-

-

Manager profile

Inspiration

Most existing loan systems alert lenders only after an EMI default occurs. From real-world observation, we found that lenders lack visibility into borrower behavior before defaults, leading to delayed action, higher risk, and manual follow-ups. This inspired us to design a system focused on proactive monitoring, early risk detection, and transparency, without changing existing loan workflows.

What it does

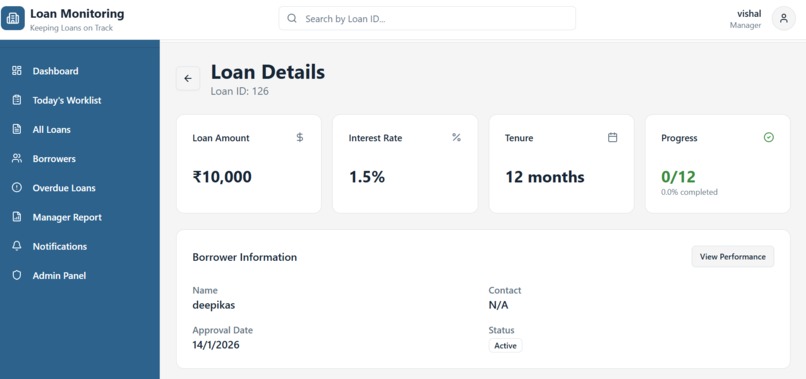

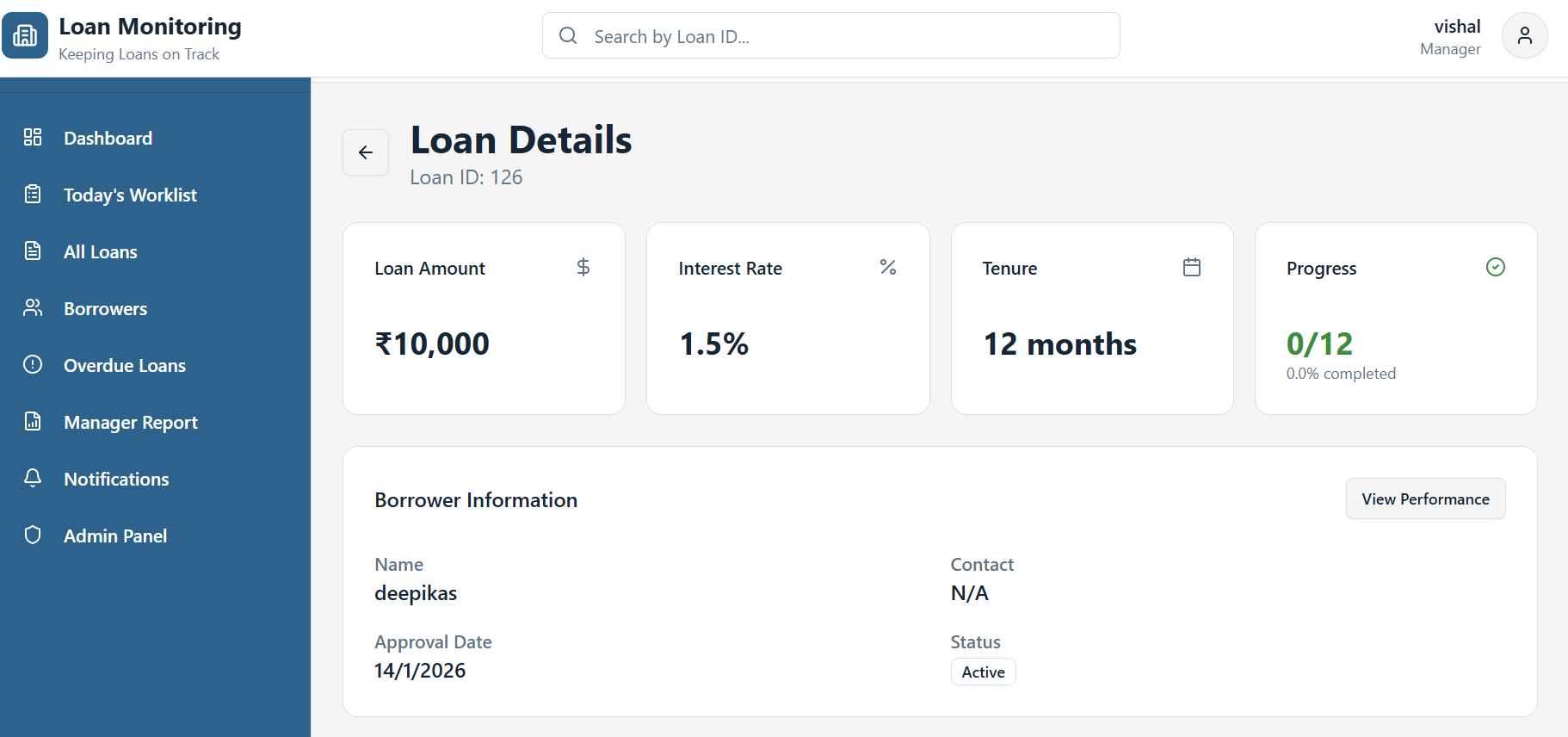

Keeping Loans On Track continuously monitors loan performance using day-wise repayment behavior, provides AI-assisted risk insights, and enables role-based governance across supervisors, managers, and borrowers. It helps lenders identify early warning signals, prioritize follow-ups, and make informed re-loan decisions—while keeping all financial control with managers.

How we built it

We built the system as an additive digital layer:

Role-based dashboards using a modern frontend framework

Secure backend APIs with branch-level data isolation

Structured loan, EMI, and day-wise repayment data models

AI models for risk tagging, repayment scoring, and explainable insights

Preventive alert mechanisms via SMS and email

Immutable audit logs to support compliance and governance

The system integrates smoothly without replacing existing loan systems.

Challenges we ran into

Designing early risk detection without over-automation

Keeping AI explainable and regulator-friendly

Ensuring borrower transparency without exposing internal risk logic

Managing multi-branch governance with clear data isolation

Balancing scalability with simplicity for real-world adoption

Accomplishments that we're proud of

Built a day-wise loan monitoring approach, not just EMI-level tracking

Designed human-in-the-loop AI for responsible decision-making

Implemented strong branch and role-based governance

Ensured full auditability and compliance readiness

Created a system that improves outcomes without disrupting existing workflows

What we learned

We learned that effective lending systems must prioritize clarity, accountability, and prevention over automation. Day-wise behavioral insights provide far more value than late-stage alerts, and AI is most powerful when it supports—not replaces—human judgment in financial decision-making.

What's next for Keeping Loans On Track

Integration with credit bureaus for deeper risk assessment

More advanced AI models for long-term default prediction

Mobile applications for managers and borrowers

Policy-based automation with supervisory approvals

Expansion to multi-lender and multi-region environments

Log in or sign up for Devpost to join the conversation.