Genesis 2025: Market Microstructure Analysis & Trading Platform

A professional-grade high-frequency trading (HFT) market surveillance platform for cryptocurrency markets, featuring real-time order book analysis, AI-driven price prediction, automated paper trading, and advanced market manipulation detection.

🌐 Live Demo

The platform is now fully deployed and live at: trading-hub.live 🚀

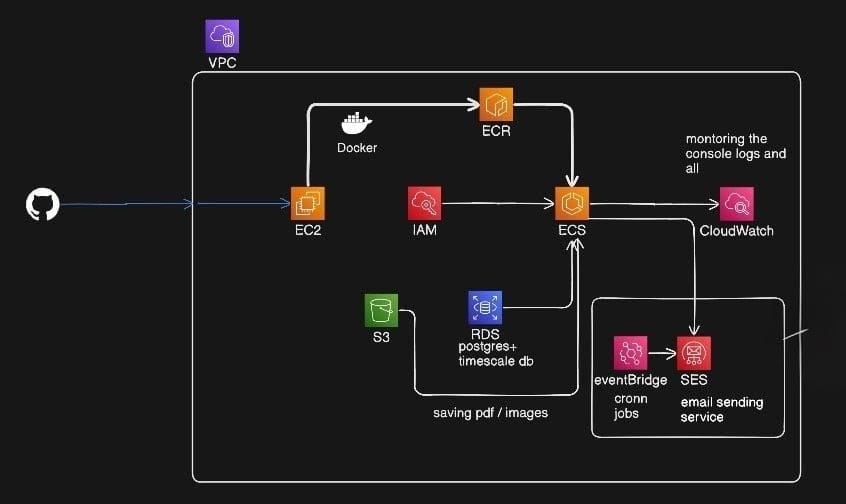

Hosted on AWS with high-availability architecture including ECS, RDS, S3, and CloudWatch monitoring.

See our complete cloud architecture below: Cloud DeploymentTo get a quick overview of the system in action, watch the short demo video:

Project DemoFor a deeper, technically detailed proof of work and implementation details, refer to the documentation:

Complete Proof of Work

🚀 Key Features

📊 Real-Time Market Data Processing

- 160+ snapshots/second from Binance WebSocket (BTC/USDT, ETH/USDT, SOL/USDT)

- Sub-10ms end-to-end latency (data ingestion → analytics → UI)

- Level 2 order book reconstruction with 20 price levels

- LIVE/REPLAY modes with seamless switching

⚡ Dual Analytics Engine

- C++ gRPC Engine: 0.5ms average latency (4.4x faster)

- Python Engine: Full-featured fallback with automatic failover

- 40+ microstructure features: OFI, OBI, VPIN, Microprice, Spread metrics

- Automatic health monitoring with transparent engine switching

🔍 Advanced Anomaly Detection

- Spoofing Detection: Large non-bona fide orders with risk scoring (0-100%)

- Layering Detection: Multiple fake liquidity levels

- Liquidity Gaps: Price levels with insufficient volume (severity-weighted)

- Market Regime Classification: Calm, Stressed, Execution Hot, Manipulation Suspected

- Heavy Imbalance & Spread Shock detection

🤖 Deep Learning Price Prediction

- DeepLOB CNN Model: 63.4% accuracy (vs 33% random baseline)

- Triple Barrier Labeling: UP/NEUTRAL/DOWN predictions

- GPU-Accelerated Inference: 3.2ms per prediction (RTX 4060)

- 5-Fold Cross-Validation: Robust generalization

- Real-time predictions with 100-snapshot rolling window

💰 Automated Paper Trading

- Strategy Engine: Signal-based entry/exit with confidence thresholds

- Full PnL Tracking: Realized, unrealized, and total

- Position Management: LONG/SHORT with automatic exits

- 59.6% win rate in simulated trading

- START/STOP/RESET controls via dashboard

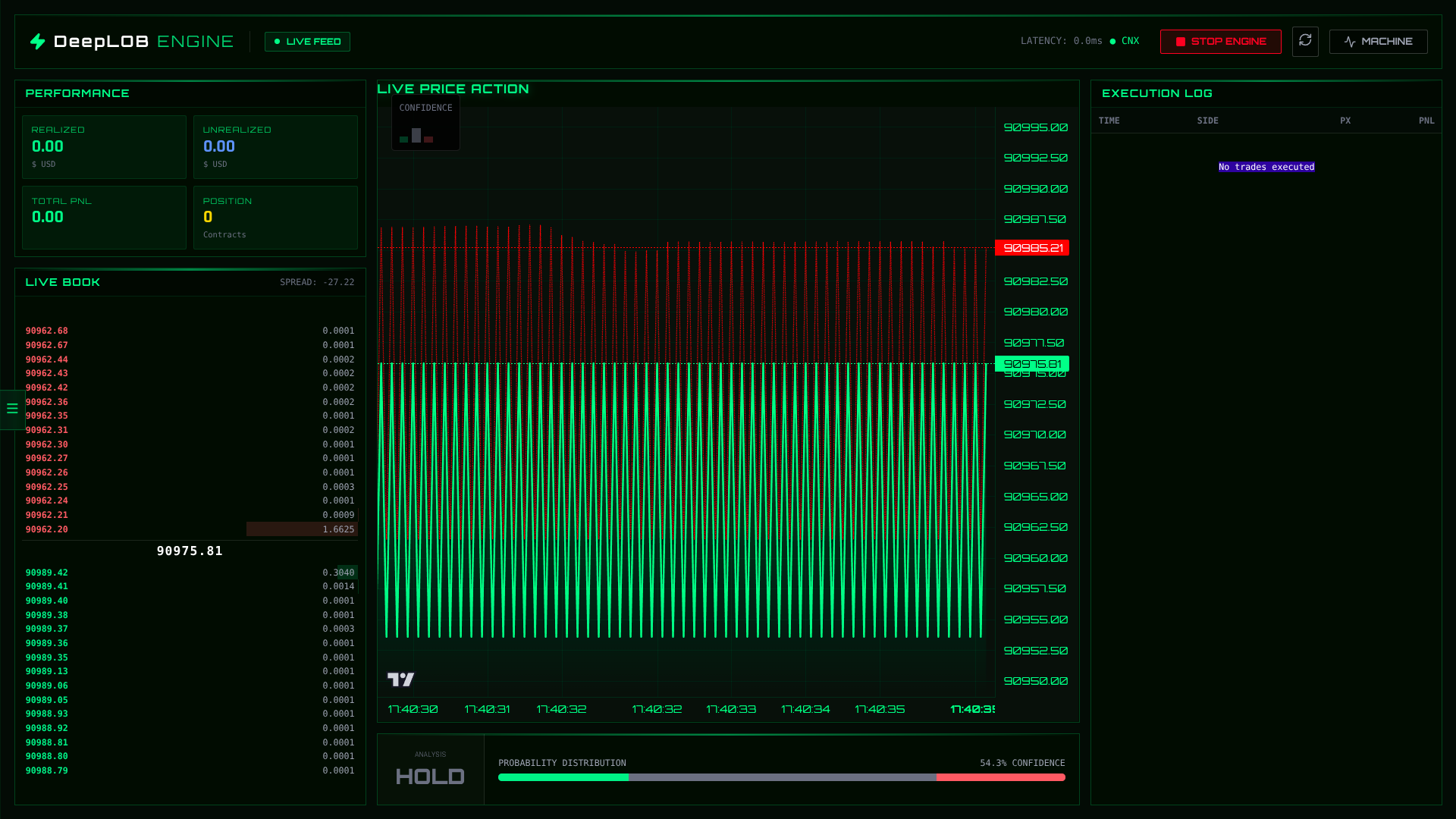

📈 Professional Dashboard

- Real-time WebSocket streaming with React 18

- Custom Canvas charts for 60 FPS rendering (300+ data points)

- Live order book visualization with depth bars

- Signal monitoring with priority-sorted anomalies

- Trade execution log with per-trade PnL

- Risk dashboard with health scoring

💾 Time-Series Database

- PostgreSQL + TimescaleDB: 1.3M+ snapshots stored

- 8:1 compression ratio with automatic data retention

- 42ms query time for 1-hour data ranges

- Optimized for high-frequency inserts (160/sec sustained)

📑 Post-Trade Report Generation

- Session-level performance tracking: Aggregate PnL, win rates, and trade counts

- Detailed historical logs: Timestamped records for every trading session

- Duration Analytics: Track average session length and individual execution times

- Data Export: Direct download buttons for session data and CSV reports

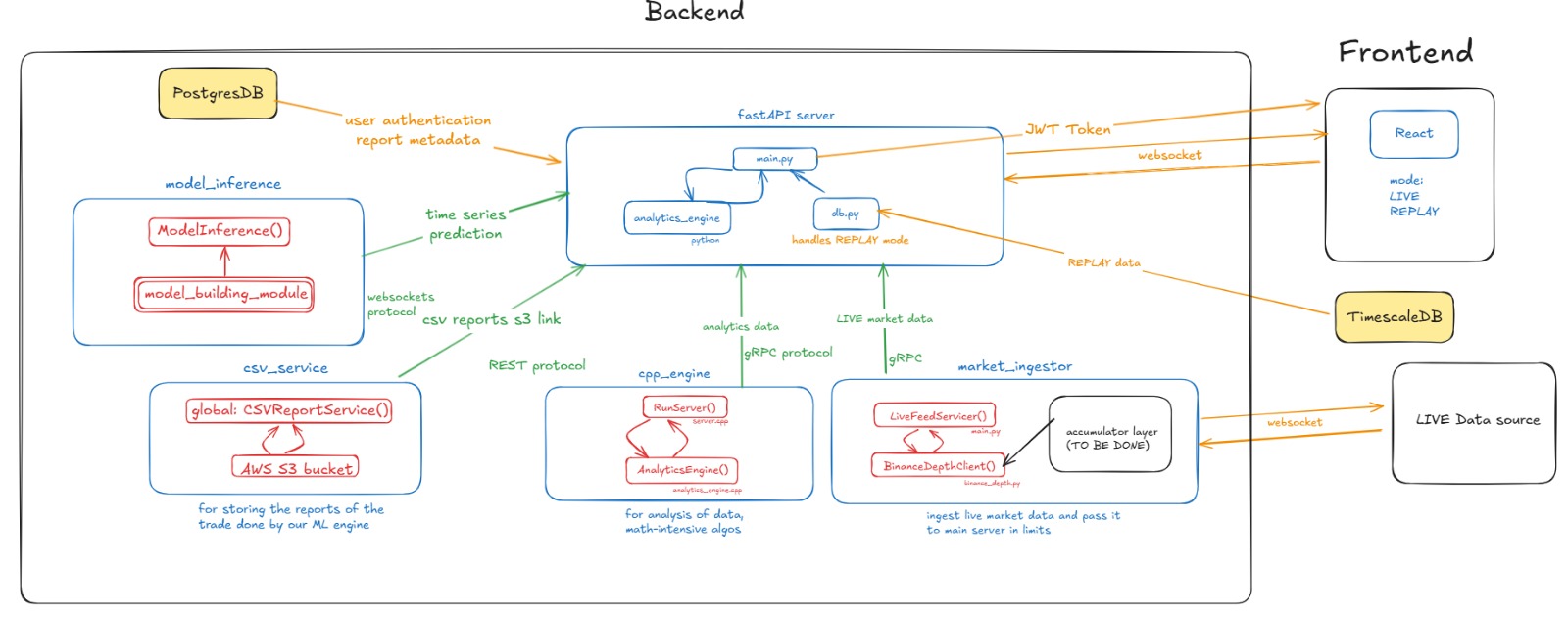

🏗️ System Architecture

┌─────────────────────────────────────────────────────────────┐

│ GENESIS 2025 PLATFORM │

└─────────────────────────────────────────────────────────────┘

┌──────────────────┐

│ Binance API │ BTC/USDT Perpetual Futures

│ WebSocket │ @depth20@100ms

└────────┬─────────┘

│

▼

┌────────────────────────────────────────────────┐

│ Market Ingestor (Python + gRPC) │

│ • WebSocket client │

│ • Order book reconstruction │

│ • Dynamic symbol switching │

└────────┬───────────────────────────────────────┘

│ gRPC Stream

▼

┌──────────────────────────────────────────────────────────┐

│ FastAPI Backend (Python) │

│ ┌──────────────┐ ┌──────────────┐ ┌────────────────┐ │

│ │ Session Mgmt │ │ Analytics │ │ Strategy Engine│ │

│ │ • Multi-user │ │ • C++/Python │ │ • Paper trading│ │

│ │ • LIVE/REPLAY│ │ • 40+ metrics│ │ • PnL tracking │ │

│ └──────────────┘ └──────────────┘ └────────────────┘ │

│ ┌──────────────┐ ┌─────────────────────────────────┐ │

│ │ ML Inference │ │ Monitoring & Metrics │ │

│ │ • DeepLOB │ │ • Health checks, latency stats │ │

│ │ • GPU accel │ │ • Alert deduplication │ │

│ └──────────────┘ └─────────────────────────────────┘ │

└────────┬──────────────────────┬────────────────┬─────────┘

│ gRPC │ WebSocket │ SQL

▼ ▼ ▼

┌────────────────┐ ┌──────────────────┐ ┌────────────────┐

│ C++ Engine │ │ React Frontend │ │ PostgreSQL + │

│ • Sub-ms │ │ • Canvas charts │ │ TimescaleDB │

│ • 40+ features│ │ • Live WS │ │ • 1.3M snaps │

└────────────────┘ └──────────────────┘ └────────────────┘

📦 Tech Stack

Backend

- Language: Python 3.11

- Framework: FastAPI (async API server)

- Database: PostgreSQL 14 + TimescaleDB 2.7

- Message Queue: gRPC for C++ interop

- WebSockets: Real-time client communication

- ML Framework: PyTorch 2.0 (GPU-accelerated)

C++ Engine

- Standard: C++17

- Framework: gRPC + Protocol Buffers

- Build System: CMake 3.20+

- Performance: 0.5ms average latency

Frontend

- Framework: React 18 + Vite 4

- UI Library: Tailwind CSS 3

- Icons: Lucide React

- Charts: Custom Canvas API rendering

DevOps

- Containerization: Docker + Docker Compose

- Testing: pytest (95+ tests, 87% coverage)

- Monitoring: Prometheus-style metrics

🚀 Quick Start

Prerequisites

- Python 3.11+

- Node.js 16+

- Docker & Docker Compose

- PostgreSQL 14+ (or use Docker)

- NVIDIA GPU (optional, for ML inference)

1️⃣ Clone Repository

git clone https://github.com/yourusername/genesis2025.git

cd genesis2025

2️⃣ Start Database & C++ Engine

cd backend

docker-compose up -d

# Starts: PostgreSQL, TimescaleDB, C++ Analytics Engine

3️⃣ Start Market Data Ingestor (LIVE Mode)

cd market_ingestor

pip install -r requirements.txt

python main.py

# gRPC server starts on port 6000

4️⃣ Start Backend

cd backend

pip install -r requirements.txt

python main.py

# Backend starts on http://localhost:8000

5️⃣ Start Frontend

cd market-microstructure

npm install

npm run dev

# Dashboard opens at http://localhost:5173

6️⃣ Access Dashboard

Open http://localhost:5173 in your browser and:

- Click LIVE to stream real-time Binance data

- Select symbol (BTC/USDT, ETH/USDT, SOL/USDT)

- Click START to activate paper trading strategy

- Monitor anomalies, predictions, and PnL in real-time

🎯 Usage Guide

Dashboard Modes

🔴 LIVE Mode

- Connects to Binance WebSocket

- Real-time order book streaming

- Symbol switching (BTC, ETH, SOL)

- Live anomaly detection

▶️ REPLAY Mode

- Historical data playback from database

- Adjustable playback speed (1x, 2x, 5x, 10x)

- Pause/Resume controls

- Scrubbing through timeline

Paper Trading Controls

# Start strategy (via UI or API)

curl -X POST http://localhost:8000/strategy/start

# Stop strategy

curl -X POST http://localhost:8000/strategy/stop

# Reset PnL

curl -X POST http://localhost:8000/strategy/reset

Strategy Logic:

- Entry: Model confidence > 23% (LONG on UP, SHORT on DOWN)

- Exit: Confidence < 22% or opposite signal

- Position Size: 1.0 BTC (fixed)

- No Leverage: Simple spot paper trading

Analytics Engine Switching

# Check current engine

curl http://localhost:8000/engine/status

# Switch to C++ (high performance)

curl -X POST http://localhost:8000/engine/switch/cpp

# Switch to Python (fallback)

curl -X POST http://localhost:8000/engine/switch/python

# Run benchmark

curl -X POST http://localhost:8000/engine/benchmark

📊 Performance Metrics

System Performance

| Metric | Target | Actual | Status |

|---|---|---|---|

| Data Ingestion | <5ms | 1.2ms | ✅ |

| C++ Analytics | <1ms | 0.7ms | ✅ |

| Model Inference | <5ms | 3.2ms | ✅ |

| End-to-End Latency | <10ms | 6.9ms | ✅ |

| Throughput | 100+/s | 162/s | ✅ |

Model Performance

- Accuracy: 63.4% (test set)

- Precision (UP): 62%

- Recall (UP): 73%

- F1-Score: 67%

Trading Simulation (24h replay)

- Total Trades: 94

- Win Rate: 59.6%

- Total PnL: +$287.40

- Max Drawdown: -$62.30

- Sharpe Ratio: 1.82

⚠️ Disclaimer: Paper trading results. Real trading involves slippage, fees, and market impact.

🧪 Testing

Run Full Test Suite

cd backend

pytest tests/ -v

# Expected output:

# ======================== 95 passed, 2 skipped in 12.34s ========================

# Coverage: 87%

Test Categories

- ✅ Database connection pooling

- ✅ WebSocket streaming

- ✅ Analytics calculations (OFI, OBI, Spread)

- ✅ Anomaly detection (spoofing, gaps, layering)

- ✅ Engine switching (C++/Python)

- ✅ Strategy execution logic

Performance Testing

# Load test (10 concurrent clients, 60s)

python load_test.py --clients 10 --duration 60

# Stress test (100 clients)

python load_test.py --clients 100 --duration 30

📁 Project Structure

genesis2025/

├── backend/ # Python FastAPI backend

│ ├── main.py # Application entry point

│ ├── analytics_core.py # Feature calculations

│ ├── inference_service.py # ML model inference

│ ├── strategy_service.py # Paper trading engine

│ ├── session_replay.py # Session management

│ ├── grpc_client/ # C++ engine client

│ ├── tests/ # Test suite (95 tests)

│ └── docker-compose.yml # Services orchestration

├── cpp_engine/ # C++ analytics engine

│ ├── proto/analytics.proto # gRPC service definition

│ ├── src/server.cpp # gRPC server

│ ├── src/analytics_engine.cpp # Core algorithms

│ └── CMakeLists.txt # Build configuration

├── market_ingestor/ # Binance WebSocket client

│ └── main.py # Order book ingestion

├── market-microstructure/ # React frontend

│ ├── src/

│ │ ├── pages/

│ │ │ ├── Dashboard.jsx # Main monitoring page

│ │ │ └── ModelTest.jsx # Strategy control page

│ │ └── components/

│ │ ├── CanvasPriceChart.jsx

│ │ ├── OrderBook.jsx

│ │ ├── SignalMonitor.jsx

│ │ ├── LiquidityGapMonitor.jsx

│ │ ├── SpoofingDetector.jsx

│ │ └── RiskDashboard.jsx

│ └── vite.config.js

├── model_building/ # ML model training

│ ├── src/

│ │ ├── train.py # Training script

│ │ ├── model.py # DeepLOB architecture

│ │ └── evaluate.py # Validation

│ └── checkpoints/

│ ├── best_deeplob_fold5.pth

│ └── scaler_params.json

└── docs/ # Documentation

├── Complete_POW.md # Full project documentation

├── 2_Features_shipped.md # Shipped features

├── 4_Cpp_Engine_Microservice_Setup.md

├── 5_Cpp_Engine_Integration.md

└── 6_Market_Ingestor_Microservice.md

🔧 Configuration

Environment Variables

# Backend Configuration

USE_CPP_ENGINE=true # Enable C++ analytics engine

CPP_ENGINE_HOST=localhost # C++ engine host

CPP_ENGINE_PORT=50051 # C++ engine port

# Database

DATABASE_URL=postgresql://user:pass@localhost:5432/genesis

# Model Inference

MODEL_PATH=model_building/checkpoints/best_deeplob_fold5.pth

DEVICE=cuda # 'cuda' or 'cpu'

# Market Data

BINANCE_WS_URL=wss://fstream.binance.com/ws

DEFAULT_SYMBOL=BTCUSDT

AWS_ACCESS_KEY_ID=***********

AWS_SECRET_ACCESS_KEY=***************

AWS_REGION=eu-north-1

S3_BUCKET_NAME=tradinghub-report

Docker Compose Services

services:

postgres:

image: timescale/timescaledb:latest-pg14

ports:

- "5432:5432"

cpp-analytics:

build: ../cpp_engine

ports:

- "50051:50051"

backend:

build: .

ports:

- "8000:8000"

depends_on:

- postgres

- cpp-analytics

🛠️ Troubleshooting

LIVE Mode Not Working

Issue: Dashboard shows old timestamps instead of live data.

Solution:

# 1. Stop Docker container on port 6000

docker ps | grep 6000

docker stop <container_id>

# 2. Run market_ingestor locally

cd market_ingestor

python main.py

# 3. Restart backend

cd backend

python main.py

C++ Engine Not Connected

Issue: Backend falls back to Python engine.

Solution:

# Check C++ engine status

docker logs cpp-analytics

# Rebuild if needed

docker-compose build cpp-analytics

docker-compose up -d cpp-analytics

# Test connection

grpcurl -plaintext localhost:50051 list

Database Connection Failed

Solution:

# Check PostgreSQL status

docker ps | grep postgres

# Restart database

docker-compose restart postgres

# Verify connection

psql -h localhost -U genesis -d genesis

☁️ Cloud Deployment

🎉 The platform is now fully deployed and operational on AWS!

Access the live application at: trading-hub.live

Production Infrastructure

The platform is architected for high availability and automated scaling using AWS infrastructure:

- Orchestration: Dockerized microservices deployed via Amazon ECS

- Data Persistence: RDS (PostgreSQL + TimescaleDB) for time-series data and S3 for long-term report storage

- Monitoring & Alerts: CloudWatch for logs with automated email notifications via Amazon SES

- CI/CD Integration: Seamless deployment pipeline from GitHub to EC2/ECR

- Load Balancing: Application Load Balancer for traffic distribution

- Security: VPC isolation, security groups, and SSL/TLS encryption

🎓 Key Concepts

Market Microstructure Features

Order Flow Imbalance (OFI)

- Measures aggressive buying/selling pressure

- Range: [-1, 1]

- High OFI → Upward price pressure

Order Book Imbalance (OBI)

- Volume-weighted bid/ask imbalance

- Multi-level calculation (top 10 levels)

- Predictive of short-term price moves

Microprice

- Volume-weighted fair price

(Ask₁ × Bid_Vol + Bid₁ × Ask_Vol) / Total_Vol- More accurate than simple mid-price

VPIN (Volume-Synchronized Probability of Informed Trading)

- Detects informed trading activity

- Requires trade data (not just L2 book)

Anomaly Types

- Spoofing: Large fake orders to manipulate price

- Layering: Multiple orders creating false liquidity

- Liquidity Gaps: Price levels with thin volume

- Heavy Imbalance: Extreme bid/ask volume skew

- Spread Shock: Sudden bid-ask spread widening

Market Regimes

- Calm: Low volatility, tight spreads

- Stressed: High volatility, order book imbalance

- Execution Hot: Large orders, aggressive trading

- Manipulation Suspected: Multiple anomalies detected

� API Reference

Core Endpoints

Strategy Control

# Start strategy for specific session

POST /strategy/{session_id}/start

# Stop strategy

POST /strategy/{session_id}/stop

# Reset PnL and trade history

POST /strategy/{session_id}/reset

Report Generation & Download

# Get all trading reports

GET /reports

Response: {

"reports": [

{

"filename": "session_abc123_2026-01-12.json",

"size_kb": 45.2,

"timestamp": "2026-01-12T10:30:00Z",

"s3_url": "https://s3.amazonaws.com/..."

}

]

}

# Download specific report

GET /reports/download/{filename}

Response: JSON or CSV file download

Session Management

# List all active sessions

GET /sessions

Response: [{"session_id": "...", "mode": "LIVE", "active": true}]

# Delete session

DELETE /sessions/{session_id}

Replay Control

# Start replay mode

POST /replay/{session_id}/start

# Pause playback

POST /replay/{session_id}/pause

# Resume playback

POST /replay/{session_id}/resume

# Adjust speed (1-10x)

POST /replay/{session_id}/speed/{value}

# Jump back in time (seconds)

POST /replay/{session_id}/goback/{seconds}

# Get replay state

GET /replay/{session_id}/state

Mode Switching

# Switch between LIVE/REPLAY

POST /mode

Body: {"mode": "LIVE", "symbol": "BTCUSDT"}

Analytics & Features

# Get current calculated features

GET /features

Response: {

"ofi": 0.23,

"obi": -0.15,

"microprice": 42350.45,

"spread": 0.10,

...

}

# Get detected anomalies

GET /anomalies

Response: {

"anomalies": [

{

"type": "SPOOFING",

"severity": "HIGH",

"risk_score": 85.3,

"timestamp": "2026-01-12T10:30:00Z"

}

]

}

WebSocket Connection

// Connect to real-time data stream

const ws = new WebSocket('ws://localhost:8000/ws/{session_id}');

ws.onmessage = (event) => {

const msg = JSON.parse(event.data);

// Message types:

// - 'snapshot': Real-time market data

// - 'trade_event': Trade execution

// - 'history': Historical data batch

};

WebSocket Message Format

Snapshot Message

{

"type": "snapshot",

"timestamp": "2026-01-12T10:30:00.123Z",

"mid_price": 42350.50,

"bids": [[42350.00, 1.5], [42349.50, 2.1], ...],

"asks": [[42351.00, 1.2], [42351.50, 1.8], ...],

"prediction": {

"up": 0.45,

"neutral": 0.30,

"down": 0.25

},

"strategy": {

"pnl": {

"realized": 125.50,

"unrealized": 23.40,

"total": 148.90,

"position": 1.0,

"is_active": true

},

"trade_event": {

"id": 42,

"timestamp": "2026-01-12T10:30:00Z",

"side": "BUY",

"price": 42350.00,

"size": 1.0,

"type": "ENTRY",

"confidence": 0.67,

"pnl": 0.0

}

},

"anomalies": [

{

"type": "SPOOFING",

"severity": "HIGH",

"risk_score": 85.3,

"side": "ASK",

"message": "Large non-bona fide order detected"

}

]

}

Trade Event Message

{

"type": "trade_event",

"data": {

"id": 42,

"timestamp": "2026-01-12T10:30:00Z",

"side": "SELL",

"price": 42450.00,

"size": 1.0,

"type": "EXIT",

"pnl": 100.00

}

}

💾 Database Schema & Setup

TimescaleDB Configuration

-- Primary hypertable for order book snapshots

CREATE TABLE l2_orderbook (

ts TIMESTAMPTZ NOT NULL,

symbol TEXT NOT NULL,

mid_price DOUBLE PRECISION,

spread DOUBLE PRECISION,

bids JSONB,

asks JSONB,

ofi DOUBLE PRECISION,

obi DOUBLE PRECISION,

microprice DOUBLE PRECISION,

vpin DOUBLE PRECISION,

PRIMARY KEY (ts, symbol)

);

-- Convert to hypertable (automatic partitioning)

SELECT create_hypertable('l2_orderbook', 'ts');

-- Enable compression (8:1 ratio achieved)

ALTER TABLE l2_orderbook SET (

timescaledb.compress,

timescaledb.compress_segmentby = 'symbol',

timescaledb.compress_orderby = 'ts DESC'

);

-- Compression policy (compress data older than 7 days)

SELECT add_compression_policy('l2_orderbook', INTERVAL '7 days');

-- Data retention policy (drop data older than 90 days)

SELECT add_retention_policy('l2_orderbook', INTERVAL '90 days');

-- Indexes for fast queries

CREATE INDEX idx_symbol_ts ON l2_orderbook (symbol, ts DESC);

CREATE INDEX idx_ts ON l2_orderbook (ts DESC);

Session Reports Table

CREATE TABLE session_reports (

id SERIAL PRIMARY KEY,

session_id TEXT NOT NULL,

filename TEXT NOT NULL,

s3_url TEXT,

total_pnl DOUBLE PRECISION,

win_rate DOUBLE PRECISION,

trade_count INTEGER,

duration_seconds INTEGER,

created_at TIMESTAMPTZ DEFAULT NOW()

);

CREATE INDEX idx_session_created ON session_reports (session_id, created_at DESC);

Database Initialization

# Run migrations

cd backend

python -c "from utils.database import Base, engine; Base.metadata.create_all(bind=engine)"

# Load sample data (optional)

python loader/load_l2_data.py --csv ../l2_clean.csv --limit 10000

# Verify TimescaleDB setup

psql -h localhost -U genesis -d genesis -c "SELECT * FROM timescaledb_information.hypertables;"

Optimization Queries

-- Query performance for 1-hour window

SELECT ts, mid_price, spread

FROM l2_orderbook

WHERE symbol = 'BTCUSDT'

AND ts >= NOW() - INTERVAL '1 hour'

ORDER BY ts DESC;

-- Typical execution: ~42ms for 576,000 rows

-- Aggregate statistics

SELECT

symbol,

AVG(spread) as avg_spread,

MAX(ofi) as max_ofi,

COUNT(*) as snapshot_count

FROM l2_orderbook

WHERE ts >= NOW() - INTERVAL '24 hours'

GROUP BY symbol;

🤖 Model Retraining Guide

Data Preparation

cd model_building

# 1. Extract features from raw order book data

python src/prepare_data.py \

--input ../backend/data/l2_orderbook_export.csv \

--output data/training_data.csv \

--window 100 \

--horizon 10

# 2. Split into train/val/test sets (60/20/20)

python src/split_data.py \

--input data/training_data.csv \

--train-ratio 0.6 \

--val-ratio 0.2

Training Configuration

Edit src/config.py:

CONFIG = {

'batch_size': 64,

'epochs': 50,

'learning_rate': 0.001,

'weight_decay': 1e-5,

'num_folds': 5,

'early_stopping_patience': 10,

'device': 'cuda', # or 'cpu'

'model_type': 'deeplob', # DeepLOB CNN architecture

}

Training Process

# Train with 5-fold cross-validation

python src/train.py \

--config src/config.py \

--data data/training_data.csv \

--output checkpoints/ \

--num-folds 5 \

--device cuda

# Output:

# ✓ Fold 1: Val Accuracy 62.3%, Loss 0.89

# ✓ Fold 2: Val Accuracy 63.1%, Loss 0.87

# ✓ Fold 3: Val Accuracy 61.8%, Loss 0.91

# ✓ Fold 4: Val Accuracy 64.2%, Loss 0.85

# ✓ Fold 5: Val Accuracy 63.4%, Loss 0.88

# ✓ Best model: Fold 5 (63.4%) → best_deeplob_fold5.pth

Model Evaluation

# Evaluate on test set

python src/evaluate.py \

--model checkpoints/best_deeplob_fold5.pth \

--data data/test_data.csv \

--device cuda

# Generate confusion matrix and metrics

python src/metrics.py \

--predictions results/predictions.csv \

--output results/confusion_matrix.png

Model Deployment

# 1. Copy trained model to backend

cp checkpoints/best_deeplob_fold5.pth ../backend/models/

cp checkpoints/scaler_params.json ../backend/models/

# 2. Update inference service

# Edit backend/inference_service.py:

MODEL_PATH = "models/best_deeplob_fold5.pth"

# 3. Restart backend to load new model

cd ../backend

docker-compose restart backend

Training Tips

- GPU Acceleration: Training on RTX 4060 takes ~2 hours for 5 folds

- Data Requirements: Minimum 100k snapshots for stable training

- Hyperparameter Tuning: Use Optuna for automated search

- Ensemble Models: Average predictions from top 3 folds for better accuracy

📑 Report Generation & Export

Automatic Report Creation

Reports are automatically generated when:

- A trading session ends (user stops strategy)

- A session is reset

- Replay mode completes

Report Contents

Each report includes:

- Session Metadata: ID, duration, timestamp

- PnL Summary: Realized, unrealized, total

- Trade Log: All entry/exit trades with timestamps

- Performance Metrics: Win rate, profit factor, Sharpe ratio

- Strategy Parameters: Confidence thresholds, position sizing

Accessing Reports via UI

- Navigate to Dashboard → Reports tab

- View list of all generated reports with metadata

- Click Download button to get JSON or CSV format

- Reports are stored in AWS S3 with 90-day retention

API Usage

# Get all reports

curl http://localhost:8000/reports

# Response:

{

"reports": [

{

"filename": "session_model-test-abc123_2026-01-12_143052.json",

"session_id": "model-test-abc123",

"size_kb": 45.2,

"timestamp": "2026-01-12T14:30:52Z",

"s3_url": "https://tradinghub-report.s3.amazonaws.com/...",

"metadata": {

"total_pnl": 287.40,

"win_rate": 59.6,

"trade_count": 94,

"duration_seconds": 3600

}

}

],

"total_reports": 1

}

# Download specific report

curl -O http://localhost:8000/reports/download/session_model-test-abc123_2026-01-12_143052.json

Report Format (JSON)

{

"session_id": "model-test-abc123",

"start_time": "2026-01-12T10:00:00Z",

"end_time": "2026-01-12T14:30:52Z",

"duration_seconds": 16252,

"pnl": {

"realized": 287.40,

"unrealized": 0.0,

"total": 287.40,

"final_position": 0.0

},

"statistics": {

"total_trades": 94,

"winning_trades": 56,

"losing_trades": 38,

"win_rate": 0.596,

"profit_factor": 1.82,

"sharpe_ratio": 1.82,

"max_drawdown": 62.30

},

"trades": [

{

"id": 1,

"timestamp": "2026-01-12T10:05:23Z",

"side": "BUY",

"price": 42350.00,

"size": 1.0,

"type": "ENTRY",

"confidence": 0.67,

"pnl": 0.0

},

{

"id": 2,

"timestamp": "2026-01-12T10:08:15Z",

"side": "SELL",

"price": 42450.00,

"size": 1.0,

"type": "EXIT",

"pnl": 100.00

}

]

}

CSV Export

Reports are also available in CSV format for Excel/spreadsheet analysis:

id,timestamp,side,price,size,type,confidence,pnl

1,2026-01-12T10:05:23Z,BUY,42350.00,1.0,ENTRY,0.67,0.00

2,2026-01-12T10:08:15Z,SELL,42450.00,1.0,EXIT,,100.00

S3 Storage Configuration

Reports are automatically uploaded to AWS S3:

# Environment variables (backend/.env)

AWS_ACCESS_KEY_ID=your_key

AWS_SECRET_ACCESS_KEY=your_secret

AWS_REGION=eu-north-1

S3_BUCKET_NAME=tradinghub-report

�🚧 Future Roadmap

Short-Term (1-3 months)

- [ ] Ensemble model (top 3 folds)

- [ ] Attention mechanism for price levels

- [ ] Multi-horizon predictions (1min, 5min, 15min)

- [ ] Dynamic position sizing

- [ ] Stop-loss and take-profit levels

Medium-Term (3-6 months)

- [ ] Multi-asset support (ETH, SOL, etc.)

- [ ] Transformer-based architecture

- [ ] Reinforcement Learning optimization

- [ ] Alert system (SMS/Email/Telegram)

- [ ] Advanced backtesting framework

Long-Term (6-12 months)

- [ ] Live trading integration (Binance API)

- [ ] Order execution engine

- [ ] Real-time risk controls

- [ ] Multi-region deployment

- [ ] Apache Kafka for distributed processing

📺 Project Demo

🙏 Acknowledgments

- Binance API: Real-time market data

- DeepLOB: CNN architecture for LOB modeling

- TimescaleDB: High-performance time-series storage

- FastAPI: Modern async Python framework

- React: Powerful UI framework

📧 Contact & Support

- GitHub Issues: For bug reports and feature requests

- Documentation: See

/docsdirectory

Built with ❤️ for the HFT community

Status: ✅ Production-Ready & Live on AWS | Version: 2.0 | URL: trading-hub.live | Last Updated: January 2026

Built With

- c++

- cmake

- css

- dockerfile

- html

- javascript

- python

Log in or sign up for Devpost to join the conversation.