-

-

novus.ai adoption

-

novus.ai adoption

-

project dashboard

-

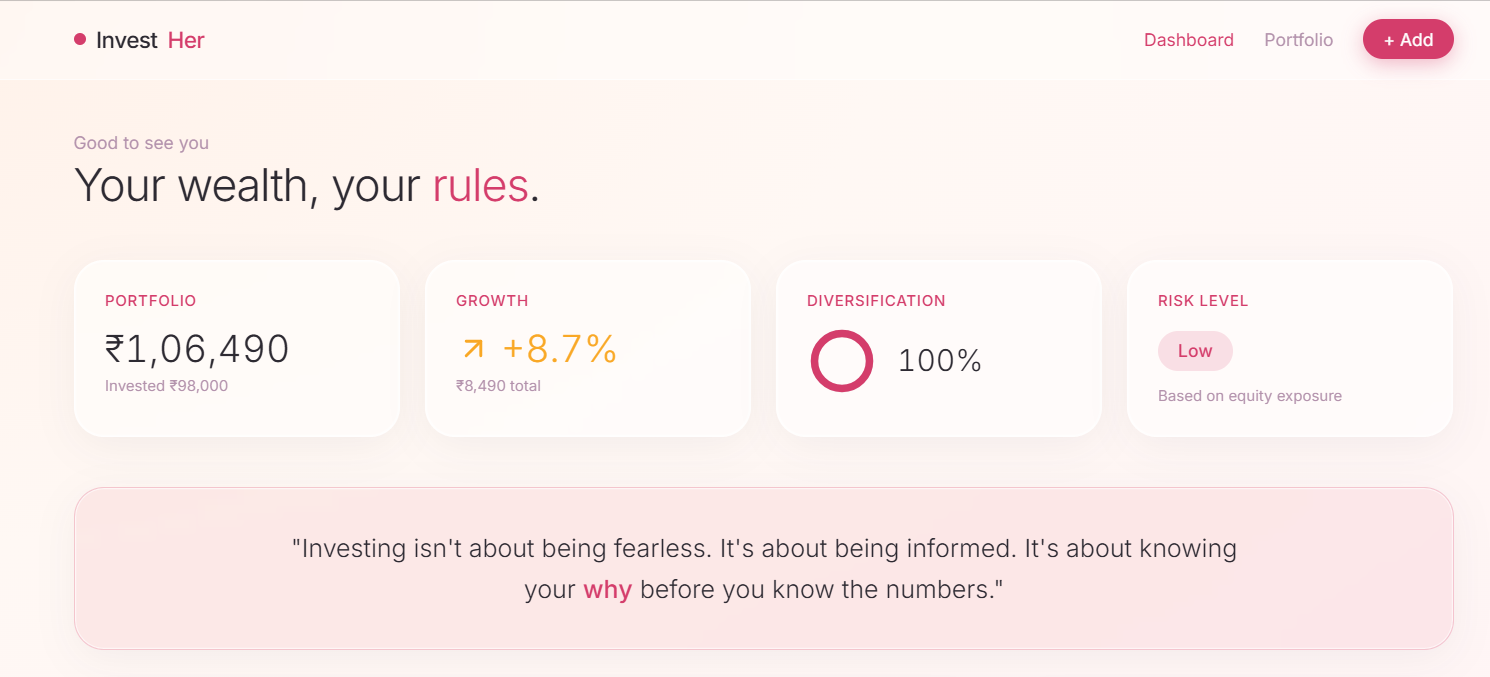

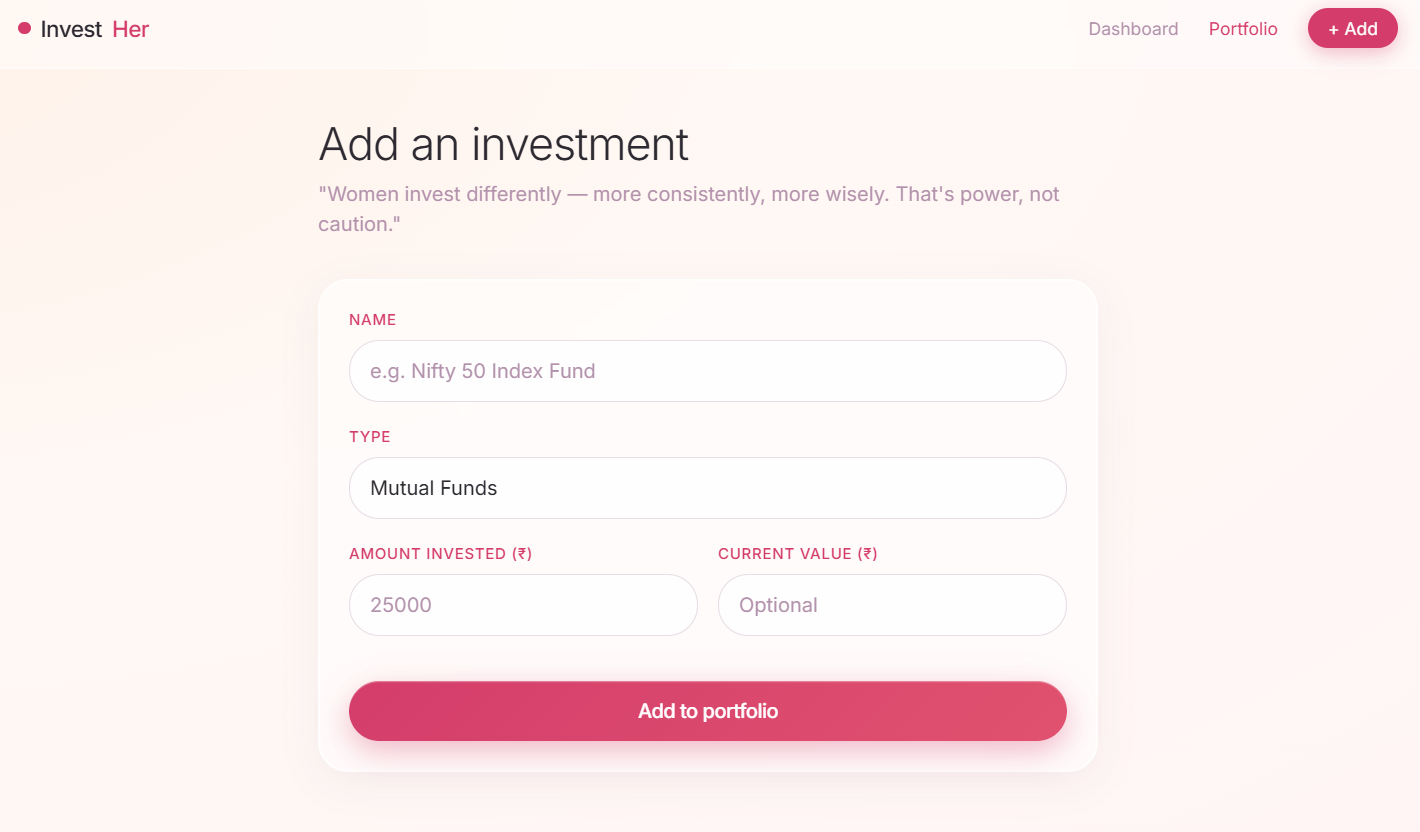

project interface

About the Project:

We built InvestHer, a research-backed investment platform designed to help women in India invest with greater confidence. Combining behavioral research with AI-powered insights, investment tracking, and personalized learning, the platform addresses barriers like financial literacy gaps and risk aversion through four distinct investor personas.

Built using Lovable, the project blends product thinking, UX design, data science, and AI to create a user-centric investing experience.

Shipping this project taught us the value of validating ideas through research, iterating quickly, and focusing on solving real user problems instead of just building features.

InvestHer - Women & Investing in India

Inspiration

It started with a number that didn't add up. Across India, women hold a growing share of the country's income, yet only 28% of their investable assets sit in equities, compared to 42% for men a gap of roughly ₹12,600 crore in unrealized participation. The easy explanation is "women don't have the money." Our early conversations told a different story.

So we ran a primary survey of 22 respondents (82% women, 91% aged 18–22) to test our assumption, and the data was unambiguous:

- 82% said "I need to learn a lot more before I start investing."

- Only 5% said they were already investing and felt good about it.

- Just 5% trust traditional financial advisors or banks.

That last number is what really hooked us. The barrier wasn't capital it was confidence, trust, and a financial industry that wasn't built with women's decision psychology in mind. If the gap is mostly behavioral, then the right product, not a bigger marketing budget could meaningfully close it. That became our founding thought, and InvestHer is our attempt to prove it.

What We Learned

1. The problem is psychological, not financial. We had assumed "don't have enough money" would dominate. It mattered (45% cited it), but "don't understand investing well enough" was the single largest barrier at 59%, and the knowledge-confidence gap (82%) dwarfed it again. Women have the same access to information as men (YouTube, Instagram, friends) - what differs is the activation step from knowing to doing.

2. Risk perception has a real, measurable gender gap. We used a simple behavioral split to quantify it. Letting $W$ and $M$ denote the share of women and men, respectively, who view a market downturn as a buying opportunity rather than a threat:

$$ W_{\text{opportunity}} = 6\%, \qquad M_{\text{opportunity}} = 50\%, \qquad \Delta = M_{\text{opportunity}} - W_{\text{opportunity}} = 44\text{ pp} $$

A 44-percentage-point difference is very large for a survey of this size. It showed us that using the same "buy the dip" messaging as existing trading apps would likely discourage our target users instead of attracting them.

3. Behavioral segmentation works better than demographic segmentation. We ran a lightweight $k$-means clustering pass on the 22 responses across five behavioral features (knowledge confidence, loss aversion, trust orientation, decision driver, and stated barrier) and consistently recovered four clean segments: the Eager Learner (36%), Cautious Analyzer (32%), Value Investor (23%), and Risk-Positive Outlier (9%). Designing for "women 18–35" would have flattened these into one persona; designing for the segments let us prioritize the Eager Learner the largest, highest-propensity group for our MVP.

4. A few features predict almost all of the behavior. We fit a simple logistic propensity model,

$$ P(\text{invests within 6 months}) = \sigma!\left(\beta_0 + \sum_{i=1}^{5} \beta_i x_i\right), \qquad \sigma(z) = \frac{1}{1 + e^{-z}} $$

where the five features peer inspiration, preference for community over advisors, a stated low-effort barrier, loss-aversion behavior, and lack of social normalization carried weights of roughly $+45\%, +38\%, +32\%, -28\%,$ and $-22\%$ respectively. The sign pattern alone was the real insight: every positive driver is something a product can manufacture (social proof, community, a low-friction first step); every negative driver is something a product can soften (small bets, transparent risk framing).

5. Unit economics in fintech reward trust, not just acquisition spend. In Year 1, we projected 35,000 users, with an average customer acquisition cost (CAC) of ₹650 and a customer lifetime value (LTV) of ₹18,000. This gives an LTV:CAC ratio of about 28:1, meaning every ₹1 spent on acquiring a user generates around ₹28 in value over time. This is much higher than the typical 8–10:1 ratio seen in other platforms. The strong ratio comes from our referral- and community-driven growth model, which reduces marketing costs. As a result, we view the community not only as a way to retain users but also as a key driver of growth.

How We Built It

- Research first. We conducted a survey with 22 respondents and grouped their answers into categories such as barriers, motivations, decision factors, and gender differences. Instead of relying only on average survey scores, we analyzed response patterns to uncover key insights, including the impact of trust issues and fear of losses on investment decisions.

- Quantitative synthesis. We grouped similar respondents and used predictive analysis to determine which people are most likely to take action and what drives their behavior.

- Market and financial modeling. We analyzed the market opportunity (₹90,000 Cr → ₹78,750 Cr → ₹25–50 Cr) and built a 24-month revenue model to see if a women-first investment platform could make a real impact while remaining financially sustainable.

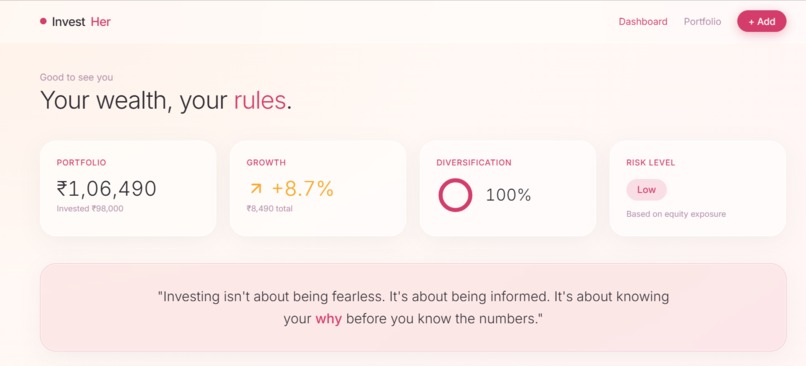

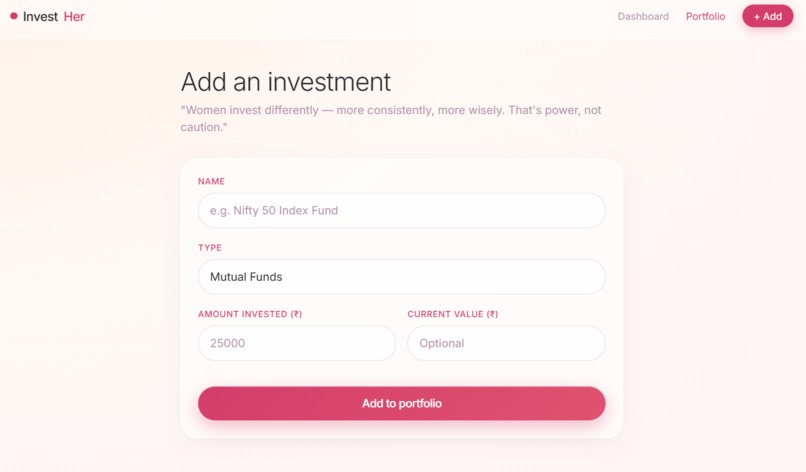

- Product design and prototyping. We translated the four product pillars: education-embedded investing, community-based trust, micro-investing from ₹100/month, and a curated transparent fund universe into InvestHer, a working frontend prototype (built with Lovable, React, and Tailwind) at

rose-quartz-ledger.lovable.app. It tracks portfolio value, growth, risk level, and diversification, and surfaces plain-language "AI Insight" nudges instead of raw numbers. - Storytelling. Finally, we packaged the research, root-cause analysis, and product into a single narrative deck Problem → Evidence → Insight → Solution → Impact, so the case for InvestHer stands on data at every step, not just intuition.

Challenges We Faced

- A small sample size. Twenty-two respondents is enough to find directional signal, not statistical certainty. We were careful to present our findings as hypotheses to validate at scale, not settled fact and we deliberately chose segmentation and propensity modeling techniques that degrade gracefully on small $n$ rather than ones that need large samples to be meaningful.

- Avoiding a patronizing tone. "Women-first fintech" can easily slip into condescension. The hardest design decisions were about how to signal safety and education without implying women need to be coddled. We kept returning to the data (control and safety as top decision drivers, not low confidence in ability) to keep the product respectful of our users' actual psychology.

- Reconciling behavioral insight with unit economics. Features that build trust (community, education, transparency) are expensive to build and slow to monetize; features that drive revenue (AUM fees, premium advisory) are not what activates a first-time investor. Sequencing the roadmap community and education first, monetization layered in later took several iterations of the financial model.

We came away convinced that the biggest unlock for women's investing in India isn't a new financial product it's a more honest, more legible relationship with the products that already exist. InvestHer is our first step toward building that.

Log in or sign up for Devpost to join the conversation.