Inspiration

Coming from a background in Banking IT within major Austrian banks, we are fully aware that compliance with regulations presents an ever-growing challenge to financial institutions around the world. With regulators taking a closer look at crypto markets, providers of innovative financial solutions such as on the XRP ledger will not be spared from implementing these regulations.

What it does

To simplify compliance for innovative blockchain-based payment solutions with Anti-Money Laundering and Counter-Terrorism Financing regulations and sanctions, we provide a smart contract-based transaction monitoring system on the XRP ledger using Multi-Signing and Escrows.

The system is notified of transactions by the ledger and then performs automated checks such as AI-based recognition of suspicious transactions patterns and checking credentials of payer and payee against publicly available sanction lists.

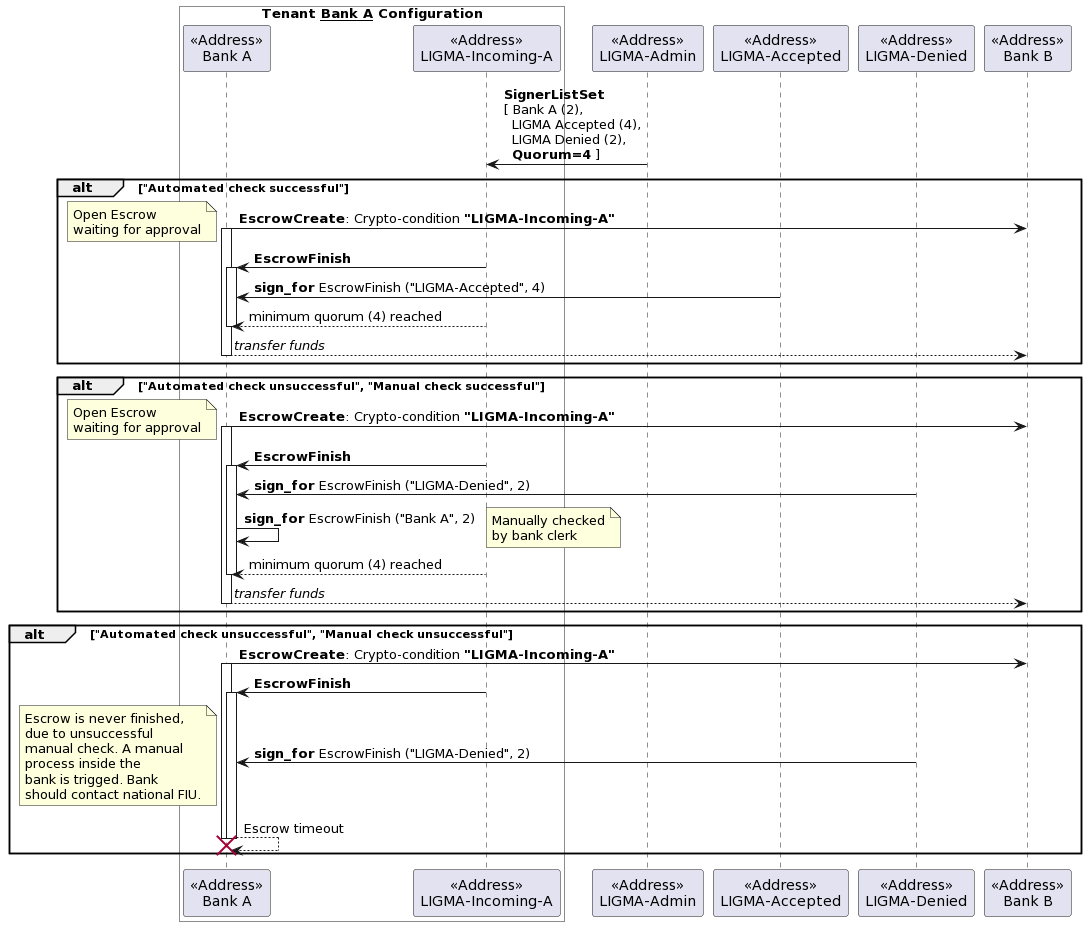

How we built it

The sending institution (Bank A) creates an Escrow with the crypto-condition by LIGMA-Incoming.

Note: the sending institution must first manually register with LIGMA so that its respective LIGMA-Incoming address is set up. This account contains the signer list necessary for manual approval.

Once the Escrow is created, a server run by LIGMA is notified and performs automated checks against sanctions lists and AI-based anomaly detection. In case the checks succeed and no suspicious activity could be found, the server sends an EscrowFinish transaction with the crypto condition from Bank A's "LIGMA Incoming" address and the funds are forwarded to the recipient institution.

If suspicious activity was detected, the server sends an EscrowFinish transaction from the "LIGMA-Denied" address which has a lower-than-required quorum on LIGMA-Incoming-A's signer list, enabling the bank to manually approve the transaction. Due to signatures being stored publicly on the XRP ledger, auditors can easily reason about whether a transaction has been approved manually.

If Bank A does not approve the transaction in due time, funds are returned to Bank A and the transaction is cancelled. The timespan for the bank to approve the transaction must be long enough for the bank to be able to contact its respective Financial Intelligence Unit to discuss further steps.

Challenges we ran into

Getting to know the XRP ledger's features in order to map out the transaction workflow such that it is compliant with EU regulations about AML and CTF.

Accomplishments that we're proud of

We think that the XRP ledger's built-in smart contract capabilities have been put to good use to build this transaction monitoring and verification solution.

What we learned

After thorough study of the ledger's capabilities, we both are fascinated by the potential that its fundamental features present for building secure, innovative payment solutions of tomorrow.

What's next for LIGMA

If we get good feedback: build it!

Built With

- ripple

- xrpl

Log in or sign up for Devpost to join the conversation.