-

-

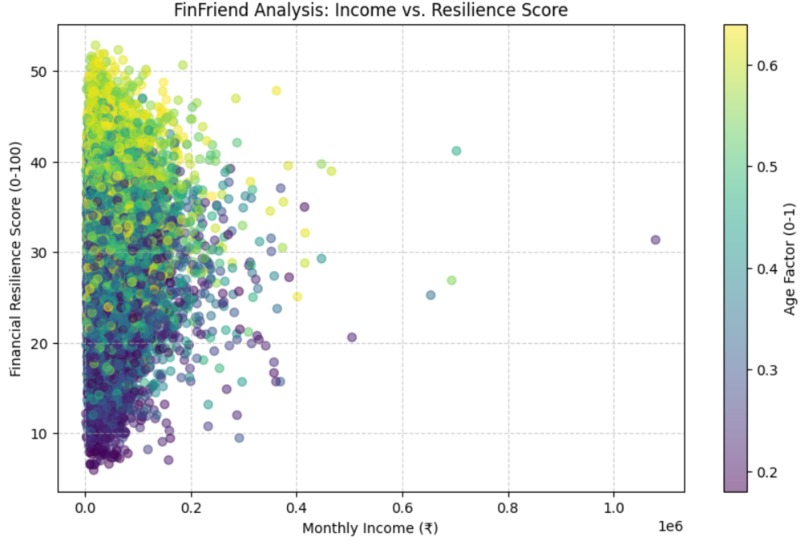

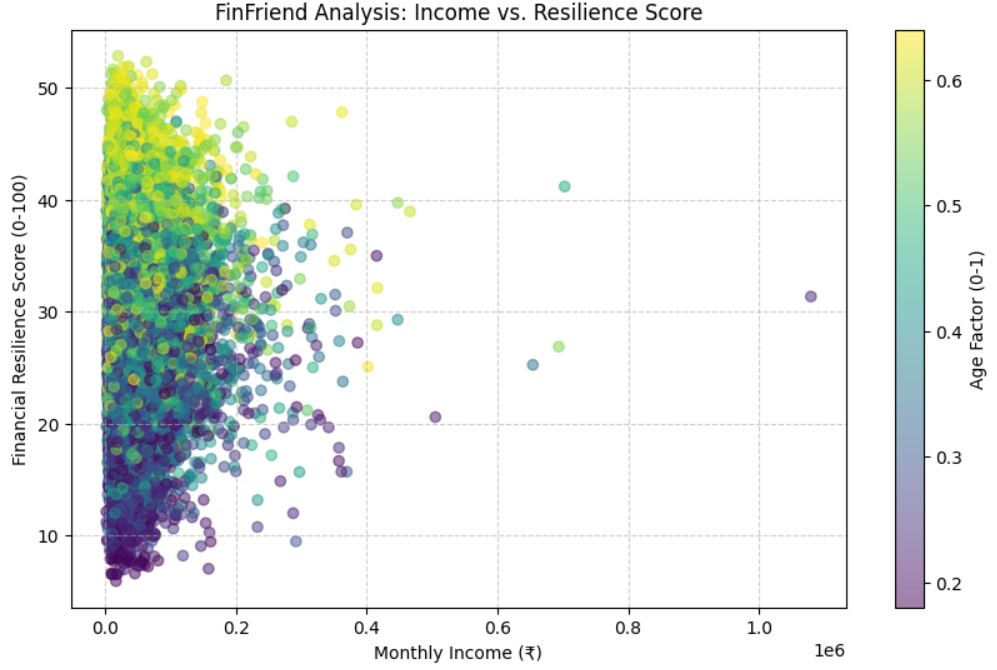

plotting of income vs resilience score

Inspiration

The inspiration for FinFriend came from observing the unique financial landscape of the Indian middle class. In India, financial planning is often a conversation held at kitchen tables, driven by intuition rather than data. While there are countless apps to track expenses, there are very few that provide a personalized benchmark for savings.

What it does

AI-Driven Savings Benchmarking: Unlike standard calculators that use flat percentages (e.g., "save 20%"), FinFriend uses a Random Forest Regressor to compare your profile—income, age, city tier, and dependents—against thousands of similar data points to predict a realistic, high-performance savings target.

The Financial Resilience Score: A custom-engineered metric built with NumPy that evaluates your "financial health" on a scale of 0–100. It doesn't just look at how much you have; it looks at your disposable income ratio weighted against your life stage (age factor).

Context-Aware Analysis: The system understands the economic difference between a Student in a Tier 3 city and a Professional in a Tier 1 city, adjusting its "advice" and predictions to match local cost-of-living realities.

Visual Budget Composition: Using Matplotlib, the app generates a real-time "Budget Pie" that visually separates your predicted savings target from your fixed costs (rent, loans, insurance) and lifestyle overhead, giving you instant clarity on your financial leaks.

How we built it

Cleaning: Processed 11,000+ records, removing "impossible" data (where costs exceeded income).

Engineering: Created an Age_Factor to normalize life stages and encoded occupations for the model.

Training: Used Scikit-Learn to build a Random Forest. We split the data 80/20 to ensure the AI could generalize to new users.

Optimization: Tuned the model's "trees" to keep the file lightweight and fast for cloud deployment.

Challenges we ran into

Filtering the "Impossible": Our biggest hurdle was data integrity. Real-world financial surveys are messy; we found many entries where a person's expenses were higher than their total income. We realized that if we let the model learn from this "noise," it would hallucinate impossible savings targets. We had to build a custom Validation Pipeline to scrub these outliers, ensuring our AI only learned from realistic, healthy financial behavior.

Making the Math "Human": We struggled to make the model understand that age isn't just a number—it’s a life stage. A 20-year-old and a 50-year-old have completely different safety nets. We solved this by engineering the Age_Factor and our custom Financial Resilience Score. This shifted our project from a basic "Calculator" to a "Smarter Agent" that actually understands the risks associated with different ages.

Accomplishments that we're proud of

Building a "Socially Aware" AI: We developed a model that understands India’s economic diversity. Our Random Forest distinguishes between the financial realities of Tier 3 towns and Tier 1 metros, providing hyper-localized, meaningful advice.

The Resilience Score Innovation: We engineered a custom Financial Resilience Score using NumPy. By factoring in age-related risks, our model accurately identifies higher risk levels for older users compared to younger individuals in identical financial positions.

Data Integrity Under Pressure: To handle "noisy" data, we built a robust Data Validation Pipeline. This ensures our model is trained on clean, realistic logic, making its final predictions reliable for real-world application.

From Complexity to Clarity: We transformed 11,000+ rows of messy data into actionable insights. Using Matplotlib, we bridged the gap between complex machine learning and human understanding through intuitive visual charts.

What we learned

Data Quality > Model Flashiness: We spent 80% of our time on Data Cleaning and only 20% on the actual ML code. We learned the hard way that "Garbage In, Garbage Out" is the absolute truth of Data Science.

Explainability is Everything: In Fintech, you can't just give a user a number and say "trust the AI." By keeping our project in a notebook, we prioritized Transparency. We can show exactly why our model made a choice, which is the only way to build real financial trust.

The Logic is the Soul: While a flashy UI is nice, the "Soul" of our hackathon entry is the mathematical integrity of this notebook. We focused on building a rock-solid foundation that actually works.

What's next for girlies haconomics

The Transition to a Live App Now that the logic is proven in the notebook, the natural next step is Deployment. We can move this into a Streamlit or Flask application. This would allow a real user to input their data on a mobile phone and get an instant savings recommendation without ever seeing a line of code.

Built With

- jupyter

- kaggle

- matplotlib

- numpy

- pandas

- scikit-learn

Log in or sign up for Devpost to join the conversation.