-

-

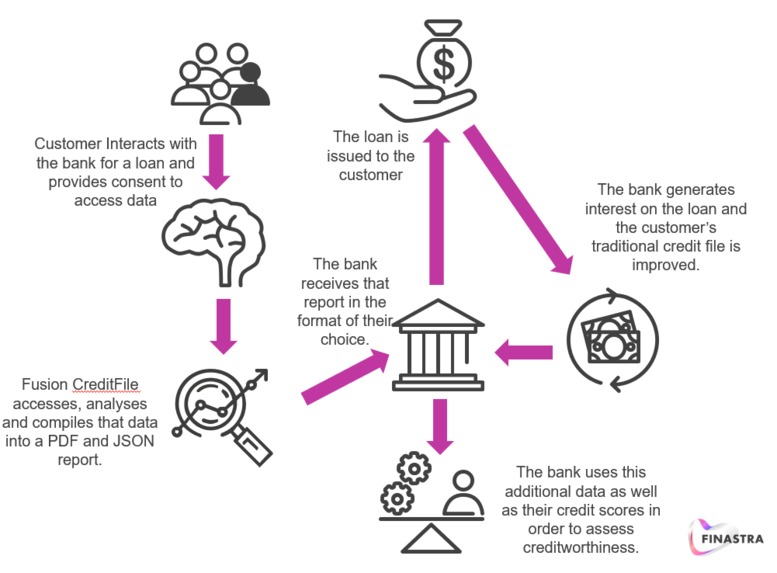

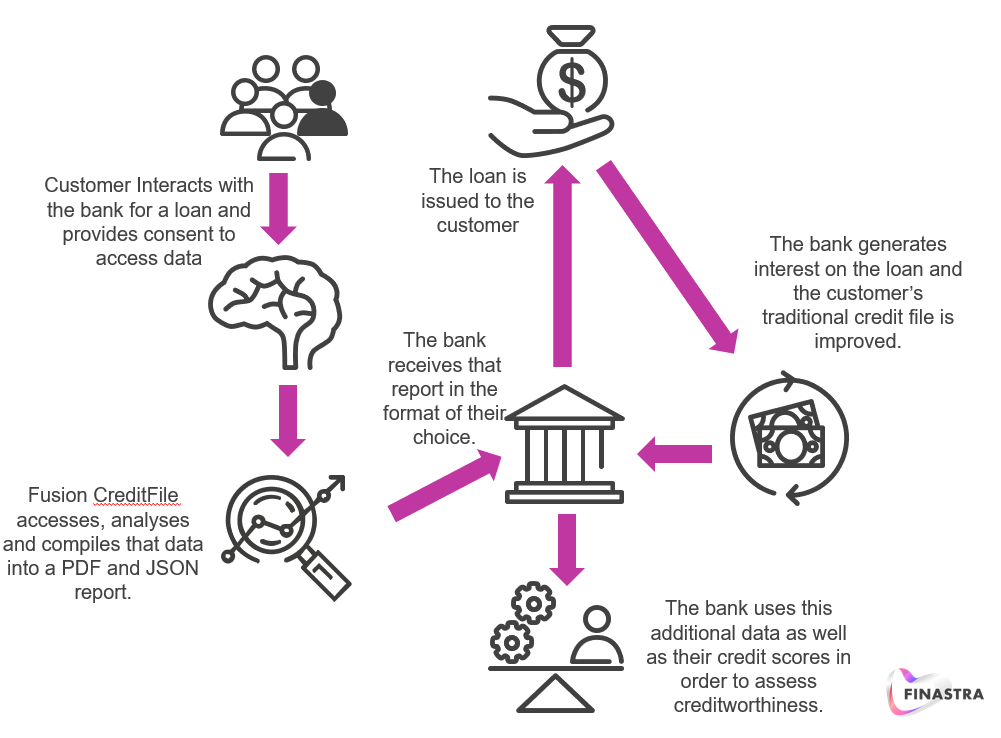

How the Banks Win?

-

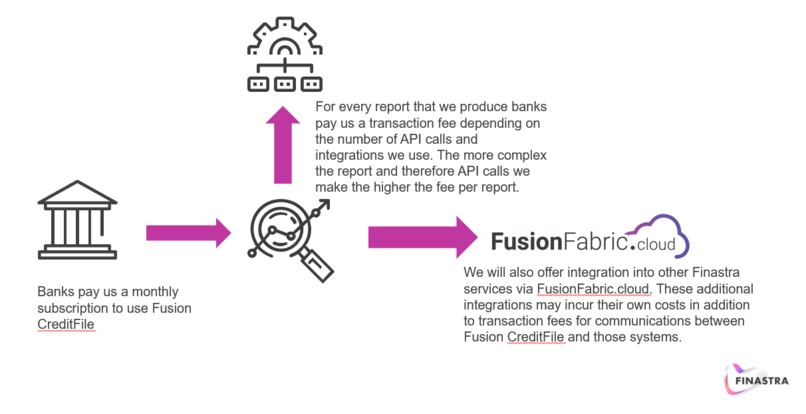

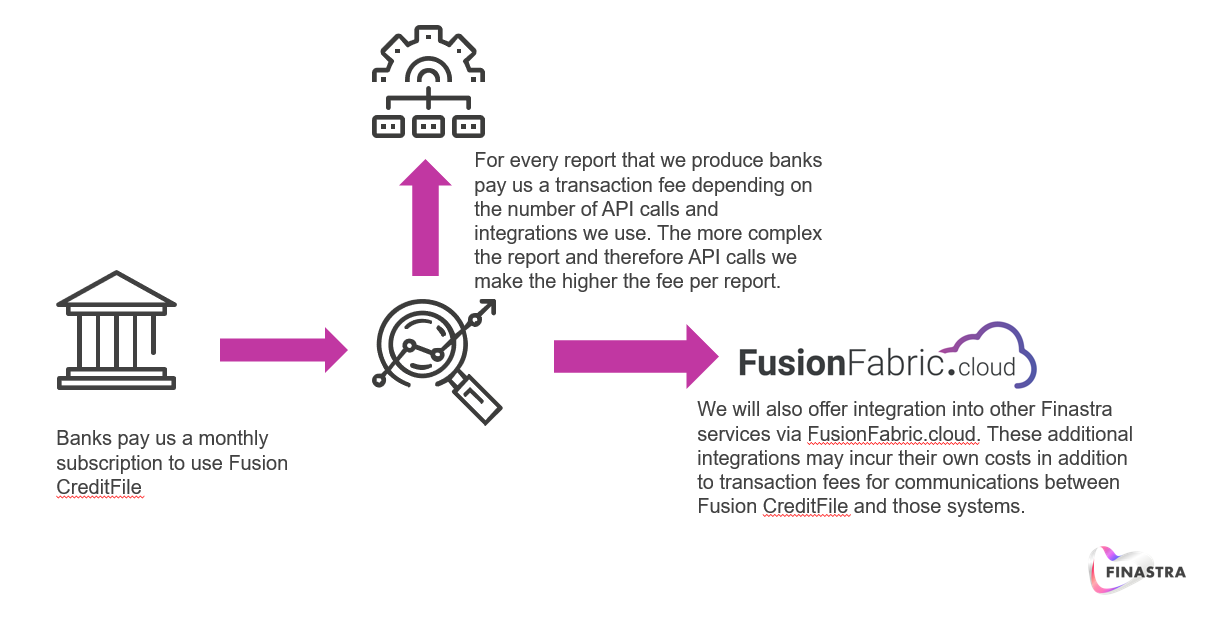

How is the product viable?

Inspiration

Fusion CreditFile was inspired by the difficulties some of us have had in recent years gaining access to credit. It goes much further than just this though. Businesses, self-employed individuals and in particular individuals between the ages of 18 and 30 find it incredibly difficult to gain access to credit. This is usually down to a number of factors:

- They've never borrowed before or are from backgrounds that distrust credit / borrowing

- The pandemic has ruined their balance sheet forcing them into difficult situations where they may have struggled to pay back loans on time or have had to engage services to assist them which have damaged their credit rating.

- Thin file clients may have a strong borrowing history with one credit reference agency but not with another as they are relatively new to the borrowing scene. As a result banks may refuse perfectly creditworthy individuals due to deficient information.

This model is broken. We need to start giving credit where credit is due, rewarding people for all-round positive and beneficial borrowing and banking practices and provide lenders with a more rounded view of potential borrowers so they can make better, more informed decisions about thin-file clients.

What it does

Fusion CreditFile works on a number of different levels to simplify the lending journey for both lenders and borrowers.

For the borrower they can easily control access to the data that is used to assess their creditworthiness. The more data they give, the more chance they've got of being approved and it also provides thin-file clients with an opportunity for their alternative positive banking trends (like income being greater than outgoings or savings) to work towards helping them build a credit report in order to apply for higher value loans like mortgages. It also means that utility bills and rent payments will be able to contribute towards your credit score for the first time ever thanks to the integration into Fusion CreditSense and Fusion OpenBanking.

For the lender they gain access to thin-file clients that their previous risk models would have rejected, increasing their target addressable market and investment potential. It also provides them with a more rounded view of clients as more data will be available on each client, not just how much have you successfully borrowed in the past, but are you a responsible financial citizen. It also simplifies the new lending journey for financial institutions. There are so many fintechs and other companies out there performing alternative credit scoring of some variety or another. No one solution is adequate to provide a reliable assessment as to creditworthiness, and integrating into multiple (perhaps dozens) of different sources and systems would take a great deal of time and cost a relative fortune before lenders would see any return on investment. By centralising these integrations into a central "super-gateway" banks need only integrate into one system, ours, and we handle the integrations into all of the other systems for them. Lenders can even configure via the screens what credentials and which applications should be used to ensure their integrations stay secure and only the applications they have negotiated the best deals with are used to reduce their cost and improve their risk-management.

How we built it

We built Fusion CreditFile using a blend of the following technologies:

- MySQL

- Microservices & Docker containers

- Python

- Django

- Tensorflow & NLP

- Machine Learning (from Fusion CreditSense)

- Angular

We chose to build the application using a number of different microservices in order to allow scalability. We can bolt on any additional services to the main application without having to bring any of the core services down. It also allowed us to work really well despite the fact we live hundreds of miles apart from one another.

We each worked on different elements of the system. Nkiru helped us iron out issues with the business rationale and focus our efforts in the most impactful area, Steven focused on the NLP elements due to his background in that area. Alan's extensive experience with API's and OpenBanking made him the perfect candidate to develop those elements and the reports. Finally, I worked on the gateway architecture and bringing the various components of the system together.

Challenges we ran into

Due to the distance between us all, it was difficult to find the time and organise effectively as a team in order to get the project done in time. It was also a challenge to integrate effectively into Finastra API's due to the distance between us and the complications that posed for organisation. We figured it out in the end and we believe we have a solid product and we're excited at the potential to bring this forward and make a real difference in the world.

Accomplishments that we're proud of

Despite the logistical challenges, we've brought a great deal of technology and concepts to bear in order to produce the prototype in our video. We're proud of what we've achieved technologically but also the business case we've put forward. There are dozens if not hundreds of different companies now, from Provenir to Stripe, all working to solve the alternative credit scoring model. We've identified expertise on our end to analyse SAP data for businesses as well as utilise OpenBanking data, however access to mobile app usage and other important data rests in the realms of a number of other stakeholders in the industry. Instead of reinventing the wheel we're simplifying and Opening the integration into those services with a single gateway. A single gateway that allows institutions to configure new integrations into other platforms and services with the click of a button instead of having to engage (potentially expensive) development resources.

What we learned

We learned a great deal about the current credit scoring system and the players that are out there today investing in alternative credit scoring. We originally thought we would develop an idea that would compete against those competitors however having seen the investment, science and data that they are working with we identified that there wasn't a real gap there to fill. There was however a gap in connecting these different scoring and analysis applications together under a single integration gateway. Once we identified this gap we pressed forward to produce the application you see before you.

What's next for Fusion CreditFile

Next for Fusion CreditFile we need to move it into MVP status. In order to do that we need to identify a number of key alternative scoring applications and systems that we should integrate into as well as finish development on our SAP / AR file processing capabilities in order to provide a wide range of tools necessary to prepare the most robust reporting possible for our clients.

Once this is done we will need to explore Finastra's Banking as a Service and Trust Machine products in depth to align with the potential go-to-market synergies there.

Log in or sign up for Devpost to join the conversation.