-

-

login

-

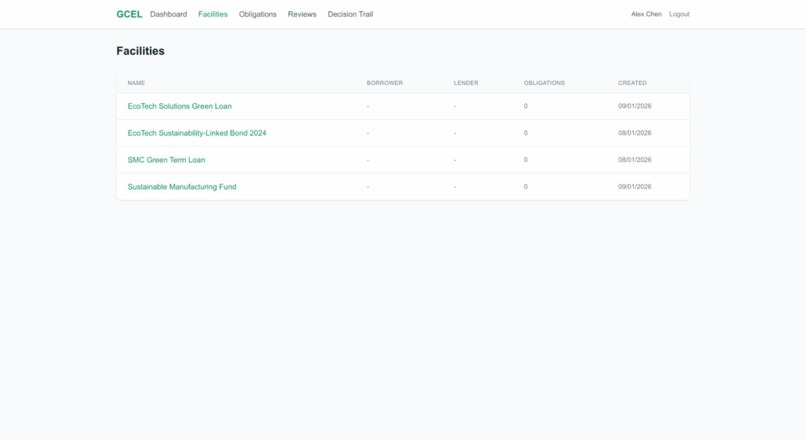

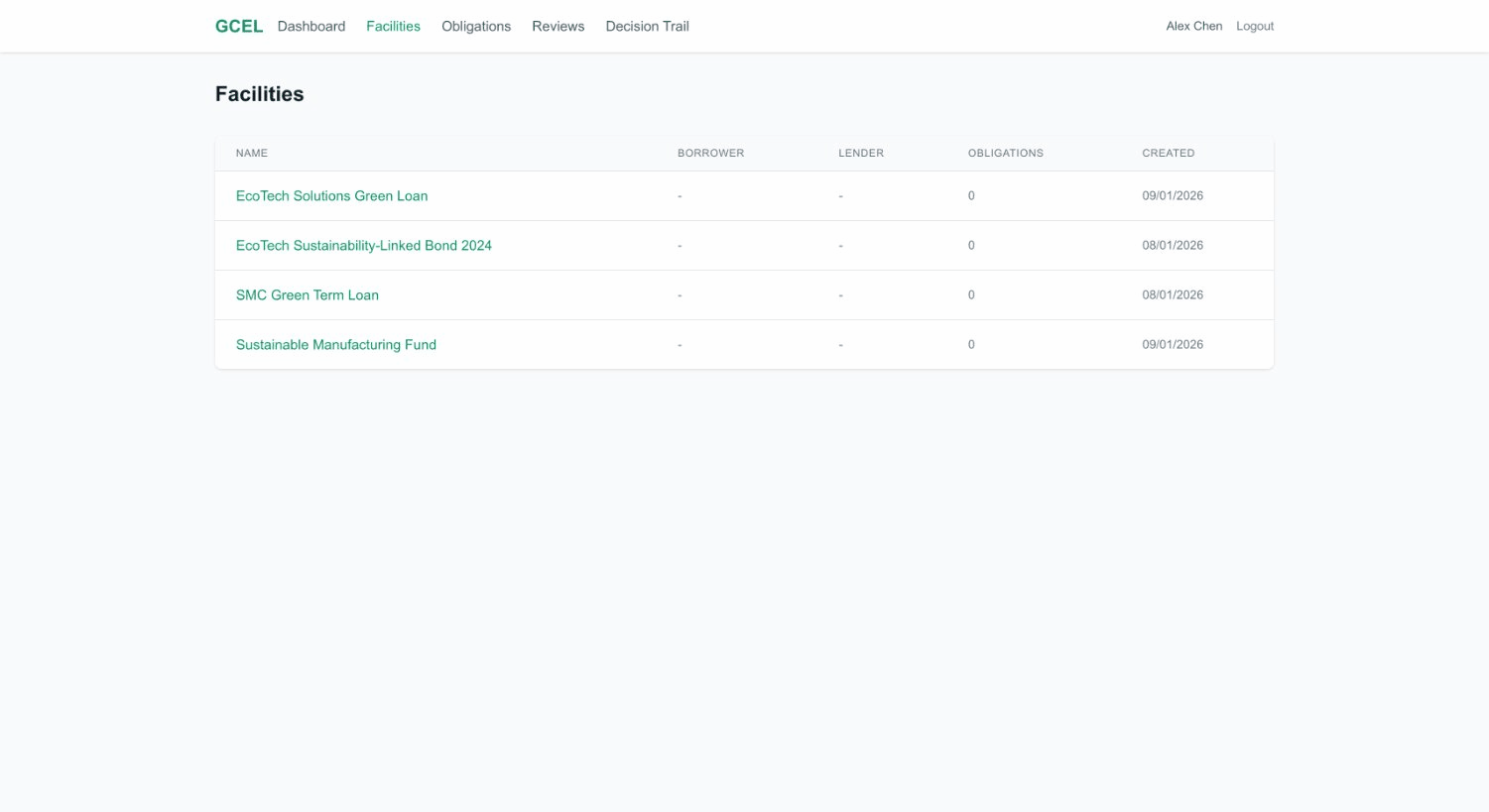

facilities list

-

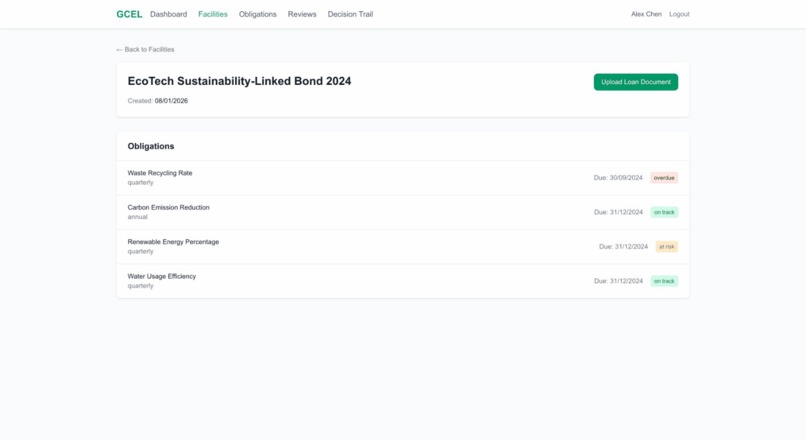

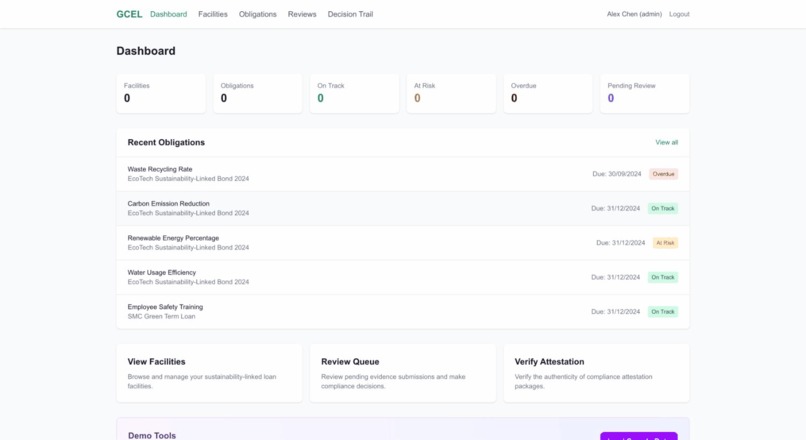

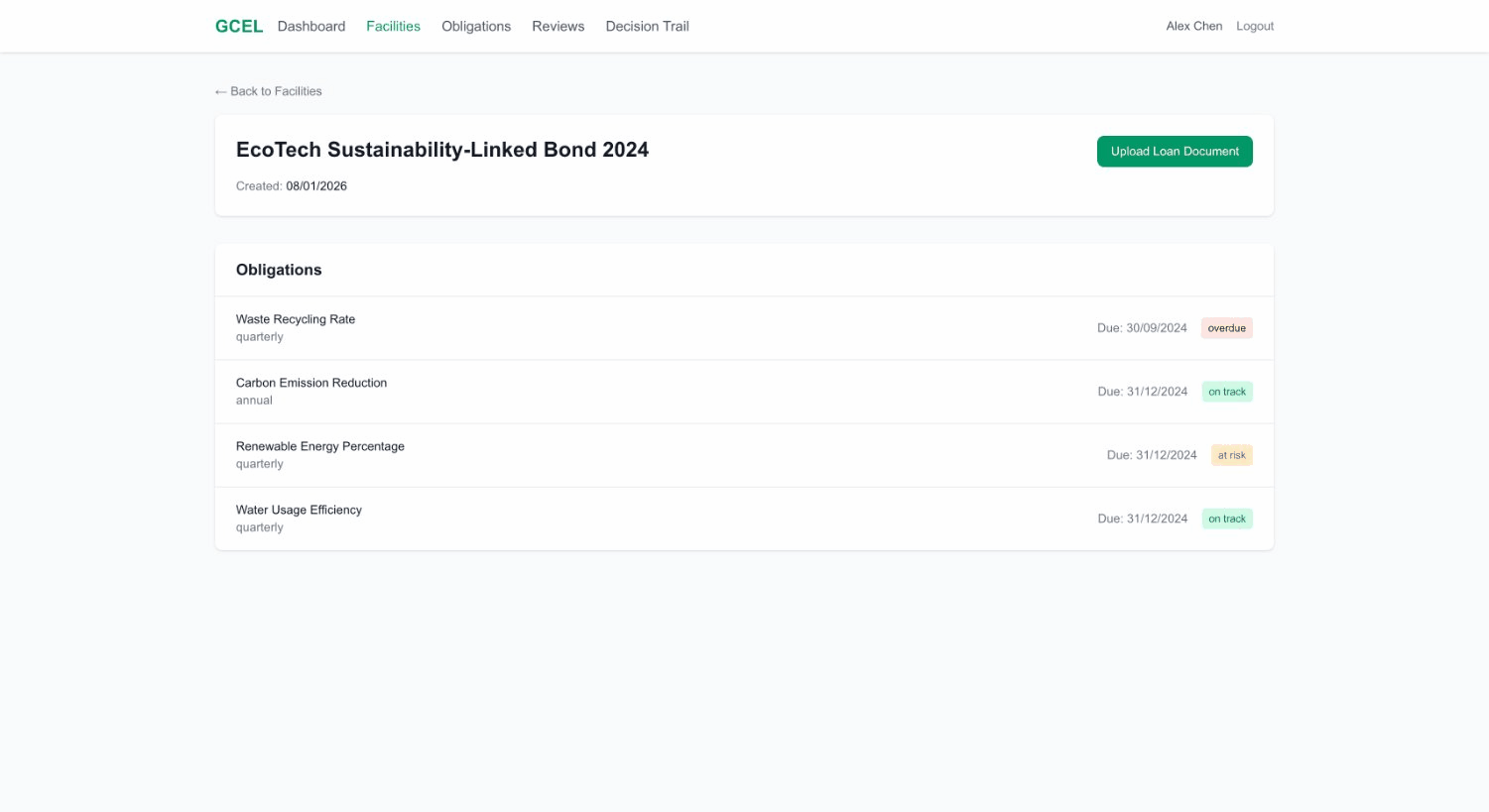

obligations

-

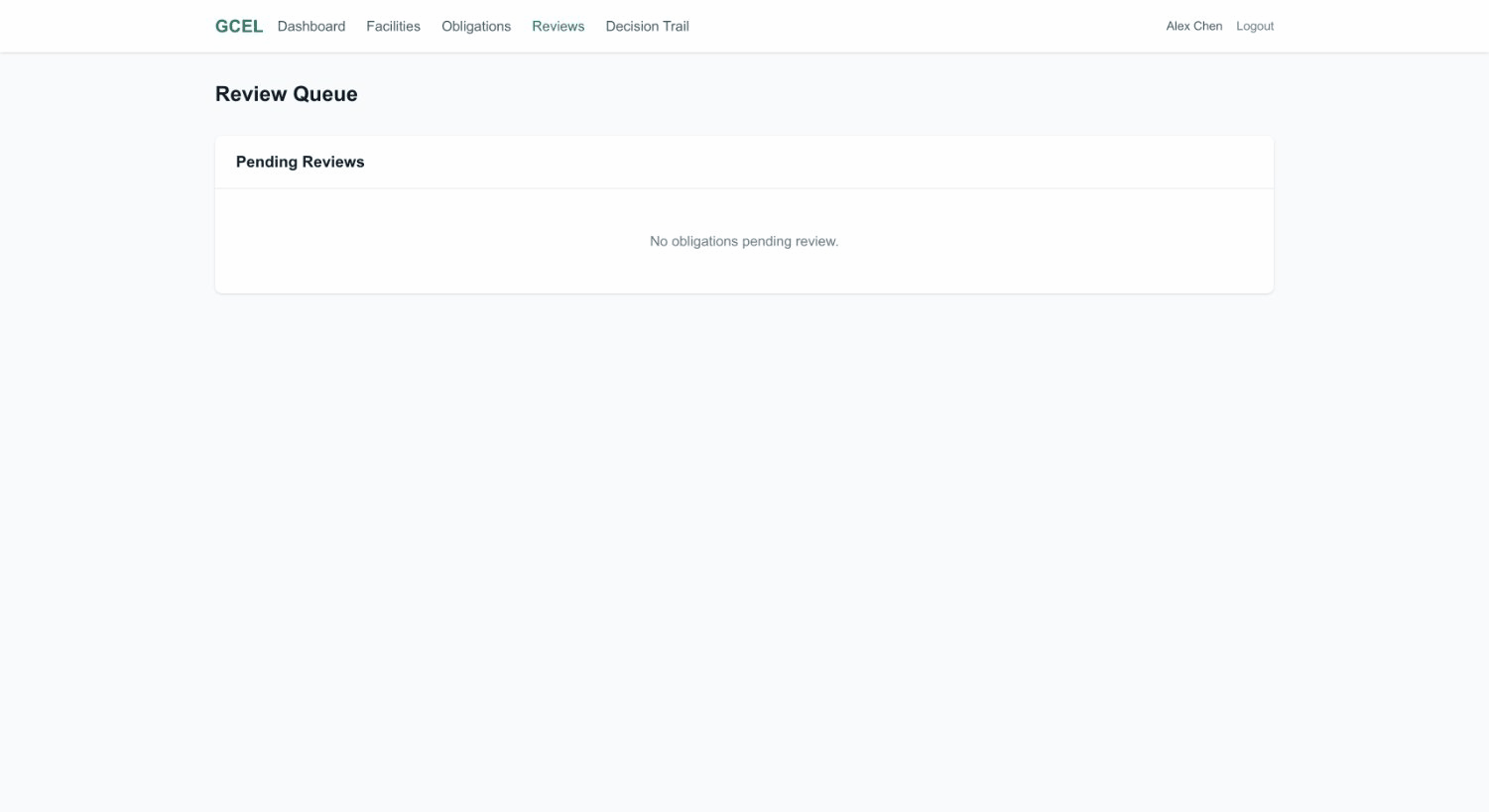

review queue

-

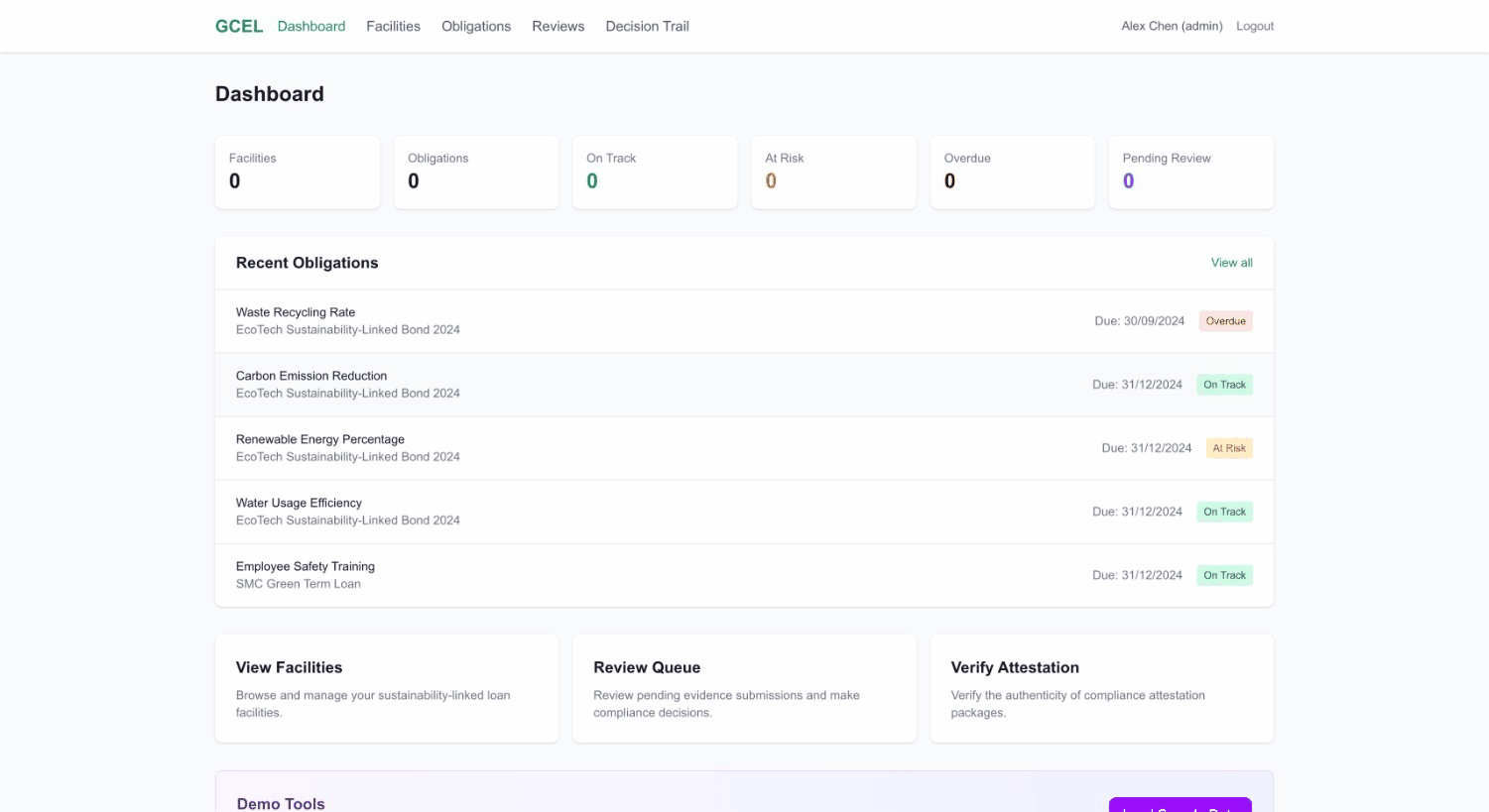

dashboard

-

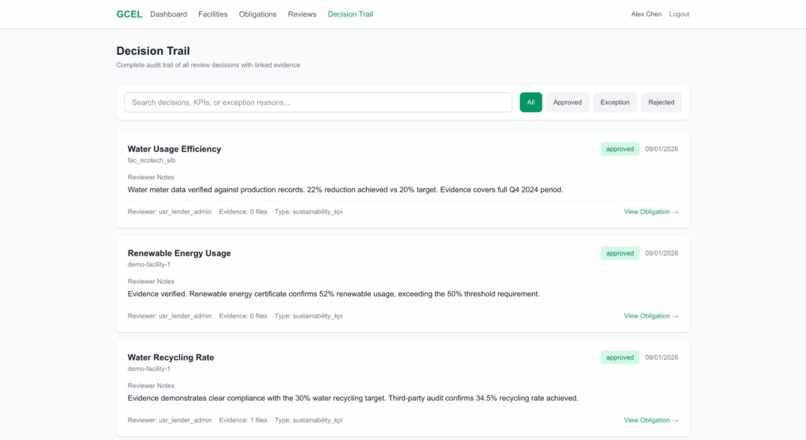

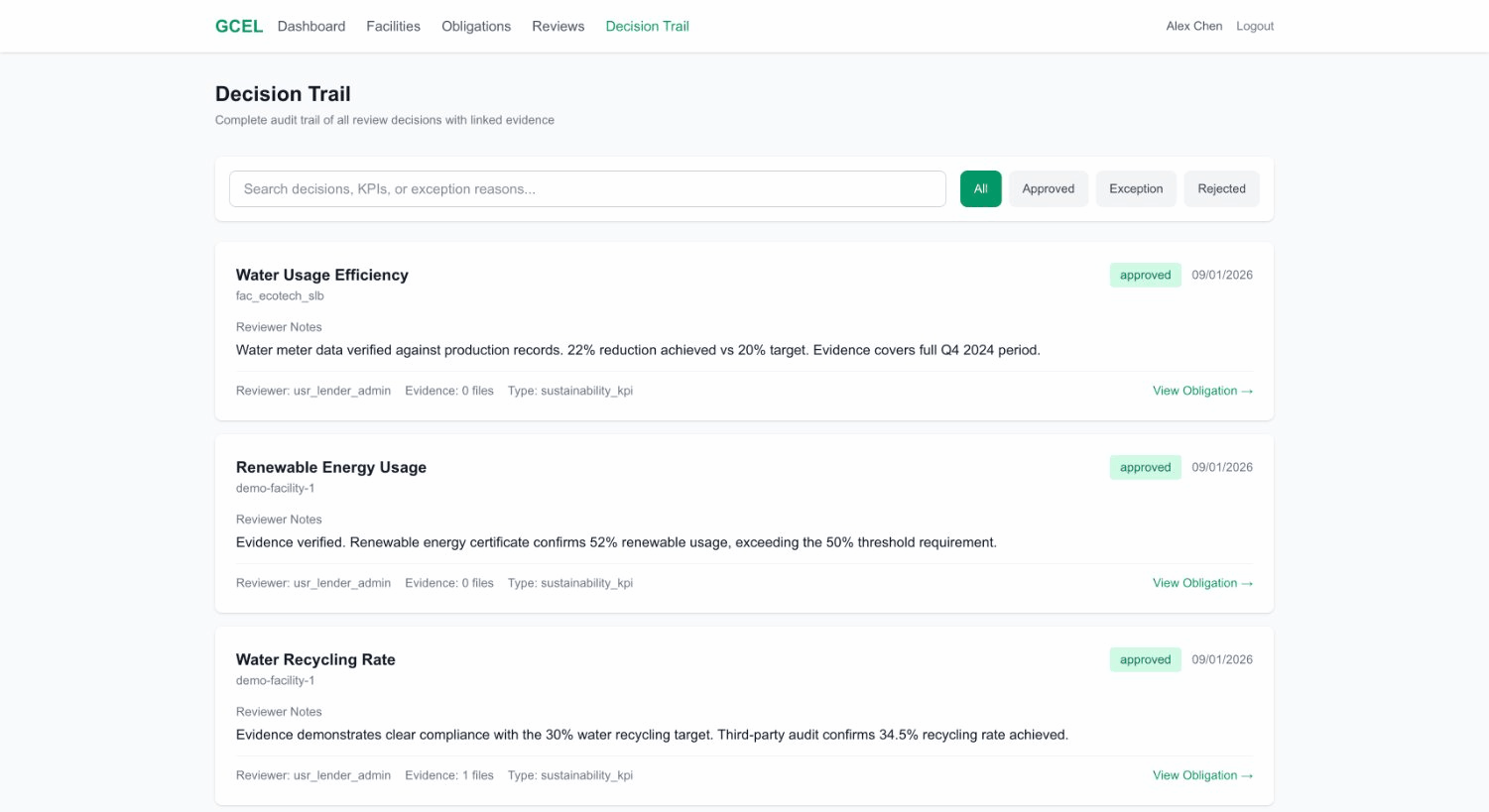

decision trail

-

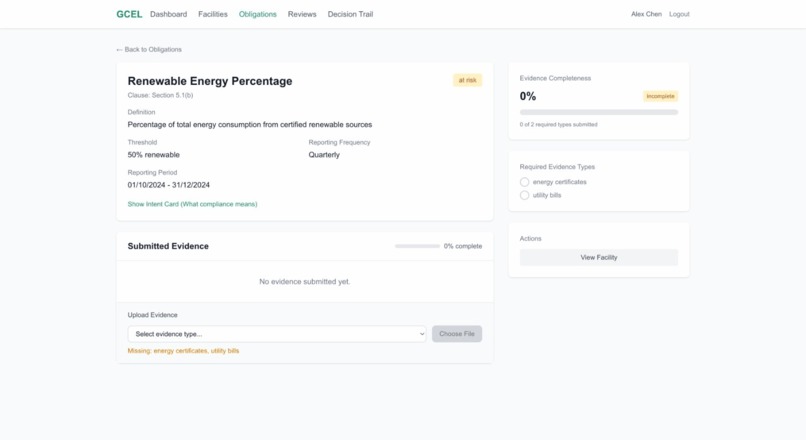

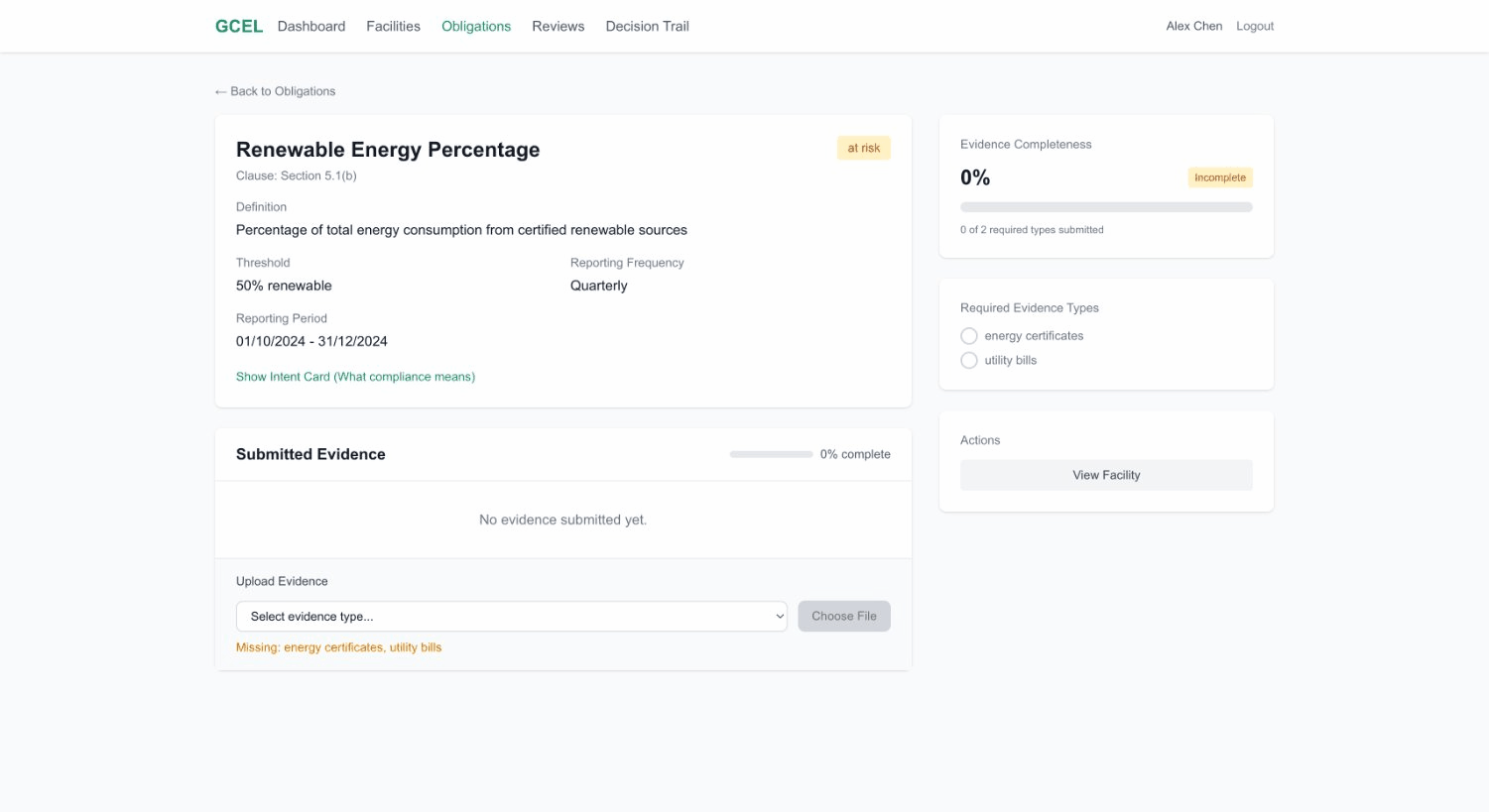

view facility

-

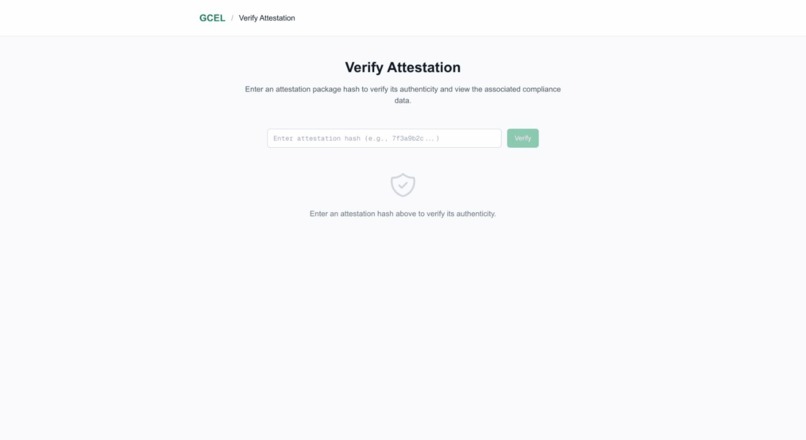

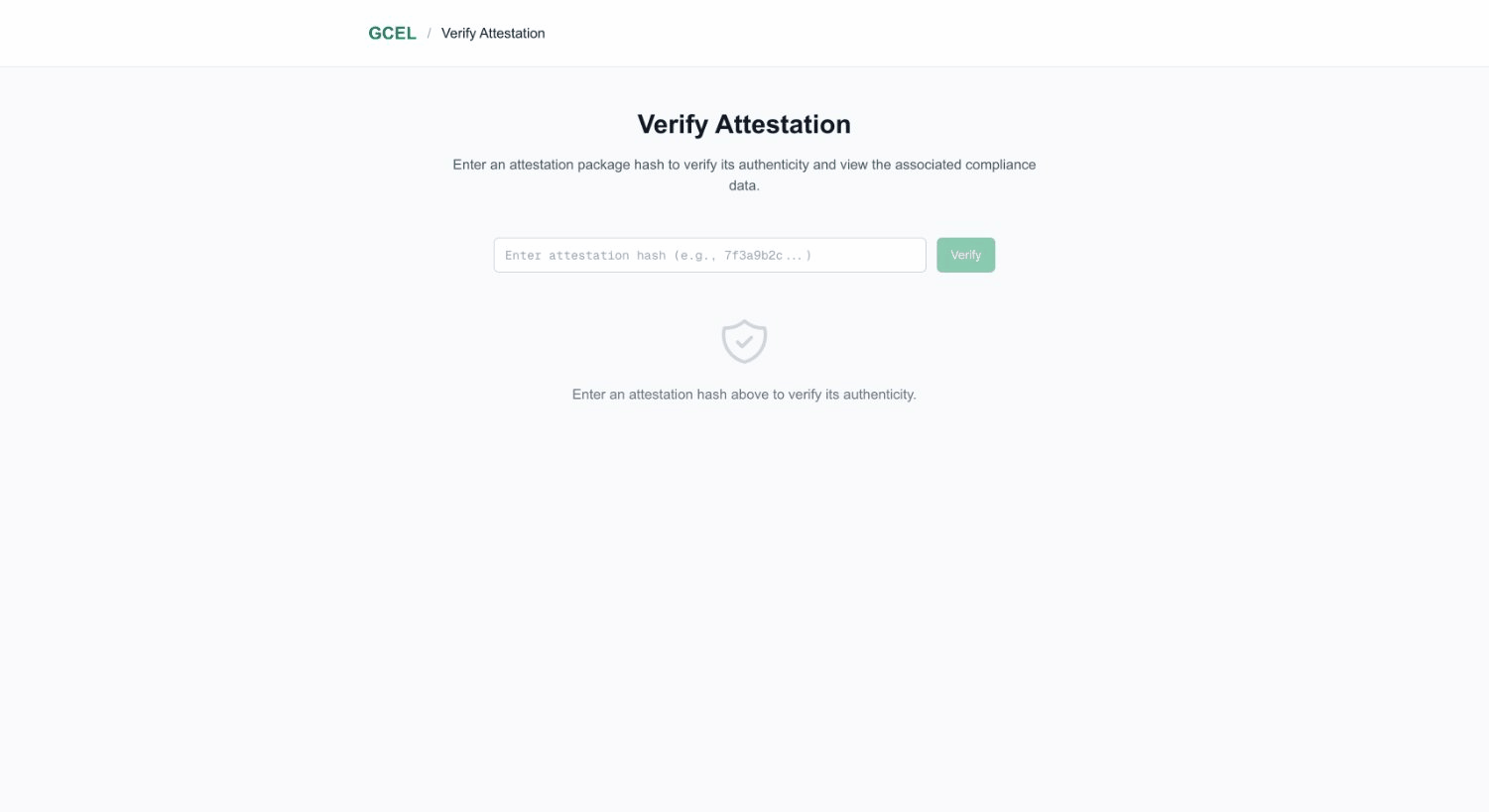

verify attestation (public)

Inspiration

Sustainability-linked and green loans are scaling, but the operational reality is still fragmented: ESG covenants live inside long-form documents, evidence is exchanged via email/spreadsheets, and audits/disputes become expensive because provenance and interpretation are inconsistent. We built GCEL to make the loan contract the source of truth and to turn covenant monitoring into a clear, repeatable workflow.

What it does

GCEL (Green Covenant Evidence Ledger) converts ESG / sustainability covenants into a structured, trackable process:

- Upload loan document → extract obligations: Parses key covenant/KPI requirements (frequency, thresholds, evidence required).

- Intent Cards (“what compliance means”): Each covenant/KPI becomes an explicit checklist and policy card that guides submission and review.

- Evidence Locker: Borrowers upload evidence artifacts (PDFs, images, exports) and map them to obligations and reporting periods.

- Completeness + readiness checks: Highlights missing or mismatched evidence before submission.

- Review workflow: Reviewer can approve, request clarification, or raise exceptions; includes AI-assisted review notes for faster internal memos.

- DecisionTrail (Context Graph): Every cycle creates a DecisionTrace linking the covenant, evidence, reviewer actions, and outcome—so teams can reuse precedent and reduce repeat disputes.

- Attestation + verification: Generates a shareable attestation package (hash/sign/verify) so permitted parties can verify integrity without re-auditing everything from scratch.

How we built it

We implemented GCEL as a desktop web workflow app with a secure backend:

- Document ingestion pipeline: PDF upload → clause/KPI extraction (LLM-assisted) → human-in-the-loop confirmation for reliability.

- Context Graph model: Facility → Covenant → KPI → Evidence → ReviewAction → DecisionTrace, enabling traceable compliance history and precedent search.

- Intent Layer: Hierarchical Intent Cards that act as stable “governing context” for workflows and agent behavior.

- Attestation service: Deterministic hashing/signing and a verification page; optional ledger anchoring can be added later (tamper-evidence only).

Challenges we ran into

- Clause variability: Loan drafting styles differ widely; we balanced extraction automation with confirmation UX.

- Evidence heterogeneity: Real-world evidence comes in many formats; we focused on checklist-driven completeness first, then extraction enhancements.

- Judge-friendly UX: We prioritized a workflow that is obvious to lenders, borrowers, and reviewers within a 3-minute demo.

Accomplishments that we’re proud of

- An end-to-end, working flow: document → obligations → evidence → review → decision trace → attestation verification.

- A clear “differentiator moment”: DecisionTrace + verification makes compliance tangible and shareable.

What we learned

In sustainable lending, the real bottleneck is not retrieval—it’s decision context: what was required, what was submitted, who approved, why, and what outcome followed. Capturing those decision traces creates compounding operational value.

What’s next

Productization for Straits AI (Malaysia/SEA-ready):

- Expand covenant/KPI templates and clause pattern coverage.

- Add integrations (utility data, ERP exports, IoT metering where applicable).

- Introduce selective disclosure packages for secondary market diligence.

- Enterprise controls: SSO, tenant isolation, data residency options, and audit retention policies.

- Optional chain anchoring and RWA-linking for tokenized loan participations (where appropriate).

Built With

- cloudflare

- d1

- nextjs

- openrouter

- resend

- typescript

Log in or sign up for Devpost to join the conversation.