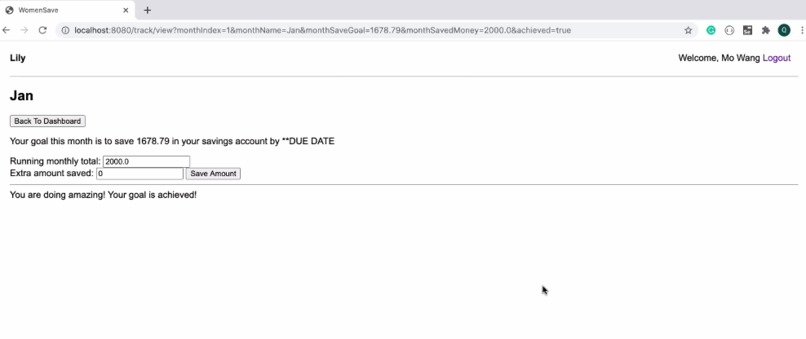

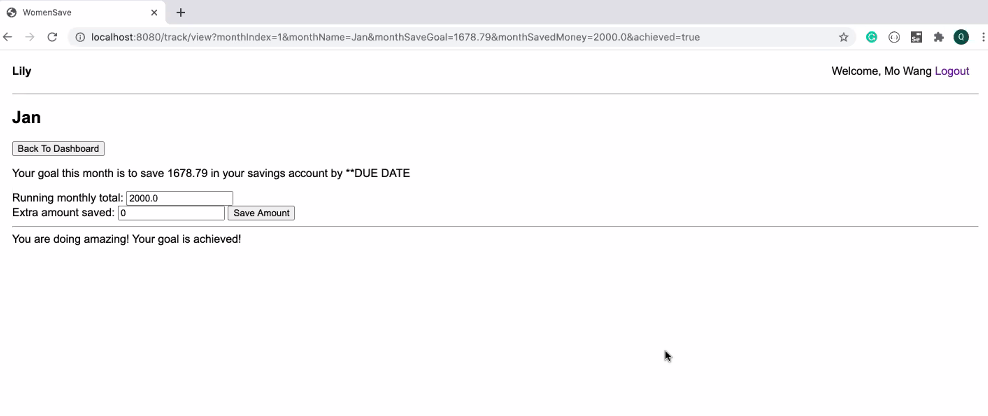

track

-

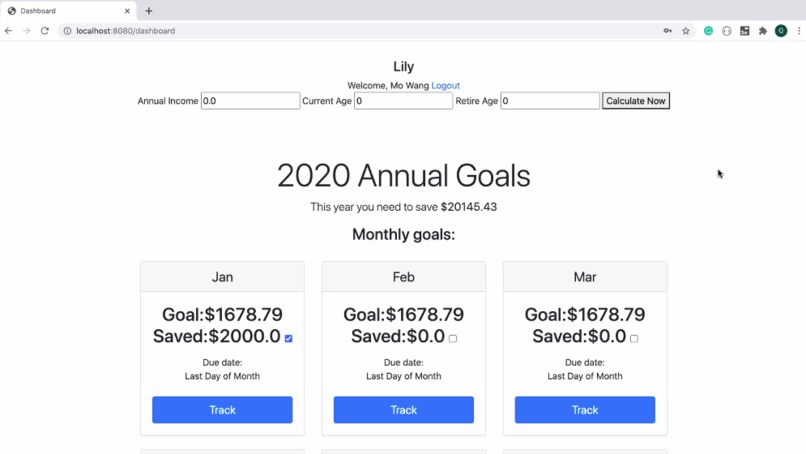

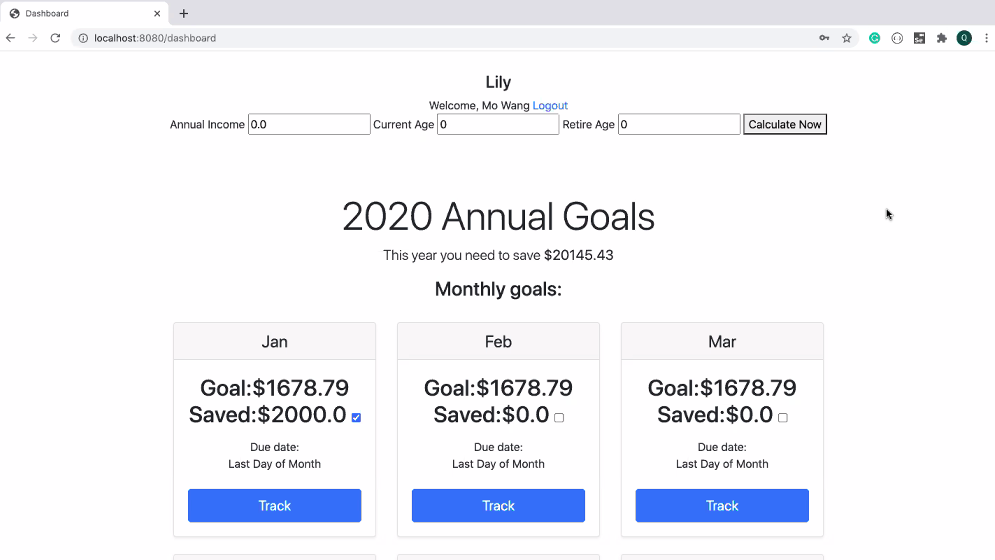

dashboard

Inspiration

What motivated us was the lack of financial and retirement planning resources available for women, femme and non-binary individulas in the market. Gen-Z and Millenial women are not saving enough. 39% of single women and 46% of married women are at risk of being unable to maintain pre-retirement standard of living at retirement. - Prudential Financial.

The factors that contribte to lack of retirement planning are:

- the gender pay gap. Women on average earn 20% less than men. Over a lifetime , we make over $400, 000 less!

- We live on average 5 years longer than men. We face rising health care costs at a higher inflation rate.

- We spend an average of **12 fewer years in the workforce*8, which means lower lifetime earnings.

We can’t afford to ignore this. Our future mental health, physical health, and standard of living are getting affected by these issues now.

We deserve better.

We are on a mission to disrupt the financial landscape and bridge the financial inequality.

Our vision is to help all femme, female-identifying and non-binary individuals save consistently towards their future with a peace of mind.

What it does

Lily is a retirement savings calculator and tracker.

We take in users' current income, current age and expected retirement age.

We calculate their pre-retirement income, savings required at time of retirement and the monthly savings amount. Our built-in tracker helps ensure consistency and tracks any savings deposits.

How we built it

We first listed the essential features that we would need, which would be the calculator, the tracker function and the login and sign up pages.

We developed wireframes on Figma and Miro to understand the user flow under different scenarios such as if the user saved enough for that month and if the user did not save up enough for that month.

We developed the mathematical formula to calculate the pre-retirement income, savings required at time of retirement and the monthly savings amount. This was done vis reseraching what inputs othr retiremnet planners use.

Our developers built the front end based on the wireframe specs and also built translated the formula and the tracking function and logic into the back end using Java, Thymeleaf, Spring, SpringBoot and MariaDB. Backend Our backend Strategy is:

Use Spring Boot to set up whole project first. Steps to develop back-end function:

- database set up with models/tables

- logic for controller and helper function

- integrate front-end with login/register feature

- integrate front-end with dashboard feature

- create track webpage and integrate with back-end track feature

Note: Use wireframes as guide for later integration with front-end webpages

Challenges we ran into

Time constraints. We had to reduce the scope of our Phase 1 solution due to time constraints. We extended our scope to integrate women femme-centric factor into Phase 2.

Complexity. The tracker function and retirement savings formula were initially very complex. We had to reduce the amount of inputs and factors we would take in to build our Phase 1 demo. We also decided to go for manual entry form the user side.

We had a difficult time to integrate the backend with the landing page.

We had problems with resolving merge conflicts in Github.

Accomplishments that we're proud of

We have successfully integrated our retirement savings formula from the back-end to the front-end and we have a working page that calculates the monthly savings amount based on the current income.

We also have successfully developed a manual tracking tool that updates correctly if the monthly savings has been met or not.

What we learned

- Next time, we will definitely reducing the scope further for a hackathon and build something simpler.

- We also aim to be more familiar with the GitHub and the tools that we use to prevent any big crashes or merge conflicts in the future.

- We also learned that it is important to make sure that we need differentiate our product by including factors in our savings formula that affect women, femme and non-binary individuals. We have addressed that in our extended Phase 2 scope.

What's next for Lily

In Phase 2 , we will be extending the features of Lily to include more factors that impact women and femme-identifying individuals.

We aim to capture the user’s current spending habits, any additional income, planned absences, and the current inflation rate to provide more accurate and feasible annual and monthly saving goals.

We are also planning to automate data transfer between the user’s bank account and Lily to provide automatic savings recommendations and to rapidly track savings deposits. This will eliminate the user from having to manually input their deposits every month.

We have thought carefully of the security considerations we will need to take.

Authentication: We require the use of a unique PIN and authentication code each time you login. This is supported by VeriSign, the leading online certificate authority. **Privacy: We use SSL to safeguard all data and ensure secure internet connectivity. Integrity: All Banking details are stored in an encrypted state using RSA and are “read only” . No one at Lily is able to view or access it, even from the back end.

We hope to continue to build and iterate Lily and move towards creating financial, social and economical equality for all. Thank you!

Log in or sign up for Devpost to join the conversation.