-

-

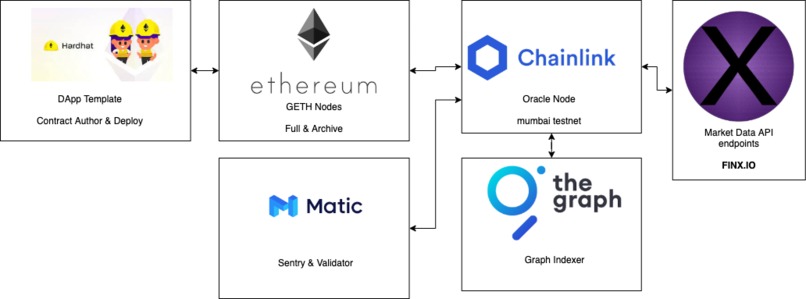

finx.io token-rates components

Token Rates: a ChainLink project to extend Credit Facilities to DeFi Collateralized Pools

Project Mission

Token Rates is a protocol for using traditional money market rates to inform credit borrowing rates on DeFi pools. Using a ChainLink Oracle, the protocol consumes current treasury rates and AAVE money market rates for the protocol interest algorithm as a risk-free benchmark upon which credit spreads can be constructed. The FinX DApp (https://app.finx.io) provides access to protocol contracts as the foundation for extending Credit Facilities to the DeFi Ecosystem.

What's Next for this Project

We intend to create Credit Pools that have interest rate algorithms linked to present credit markets so that credit can easily be extended to the tokenized economy. These enhanced interest rate algorithms and credit pools will be further developed and implemented in 2021 and 2022.

We are very excited about the rapid progress that can be made with Chainlink, The Graph, and other protocols and encourage developers to add to this promising technology.

About This Document

Token Rates is an integrated ecosystem of protocols currently used for using traditional money market rates and serve as bridge for determining interest rates on DeFi credit pools for Ethereum as well as Matic, Polkadot and Cardano networks. Using a Chainlink Oracle, the protocol provides both fiat-based and crypto-based reference lending and borrowing rates that inform the algorithmically determined credit rate charged by the credit pool.

For the Chainlink Hackathon 2021 project, this project contains the following functionality:

Chainlink Oracle node (Rinkeby testnet)

The Graph node indexing Oracle requests as subgraph

Contracts which are credit rate borrowing pools using oracle requests to determine the appropriate credit spread.

DApp using Hardhat that allows requests, queries, and interaction with Chainlink Oracle and The Graph subgraphs

About This Project

This project is a submission to the ChainLink Hackathon 2021 and currently runs on the Ethereum Rinkeby test network.

Fiat-based Capital Markets are built upon (theoretically) risk-free rates, against which all individual securities are priced relative to risk. A bond that pays a higher interest rate than another is assumed to be riskier, by virtue of the fact that the markets are built to be a price-discovery mechanism and to reward those who properly measure the risk of a particular security.

Tokenized decentralized capital pools that operate on collateralized pool algorithms to determine interest rates are a significant step forward in creating a new paradigm for assigning risk, but most of the capital deployed to these pools is currently unleveraged and therefore not risk-adjusted.

In order for the Tokenized Capital Markets to expand and fulfill the needs of our global economy, there must be a paradigm for measuring and pricing counterparty risk. Risk-free treasury rates are a starting requirement to relative-risk pricing and the Token Rates protocol introduces fiat-based rate engines so that credit spreads can be determined for tokenized capital.

Team Members

- Geoff Fite @GFite

- Dick Mule @dick-mule

- Jake Mathai @jakemathai5

Log in or sign up for Devpost to join the conversation.