-

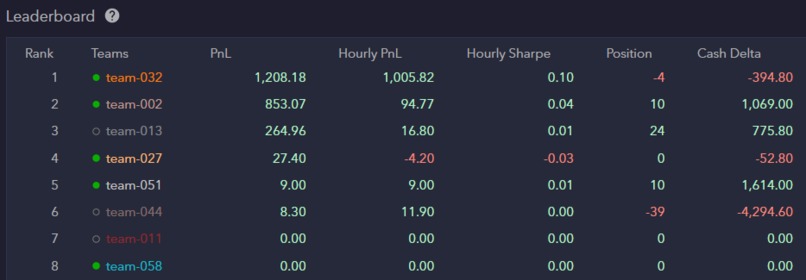

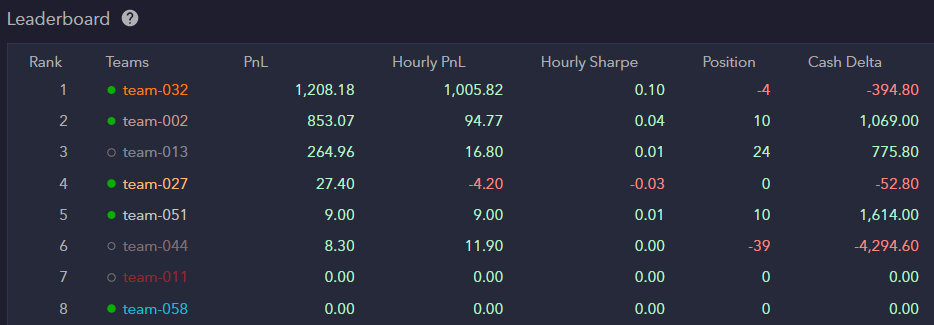

Leaderboard

Project Submission - Optiver Challenge - Team 032 (I Triple W)

Idea Description and Implementation Explanation

Part 1

- Check if there is a market inefficiency, i.e. a difference between theoretical basket price and real basket price, in a loop

- Separate inefficiency situation into two cases:

- Highest bid price for the basket is larger than the combined partial stock prices. → Basket is overvalued and we want to sell the basket and buy the stocks

- Lowest ask price for the basket is smaller than the combined partial stock prices. → Basket is undervalued and we want to buy the basket and sell the stocks.

- Determine optimal order volume for each instrument by considering a balancing of our position and a maximisation of the order volume

- Start with maximum potential order volumes from the order book

- At first, reduce the order volumes of both stock instruments to be as balanced as possible

- Afterwards, adjust the order volumes of basket and both instrument to keep the basket positions as equal as possible to the stock positions

- Place IOC orders if the profit is larger than a threshold

Part 2

- We quote between the lowest ask and the highest bid to provide liquidity to an illiquid market: we make sure to always overbid and underask the current order book

- Long term quoting plan: quoting depends on: “hit” and “lift” rate, market liquidity, risk we are willing to take, our current inventory

- Our orders are reset on every tick in order to account for market movements such that our bids and asks always adapt to the current order book

- For our prototype we measured market metrics (by analysing the order book) and found that an order volume of 4 on both sides respectively is small enough to limit risk exposure and high enough to make a significant profit

- Long term volume plan: we propose a dynamic approach: the order volume should depend on the inventory (positive position: higher ask volume, negative position: higher bid volume) and our current/forecasted “hit” and “lift” rate

- Hedging: We combined our market making strategy with the opportunity detection strategy from part 1 which handles the balancing

- Long term hedging plan: having an optimizer function that outputs “Hedge” or “Wait” depending on parameters: our position size, PnL of the hedge (best current market price that we can go short/ long on the stocks for minus our market making bid-ask spread, i.e. the price that we might pay for the hedge minus the profit that we make with market making)

Additional implementation details:

- Start multiple threads, one for the green energy market making algorithm (part 2) and one for the hedging of each market segment (part 1), i.e. three threads in total

Risk Handling

- We chose a minimal risk strategy by keeping our positions as balanced as possible

- Risks for hedging:

- We do not fully realise our orders and therefore get an unbalanced portfolio.

- Being unbalanced is risky because we are dependent on the random movement of the market

- We adjust our orders to our imbalances, such that we tend towards a balanced portfolio

- Risks for market making:

- Depend heavily on part 1 (since we combined the two strategies)

- Additional risk sources: We are not able to hedge the size of our market making exposure/volume profitably

Built With

- algorithms

- amazon-web-services

- cloud9

- python

- trading

Log in or sign up for Devpost to join the conversation.