-

-

Speeding up access to financial support for SMEs with Flint

-

Our mission

-

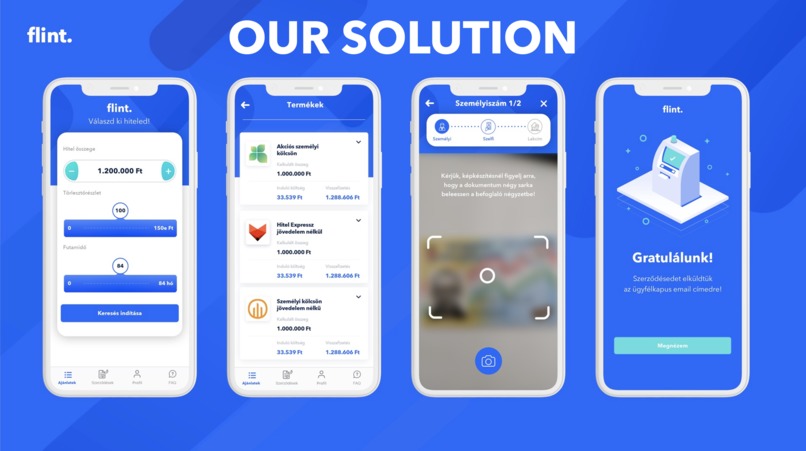

Our solution

-

How we tackle UX issues

-

Main building blocks of Flint

-

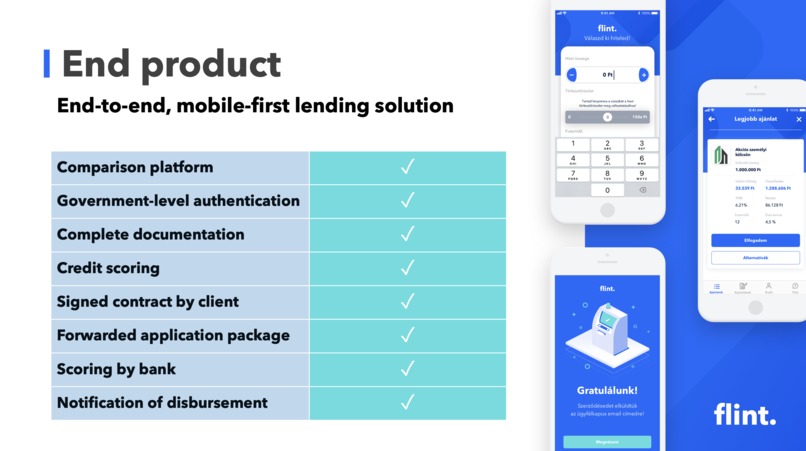

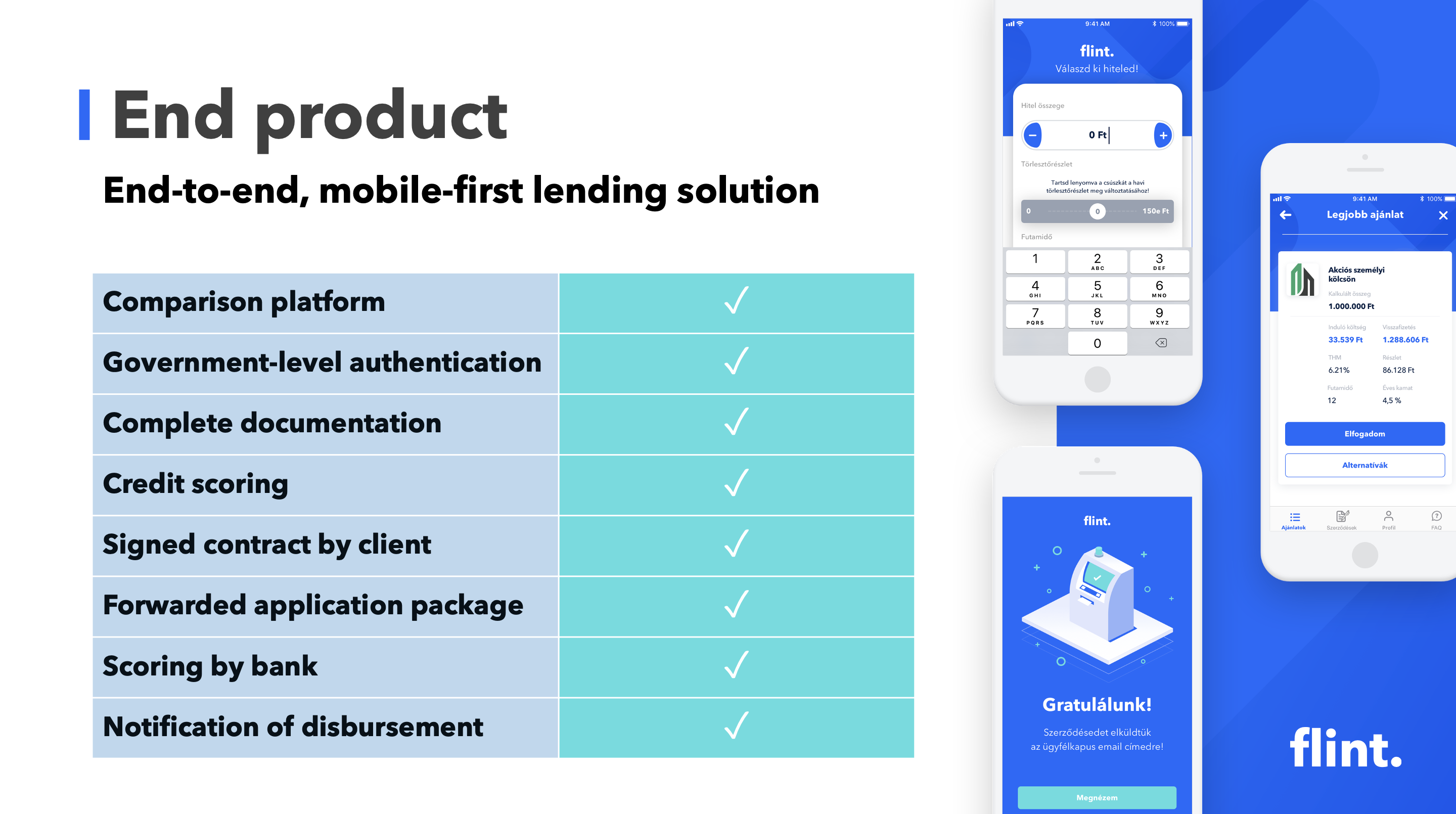

What the end product consists of

-

Complying with both regulation & UX

Inspiration

In order to help other fintechs and startups to overcome the financial difficulties caused by the crisis, we have started to prepare the functions of our solution called Flint for SME lending as well. Small and medium sized enterprises are facing a particularly hard situation nowadays and banks will play a critical role in the crisis as systemic stabilizers for customers, employees, and for their economies at large. They need to enhance their current digital offerings, identifying key functionalities that can be improved quickly. From a credit perspective, banks should identify most affected sectors & customers to see how they can be most supportive to their clients & communities.

Some are already considering availability of credit, thus creating positive effect on customer relationships and helping to maintain the operations of thousands of SMEs. According to McKinsey & Company, 74% of US workers said they are living from paycheck to paycheck, while 58% of workers are paid by the hour. For them, financial impact of quarantine measures and lack of employment—due to reduced sector activity, such as travel—will be particularly difficult. In the UK, digital bank Tide expects small business revenues to be down nearly 60% in April 2020. At least 21,000 more UK companies failed in March 2020 compared with the year before. Governments need to support workers and businesses directly, but they lack the tools to lend to SMEs. Banks are being inundated with requests for credit from SMEs and they need to make hundreds of urgent credit decisions.

Digital processes will be crucial throughout the pandemic: digital identity & verification are the only way to open new accounts and digital credit scoring is the only way to lend. We feel that we can help SMEs which are having liquidity issues, banks which are struggling to digitalise and governments which are not possessing the right tools to help their communities at the same time!

What it does

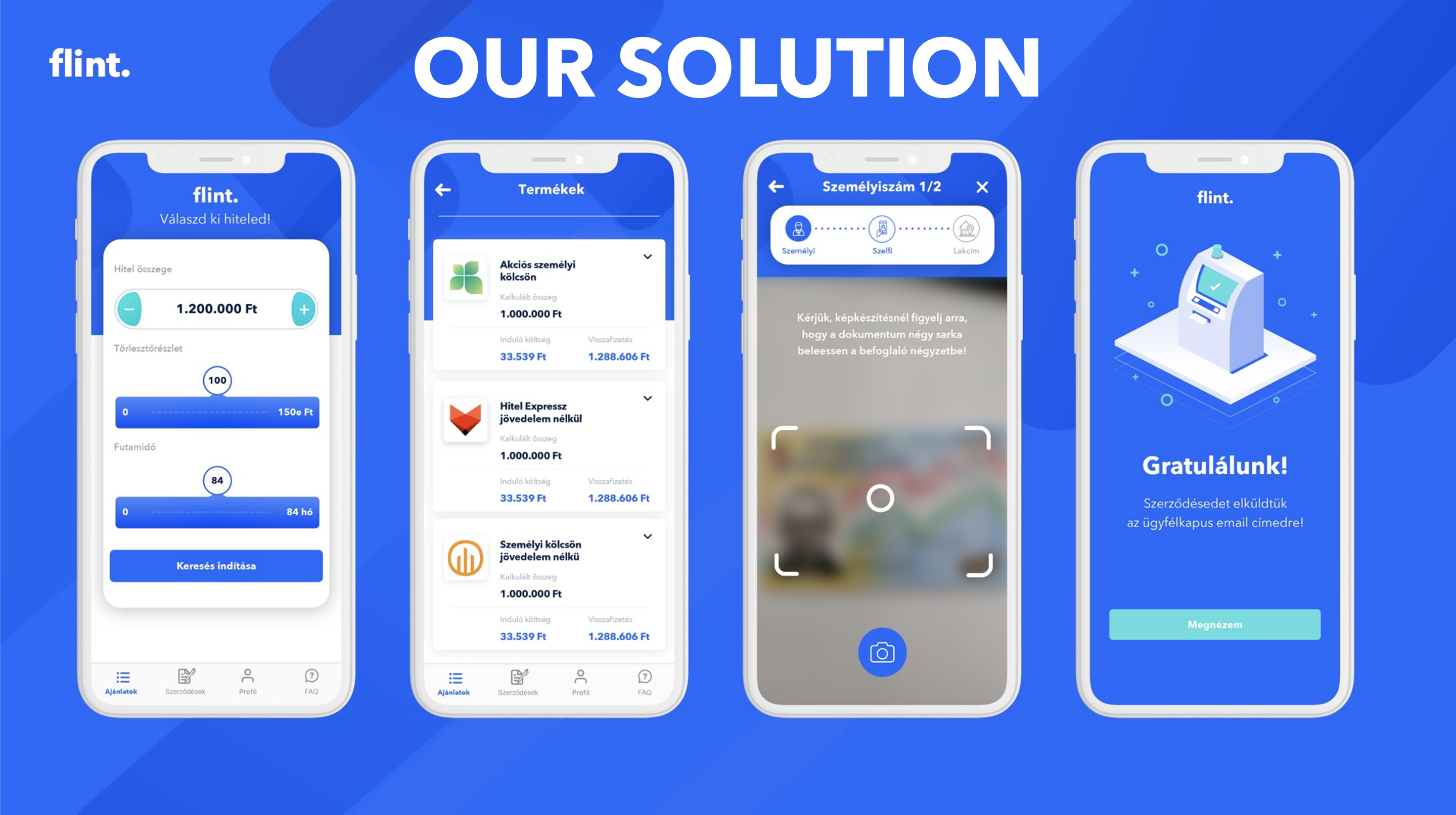

Our application, Flint basically allows customers of financial institutions to request financial products, credit cards, personal loans or open a bank account from the security of their homes via their mobile phones. In addition to these already existing functionalities, we also made the product suitable for small and medium-sized enterprises with liquidity problems to choose from several different credit products. Although unsecured retail and SME lending might differ, we believe that this development is the way to go.

The client representing a certain SME only needs to manually provide a fraction of all the necessary data, while also getting help, like useful tooltips which make the application process even smoother. Most of our credit scoring is automated due to the use of e.g. Bisnode's and governmental company information system, tax authority databases, the central credit information system and account information based on open banking.

As soon as the scoring is completed, we can see the details of a customized loan product and our contract can be generated immediately. This contract can be signed with a qualified e-signature following an SMS authentication and then the complete transaction documentation is forwarded to the back end of our banking partner and to the customer via email.

How we built it

Our initial solution - aimed at the retail segment - has been implemented as native iOS and Android applications. As we modified this product to satisfy the needs of SMEs as well, we started our digital product development processes from the very beginning, including UX research (customer journey mapping), UX design (wireframing), UI design (building the actual screens) and we’ve animated the screens to conduct usability tests as well as implemented them for Flint for SMEs iOS version.

Challenges we ran into

One of the biggest challenges was bridging the differences of retail and SME lending. Providing credit to SMEs is a complex process with way more required documents and data, which need to be uploaded through different systems and platforms. In order to be able to fill in their data automatically as well, we needed to transform many of the already existing functionalities.

Furthermore, we needed to come up with a solution that is truly omnichannel, since providing loans to companies needs to work on desktop as well along with the mobile-first approach, which also held difficulties. Our team had to optimize an already painful process for mobile and create a smoother and more seamless experience altogether.

Accomplishments that we're proud of

We are particularly proud of the fact that we managed to incorporate the whole SME lending process into a mobile solution, including an onboarding process, eKYC and e-signature solutions, and credit scoring. It is also outstanding that this way we can help banks significantly reduce the amount of time needed to validate the creditworthiness of applicants.

What we learned

Although SME financing is far more complex than providing credit for private individuals, there is an immense amount of data sources, which you can connect with and integrate in order to prefill as many information on applications as possible in order to truly speed up access to funding of one of the most endangered economic group, SMEs.

What's next for Flint for SMEs

We truly believe that Flint for SMEs is a solution that can have a hugely positive impact throughout the evolving financial crisis. We are willing to partner up with financial institutions and mediate their credit products through our application, so even more SMEs will have access to funding in these hard times.

Log in or sign up for Devpost to join the conversation.