-

-

Home

-

About

-

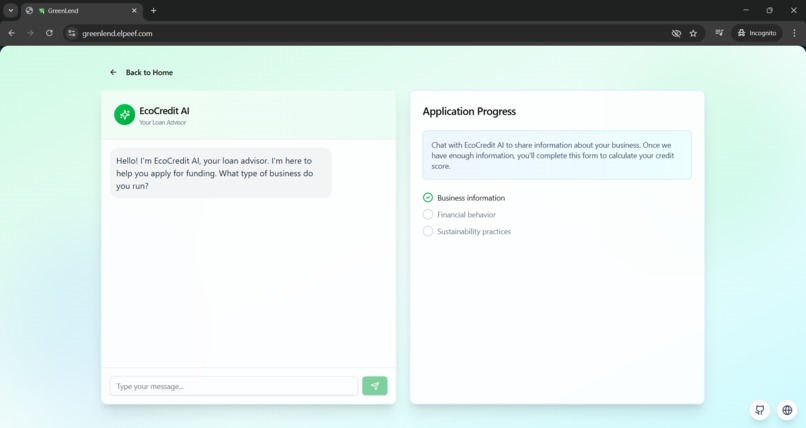

EcoCredit AI

-

Lender Dashboard

Inspiration

When we talk about "Payment Without Limits," most projects focus on speed and fees.

We asked a different question:

What if the real limit isn’t technical — but who gets access to the payment system at all?

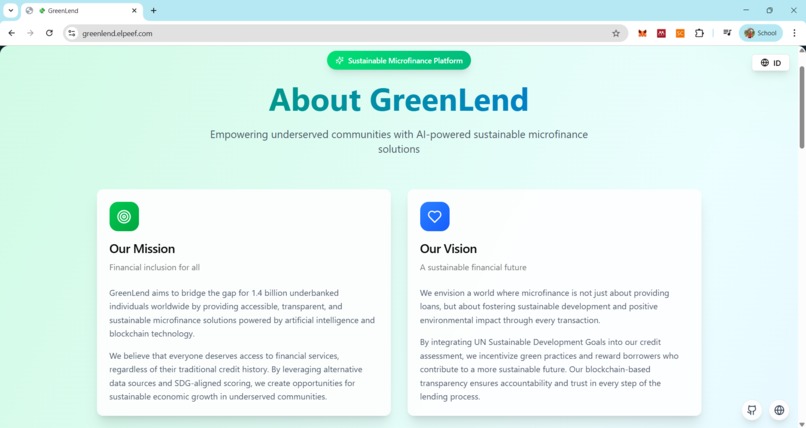

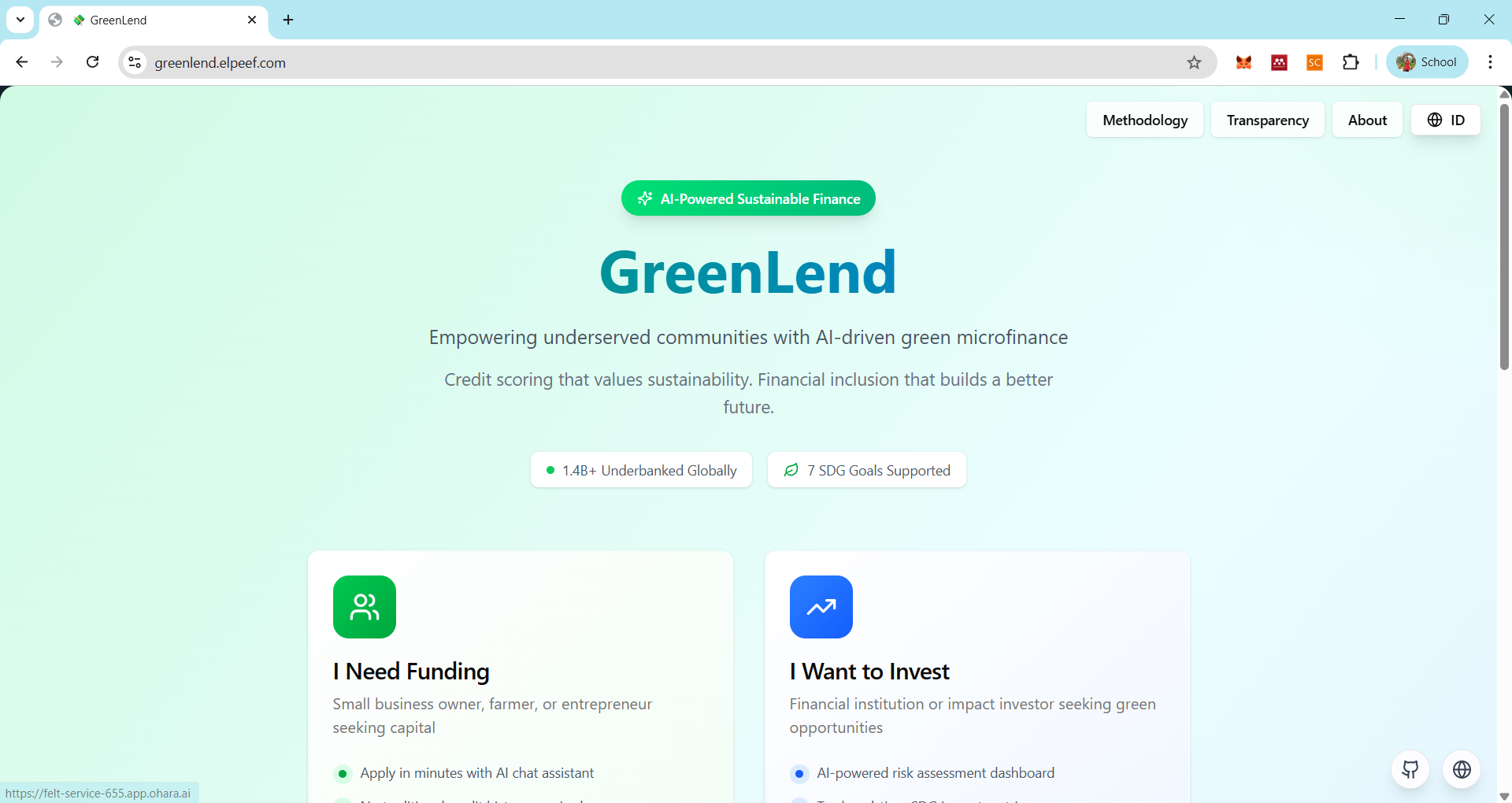

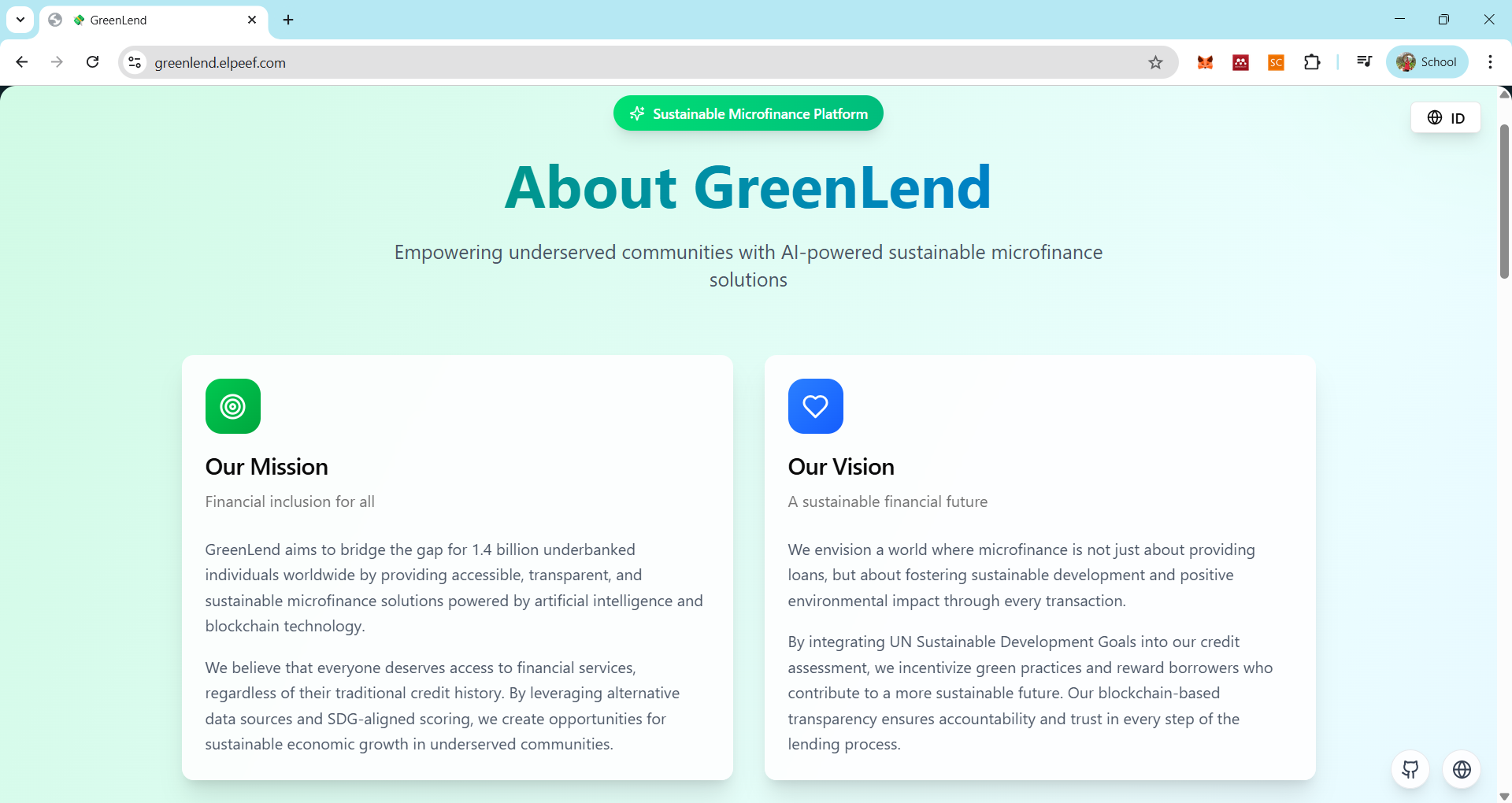

1.4 billion people are financially excluded — not because they lack creditworthiness,

but because traditional payment infrastructure was never designed for them.

No bank account? No credit history? No literacy? You’re locked out.

We built GreenLend Suite to remove those limits — not just to make payments faster,

but to make them accessible, transparent, and dignified for the people who need them most.

This is payment infrastructure that puts humanity first.

What It Does

GreenLend Suite is a voice-powered, multi-rail payment infrastructure for the financially excluded,

built on LoanChain Ledger — our borderless payment settlement layer.

Core Payment Infrastructure

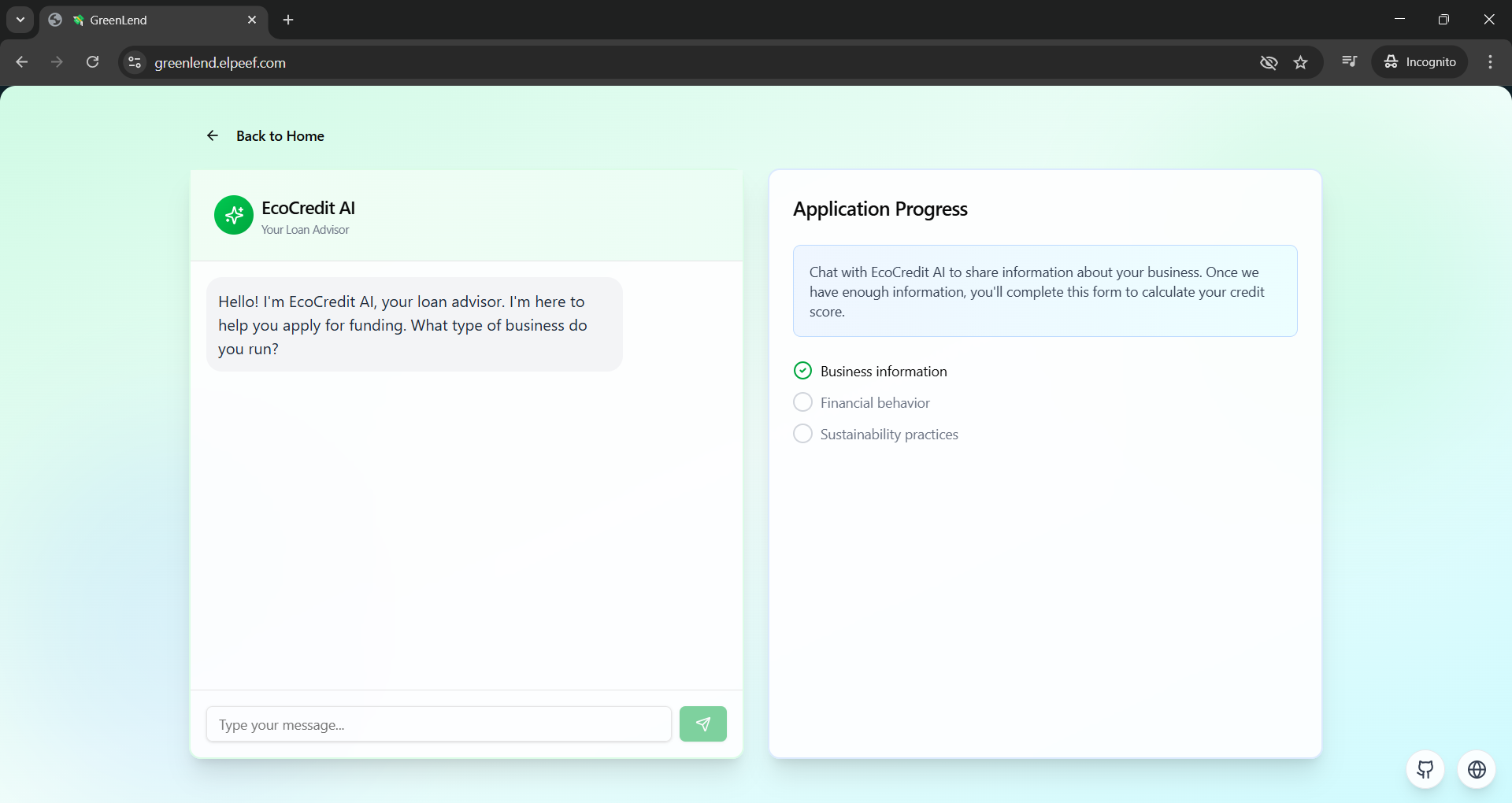

- 🎤 Voice-first access (Maya, ElevenLabs) — Removes literacy barriers

- 🌍 Multi-rail disbursement — PayPal (Web2) + Ethereum (Web3)

- 🔗 LoanChain Ledger — Cross-app payment settlement & real-time sync

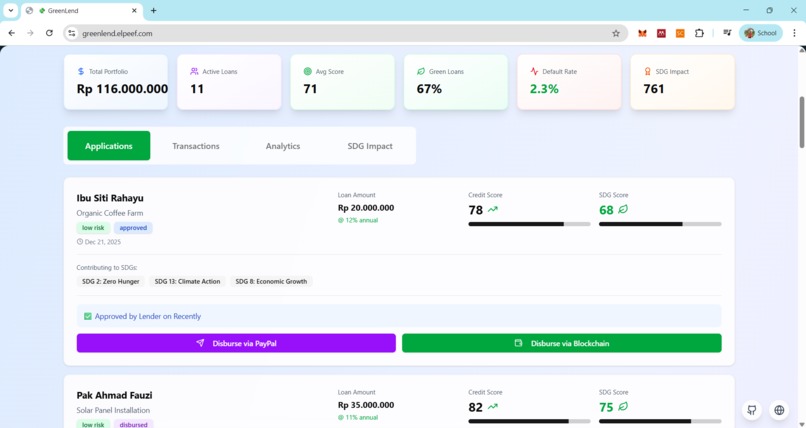

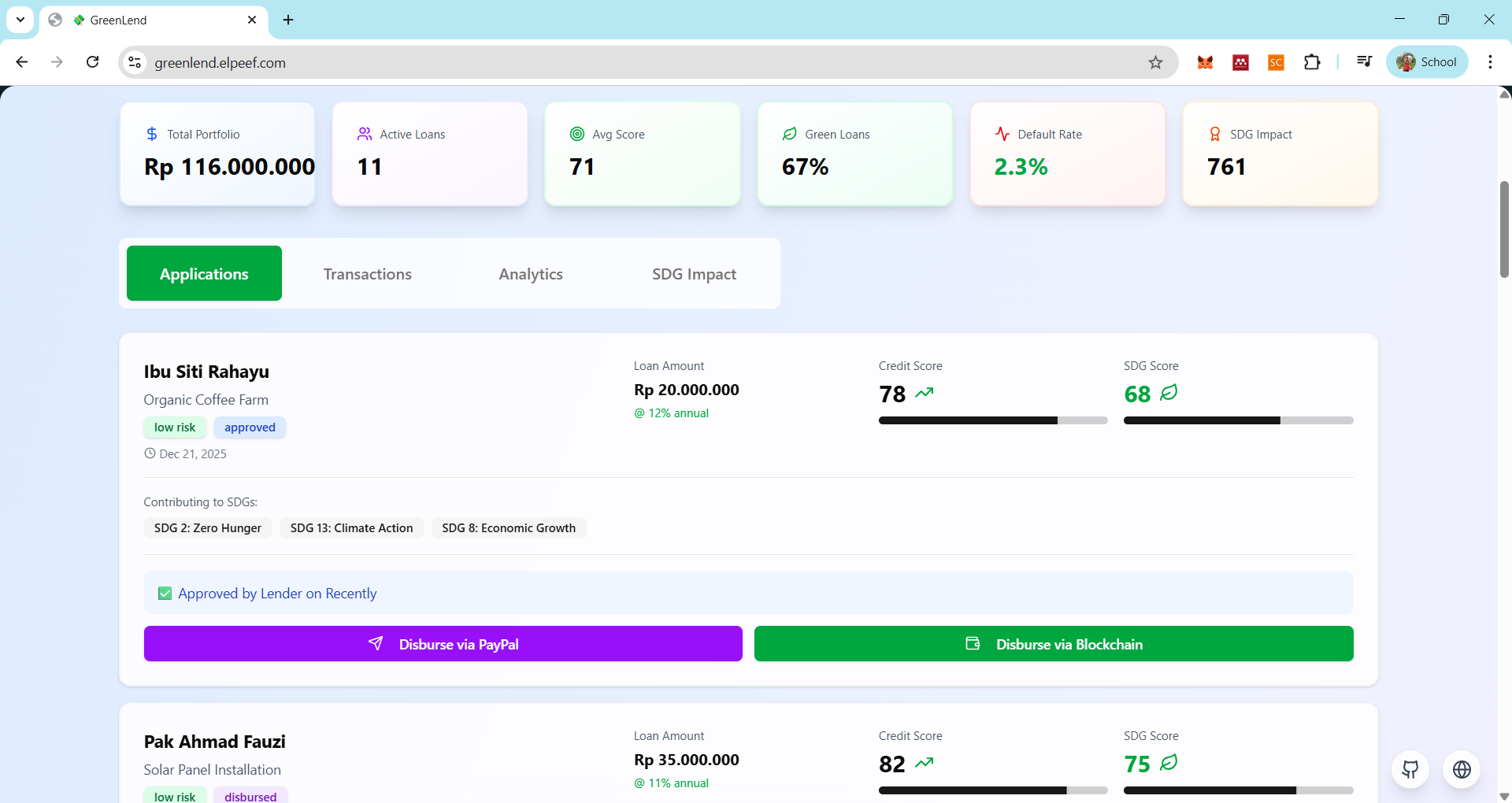

- 🔍 Transparent credit scoring — Full decomposition dashboard

- 💚 SDG-native assessment — Sustainability built into the payment layer

- 📦 Decentralized storage — IPFS via Pinata for immutable records

How It Removes Payment Limits

- Geography Limit → Multi-rail (PayPal + ETH) + Base Network bridge

- Literacy Limit → Voice AI with intent classification & entity extraction

- Access Limit → No bank account needed, alternative data scoring

- Trust Limit → Blockchain transparency + score decomposition

- Dignity Limit → Rejection with empowerment (actionable improvement paths)

The Flow

Voice conversation with Maya →

AI extracts 25+ data points →

Transparent scoring (Traditional 20% + Alternative 50% + SDG 30%) →

Multi-rail disbursement →

LoanChain settlement →

Real-time portfolio tracking

Why It's Infrastructure, Not Just an App

GreenLend Micro (microfinance) is our first vertical on LoanChain Ledger.

The same payment rails will power merchant payments, cross-border commerce,

and embedded finance — starting with the 65M+ underserved MSMEs who need it most.

How We Built It

Architecture: Payment Infrastructure Layer

1. Voice-Powered Payment Gateway

- ElevenLabs Conversation SDK (Maya agent) for intent classification

- Claude AI (Anthropic) for entity extraction (25+ fields)

- Auto form-fill eliminates manual data entry

- <2 minute application-to-decision pipeline

2. Multi-Rail Disbursement Engine

- PayPal REST API for fiat disbursements (global reach)

- Ethereum smart contracts on Sepolia testnet

- Viem + Wagmi for Web3 interactions

- Cross-chain bridge via LoanChain to Base Network

3. LoanChain Ledger (Payment Settlement Layer)

- Real-time loan data synchronization between apps

- API health monitoring with auto-refresh

- Push-model data propagation (LoanChain → GreenLend)

- Shared control plane for institutional + grassroots finance

4. Ethical Credit Scoring Engine

- Weighted algorithm: Traditional (20%) + Alternative (50%) + SDG (30%)

- Alternative data: mobile payments, utility history, social proof

- SDG indicators: renewable energy, job creation, carbon footprint

- Transparent breakdown with exact point allocation

5. Rejection with Dignity Interface

- 7 actionable improvement recommendations

- Exact score impact simulation (+10 points for solar panels)

- Timeline and resource requirements for each action

- Cumulative transformation potential calculator

6. Blockchain Transparency Layer

- Ethereum Sepolia for immutable loan records

- IPFS (Pinata) for decentralized document storage

- Real-time transaction explorer links

- 40% cost reduction through automation

Tech Stack

- Frontend: Next.js 15, TypeScript, Tailwind CSS

- Voice AI: ElevenLabs SDK v0.13.0

- AI Processing: Claude API (Anthropic)

- Blockchain: Ethereum Sepolia, Base Network, Viem, Wagmi

- Storage: Pinata IPFS

- Payments: PayPal REST API, Ethereum smart contracts

Challenges We Ran Into

1. Cross-Origin Payment Sync

Challenge: LoanChain API CORS policies blocked direct client-side calls

Solution: Built Next.js proxy API routes (/api/loanchain/sync, /api/loanchain/health)

to handle server-side forwarding with proper headers

2. Voice-to-Structured Data Pipeline

Challenge: Converting natural conversation into 25+ structured fields

Solution: Multi-stage AI pipeline

ElevenLabs → Claude → validation layer → auto form-fill with confidence scoring

3. Transparent Scoring Without Black Boxes

Challenge: Traditional scoring is opaque

Solution: Weight-based decomposition dashboard:

(Traditional × 0.2) + (Alternative × 0.5) + (SDG × 0.3)

Every single point is traceable by borrowers

4. Multi-Rail Disbursement Coordination

Challenge: Coordinating PayPal (Web2) and Ethereum (Web3)

Solution: Unified disbursement API with fallback logic and real-time tracking

5. Rejection That Empowers, Not Discourages

Built improvement engine with:

- Exact score impact

- Timeline estimates

- Resource requirements

- Cumulative transformation modeling

6. Real-Time Health Monitoring

Smart caching (30s TTL), auto-refresh toggle, and graceful degradation

with clear error context

Accomplishments We're Proud Of

Infrastructure Innovation

✅ Built payment settlement layer bridging $6T syndicated loan markets to grassroots microfinance

✅ Multi-rail disbursement (PayPal + Ethereum)

✅ Cross-chain bridge (Ethereum Sepolia ↔ Base Network)

✅ Real-time API health monitoring with sync history

Ethical Differentiation

✅ Transparent credit score decomposition

✅ Rejection with Dignity interface

✅ SDG-native scoring (30% weight)

✅ Alternative data prioritization (50% weight)

Impact Potential

✅ Addresses 1.4B financially excluded people

✅ Targets 65M+ underserved MSMEs in Southeast Asia

✅ 23% lower default rate projection (SDG-aligned borrowers)

✅ 40% operational cost reduction through automation

We didn’t just build a feature — we built infrastructure.

Payment without limits isn’t about transactions per second.

It’s about removing barriers so everyone can participate.

What We Learned

1. Payment Infrastructure ≠ Payment Features

True payment without limits requires settlement layers, multi-rail coordination, and cross-app sync — not just payment buttons.

2. Voice AI Changes Financial Inclusion

Voice-first eliminates literacy barriers entirely. It’s not a feature — it’s the gateway for 1.4B people.

3. Transparency Builds Trust

Score decomposition transformed borrower-lender relationships. Trust is a technical feature.

4. Rejection Can Be Empowerment

We turned “No” into a growth roadmap. That’s ethical engineering.

5. Sustainability Is a Credit Signal

Green businesses show 23% lower default rates. Ethical finance is smart finance.

6. Blockchain for Accountability, Not Hype

Used for immutable records, transparent settlement, and interoperability — not trend-chasing.

7. Observability Is Non-Negotiable

API health, sync history, and error context are core architecture — not afterthoughts.

Key Insight:

Payment without limits is a systems design problem.

You must remove limits at every layer: UI, scoring, disbursement, settlement, and psychology.

What's Next for GreenLend Suite

Phase 1: Microfinance Foundation (COMPLETE ✅)

- Voice-powered loan applications

- Multi-rail disbursement (PayPal + Ethereum)

- LoanChain Ledger integration

- Transparent scoring & rejection with dignity

Phase 2: Merchant Payment Acceptance (Q2 2025)

- MSME payment gateway

- QR code + voice payment initiation

- Instant settlement via LoanChain

- SDG-based transaction fee discounts

Phase 3: Cross-Border MSME Commerce (Q3 2025)

- P2P payment rails between MSMEs

- Multi-currency support

- Escrow & dispute resolution via smart contracts

- Supply chain financing

Phase 4: Embedded Finance SDK (Q4 2025)

- Developer-facing payment API

- White-label voice-powered credit assessment

- Plug-and-play multi-rail disbursement

- Open-source SDG scoring engine

Scaling Strategy

- Geographic: Indonesia → Southeast Asia → Sub-Saharan Africa

- Vertical: Microfinance → Merchant payments → Supply chain finance

- Technical: Ethereum/Base → Multi-chain

- Partnerships: MFIs, cooperatives, impact investors, UN SDG funds

Long-Term Vision

LoanChain becomes the Stripe for the financially excluded —

a payment infrastructure layer where dignity, transparency,

and sustainability are defaults, not exceptions.

Immediate Next Steps

- Pilot with 5 Indonesian MFIs (1,000 borrowers)

- Integrate Farcaster Frames for Web3 social lending

- Add USDC stablecoin rail

- Open-source SDG scoring methodology

Log in or sign up for Devpost to join the conversation.