-

-

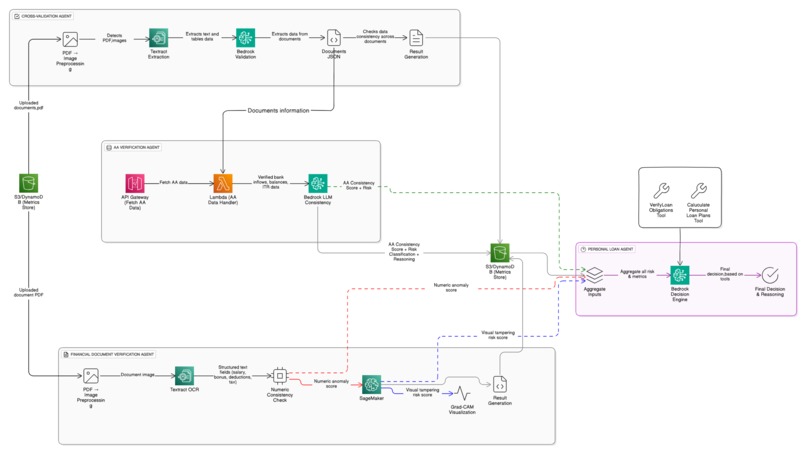

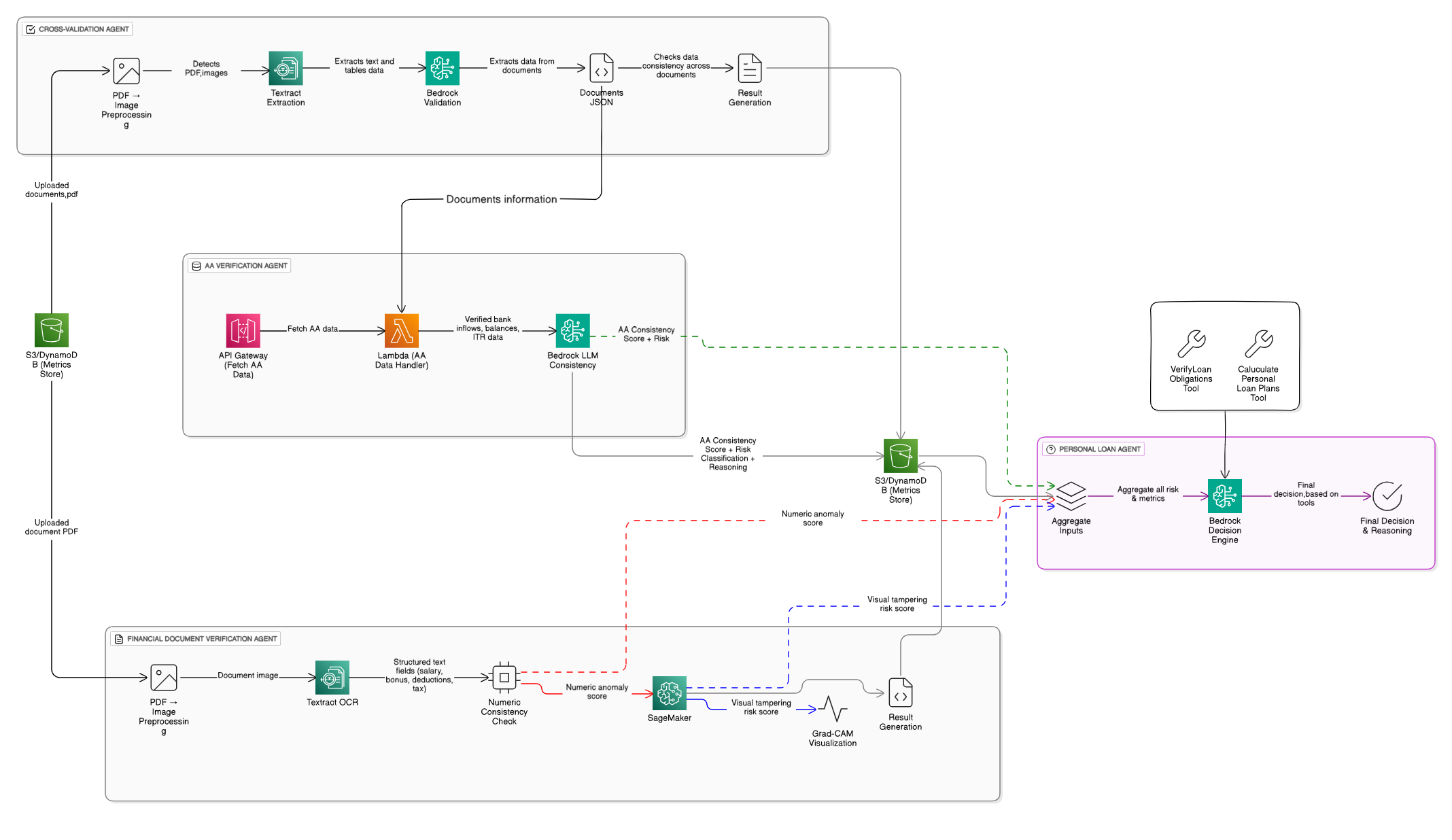

Architecture

Inspiration

The LendIQ Story: Built To Make “Yes” Fair, Fast, and Honest Prologue: A Room Full of Rejections We started LendIQ after a month that felt like a mirror held to everything broken in lending. A teammate’s sister, a nurse with spotless records, was denied twice for a small personal loan—no explanation, no appeal path, just silence. That same week, a mid-sized lender told us they were seeing a surge in forged documents—some so polished that even senior officers missed them. Two truths, one pain: honest borrowers waited, while sophisticated fraud slipped through.

Sitting around a whiteboard late one evening, we wrote six words we wished were true for everyone: “Fair decisions. In minutes. With proof.”

That was the moment LendIQ began.

Why We Built It To protect dignity. No one should beg for a loan they rightfully deserve. To restore trust. Lenders should never have to choose between speed and safety. To fight quiet biases. Good people are too often penalized by manual, inconsistent, or opaque processes. To bring light to decisions. A “no” without reasons is a closed door; a reasoned answer is a path forward. What We Built (In Plain Words) We built a system where several specialized AI agents work together like a good team:

Document Analyzer: Spots subtle signs of tampering in payslips, offers, statements, and tax forms—then shows why, not just what. Cross Validator: Checks if numbers and names line up across documents the way they should. Account Aggregator Verifier: Confirms that what documents state matches account data wherever possible. Decision Agent: Weighs risk, income, and obligations to suggest a decision—always with a clear explanation. Finalizer: Consolidates evidence, storing it transparently so auditors, applicants, and lenders can all understand the “why.” We obsessed over one idea: if a decision affects someone’s life, it must be explainable.

Three Real Moments That Kept Us Going Anika, the nurse. We ran her anonymized documents through our workflow. The system flagged no tampering, matched her income across files, calculated a healthy DTI, and produced a clean, step-by-step justification. The loan officer told us, “For the first time, I can defend a ‘yes’ with evidence.” Ravi, the loan officer. He’d been trained to “trust instincts,” which also meant carrying the weight of being wrong. With LendIQ, he wasn’t guessing—he was reviewing explanations, heatmaps, and matches. He said, “It feels like I’m not alone anymore.” Meera, the risk head. She didn’t want more approvals; she wanted better ones. She liked that every decision had a trail—what matched, what didn’t, and where human review was required. “We’re not just faster—we’re accountable,” she said. None of these are miracles. They’re what happens when you replace speculation with clarity.

What Changes When This Exists For borrowers: Decisions in minutes, reasons they can understand, and respect maintained even in a “no.” For loan officers: Less time on paperwork, more time on people; fewer errors, more confidence. For lenders: Consistent decisions, defensible outcomes, and a system that scales without losing integrity. For society: More honest approvals, fewer fraudulent payouts, and a fairer path to opportunity. Our North Star Principles Fairness over speed; speed through fairness. Transparency over mystery. Human judgment augmented, never replaced. Proof first, opinion second. A Day We’ll Always Remember We were testing an early version when a case arrived that looked ordinary. The documents were pristine—too pristine. The analyzer surfaced a small but consistent artifact in one page of the bank statement. The cross validator found timing mismatches across salary credits. The system didn’t loudly cry fraud; it quietly asked for a human review and explained why. When the manual team dug deeper, they found the inconsistencies were real.

That day, an undeserved approval didn’t happen—and a real borrower somewhere else got their answer faster. That balance is the heart of LendIQ.

What We Hope People Appreciate LendIQ isn’t about replacing trust. It’s about earning it—by showing our work, telling the truth, and making decisions that people can inspect, challenge, and understand. If technology is power, then transparency is how we use it responsibly.

Epilogue: The Promise We didn’t build LendIQ to make loans easier. We built it to make them fair. If we do our jobs right, a single parent gets a timely “yes,” a lender keeps a promise to be prudent, and the system becomes a little more human—even as it becomes more intelligent.

That’s the story we’re writing every day: not just with code, but with conscience.

What it does

End-to-end loan verification and decisioning that’s fast, explainable, and fraud-aware. Runs a multi-agent pipeline: Document Analyzer detects tampering in PDFs/images using ResNet50 + ELA + noise stats with Grad-CAM heatmaps for explainability. Cross Validator matches identity, salary, tax, and dates across payslip, offer, bank statement, and Form-16. AA Agent verifies numbers against Account Aggregator JSON. Decision Agent (LLM on Bedrock) composes a clear decision with risk, DTI, eligibility, and loan plans. Finalizer compiles results and persists artifacts. UI Dashboard to run the workflow per customer, view decisions, track escalations and approved loans, and download artifacts.

How we built it

Backend: backend/main.py (FastAPI + Uvicorn) Endpoints to run orchestration (/run_workflow) and fetch results (/results/{customer_id}). Uses boto3 to read/write from S3 bucket documents-loaniq under per-customer folders. Orchestration: orchestration_strands.py Parallel: document analysis + cross-validation. Sequential: AA verification → decision agent → finalization. Passes structured state through each agent. Decision Agent: decision_agent_strands.py Tools: extract_financial_data(path) and calculate_loan_plans("Calculate loan for {amount} using {path}") . Dynamically reads loan_amount_requested from AA_data.json in S3/local. Document forensics: combined_agents.py ResNet50 feature maps + Grad-CAM overlays. Error Level Analysis and noise statistics to reduce false positives. Frontend: frontend/src/App.jsx (+ MUI) React dashboard with tabs for end-to-end run, outcomes, and lists (approved/escalations). Storage & artifacts: Per-customer directory in S3 (e.g., LID.../): uploads docs, results.json , Grad-CAM images, and AA JSON. Explainability by design: Every decision includes evidence: cross-check summaries, risk factors, DTI, eligibility, heatmaps.

Challenges we ran into

Document diversity: Varying PDF/image quality and layouts required robust preprocessing and fallback heuristics. False positives in tampering: Tuned ensemble thresholds and added Grad-CAM evidence to avoid over-flagging. Cross-document alignment: Normalizing names, dates, and salary fields across different formats. Windows PDF pipeline: Poppler installation and path management on Windows dev setups. Consistent environments: Ensuring deterministic builds (e.g., keeping package-lock.json), caching issues in the UI, and explicit S3 object keys. Human-readable outputs: Designing LLM prompts to return strictly structured JSON and plain-text explanations suitable for UI rendering.

Accomplishments that we're proud of

Agentic orchestration with clear parallel/sequential stages that cut latency. Explainable AI: Grad-CAM overlays and evidence-first decisions, not black-box outputs. Reliable S3-first workflows: All major artifacts are persisted per customer, enabling auditability. Dynamic loan planning: Loan plans tuned to requested amount from AA_data.json . Resilient UX: Clean UI states, graceful fallbacks, and dummy-data mode for safe demos.

What we learned

Explainability wins trust: Heatmaps + cross-validation diffs dramatically improve stakeholder confidence. Prompt grounding matters: Tool-invocation prompts with strict schemas reduce LLM variability. Data contracts > code: Stable S3 key structure and JSON schemas simplified the entire pipeline. Feature toggles are essential: Being able to switch between real results.json and dummy_results.json accelerates demos and testing. Small details save hours: Poppler, CORS, caching, and version locks can derail timelines if not handled early.

What's next for LendIQ

Production AA integration (ReBIT-compliant, consented data flows). Advanced OCR + layout parsing (Textract/Tesseract + layout models) for unstructured docs. Credit bureau & fraud graph signals integrated into risk scoring. Streaming progress updates in UI and webhooks for downstream systems. Policy simulation: Sandbox different risk policies and see approval/portfolio impact. Security & compliance: Signed document verification, encryption by default, audit trails, and role-based access. Autoscaling & multi-tenant support for enterprise deployments. Summary Provided a concise, submission-ready write-up under each requested section, grounded in your current architecture and code files ( backend/main.py , orchestration_strands.py, decision_agent_strands.py, combined_agents.py , frontend/src/App.jsx )

Built With

- amazon-ec2

- amazon-web-services

- awsiam

- awstextract

- axios

- bedrock

- ensemble

- fastapi

- git

- github

- gradcam

- javascript

- llm

- matplotlib

- numpy

- opencv

- pypdf

- python

- pythorch

- react

- restnet50

- s3

- sagemaker

- scikit-learn

- skimage

- strands

- transferlearning

- uvicorn

Log in or sign up for Devpost to join the conversation.